|

市场调查报告书

商品编码

1773426

肩射武器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Shoulder Fired Weapons Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

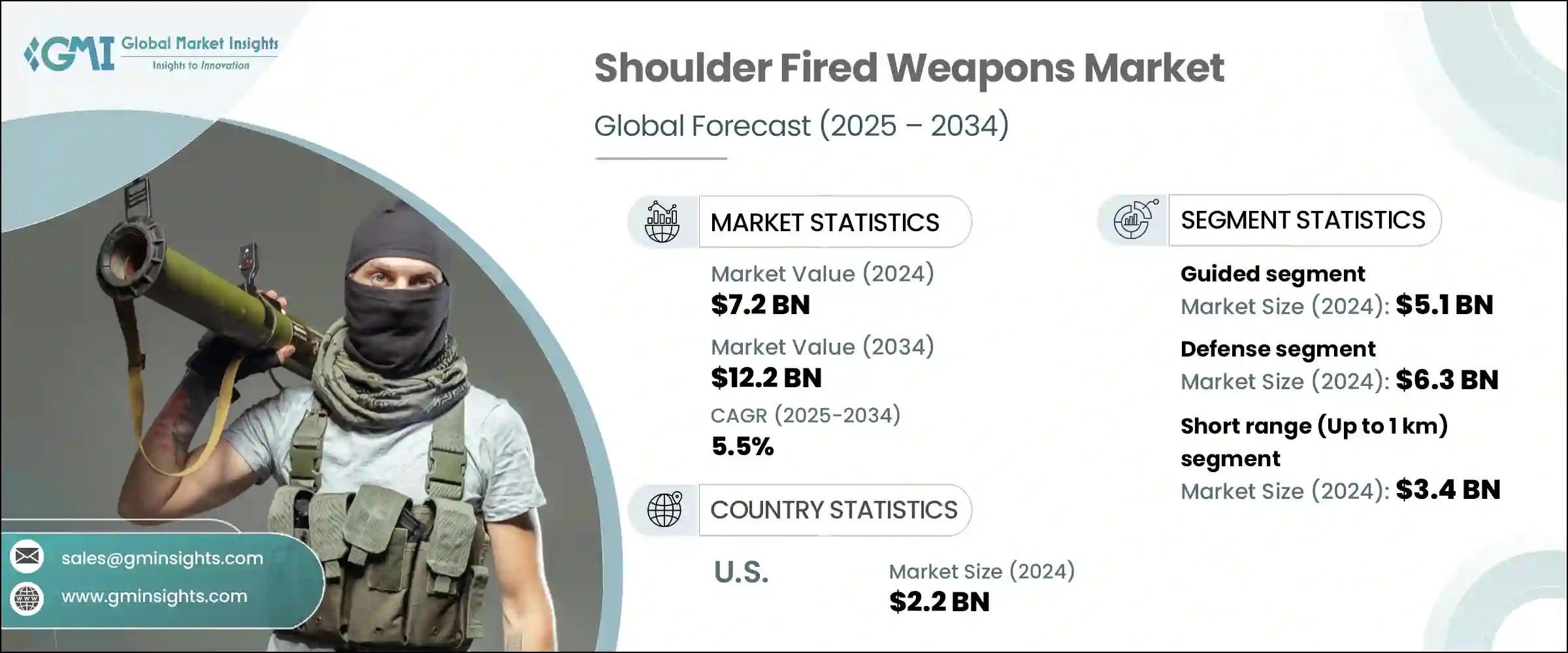

2024 年全球肩扛式武器市场规模为 72 亿美元,预计到 2034 年将以 5.5% 的复合年增长率成长,达到 122 亿美元。这一增长主要得益于全球范围内不断加强的军事现代化计划。日益加剧的地缘政治紧张局势和持续的边界争端极大地刺激了对肩扛式武器的需求,因为武装部队正在寻求价格合理、可部署的兵力倍增器。各地区的衝突和对峙加剧了对便携式、精确反装甲和防空系统的需求。此外,军事现代化工作的重点是开发下一代轻型武器,以提高其在城市和非对称战争中的机动性和作战效能。这些计画优先考虑改进瞄准能力和减轻发射重量等升级,这推动了对先进肩扛式飞弹的需求。

全球战略防御计画正投入大量资源用于便携式武器系统的研发,以加速创新并扩展其能力。这些投入的重点是研发更先进、更轻、更广泛用途的肩扛式武器,以满足现代作战场景的需求。更高的精准度、更先进的瞄准技术和更高的便携性是推动这些努力的关键优先事项。随着各国军队寻求使用能够适应多样化作战环境的尖端系统来升级其武器库,研发资金持续增加,这不仅推动了市场扩张,也促进了为士兵效能和战场敏捷性树立新标准的突破性进展。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 72亿美元 |

| 预测值 | 122亿美元 |

| 复合年增长率 | 5.5% |

导引武器领域在2024年引领市场,价值51亿美元。导引肩扛式武器融入先进指挥控制系统等综合防御网络,提升了其战略重要性。这些武器具备精准度、灵活性和即时目标调整能力,使其成为现代战场上不可或缺的武器。这种整合提升了作战效能,刺激了对先进导引系统的需求,进而推动市场成长。

2024年,国防领域产值达63亿美元。为了提升士兵的敏捷性和战斗力,对轻型、易部署武器的需求日益增长,肩扛式武器也因此成为当务之急。这些系统在反装甲和防空任务中发挥越来越重要的作用,并且是旨在以多功能、精准的解决方案取代过时武器的国防现代化项目的核心。它们在常规战争和非常规战争中的适应性确保了其在各军种中占据稳固的地位。

2024年,美国肩扛式武器市场规模达22亿美元。该市场的成长主要得益于国防部持续采购先进便携式系统。旨在提升士兵杀伤力、机动性和城市作战能力的项目,正在推动肩扛式反装甲和反结构武器的持续升级。对城市战备和部署的高度重视进一步支持了市场需求。

肩扛式武器市场的主要参与者包括洛克希德·马丁公司、RTX、萨博公司和欧洲飞弹集团(MBDA)。肩扛式武器市场的公司正在采取多种策略来巩固其市场地位。他们在研发方面投入巨资,以创新更轻、更精确、功能更强大的武器,以满足不断变化的战场需求。

与军事机构建立战略伙伴关係和协作,有助于他们获得关键合同,并根据特定的国防需求量身定制产品。这些公司也专注于透过有针对性的行销和区域办事处扩大其全球影响力,增强客户支援和售后服务。此外,许多参与者优先整合精确导引和互联互通等尖端技术,以提高作战效能,将自己定位为现代战争解决方案的领导者。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响

- 关键零件价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 产业衝击力

- 成长动力

- 地缘政治紧张局势与边界衝突加剧

- 增加军事现代化计划

- 对便携式和轻型武器的需求不断增长

- 不对称战争和城市战争场景激增

- 导引和瞄准系统的技术进步

- 产业陷阱与挑战

- 先进系统的生命週期及维护成本高

- 严格的出口管制和监管壁垒

- 市场机会

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 先进瞄准系统的集成

- 增强便携性和轻质材料

- 改进的弹头和推进能力

- 新兴技术

- 人工智慧火控系统

- 网路中心战一体化

- 定向能和电磁发射系统

- 当前的技术趋势

- 新兴商业模式

- 合规性要求

- 国防预算分析

- 全球国防开支趋势

- 区域国防预算分配

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 重点国防现代化项目

- 预算预测(2025-2034)

- 对产业成长的影响

- 各国国防预算

- 国防预算按部门分配

- 人员

- 营运和维护

- 采购

- 研究、开发、测试和评估

- 基础设施和建筑

- 科技与创新

- 永续发展倡议

- 供应链弹性

- 地缘政治分析

- 劳动力分析

- 数位转型

- 合併、收购和策略伙伴关係格局

- 风险评估与管理

- 主要合约授予(2021-2024)

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 市场集中度分析

- 按地区

- 关键参与者的竞争基准

- 财务绩效比较

- 收入

- 利润率

- 研发

- 产品组合比较

- 产品范围广度

- 科技

- 创新

- 地理位置比较

- 全球足迹分析

- 服务网路覆盖

- 各区域市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 利基市场参与者

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年关键发展

- 併购

- 伙伴关係和合作

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型倡议

- 新兴/新创企业竞争对手格局

第五章:市场估计与预测:按技术,2021 年至 2034 年

- 主要趋势

- 引导式

- 无引导

第六章:市场估计与预测:按范围,2021 年至 2034 年

- 主要趋势

- 短距离(最远 1 公里)

- 中距离(1-2.5公里)

- 远距离(2.5公里以上)

第七章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 防御

- 防空

- 反坦克

- 其他的

- 国土安全部

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- Daycraft Systems

- Dynamit Nobel Defence GmbH

- Lockheed Martin Corporation

- MBDA

- Nammo AS

- RAFAEL Advanced Defense Systems Ltd.

- Rheinmetall AG

- RTX

- Saab AB

The Global Shoulder Fired Weapons Market was valued at USD 7.2 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 12.2 billion by 2034. This growth is primarily driven by intensified military modernization programs worldwide. Rising geopolitical tensions and ongoing border disputes are significantly fueling demand for shoulder-fired weapons, as armed forces seek affordable, deployable force multipliers. Conflicts and standoffs in various regions have heightened the need for portable, precise anti-armor and anti-air systems. Additionally, military modernization efforts focus on developing next-generation lightweight weapons that enhance mobility and effectiveness in urban and asymmetric warfare scenarios. These programs prioritize upgrades like improved targeting and reduced launch weight, which propel demand for advanced shoulder-fired missiles.

Strategic defense initiatives worldwide are channeling significant resources into the research and development of man-portable weapon systems, accelerating innovation, and expanding capabilities. This investment focuses on creating more advanced, lightweight, and versatile shoulder-fired weapons that meet the demands of modern combat scenarios. Enhanced precision, improved targeting technologies, and greater portability are key priorities driving these efforts. As militaries seek to upgrade their arsenals with cutting-edge systems capable of adapting to diverse operational environments, funding for R&D continues to rise, fueling market expansion and fostering breakthroughs that set new standards in soldier effectiveness and battlefield agility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.2 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 5.5% |

The guided weapons segment led the market in 2024, valued at USD 5.1 billion. The integration of guided shoulder-fired weapons into comprehensive defense networks, such as advanced command and control systems, has elevated their strategic importance. These weapons deliver precision, flexibility, and real-time target adjustment capabilities, making them indispensable on modern battlefields. This integration enhances operational effectiveness and stimulates demand for sophisticated guided systems, driving market growth.

The defense segment generated USD 6.3 billion in 2024. The increasing need for lightweight, easily deployable weaponry to enhance soldier agility and combat effectiveness is pushing shoulder-fired weapons to the forefront. These systems are increasingly vital in anti-armor and anti-air roles and are central to defense modernization programs aiming to replace outdated weaponry with versatile, accurate solutions. Their adaptability across conventional and irregular warfare ensures a solid position within various military branches.

United States Shoulder Fired Weapons Market was valued at USD 2.2 billion in 2024. Growth here is fueled largely by ongoing procurements of advanced portable systems by the Department of Defense. Programs focused on enhancing soldier lethality, mobility, and capabilities in urban combat are driving continuous upgrades in shoulder-fired anti-armor and anti-structure weaponry. Heightened attention to urban warfare readiness and deployment further sustains demand.

Key players in the Shoulder Fired Weapons Market include Lockheed Martin Corporation, RTX, Saab AB, and MBDA. Companies in the shoulder-fired weapons market are adopting multiple strategies to solidify their market presence. They invest heavily in research and development to innovate lighter, more accurate, and multifunctional weapons that meet evolving battlefield needs.

Strategic partnerships and collaborations with military agencies help them secure key contracts and tailor products to specific defense requirements. Firms also focus on expanding their global footprint through targeted marketing and regional offices, enhancing customer support and after-sales services. Moreover, many players prioritize integrating cutting-edge technologies such as precision guidance and connectivity features to improve operational effectiveness, positioning themselves as leaders in modern warfare solutions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Technology

- 2.2.2 Range

- 2.2.3 Application

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Trump Administration Tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising geopolitical tensions and border conflicts

- 3.3.1.2 Increased military modernization programs

- 3.3.1.3 Growing demand for portable and lightweight weaponry

- 3.3.1.4 Surge in asymmetric and urban warfare scenarios

- 3.3.1.5 Technological advancements in guidance and targeting systems

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High lifecycle and maintenance costs of advanced systems

- 3.3.2.2 Stringent export controls and regulatory barriers

- 3.3.3 Market opportunities

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 Latin America

- 3.5.5 Middle East & Africa

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and innovation landscape

- 3.8.1 Current technological trends

- 3.8.1.1 Integration of advanced targeting systems

- 3.8.1.2 Enhanced portability and lightweight materials

- 3.8.1.3 Improved warhead and propulsion capabilities

- 3.8.2 Emerging technologies

- 3.8.2.1 AI-enabled fire control systems

- 3.8.2.2 Network-centric warfare integration

- 3.8.2.3 Directed energy and electromagnetic launch systems

- 3.8.1 Current technological trends

- 3.9 Emerging business models

- 3.10 Compliance requirements

- 3.11 Defense budget analysis

- 3.12 Global defense spending trends

- 3.13 Regional defense budget allocation

- 3.13.1 North America

- 3.13.2 Europe

- 3.13.3 Asia Pacific

- 3.13.4 Middle East and Africa

- 3.13.5 Latin America

- 3.14 Key defense modernization programs

- 3.15 Budget forecast (2025-2034)

- 3.15.1 Impact on industry growth

- 3.15.2 Defense budgets by country

- 3.15.3 Defense budget allocation by segment

- 3.15.3.1 Personnel

- 3.15.3.2 Operations and maintenance

- 3.15.3.3 Procurement

- 3.15.3.4 Research, development, test and evaluation

- 3.15.3.5 Infrastructure and construction

- 3.15.3.6 Technology and innovation

- 3.16 Sustainability initiatives

- 3.17 Supply chain resilience

- 3.18 Geopolitical analysis

- 3.19 Workforce analysis

- 3.20 Digital transformation

- 3.21 Mergers, acquisitions, and strategic partnerships landscape

- 3.22 Risk assessment and management

- 3.23 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.2 Market concentration analysis

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2021 – 2034 (USD Million)

- 5.1 Key trends

- 5.2 Guided

- 5.3 Unguided

Chapter 6 Market Estimates and Forecast, By Range, 2021 – 2034 (USD Million)

- 6.1 Key trends

- 6.2 Short range (up to 1 km)

- 6.3 Medium range (1–2.5 km)

- 6.4 Long range (above 2.5 km)

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million)

- 7.1 Key trends

- 7.2 Defense

- 7.2.1 Anti-aircraft

- 7.2.2 Anti-tank

- 7.2.3 Others

- 7.3 Homeland Security

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Daycraft Systems

- 9.2 Dynamit Nobel Defence GmbH

- 9.3 Lockheed Martin Corporation

- 9.4 MBDA

- 9.5 Nammo AS

- 9.6 RAFAEL Advanced Defense Systems Ltd.

- 9.7 Rheinmetall AG

- 9.8 RTX

- 9.9 Saab AB

2026年全球武器市场报告2026年全球武器弹药市场报告2026年全球肩扛式枪械市场报告

2026年全球武器市场报告2026年全球武器弹药市场报告2026年全球肩扛式枪械市场报告 动能衝击武器市场:2026-2032年全球市场预测(依产品类型、口径、最终用户、应用、通路和部署模式划分)武器製造市场:依产品类型、技术、平台、口径和最终用户划分-2026-2032年全球预测

动能衝击武器市场:2026-2032年全球市场预测(依产品类型、口径、最终用户、应用、通路和部署模式划分)武器製造市场:依产品类型、技术、平台、口径和最终用户划分-2026-2032年全球预测 航空航太武器市场-全球产业规模、份额、趋势、机会和预测:按飞机、武器类型、地区和竞争对手划分,2021-2031年

航空航太武器市场-全球产业规模、份额、趋势、机会和预测:按飞机、武器类型、地区和竞争对手划分,2021-2031年 肩射式武器市场规模、份额和成长分析(按组装、技术、射程、应用和地区划分)—产业预测(2026-2033 年)

肩射式武器市场规模、份额和成长分析(按组装、技术、射程、应用和地区划分)—产业预测(2026-2033 年) 远距离操纵武器站的全球市场:2025年~2035年40mm子弹的全球市场:2025-2035年

远距离操纵武器站的全球市场:2025年~2035年40mm子弹的全球市场:2025-2035年 全球武器弹药市场(至2032年):依类型、应用、武器系统、最终用户和地区

全球武器弹药市场(至2032年):依类型、应用、武器系统、最终用户和地区