|

市场调查报告书

商品编码

1773470

宠物服务市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Pet Services Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

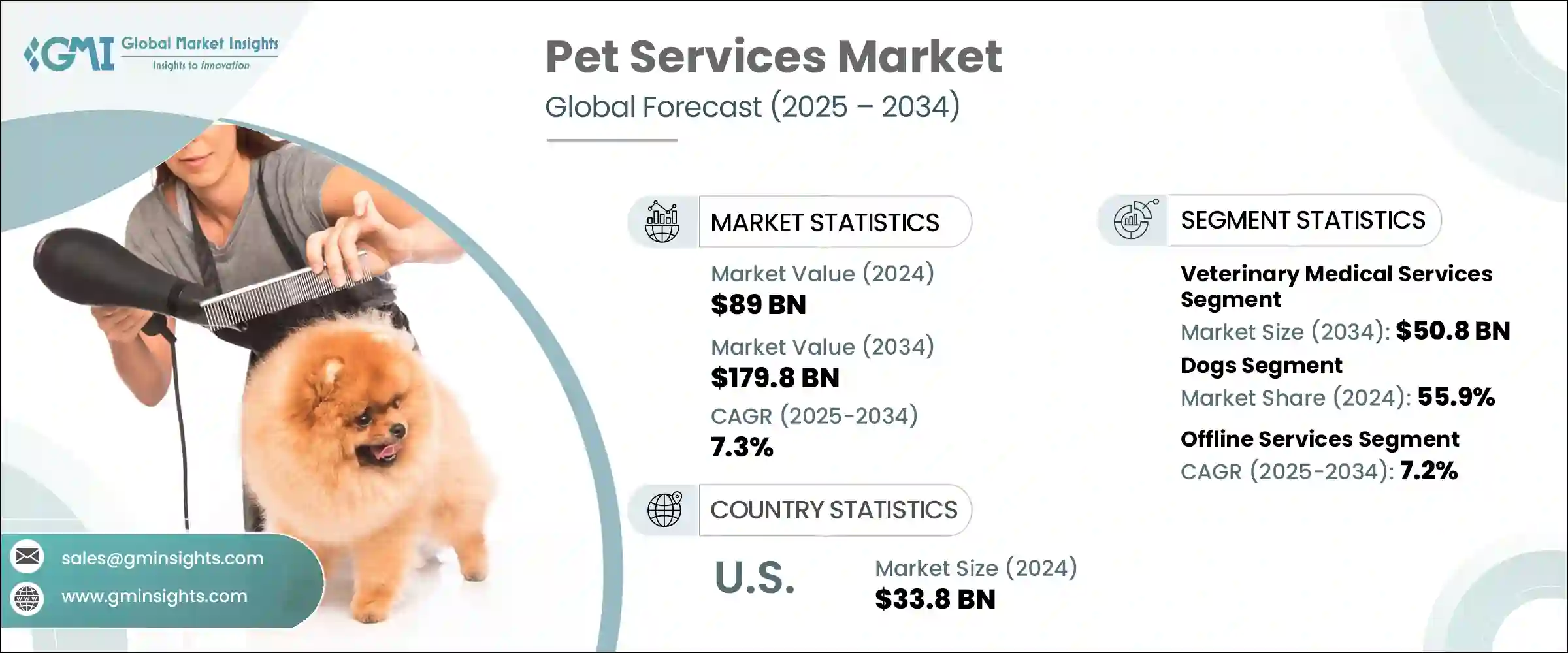

2024年,全球宠物服务市场规模达890亿美元,预计到2034年将以7.3%的复合年增长率成长,达到1,798亿美元。这一增长主要源于宠物慢性健康问题(例如关节炎、糖尿病和肥胖症)发病率的上升,这促使宠物对常规体检、復健护理和专科治疗的需求不断增加。宠物主人越来越重视宠物的健康和卫生,导致专业美容、兽医诊疗和保险投保数量激增。

此外,向数位化工具(例如虚拟兽医预约和线上预约系统)的转变提升了护理服务的可近性。这种科技驱动的转型,加上宠物拥有量的上升和人性化趋势,正在强化全球市场的宠物照护服务生态系统。宠物服务涵盖了广泛的服务,以满足伴侣动物的需求,包括医疗和非医疗服务。这些服务包括美容、兽医护理、日托、寄养和训练。保险覆盖范围的扩大进一步提升了优质服务的可近性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 890亿美元 |

| 预测值 | 1798亿美元 |

| 复合年增长率 | 7.3% |

同时,兽医医疗保健产业正在经历数位转型,这正在重新定义宠物服务的提供和取得方式。远距会诊的日益普及不仅为宠物主人带来了便利,也确保了及时的医疗干预,尤其是在偏远或医疗资源匮乏的地区。智慧健康追踪设备,包括穿戴式项圈和可植入感测器,能够即时监测宠物的生命征象、活动量和行为变化,为兽医和宠物主人提供切实可行的洞察。

2024年,兽医医疗服务领域产值达264亿美元,预计到2034年将达到508亿美元,复合年增长率为6.8%。此领域涵盖普通医疗、专科治疗和紧急服务。宠物数量的成长,加上传染病和慢性病的发病率上升,加速了兽医照护的需求。此外,城市环境中宠物人性化程度的提高正在影响消费模式,越来越多的家庭开始为高端宠物服务和产品预留预算。医疗基础设施的改善使宠物主人更容易获得先进的兽医护理。因此,医疗服务仍然是整个市场的基础支柱,而人们日益增长的宠物健康意识和投资意愿也为医疗服务的发展提供了支持。

2024年,狗狗细分市场占据了55.9%的市场份额,这得益于狗狗作为伴侣动物的广泛普及以及宠物与主人之间日益增长的情感纽带。狗狗主人在日托、美容和健康体检等高品质服务上的支出不断增加,进一步强化了全面宠物照护的价值。针对特定犬种的美容、专业训练和高级医疗保健服务的需求持续激增。此外,商业宠物护理机构的扩张和数位服务平台的兴起,使得与狗狗相关的服务更加便捷易得,巩固了其在全球市场的地位。

2024年,北美宠物服务市场规模达357亿美元,预计2034年将达到694亿美元,复合年增长率为6.9%。该地区的领先地位源于其高度发展的宠物护理基础设施、日益增长的宠物拥有量以及日益增强的宠物健康意识。该地区各国对预防性兽医护理和个人化美容等高端服务的需求激增。现代兽医诊所、高端服务连锁店和数位化宠物护理解决方案的普及也推动了这一成长。此外,宠物主人正在积极利用科技驱动的平台来安排和管理服务。区域性公司正在扩展服务组合,并充分利用消费者偏好,这有助于持续的市场扩张。

全球宠物服务市场的知名企业包括 IDEXX Laboratories、Dogtopia、PetIQ、VIP Petcare、Petfirst Healthcare、PetSmart、Hartville Group、Vetcor、Anicom Holding、The Barkley Pet Hotel & Day Spa、DogVacay、Mars、K9 Resorts、Rover、Figo Insurance、Holleter为了巩固市场地位,宠物服务领域的公司正在投资服务多元化和数位转型。

许多公司正在采用基于应用程式的平台和远距医疗服务,以简化客户体验并提高服务便利性。与兽医网络、保险公司和科技公司建立策略伙伴关係,有助于扩大服务范围,同时提升护理品质。该公司还推出了健康计划和订阅模式,以提高客户忠诚度和经常性收入来源。此外,针对兽医和护理人员的持续培训计画正在提升服务标准。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 宠物拥有率上升

- 宠物人性化趋势

- 提高宠物主人的健康意识

- 兽医服务技术不断进步

- 产业陷阱与挑战

- 服务成本高

- 动物福利监理挑战

- 市场机会

- 数位转型和线上预订的成长

- 扩大宠物保险

- 成长动力

- 成长潜力分析

- 2024年宠物数量统计

- 监管格局

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 扩张计划

第五章:市场估计与预测:依服务类型,2021 年至 2034 年

- 主要趋势

- 宠物美容

- 宠物寄养和日托

- 宠物训练服务

- 宠物保险

- 兽医医疗服务

- 一般服务

- 专业服务

- 紧急服务

- 其他服务类型

第六章:市场估计与预测:按宠物类型,2021 年至 2034 年

- 主要趋势

- 狗

- 猫

- 鸟类

- 鱼类

- 马匹

- 其他宠物类型

第七章:市场估计与预测:依交付方式,2021 年至 2034 年

- 主要趋势

- 线上服务

- 线下服务

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Anicom Holding

- Dogtopia

- DogVacay

- Ethos Veterinary Health

- Figo Pet Insurance

- Hartville Group

- Hollard

- IDEXX Laboratories

- K9 Resorts

- Mars

- Petfirst Healthcare

- PetIQ

- PetSmart

- Rover

- The Barkley Pet Hotel & Day Spa

- Vetcor

- VIP Petcare

The Global Pet Services Market was valued at USD 89 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 179.8 billion by 2034. This growth is largely driven by the increasing incidence of chronic health issues in pets, such as arthritis, diabetes, and obesity, which prompts a higher demand for routine check-ups, rehabilitation care, and specialty treatments. Pet owners are placing more importance on wellness and hygiene, resulting in a spike in professional grooming, veterinary visits, and insurance enrollments.

Additionally, the shift toward digital tools-such as virtual vet appointments and online booking systems-has enhanced the accessibility of care services. This tech-driven transformation, combined with rising pet ownership and humanization trends, is strengthening the pet care service ecosystem across global markets. Pet services encompass a wide range of offerings tailored to companion animals' needs, both medical and non-medical. These include grooming, veterinary care, daycare, boarding, and training. Expanding insurance coverage has further boosted access to premium services.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $89 Billion |

| Forecast Value | $179.8 Billion |

| CAGR | 7.3% |

In parallel, the veterinary healthcare sector is undergoing a digital transformation that is redefining how pet services are delivered and accessed. The growing integration of teleconsultations is not only improving convenience for pet owners but also ensuring timely medical intervention, especially in remote or underserved areas. Smart health tracking devices, including wearable collars and implantable sensors, are enabling real-time monitoring of pets' vital signs, activity levels, and behavioral changes-empowering both veterinarians and owners with actionable insights.

The veterinary medical services segment generated USD 26.4 billion in 2024 and is projected to reach USD 50.8 billion by 2034, growing at a CAGR of 6.8%. This segment includes general medical care, specialized treatments, and emergency services. A growing population of pets combined with increasing occurrences of both infectious and chronic conditions is accelerating the demand for veterinary care. Additionally, rising pet humanization in urban settings is influencing spending patterns, as more households allocate budgets for premium pet services and products. Improvements in healthcare infrastructure are making advanced veterinary care more accessible to pet owners. As a result, medical services remain a foundational pillar in the overall market, supported by growing awareness and willingness to invest in pet health.

The dogs segment held a 55.9% share in 2024 fueled by the widespread adoption of dogs as companion animals and the increasing emotional bond shared between pets and owners. Dog owners are spending more on high-quality services such as daycare, grooming, and health checkups, reinforcing the value of comprehensive pet care. The demand for breed-specific grooming, specialized training, and advanced healthcare options continues to surge. Additionally, the expansion of commercial pet care establishments and the emergence of digital service platforms have made dog-related services more convenient and accessible, solidifying their position in the global market.

North America Pet Services Market generated USD 35.7 billion in 2024 and is expected to reach USD 69.4 billion by 2034, with a CAGR of 6.9%. The region's leadership stems from its highly developed pet care infrastructure, increasing pet ownership, and heightened awareness about pet well-being. Countries across the region are seeing a surge in demand for high-end services such as preventive veterinary care and personalized grooming. The growth is also propelled by widespread access to modern veterinary clinics, premium service chains, and digital pet care solutions. Moreover, pet owners are actively engaging with technology-driven platforms to schedule and manage services. Regional companies are expanding service portfolios and capitalizing on consumer preferences, which is contributing to consistent market expansion.

Prominent players in the Global Pet Services Market include IDEXX Laboratories, Dogtopia, PetIQ, VIP Petcare, Petfirst Healthcare, PetSmart, Hartville Group, Vetcor, Anicom Holding, The Barkley Pet Hotel & Day Spa, DogVacay, Mars, K9 Resorts, Rover, Figo Pet Insurance, Hollard, Ethos Veterinary Health. To strengthen their market positioning, companies in the pet services space are investing in service diversification and digital transformation.

Many are adopting app-based platforms and telehealth services to streamline customer experiences and increase service convenience. Strategic partnerships with veterinary networks, insurance providers, and tech firms help expand their service footprint while also improving care quality. Firms are also launching wellness programs and subscription-based models to enhance customer loyalty and recurring revenue streams. Moreover, continuous training programs for veterinary and care staff are elevating service standards.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Service type

- 2.2.3 Pet type

- 2.2.4 Delivery mode

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership rate

- 3.2.1.2 Pet humanization trend

- 3.2.1.3 Increasing health awareness among pet owners

- 3.2.1.4 Growing technological advancements in veterinary services

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High service costs

- 3.2.2.2 Regulatory challenges on animal welfare

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in digital transformation and online booking

- 3.2.3.2 Expanding pet insurance

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pet population statistics 2024

- 3.5 Regulatory landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers and acquisitions

- 4.5.2 Partnerships and collaborations

- 4.5.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Service Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pet grooming

- 5.3 Pet boarding and daycare

- 5.4 Pet training services

- 5.5 Pet insurance

- 5.6 Veterinary medical services

- 5.6.1 General services

- 5.6.2 Specialty services

- 5.6.3 Emergency services

- 5.7 Other service types

Chapter 6 Market Estimates and Forecast, By Pet Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Birds

- 6.5 Fishes

- 6.6 Horses

- 6.7 Other pet types

Chapter 7 Market Estimates and Forecast, By Delivery Mode, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Online services

- 7.3 Offline services

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Anicom Holding

- 9.2 Dogtopia

- 9.3 DogVacay

- 9.4 Ethos Veterinary Health

- 9.5 Figo Pet Insurance

- 9.6 Hartville Group

- 9.7 Hollard

- 9.8 IDEXX Laboratories

- 9.9 K9 Resorts

- 9.10 Mars

- 9.11 Petfirst Healthcare

- 9.12 PetIQ

- 9.13 PetSmart

- 9.14 Rover

- 9.15 The Barkley Pet Hotel & Day Spa

- 9.16 Vetcor

- 9.17 VIP Petcare

全球宠物服务市场规模、份额、趋势和成长分析报告(2026-2034年)

全球宠物服务市场规模、份额、趋势和成长分析报告(2026-2034年) 宠物临终关怀服务市场(按服务类型、宠物类型和支付模式划分)-2026-2032年全球预测宠物纪念产品市场依产品类型、材质类型、宠物品种、价格范围及通路划分-2026年至2032年全球预测纪念叶服务市场依产品类型、服务模式、价格范围、最终用户和销售管道,全球预测(2026-2032年)虚拟宠物模拟器应用市场:平台、获利模式、游戏类型、宠物类型、使用者互动、画面风格、年龄层、全球预测(2026-2032年)

宠物临终关怀服务市场(按服务类型、宠物类型和支付模式划分)-2026-2032年全球预测宠物纪念产品市场依产品类型、材质类型、宠物品种、价格范围及通路划分-2026年至2032年全球预测纪念叶服务市场依产品类型、服务模式、价格范围、最终用户和销售管道,全球预测(2026-2032年)虚拟宠物模拟器应用市场:平台、获利模式、游戏类型、宠物类型、使用者互动、画面风格、年龄层、全球预测(2026-2032年) 宠物友善住宅解决方案市场预测至2032年:按住宅类型、解决方案、宠物类型、最终用户和地区分類的全球分析宠物友善咖啡馆市场预测至2032年:按服务类型、宠物类型、产品/服务、位置类型、经营模式、分销管道和区域分類的全球分析

宠物友善住宅解决方案市场预测至2032年:按住宅类型、解决方案、宠物类型、最终用户和地区分類的全球分析宠物友善咖啡馆市场预测至2032年:按服务类型、宠物类型、产品/服务、位置类型、经营模式、分销管道和区域分類的全球分析 全球宠物保存服务市场(依类型、应用和地区划分)-市场规模、产业趋势、机会分析及预测(2025-2033 年)全球高端宠物服务市场:预测至2032年-按宠物类型、服务类型、通路、最终用户和地区分類的分析宠物旅行服务市场预测至2032年:全球旅行类型、宠物类型、预订管道、价格分布、应用、最终用户和区域分析

全球宠物保存服务市场(依类型、应用和地区划分)-市场规模、产业趋势、机会分析及预测(2025-2033 年)全球高端宠物服务市场:预测至2032年-按宠物类型、服务类型、通路、最终用户和地区分類的分析宠物旅行服务市场预测至2032年:全球旅行类型、宠物类型、预订管道、价格分布、应用、最终用户和区域分析