|

市场调查报告书

商品编码

1773430

处方护目镜市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Prescription Goggles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

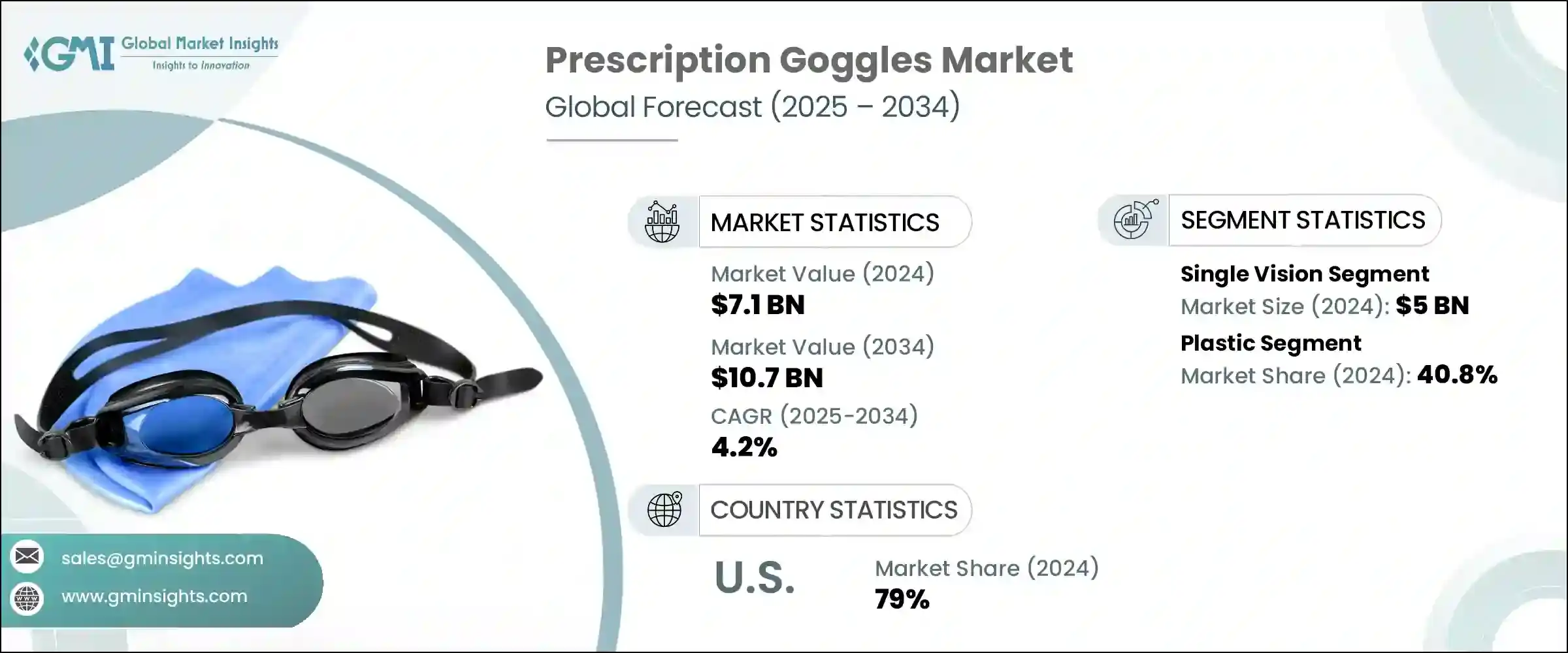

2024 年全球处方护目镜市场规模达 71 亿美元,预计到 2034 年将以 4.2% 的复合年增长率增长至 107 亿美元。人们对职业和休閒环境中眼睛保护问题的日益关注,极大地推动了市场的发展。处方安全护目镜具有双重功能,不仅可以矫正视力,还可以保护眼睛免受物理伤害。这些护目镜通常由耐用、抗衝击的材料製成,能够有效阻挡空气中的颗粒物、化学物质飞溅和其他环境危害。随着全球职业安全准则日益严格,雇主有义务为员工配备符合处方要求的防护眼镜。对更安全工作环境的追求,以及各行各业对合规性要求的严格要求,正在推动对安全护目镜的持续需求。

除了工作场所,消费者也越来越注重日常活动中的眼睛健康。户外休閒人士寻求既能矫正视力,又能抵御灰尘、水和紫外线等自然因素的眼镜。处方护目镜兼具功能性和舒适性,尤其在镜片技术不断发展的今天,满足了这项需求。涂层技术的创新提升了清晰度、耐刮擦性和镜片寿命,使防护眼镜的用途比以往任何时候都更加广泛。此外,人们越来越青睐由聚碳酸酯製成的轻质镜片,尤其是具有防反射性能的镜片,它们可以提升视觉效果并减轻眼睛疲劳。随着数位接触的增加,近视、远视和老花眼等视力问题变得越来越普遍,对矫正性防护镜的需求也稳定成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 71亿美元 |

| 预测值 | 107亿美元 |

| 复合年增长率 | 4.2% |

生活方式的改变,加上长时间坐在数位萤幕前,导致各年龄层的视力问题显着增加。这刺激了对具有矫正功能的防护眼镜的需求。此外,人们越来越倾向于健身和休閒活动,这进一步推动了市场的发展,在这些活动中,使用者需要既能矫正视力又不损害安全性的护目镜。无论是在运动、专业工作或日常活动中使用,处方护目镜如今都被视为个人防护装备的重要组成部分。

根据镜片类型,市场细分为单光镜片和双光渐进镜片。单光镜片占最大份额,2024年收入达50亿美元。这种优势可以归因于单光护目镜在矫正近视和远视等常见疾病方面的有效性。这类护目镜因其价格实惠、易于自订和适用性广泛而备受青睐。它们可以配备各种镀膜和材质,以满足不同的使用者需求,适合不同年龄和职业的人士。与双光镜片或渐进镜片相比,单光镜片相对较低的价格也使其广受欢迎。

就镜框材质而言,处方护目镜市场分为塑胶、硅胶/橡胶和其他材质。 2024年,塑胶镜框占据了全球40.8%的市场份额,估值达29.1亿美元。塑胶镜框的广泛应用主要源自于其轻量和抗破损的特性。在塑胶材料中,聚碳酸酯仍然是首选,因其卓越的抗衝击性和内建的紫外线防护功能而闻名。这些特性在安全性至关重要的应用中尤其重要。其他材料,例如硅胶和橡胶,则用于密封圈和绑带等非光学部件,以增强佩戴的贴合度和舒适度,但由于它们无法提供矫正视力的功能,因此不适用于镜片。

北美继续成为处方护目镜行业的领先地区,其中美国扮演着核心角色。 2024年,美国占了该地区79%的市场份额,凸显了该国对眼部健康和矫正视力产品的高度重视。高视力矫正使用率和安全意识的提升,正在推动处方护目镜在消费和职业领域的普及。美国眼镜的普及也反映了光学解决方案的广泛普及以及消费者对视力保护益处的认知度不断提高。

产业新兴趋势包括采用先进的镜片材料和改进的镀膜,例如具有蓝光过滤和眩光减少功能的镀膜。可客製化的镜框设计和个人化的配戴选择正变得越来越普遍,这与消费者追求个人化产品的普遍趋势相契合。电商平台的兴起使消费者更容易获得各种符合特定视觉和生活方式需求的处方护目镜。

塑造全球格局的关键参与者包括领先的光学製造商和处方安全眼镜领域的专业厂商。这些公司正在利用技术,将防雾、变色镜片和偏光涂层等功能融入其产品中。他们也专注于采用耐用且轻巧的材料,例如Trivex和聚碳酸酯,以增强使用者的舒适度和防护性。从工作场所到休閒娱乐,处方护目镜在当今这个对视觉要求极高的世界变得越来越不可或缺。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 视力障碍盛行率

- 眼部健康和安全意识不断增强

- 增加户外和体育活动的参与度

- 对个性化和时尚眼镜的需求

- 产业陷阱与挑战

- 专用镜头和客製化成本高

- 组装和客製化的复杂性

- 机会

- 成长动力

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按产品

- 按地区

- 监管格局

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按镜头类型,2021 - 2034 年

- 主要趋势

- 单视

- 双焦渐进镜片

第六章:市场估计与预测:按框架材料,2021 - 2034 年

- 主要趋势

- 塑胶

- 硅/橡胶

- 其他的

第七章:市场估计与预测:按价格,2021 - 2034 年

- 主要趋势

- 低的

- 中等的

- 高的

第八章:市场估计与预测:按消费者群体,2021 - 2034 年

- 主要趋势

- 男性

- 女性

第九章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 游泳/浮潜护目镜

- 运动护目镜

- 工业安全护目镜

- 时尚护目镜

- 摩托车/自行车护目镜

- 其他的

第 10 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 在线的

- 电子商务

- 公司网站

- 离线

- 专卖店

- 大型零售商店

- 其他的

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- Arena

- First Lens

- GOGGLEMAN

- SafeVision

- John Jacobs

- Liberty Sport

- MSA Safety

- Oakley

- RxSport

- Safety-RX

- Speedo

- Sutton Swimwear

- TYR

- Uvex

- Wiley X

The Global Prescription Goggles Market was valued at USD 7.1 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 10.7 billion by 2034. Growing concerns about eye protection across professional and recreational environments are significantly driving the market. Prescription safety goggles serve a dual function by not only correcting vision but also shielding eyes from physical harm. These goggles are commonly manufactured using durable, impact-resistant materials that offer a reliable barrier against airborne particles, chemical splashes, and other environmental hazards. With occupational safety guidelines becoming increasingly stringent worldwide, employers are obligated to equip their workforce with proper protective eyewear that accommodates prescription needs. The push for safer work environments, along with compliance mandates across industrial sectors, is fueling consistent demand.

Apart from the workplace, consumers are becoming more mindful of maintaining their eye health during daily activities. People involved in outdoor recreation are seeking eyewear that provides both visual correction and defense from natural elements like dust, water, and UV radiation. Prescription goggles meet this demand by combining functionality with comfort, especially as lens technology continues to evolve. Innovations in coatings that improve clarity, scratch resistance, and lens longevity are making protective eyewear more versatile than ever. There is also a rising preference for lightweight lenses made from polycarbonate, especially those with anti-reflective properties, which enhance visual performance and reduce eye strain. As digital exposure increases, vision issues such as nearsightedness, farsightedness, and presbyopia have become more common, and the need for corrective protective goggles is steadily increasing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.1 Billion |

| Forecast Value | $10.7 Billion |

| CAGR | 4.2% |

Changing lifestyles, combined with longer hours in front of digital screens, are contributing to a noticeable uptick in vision-related problems across various age groups. This has spurred a rise in demand for protective eyewear with corrective capabilities. The market is further supported by the growing inclination toward physical fitness and recreational activities, where users require goggles that offer vision correction without compromising on safety. Whether used during sports, professional work, or everyday activities, prescription goggles are now considered an essential part of personal protective equipment.

By lens type, the market is segmented into single vision and bifocal progressive lenses. The single vision category accounted for the largest share, bringing in USD 5 billion in revenue in 2024. This dominance can be attributed to the effectiveness of single vision goggles in correcting widely prevalent conditions like nearsightedness and farsightedness. These goggles are often preferred due to their affordability, ease of customization, and wide applicability. They can be equipped with various coatings and materials to meet diverse user requirements, making them suitable for individuals across different age groups and occupations. Their relatively lower cost compared to bifocal or progressive lenses also contributes to their popularity.

In terms of frame materials, the prescription goggles market is categorized into plastic, silicone/rubber, and others. Plastic frames held a significant 40.8% of the global market share in 2024, with a valuation of USD 2.91 billion. The widespread use of plastic in frames is primarily due to its lightweight properties and resistance to breakage. Among plastic materials, polycarbonate remains a leading choice, known for its superior impact resistance and built-in UV protection. These features are especially critical in applications where safety is non-negotiable. Other materials, such as silicone and rubber, are used in non-optical components like seals and straps to enhance fit and comfort, although they are not suitable for lenses due to their inability to support corrective vision properties.

North America continues to be a leading region for the prescription goggles industry, with the United States playing a central role. In 2024, the U.S. held 79% of the regional market, underscoring the country's strong focus on eye health and corrective vision products. A high rate of vision correction usage and heightened safety awareness are pushing the adoption of prescription goggles across consumer and occupational segments. The popularity of eyewear in the U.S. also reflects widespread access to optical solutions and heightened consumer awareness regarding the benefits of vision protection.

Emerging trends in the industry include the adoption of advanced lens materials with improved coatings, such as those offering blue light filtration and glare reduction. Customizable frame designs and personalized fitting options are becoming more common, aligning with the broader consumer trend toward individualized products. The rise of e-commerce platforms is making it easier for consumers to access a wide range of prescription goggles tailored to specific visual and lifestyle needs.

Key players shaping the global landscape include leading optical manufacturers and niche specialists in prescription safety eyewear. These companies are leveraging technology to integrate features like anti-fogging, photochromic lenses, and polarized coatings into their products. They are also focusing on durable yet lightweight materials such as Trivex and polycarbonate to enhance user comfort and protection. From workplace applications to recreational use, prescription goggles are becoming increasingly indispensable in a visually demanding world.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Lens type

- 2.2.3 Frame material

- 2.2.4 Price

- 2.2.5 Consumer group

- 2.2.6 Application

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Prevalence of vision impairment

- 3.2.1.2 Growing awareness of eye health and safety

- 3.2.1.3 Increased participation in outdoor and sports activities

- 3.2.1.4 Demand for personalized and fashionable eyewear

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High costs of specialized lenses and customization

- 3.2.2.2 Fitting and customization complexity

- 3.2.3 Opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By Product

- 3.6.2 By region

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Lens Type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Single vision

- 5.3 Bi-focal progressive

Chapter 6 Market Estimates and Forecast, By Frame Material, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Silicon/rubber

- 6.4 Others

Chapter 7 Market Estimates and Forecast, By Price, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates and Forecast, By Consumer Group, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Male

- 8.3 Female

Chapter 9 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Swimming/snorkeling goggles

- 9.3 Sports goggles

- 9.4 Industrial safety goggles

- 9.5 Fashion goggles

- 9.6 Motorcycle/bicycle goggles

- 9.7 Others

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Online

- 10.2.1 E-commerce

- 10.2.2 Company website

- 10.3 Offline

- 10.3.1 Specialty stores

- 10.3.2 Mega retail stores

- 10.3.3 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Arena

- 12.2 First Lens

- 12.3 GOGGLEMAN

- 12.4 SafeVision

- 12.5 John Jacobs

- 12.6 Liberty Sport

- 12.7 MSA Safety

- 12.8 Oakley

- 12.9 RxSport

- 12.10 Safety-RX

- 12.11 Speedo

- 12.12 Sutton Swimwear

- 12.13 TYR

- 12.14 Uvex

- 12.15 Wiley X