|

市场调查报告书

商品编码

1773393

菌丝砖市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Mycelium Bricks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

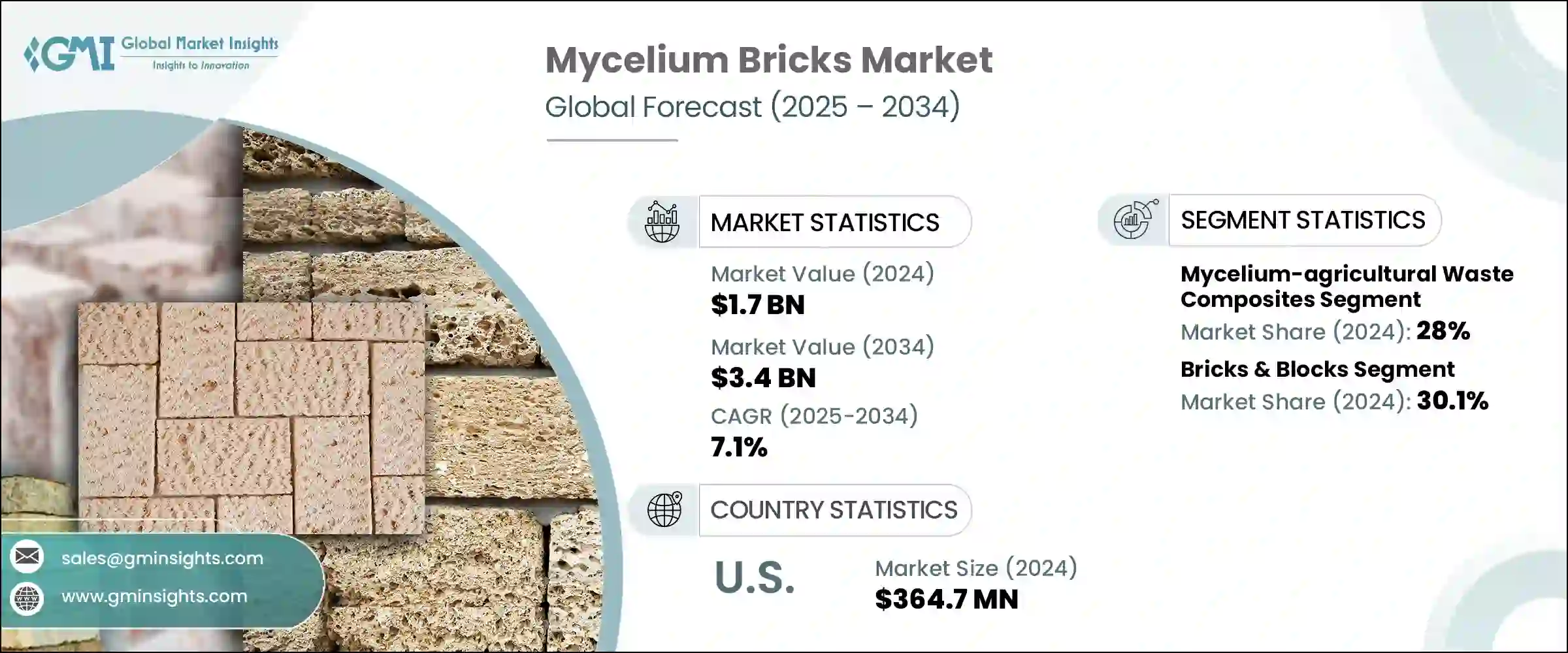

2024 年全球菌丝砖市场价值为 17 亿美元,预计到 2034 年将以 7.1% 的复合年增长率增长至 34 亿美元。这一增长反映出人们日益转向永续、低碳建筑材料。这些可生物降解的菌丝砖由在农业废弃物中生长的真菌菌丝体製成,具有出色的隔热性能,可减少环境污染,同时符合循环生物经济原则。研究表明,菌丝体复合材料具有负隐含碳(约 -39.5 公斤二氧化碳当量/立方米),生产能耗仅为 7.7 兆焦/公斤,远低于传统隔热材料的 83.5 兆焦/公斤。在此基础上,培养方法的进步显着提高了菌丝体材料的性能和价格承受能力,使製造商能够直接在建筑工地生产负碳隔热材料。

这项创新不仅降低了成本,还显着减少了运输排放,使其成为永续建筑实践的关键组成部分。透过实现碳负性隔热材料的现场生产,它消除了长途运输大件材料的需要,从而减少了与传统供应链相关的碳足迹。此外,製造和运输相关排放的减少有助于实现更绿色的建筑流程,这与日益增长的低影响、环保建筑趋势一致。在本地生产菌丝体产品的能力也能确保更快的周转时间和更大的供应链弹性,同时支援区域经济。这种精简的生产方式不仅提高了整体永续性,也增强了菌丝体作为传统建筑材料可行替代品的可扩展性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 17亿美元 |

| 预测值 | 34亿美元 |

| 复合年增长率 | 7.1% |

菌丝体-农业废弃物复合材料市场在2024年将占据28%的市场份额,由于其成本效益高,且在亚太发达国家小麦秸秆和玉米壳等原材料供应充足,该领域将继续蓬勃发展。菌丝体-农业废弃物复合材料能够无缝整合到模组化面板系统和隔热应用中,已成为环保建筑计画的基石。

2024年,菌丝砖市场中的砖块和砌块部分占据了30.1%的市场份额,其标准化尺寸和坚固的结构特性使其备受青睐。这些特性使其成为传统材料的直接替代品,使建筑商能够采用更环保的替代方案,而无需牺牲现有的施工流程。

美国菌丝砖市场规模预计2024年达到3.647亿美元,得益于强而有力的监管环境,包括绿建筑激励措施和LEED认证。专注于永续设计的建筑公司和创新中心日益增多,加上城市需求(尤其是来自具有环保意识的年轻一代)的不断增长,推动了可生物降解、美观的菌丝砖在全国范围内的使用稳步增长。

菌丝砖产业的知名企业包括 Biohm、MycoWorks、Ecovative Design、Grown Bio 和 Mogu Srl。这些公司正在透过建立研究合作伙伴关係来改进种植和生产工艺,投资研发以提高耐火性和结构性能,以及开发可扩展的生产系统,从而巩固其市场地位。此外,他们也正在争取认证(例如 LEED、BREEAM)以提高在绿建筑市场的信誉,透过板材、隔热材料和模组化解决方案来丰富产品线,并与建筑师和建筑商合作以提高其应用率。这些策略增强了市场信任度,并确保了长期成长。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)

(註:仅提供重点国家的贸易统计数据

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021-2034 年

- 主要趋势

- 纯菌丝砖

- 菌丝体-农业废弃物复合材料

- 秸秆基复合材料

- 玉米壳和玉米秸秆复合材料

- 稻壳与农作物残渣复合材料

- 其他的

- 菌丝体-木材废料复合材料

- 锯末和木屑复合材料

- 纸和纸板废料复合材料

- 其他的

- 菌丝体增强复合材料

- 纤维增强复合材料

- 矿物增强复合材料

- 其他的

- 专门设计的菌丝体产品

第六章:市场估计与预测:依形式,2021-2034 年

- 主要趋势

- 砖块和砌块

- 标准砖

- 联锁块

- 客製化形状的积木

- 面板和电路板

- 平板

- 隔音板

- 结构板

- 绝缘材料

- 鬆散填充绝缘材料

- 硬质隔热板

- 喷涂绝缘材料

- 3D列印和定製表格

- 其他的

第七章:市场估计与预测:按应用,2021-2034 年

- 主要趋势

- 建筑施工

- 室内非承重墙

- 绝缘

- 声学

- 结构部件

- 其他的

- 室内设计和家具

- 装饰元素

- 家具部件

- 其他的

- 临时建筑和展览

- 展览展示

- 临时设施

- 事件结构

- 包装和保护材料

- 艺术与设计应用

- 其他的

第八章:市场估计与预测:依最终用途,2021-2034 年

- 主要趋势

- 住宅建筑

- 商业建筑

- 办公大楼

- 零售和酒店

- 其他的

- 机构及公共建筑

- 教育设施

- 文化和社区建筑

- 医疗保健设施

- 其他的

- 工业和製造业

- 其他的

第九章:市场估计与预测:按地区,2021-2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Biohm

- Biomyc

- Ecovative Design

- Grown Bio

- Mogu Srl

- Mycel

- Mycovation

- MycoWorks

The Global Mycelium Bricks Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 7.1% to reach USD 3.4 billion by 2034. This growth reflects a growing shift toward sustainable, low-carbon construction materials. Made from fungal mycelium grown on agricultural waste, these biodegradable bricks deliver outstanding insulation and reduce environmental pollution while aligning with circular bioeconomy principles. Studies show mycelium composites have negative embodied carbon (approximately -39.5 kg CO2e/m3) and consume only 7.7 MJ/kg in production, far less than conventional insulation materials at 83.5 MJ/kg. Building on this momentum, advancements in cultivation methods are significantly enhancing the performance and affordability of mycelium-based materials, allowing manufacturers to produce carbon-negative insulation directly at construction sites.

This innovation not only reduces costs but also significantly lowers transportation emissions, making it a key component of sustainable construction practices. By enabling on-site production of carbon-negative insulation, it eliminates the need for long-distance transportation of bulky materials, thereby decreasing the carbon footprint associated with traditional supply chains. Furthermore, the reduction in manufacturing and transportation-related emissions contributes to greener building processes, aligning with the growing push toward low-impact, eco-friendly construction. The ability to produce mycelium-based products locally also ensures faster turnaround times and greater supply chain flexibility, while simultaneously supporting regional economies. This streamlined production approach not only improves overall sustainability but also enhances the scalability of mycelium as a viable alternative to conventional building materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $3.4 Billion |

| CAGR | 7.1% |

The mycelium-agricultural waste composites segment, holding a 28% share in 2024, continues to thrive due to its cost efficiency and the ready availability of raw materials like wheat straw and corn husks in developed Asia-Pacific countries. Their seamless integration into modular panel systems and insulation applications has made them a cornerstone of eco-friendly construction projects.

The bricks and blocks segment from the mycelium bricks market accounted for a 30.1% share in 2024, favored for their standardized dimensions and robust structural qualities. These attributes make them a straightforward substitute for traditional materials, allowing builders to adopt greener alternatives without compromising established construction workflows.

U.S. Mycelium Bricks Market, valued at USD 364.7 million in 2024, benefits from a strong regulatory environment, including green building incentives and LEED certifications. The growing presence of architecture firms and innovation centers focused on sustainable design, coupled with increasing urban demand-especially from environmentally conscious younger generations-is fueling steady growth in the use of biodegradable, aesthetically pleasing mycelium bricks across the country.

Prominent players include Biohm, MycoWorks, Ecovative Design, Grown Bio, and Mogu S.r.l. Companies in the mycelium bricks industry are strengthening their position by forming research partnerships to refine cultivation and production processes, investing in R&D to improve fire resistance and structural performance, and developing scalable manufacturing systems. They're also securing certifications (e.g., LEED, BREEAM) to enhance credibility in green construction markets, diversifying product lines with panel, insulation, and modular solutions, and pursuing collaborations with architects and builders to increase adoption. These strategies enhance market trust and ensure long-term growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Product type

- 2.2.2 Form method

- 2.2.3 Application

- 2.2.4 End use

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021–2034 (USD Billion) (Cubic Meters)

- 5.1 Key trends

- 5.2 Pure mycelium bricks

- 5.3 Mycelium-agricultural waste composites

- 5.3.1 Straw-based composites

- 5.3.2 Corn husk & stalk composites

- 5.3.3 Rice hulls & crop residue composites

- 5.3.4 Others

- 5.4 Mycelium-wood waste composites

- 5.4.1 Sawdust & wood chip composites

- 5.4.2 Paper & cardboard waste composites

- 5.4.3 Others

- 5.5 Mycelium-reinforced composites

- 5.5.1 Fiber-reinforced composites

- 5.5.2 Mineral-reinforced composites

- 5.5.3 Others

- 5.6 Specialized & engineered mycelium products

Chapter 6 Market Estimates and Forecast, By Form, 2021–2034 (USD Billion) (Cubic Meters)

- 6.1 Key trends

- 6.2 Bricks & blocks

- 6.2.1 Standard bricks

- 6.2.2 Interlocking blocks

- 6.2.3 Custom-shaped blocks

- 6.3 Panels & boards

- 6.3.1 Flat panels

- 6.3.2 Acoustic panels

- 6.3.3 Structural panels

- 6.4 Insulation materials

- 6.4.1 Loose fill insulation

- 6.4.2 Rigid insulation boards

- 6.4.3 Spray-applied insulation

- 6.5 3D-printed & custom forms

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021–2034 (USD Billion) (Cubic Meters)

- 7.1 Key trends

- 7.2 Building construction

- 7.2.1 Interior non-load bearing walls

- 7.2.2 Insulation

- 7.2.3 Acoustic

- 7.2.4 Structural components

- 7.2.5 Others

- 7.3 Interior design & furniture

- 7.3.1 Decorative elements

- 7.3.2 Furniture components

- 7.3.3 Others

- 7.4 Temporary structures & exhibitions

- 7.4.1 Exhibition displays

- 7.4.2 Temporary installations

- 7.4.3 Event structures

- 7.5 Packaging & protective materials

- 7.6 Art & design applications

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By End Use, 2021–2034 (USD Billion) (Cubic Meters)

- 8.1 Key trends

- 8.2 Residential construction

- 8.3 Commercial construction

- 8.3.1 Office buildings

- 8.3.2 Retail & hospitality

- 8.3.3 Others

- 8.4 Institutional & public buildings

- 8.4.1 Educational facilities

- 8.4.2 Cultural & community buildings

- 8.4.3 Healthcare facilities

- 8.4.4 Others

- 8.5 Industrial & manufacturing

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021–2034 (USD Billion) (Cubic Meters)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Biohm

- 10.2 Biomyc

- 10.3 Ecovative Design

- 10.4 Grown Bio

- 10.5 Mogu S.r.l.

- 10.6 Mycel

- 10.7 Mycovation

- 10.8 MycoWorks