|

市场调查报告书

商品编码

1773438

建筑用秸秆捆市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Straw Bale for Construction Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

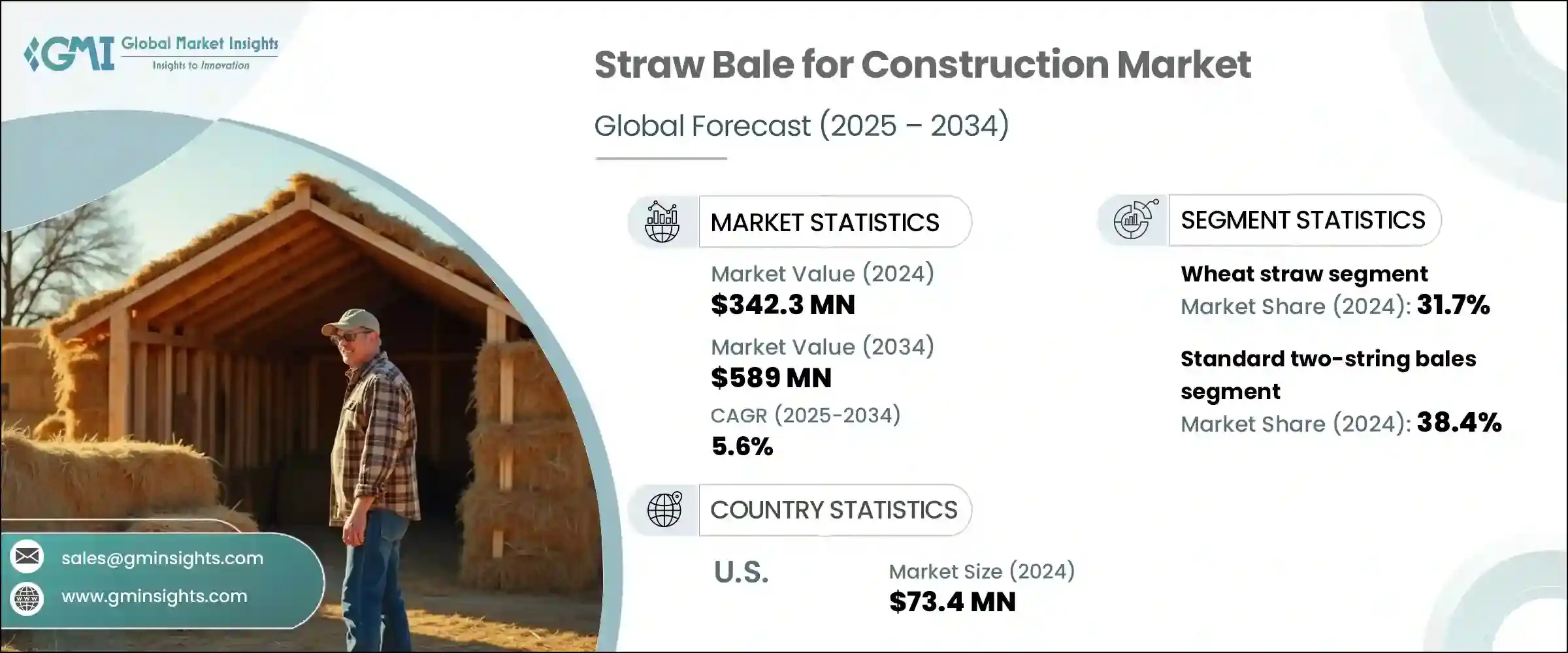

2024年,全球建筑用秸秆捆市场价值为3.423亿美元,预计到2034年将以5.6%的复合年增长率成长,达到5.89亿美元。这项成长主要归功于秸秆捆建筑的环保节能特性。该技术利用紧密压实的秸秆捆作为主要墙体材料,并以天然灰泥或涂料进行表面处理,因其对环境影响较小而备受青睐。作为农业副产品,秸秆来源丰富且价格低廉,使其成为建筑业的永续替代品。秸秆捆结构的优点在于其卓越的隔热性能,其R值通常在R-30到R-35之间,取决于捆包密度和墙体厚度。

这些高隔热值可降低能耗,尤其是在暖气和冷气方面,从而节省成本并带来环境效益。此外,秸秆还能作为天然的碳汇,封存植物生长週期中吸收的二氧化碳。这种碳储存能力增强了材料在减少建筑物整体碳足迹方面的作用。随着人们对低影响建筑解决方案的兴趣日益浓厚,秸秆捆包建筑在不同地区正成为越来越受欢迎的选择,尤其是在重视绿色基础设施、永续住房和可再生材料的地区。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3.423亿美元 |

| 预测值 | 5.89亿美元 |

| 复合年增长率 | 5.6% |

小麦秸秆因其易得性和结构优势,在2024年占据了31.7%的市场。其纤维平行排列的特性使其在结构应用上具有良好的填充性、优异的隔热性能和耐久性。此外,小麦秸秆易于生物降解,对建筑环境的适应性也使其应用范围不断扩大。小麦秸秆因其防潮性能和与生态建筑方法的兼容性而广受认可。小麦秸秆长期以来与传统建筑技术的融合,以及其在当代永续建筑中的卓越性能,进一步推动了其在各个地区的应用。

2024年,标准双绳捆包市占38.4%的市占率。这些捆包因其易于整合到承重建筑系统中而被广泛使用。其均衡的尺寸和重量提高了搬运效率,并且与传统捆包设备相容,使其非常容易获得。建筑商、承包商和自建房业主青睐这些捆包,因为它们经济高效且易于运输。此外,旨在推广永续建筑的培训计画和教育活动经常将这些捆包作为教学工具,帮助增强社区对环保建筑实践的理解。

2024年,美国建筑用秸秆捆市场产值达7,340万美元。美国在秸秆捆建筑领域的领先地位得益于日益重视环保住房,以及推广低碳建筑方法的区域性倡议。秸秆作为农业副产品的可取得性,加上市场对永续离网和客製化住宅日益增长的需求,持续推动着秸秆捆建筑的普及。政府鼓励生态住宅开发的计划,以及注重清洁材料的州级能源政策,进一步强化了这一趋势,并促进了全球郊区和半乡村地区的秸秆捆建筑的扩张。

全球建筑用秸秆捆产业仍较为分散,Endeavour Centre、Strawcture Eco、ModCell Straw Technology、Ecococon 和 Straw-Bale Building UK 等主要参与者积极布局利基市场,并满足本地需求。建筑用秸秆捆市场中的企业正在采取有针对性的策略,以增强其市场影响力,并适应不断变化的环境和消费者需求。

许多公司专注于秸秆的本地生产和采购,以降低物流成本和碳排放。产品标准化工作正在推进,以符合地区建筑规范并赢得主流建筑业的信任。与建筑师和注重永续发展的开发商的策略合作,有助于公司展示秸秆捆包建筑在现代生态住宅中的应用案例。以教育为主导的活动和以社区为基础的研讨会进一步提升了市场认知,而实践培训计划则增强了承包商和自建者的信心。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按秸秆类型

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)

(註:仅提供重点国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按秸秆类型,2021 - 2034 年

- 主要趋势

- 麦秸

- 稻草

- 大麦秸秆

- 燕麦秸秆

- 黑麦秸秆

- 其他的

第六章:市场估计与预测:按捆包格式,2021 - 2034 年

- 主要趋势

- 标准双绳捆包

- 三串捆包

- 巨型捆包

- 客製尺寸的捆包

- 预製秸秆板

第七章:市场估计与预测:依施工方法,2021 - 2034 年

- 主要趋势

- 承重/内布拉斯加风格

- 柱樑填充

- 混合方法

- 预製板系统

- 其他的

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 外墙

- 内墙

- 屋顶隔热

- 地板隔热

- 隔音效果

- 其他的

第九章:估计和预测:按最终用途领域,2021 - 2034 年

- 主要趋势

- 住宅建筑

- 独栋住宅

- 多户建筑

- 微型住宅和小木屋

- 增建和翻新

- 商业建筑

- 教育设施

- 生态旅游设施

- 零售和办公空间

- 其他的

- 农业建筑

- 社区与公共建筑

- 其他的

第十章:估计与预测:按表面处理类型,2021 - 2034 年

- 主要趋势

- 石灰石膏

- 黏土灰泥

- 水泥灰泥

- 土製灰泥

- 壁板和覆层

- 其他的

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十二章:公司简介

- BRAR AGRO WORKS

- CalFibre

- Ecococon

- Endeavour Centre

- Grass Land Gold Pvt. Ltd

- Gruppo Carli

- ModCell Straw Technology

- Profodd Private Limited

- Straw-Bale Building UK

- Strawcture Eco

The Global Straw Bale for Construction Market was valued at USD 342.3 million in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 589 million by 2034. This growth is largely attributed to the eco-friendly and energy-efficient characteristics of straw bale construction. Utilizing tightly compacted straw bales as primary wall material, the technique is finished with natural plasters or coatings and has gained traction for its low environmental impact. As an agricultural by-product, straw is abundantly available and affordable, making it a sustainable alternative in construction. What makes straw bale structures stand out is their impressive insulation capability, with R-values typically ranging between R-30 and R-35, depending on bale density and wall thickness.

These high insulation values reduce energy consumption, especially in heating and cooling, resulting in cost savings and environmental benefits. Additionally, straw serves as a natural carbon sink, sequestering carbon dioxide absorbed during the plant's growth cycle. This carbon-storing ability enhances the material's role in reducing the overall carbon footprint of buildings. With rising interest in low-impact building solutions, straw bale construction is becoming an increasingly popular choice across different geographies, particularly in areas emphasizing green infrastructure, sustainable housing, and renewable materials.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $342.3 Million |

| Forecast Value | $589 Million |

| CAGR | 5.6% |

The wheat straw segment held a 31.7% share in 2024 due to its availability and structural advantages. Its parallel fiber orientation enables compact packing, consistent insulation, and durability in structural applications. Furthermore, its ease of biodegradation and adaptability to construction environments contribute to its growing use. Wheat straw is recognized for its moisture-resistant properties and compatibility with eco-construction methods. The material's long-standing integration into traditional building techniques and its proven performance in contemporary sustainable construction further boost its adoption across various regions.

The standard two-string bales segment held a 38.4% share in 2024. These bales are widely used because of their ease of integration into load-bearing construction systems. Their balanced size and weight improve handling efficiency, and their compatibility with conventional baling equipment makes them highly accessible. Builders, contractors, and self-builders favor these bales for their cost-effectiveness and ease of transport. Additionally, training programs and educational initiatives aimed at promoting sustainable building often feature these bales as teaching tools, helping to enhance community understanding of eco-friendly construction practices.

United States Straw Bale for Construction Market generated USD 73.4 million in 2024. The country's leadership in straw bale construction is supported by a growing emphasis on environmentally conscious housing and regional initiatives promoting low-carbon building methods. The availability of straw as a farming by-product, combined with evolving demand for sustainable off-grid and custom-built homes, continues to push adoption forward. Support from governmental programs encouraging ecological housing development, alongside state-level energy policies focused on clean materials, reinforces this trend and fosters expansion in suburban and semi-rural areas globally.

The Global Straw Bale for Construction Industry remains moderately fragmented, with key players such as Endeavour Centre, Strawcture Eco, ModCell Straw Technology, Ecococon, and Straw-Bale Building UK actively operating in niche markets and supporting localized demand. Companies in the straw bale construction market are employing targeted strategies to bolster their market presence and adapt to changing environmental and consumer demands.

Many firms are focusing on local production and sourcing of straw to reduce logistics costs and carbon emissions. Product standardization efforts are being pursued to comply with regional building codes and gain trust from mainstream construction sectors. Strategic collaborations with architects and sustainability-focused developers help companies showcase use cases of straw bale construction in modern eco-homes. Education-driven campaigns and community-based workshops further promote market awareness, while hands-on training initiatives increase confidence among contractors and self-builders.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Straw type

- 2.2.2 Bale format

- 2.2.3 Construction method

- 2.2.4 Application

- 2.2.5 End use sector

- 2.2.6 Finishing type

- 2.2.7 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By straw type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Straw Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Wheat straw

- 5.3 Rice straw

- 5.4 Barley straw

- 5.5 Oat straw

- 5.6 Rye straw

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Bale Format, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Standard two-string bales

- 6.3 Three-string bales

- 6.4 Jumbo bales

- 6.5 Custom-sized bales

- 6.6 Prefabricated straw panels

Chapter 7 Market Estimates and Forecast, By Construction Method, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Load-bearing/nebraska style

- 7.3 Post-and-beam infill

- 7.4 Hybrid methods

- 7.5 Prefabricated panel systems

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Exterior walls

- 8.3 Interior walls

- 8.4 Roof insulation

- 8.5 Floor insulation

- 8.6 Sound insulation

- 8.7 Others

Chapter 9 Estimates and Forecast, By End Use Sector, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Residential construction

- 9.2.1 Single-family homes

- 9.2.2 Multi-family buildings

- 9.2.3 Tiny homes and cabins

- 9.2.4 Additions and renovations

- 9.3 Commercial construction

- 9.3.1 Educational facilities

- 9.3.2 Eco-tourism facilities

- 9.3.3 Retail and office spaces

- 9.3.4 Others

- 9.4 Agricultural buildings

- 9.5 Community and public buildings

- 9.6 Others

Chapter 10 Estimates and Forecast, By Finishing Type, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Lime plaster

- 10.3 Clay plaster

- 10.4 Cement stucco

- 10.5 Earthen plasters

- 10.6 Siding and cladding

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Rest of Europe

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Rest of Asia Pacific

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Rest of Latin America

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

- 11.6.4 Rest of Middle East and Africa

Chapter 12 Company Profiles

- 12.1 BRAR AGRO WORKS

- 12.2 CalFibre

- 12.3 Ecococon

- 12.4 Endeavour Centre

- 12.5 Grass Land Gold Pvt. Ltd

- 12.6 Gruppo Carli

- 12.7 ModCell Straw Technology

- 12.8 Profodd Private Limited

- 12.9 Straw-Bale Building UK

- 12.10 Strawcture Eco