|

市场调查报告书

商品编码

1773400

先进汽车照明市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Advanced Vehicle Lighting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

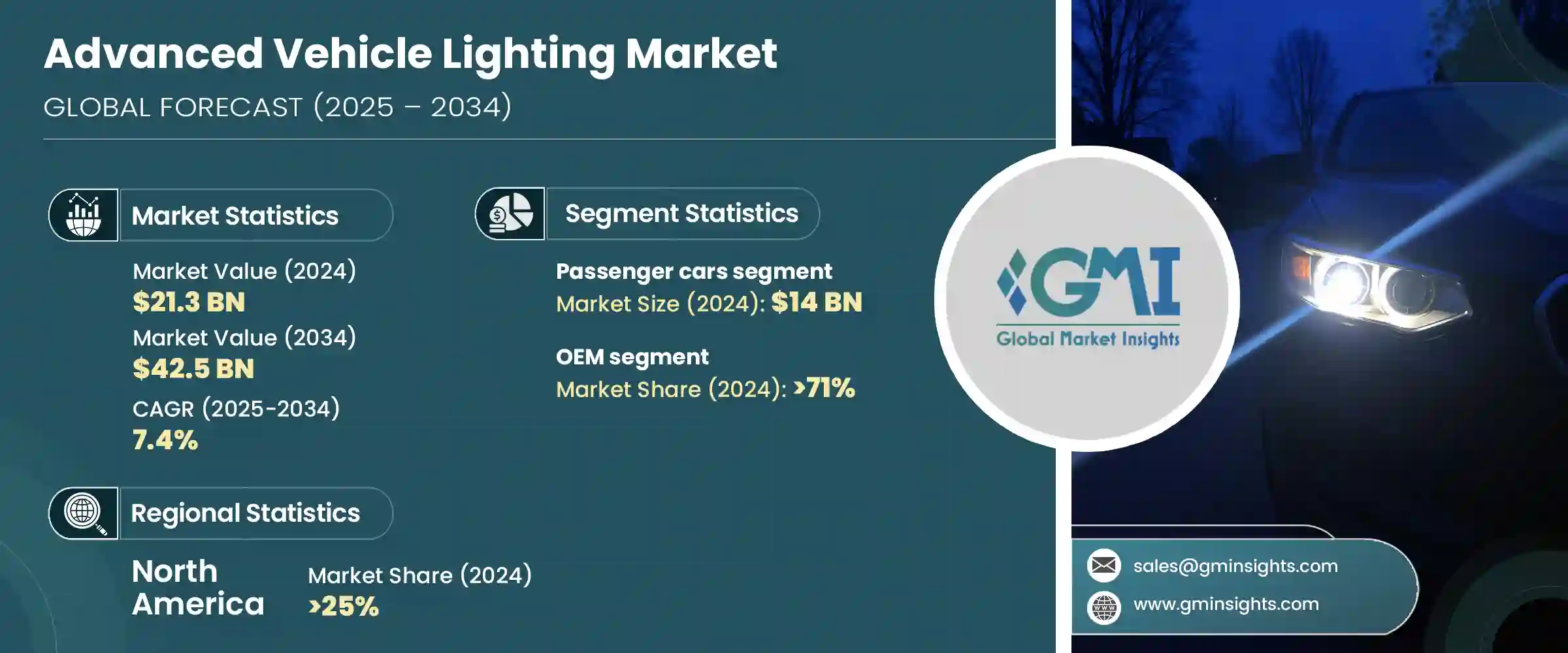

2024年,全球先进汽车照明市场规模达213亿美元,预计2034年将以7.4%的复合年增长率成长,达到425亿美元。这一成长主要得益于先进驾驶辅助系统(ADAS) 和自动驾驶技术的日益融合,这些技术正在彻底改变现代汽车的照明需求。矩阵LED和雷射头灯等智慧照明解决方案的需求日益增长,因为它们可以即时调整光束模式,以支援感测器功能并减少眩光。

汽车製造商正在大力投资动态照明系统,该系统能够与行人和其他车辆进行通信,尤其是在能见度有限的条件下。随着汽车产业竞争的加剧,製造商们正在利用复杂的照明设计来创造独特的品牌标誌。动态方向灯、3D尾灯和车内氛围灯等功能如今已成为必备的造型元素,尤其是在电动车和豪华车领域。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 213亿美元 |

| 预测值 | 425亿美元 |

| 复合年增长率 | 7.4% |

灵活的 LED 和 OLED 技术使汽车製造商能够打造高度可自订的动态照明效果,从而显着提升车辆的辨识度和视觉吸引力。这些自适应照明解决方案可以客製化形状并整合到车辆的各个部件,让设计师能够自由地开发独特的标誌性设计,使每款车型在竞争激烈的市场中脱颖而出。动态动画程式功能(例如顺序方向灯、迎宾灯光秀或营造氛围的车内照明)更增添了精緻感,能够与追求未来感和个人化功能的消费者产生强烈共鸣。

2024年,乘用车市场规模达140亿美元。全球范围内的监管规定,例如日间行车灯 (DRL) 和自适应远光灯 (ADB) 系统的采用,正迫使原始设备製造商 (OEM) 整合先进的照明技术。这些功能不仅提高了日间和夜间的可视性,还能确保符合国际安全标准。随着各国政府实施更严格的照明法规,主流乘用车越来越多地配备此类系统,推动了对先进汽车照明的需求。此外,消费者对高端沉浸式内装的兴趣促使汽车製造商安装多色LED灯带、同步情绪照明和可自订的灯光主题,以打造精緻的车内体验。

2024年,原始设备OEM)占据了71%的市场。先进的照明系统已成为定义车辆设计和强化製造商品牌形象的关键。标誌性的LED日行灯、动态迎宾灯和可配置的尾灯设计,有助于提升车辆的辨识度,同时支援以创新和奢华为重点的行销活动。为了在竞争激烈的市场中脱颖而出,OEM厂商投入大量资源进行照明研发,旨在打造引人注目、独特的设计,吸引消费者,并使其产品脱颖而出。

2024年,北美先进汽车照明市场占据25%的市场。美国国家公路交通安全管理局(NHTSA)正逐步支持允许使用自适应远光灯(ADB)和其他智慧照明技术的法规。这些政策转变鼓励汽车製造商采用先进的照明系统,以提高道路安全性、减少眩光并符合不断发展的联邦安全标准,为高品质照明解决方案创造了更大的市场机会。此外,在政府激励措施和消费者浓厚兴趣的推动下,美国电动车(EV)和自动驾驶汽车的快速成长,刺激了对LED矩阵、整合式雷射雷达的头灯和以通讯为中心的照明功能等先进照明技术的需求,这些技术对于下一代汽车的安全性和性能至关重要。

全球先进汽车照明市场的领导者包括欧司朗 (OSRAM)、ZKW、小纟 (Koito)、Lumileds、Forvia、史丹利 (STANLEY) 和法雷奥 (Valeo)。这些公司占据了全球相当一部分市场份额,透过创新和策略定位展开激烈竞争。为了巩固市场地位,先进汽车照明领域的公司正专注于照明技术的持续创新,例如开发符合自动驾驶和电动车趋势的自适应、智慧和连网照明系统。他们正大力投资研发,以推出功能增强、能源效率更高、设计独特的新产品。与汽车原始设备製造商 (OEM) 建立策略合作伙伴关係和合作关係,使这些公司能够将其照明解决方案无缝整合到汽车平台中,从而确保早期采用和签订长期合约。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 车辆中自适应照明的采用日益增多

- 汽车电气化和电动车生产率不断提高

- 更重视道路和乘客安全

- 政府强制推行高效照明系统

- 产业陷阱与挑战

- 先进照明元件成本高

- 与车辆电子设备的系统整合的复杂性

- 市场机会

- 自动驾驶智慧照明的开发

- 电动车和豪华车领域的成长

- 新兴汽车製造市场的扩张

- 照明与车辆通讯系统的集成

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品

- 生产统计

- 生产中心

- 消费中心

- 汇出和汇入

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 卤素

- 氙气/HID

- 引领

- 雷射

- OLED

- 矩阵LED

第六章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 头灯

- 后部照明

- 室内照明

- 侧面和角落照明

- 雾灯和辅助灯

- 通讯照明

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 商用车

- 轻型

- 中型

- 重负

第八章:市场估计与预测:依销售管道,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第九章:市场估计与预测:按推进方式,2021 - 2034 年

- 主要趋势

- 冰

- 纯电动车

- 油电混合车

- 插电式混合动力

- 燃料电池电动车

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 东南亚

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- Koito Manufacturing Co., Ltd.

- Valeo SA

- Hella GmbH & Co. KGaA (FORVIA Group)

- Marelli Automotive Lighting

- Stanley Electric Co., Ltd.

- ZKW Group GmbH

- OSRAM Continental GmbH

- Hyundai Mobis Co., Ltd.

- Lumileds Holding BV

- Nichia Corporation

- Bosch Mobility Solutions

- TYC Brother Industrial Co., Ltd.

- Texas Instruments

- Denso Corporation

- GE Lighting (Savant Systems Inc.)

- Varroc Engineering Ltd.

- Bosla Lighting

- SL Corporation

- Ichikoh Industries, Ltd.

- JW Speaker Corporation

The Global Advanced Vehicle Lighting Market was valued at USD 21.3 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 42.5 billion by 2034. This growth is driven largely by the rising integration of advanced driver assistance systems (ADAS) and autonomous driving technologies, which are transforming the lighting requirements of modern vehicles. Intelligent lighting solutions, such as matrix LED and laser headlamps, are increasingly in demand because they can adjust beam patterns in real-time to support sensor functions and reduce glare.

Automakers are heavily investing in dynamic lighting systems that can communicate with pedestrians and other vehicles, especially in conditions with limited visibility. As competition intensifies in the automotive sector, manufacturers are leveraging complex lighting designs as a distinctive brand signature. Features like dynamic turn signals, 3D taillights, and interior ambient lighting are now essential styling elements, particularly in electric and luxury vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Billion |

| Forecast Value | $42.5 Billion |

| CAGR | 7.4% |

Flexible LED and OLED technologies allow automakers to create highly customizable and animated lighting effects that significantly boost a vehicle's identity and visual appeal. These adaptable lighting solutions can be shaped and integrated into various parts of the vehicle, offering designers the freedom to develop unique signatures that set each model apart in a competitive market. The ability to program dynamic animations-such as sequential turn signals, welcoming light shows, or mood-enhancing interior lighting-adds a layer of sophistication that resonates strongly with consumers seeking futuristic and personalized features.

In 2024, the passenger cars segment held USD 14 billion. Regulatory mandates worldwide, such as the adoption of daytime running lights (DRLs) and adaptive driving beam (ADB) systems, are compelling original equipment manufacturers (OEMs) to integrate advanced lighting technologies. These features not only improve visibility during both day and night but also ensure compliance with international safety standards. As governments enforce stricter lighting regulations, mainstream passenger cars are increasingly outfitted with such systems, pushing demand for advanced vehicle lighting higher. Furthermore, consumer interest in premium, immersive interiors is driving automakers to install multi-color LED strips, synchronized mood lighting, and customizable light themes to create a sophisticated in-car experience.

The OEM segment held a 71% share in 2024. Advanced lighting systems have become crucial in defining vehicle design and reinforcing brand identity for manufacturers. Signature LED DRLs, animated welcome lights, and configurable taillight designs contribute to making vehicles instantly recognizable while supporting marketing campaigns focused on innovation and luxury. To stand out in a crowded marketplace, OEMs are dedicating significant resources to lighting research and development, aiming to create striking, distinctive designs that attract consumers and differentiate their offerings.

North America Advanced Vehicle Lighting Market held a 25% share in 2024. The U.S. National Highway Traffic Safety Administration (NHTSA) is increasingly supporting regulations that permit adaptive driving beam (ADB) headlights and other intelligent lighting technologies. These policy shifts encourage automakers to adopt advanced lighting systems that enhance on-road safety, reduce glare, and comply with evolving federal safety standards, generating greater market opportunities for high-quality lighting solutions. Additionally, the rapid growth of electric vehicles (EVs) and autonomous cars in the U.S., spurred by government incentives and strong consumer interest, fuels demand for sophisticated lighting technologies such as LED matrices, LiDAR-integrated headlamps, and communication-focused lighting features that are critical for next-generation vehicle safety and performance.

Leading players in the Global Advanced Vehicle Lighting Market include OSRAM, ZKW, Koito, Lumileds, Forvia, STANLEY, and Valeo. Together, these companies hold a significant portion of the global market share, competing vigorously through innovation and strategic positioning. To solidify their presence and strengthen market positions, companies in the advanced vehicle lighting space are focusing on continuous innovation in lighting technologies, such as the development of adaptive, smart, and connected lighting systems that align with autonomous and electric vehicle trends. They are investing heavily in research and development to introduce new products that offer enhanced functionality, energy efficiency, and distinctive design features. Strategic partnerships and collaborations with automotive OEMs allow these companies to integrate their lighting solutions seamlessly into vehicle platforms, ensuring early adoption and long-term contracts.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Sales Channel

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of adaptive lighting in vehicles

- 3.2.1.2 Rising vehicle electrification and EV production rates

- 3.2.1.3 Increasing emphasis on road and passenger safety

- 3.2.1.4 Government mandates for efficient lighting systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced lighting components

- 3.2.2.2 Complexity in system integration with vehicle electronics

- 3.2.3 Market opportunities

- 3.2.3.1 Development of smart lighting for autonomous driving

- 3.2.3.2 Growth in EV and luxury vehicle segments

- 3.2.3.3 Expansion in emerging automotive manufacturing markets

- 3.2.3.4 Integration of lighting with vehicle communication systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn & Units)

- 5.1 Key trends

- 5.2 Halogen

- 5.3 Xenon/HID

- 5.4 LED

- 5.5 Laser

- 5.6 OLED

- 5.7 Matrix LED

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn & Units)

- 6.1 Key trends

- 6.2 Front Lighting

- 6.3 Rear Lighting

- 6.4 Interior Lighting

- 6.5 Side & Corner Lighting

- 6.6 Fog and Auxiliary Lights

- 6.7 Communication Lighting

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn & Units)

- 7.1 Key trends

- 7.2 Passenger Car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial Vehicle

- 7.3.1 Light-duty

- 7.3.2 Medium-duty

- 7.3.3 Heavy-duty

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn & Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn & Units)

- 9.1 Key trends

- 9.2 ICE

- 9.3 BEV

- 9.4 HEV

- 9.5 PHEV

- 9.6 FCEV

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Koito Manufacturing Co., Ltd.

- 11.2 Valeo S.A.

- 11.3 Hella GmbH & Co. KGaA (FORVIA Group)

- 11.4 Marelli Automotive Lighting

- 11.5 Stanley Electric Co., Ltd.

- 11.6 ZKW Group GmbH

- 11.7 OSRAM Continental GmbH

- 11.8 Hyundai Mobis Co., Ltd.

- 11.9 Lumileds Holding B.V.

- 11.10 Nichia Corporation

- 11.11 Bosch Mobility Solutions

- 11.12 TYC Brother Industrial Co., Ltd.

- 11.13 Texas Instruments

- 11.14 Denso Corporation

- 11.15 GE Lighting (Savant Systems Inc.)

- 11.16 Varroc Engineering Ltd.

- 11.17 Bosla Lighting

- 11.18 SL Corporation

- 11.19 Ichikoh Industries, Ltd.

- 11.20 J.W. Speaker Corporation

汽车卤素灯泡市场:依产品类型、应用、车辆类型和通路划分,全球预测,2026-2032年

汽车卤素灯泡市场:依产品类型、应用、车辆类型和通路划分,全球预测,2026-2032年 汽车照明市场机会、成长要素、产业趋势分析及2026年至2035年预测

汽车照明市场机会、成长要素、产业趋势分析及2026年至2035年预测 汽车照明:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

汽车照明:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026年全球小型发光二极体(LED)汽车丛集市场报告2026年全球汽车卤素灯泡市场报告2026年全球汽车发光二极体(LED)灯泡市场报告2026年全球汽车外观发光二极体(LED)动画市场报告2026年全球汽车照明市场报告2026年全球自行车反光片市场报告

2026年全球小型发光二极体(LED)汽车丛集市场报告2026年全球汽车卤素灯泡市场报告2026年全球汽车发光二极体(LED)灯泡市场报告2026年全球汽车外观发光二极体(LED)动画市场报告2026年全球汽车照明市场报告2026年全球自行车反光片市场报告 汽车外饰智慧照明市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、技术类型、产品类型、地区及竞争格局划分,2021-2031年)

汽车外饰智慧照明市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、技术类型、产品类型、地区及竞争格局划分,2021-2031年)