|

市场调查报告书

商品编码

1797681

糖尿病酮酸中毒治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Diabetic Ketoacidosis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

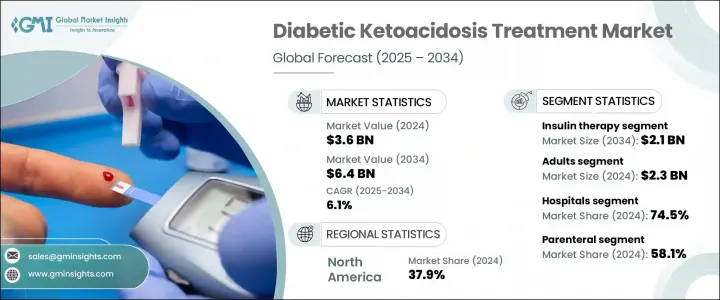

2024年,全球糖尿病酮酸中毒治疗市场规模达36亿美元,预计2034年将以6.1%的复合年增长率成长,达到64亿美元。这一成长轨迹主要受全球糖尿病发生率(尤其是第1型糖尿病)的上升以及技术先进的胰岛素给药方案的日益普及的影响。自动化胰岛素系统和持续血糖监测工具的突破有助于提供更精准的治疗,并改善患者的临床疗效。液体疗法和均衡的电解质配方也在加速康復和最大程度地减少潜在併发症方面发挥关键作用。

公共卫生资金、提高糖尿病认知的政策措施以及成熟市场和发展中市场急救体系的加强,显着推动了需求成长。糖尿病酮酸中毒的标准治疗方案包括速效胰岛素类似物、静脉补液和电解质调整,所有这些方案都旨在快速稳定患者病情。赛诺菲、美敦力、辉瑞、礼来和诺和诺德等行业领导者持续投资于先进製剂和合作,以扩大其全球影响力。人工智慧胰岛素帮浦和即时监测设备的进步正在透过提高反应速度和缩短復健时间重新定义治疗标准。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 36亿美元 |

| 预测值 | 64亿美元 |

| 复合年增长率 | 6.1% |

2024年,胰岛素治疗市场规模达12亿美元,预计2034年将成长至21亿美元,复合年增长率为5.6%。胰岛素在控制血糖和阻止酮容积方面发挥关键作用,这巩固了其在治疗领域的主导地位。速效胰岛素类似物因其起效迅速且疗效稳定,在急诊护理中被广泛采用。该领域的一项重大进展是智慧给药系统的集成,该系统将连续血糖监测仪与自动胰岛素输送系统连接起来。这些智慧系统可以即时优化胰岛素给药,降低低血糖风险,并提高病患安全性。

2024年,成年人口细分市场创造了23亿美元的收入。由于第1型糖尿病和胰岛素依赖型第2型糖尿病的广泛流行,成年人是受影响最严重的年龄层。这群人通常面临额外的健康併发症、诊断延迟以及血糖管理不规范,使他们更容易罹患糖尿病酮症酸中毒。这些复杂的情况需要有针对性的治疗方法,包括先进的胰岛素治疗和密切的电解质监测。鑑于对定制干预措施的需求以及该群体的高治疗量,製药公司将重点放在了这个群体上。

2024年,美国糖尿病酮酸中毒治疗市场占据90.1%的市场份额,这得益于高糖尿病盛行率和先进的医疗基础设施。美国持续受益于支持性的监管环境、密集的研发计划以及促进早期诊断和及时治疗的公众意识宣传活动。整合人工智慧和电子病历 (EHR) 平台的智慧胰岛素设备正成为许多医院的标配,有助于简化护理方案并缩短患者復健时间。美国无论是在紧急情况下或长期糖尿病照护中,对胰岛素的整体需求仍保持高位。

全球糖尿病酮酸中毒治疗市场的领导公司包括赛诺菲、默克公司、诺和诺德、礼来公司、费森尤斯卡比、沃克哈特、百特国际和辉瑞。各公司正优先开发人工智慧驱动的胰岛素输送系统、下一代类似物和联合疗法,以满足新兴的临床需求。与医院、研究机构和数位医疗公司建立策略联盟有助于加速技术整合和个人化治疗。各大公司正大力投资,透过在高负担地区进行临床试验和获得监管部门批准来扩大其产品组合。此外,全球製药业的领导者正在优化供应链并加强分销网络,以确保在已开发市场和服务不足市场的持续供应,从而增强其竞争优势。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球1型和第2型糖尿病盛行率上升

- 胰岛素输送与血糖监测技术的进步

- 提高对糖尿病酮症酸中毒的认识和早期诊断

- 产业陷阱与挑战

- 糖尿病酮酸中毒治疗和胰岛素治疗费用高昂

- 低收入和农村地区获得高级护理的机会有限

- 市场机会

- 向糖尿病负担日益加重的新兴市场扩张

- 远距医疗和数位健康工具的集成,实现远端管理

- 成长动力

- 成长潜力分析

- 监管格局

- 技术进步

- 当前的技术趋势

- 新兴技术

- 报销场景

- 临床试验概况

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按治疗类型,2021 - 2034 年

- 主要趋势

- 液体替代疗法

- 电解质替代疗法

- 胰岛素治疗

- 其他疗法

第六章:市场估计与预测:按年龄组,2021 - 2034 年

- 主要趋势

- 儿科

- 成年人

第七章:市场估计与预测:按管理路线,2021 - 2034 年

- 主要趋势

- 肠外

- 皮下

- 口服

- 其他给药途径

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 门诊手术中心

- 居家照护环境

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- Global Players

- Regional Players

- Emerging Players

The Global Diabetic Ketoacidosis Treatment Market was valued at USD 3.6 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 6.4 billion by 2034. This growth trajectory is largely shaped by the increasing incidence of diabetes worldwide, especially type 1 diabetes, combined with the rising use of technologically advanced insulin delivery solutions. Breakthroughs in automated insulin systems and continuous glucose monitoring tools are helping deliver more precise treatment and improve clinical outcomes for patients. Fluid therapy and well-balanced electrolyte formulations also play a key role in accelerating recovery and minimizing potential complications.

Public health funding, policy initiatives to increase diabetes awareness, and the strengthening of emergency care frameworks in both mature and developing markets are significantly propelling demand. Standard treatment regimens for diabetic ketoacidosis include rapid-acting insulin analogs, intravenous hydration, and electrolyte correction, all aimed at quickly stabilizing patients. Industry leaders such as Sanofi, Medtronic, Pfizer, Eli Lilly, and Novo Nordisk continue to invest in advanced formulations and collaborative efforts that expand their global presence. Progress in AI-powered insulin pumps and real-time monitoring devices is redefining treatment standards by enhancing responsiveness and reducing time to recovery.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 6.1% |

In 2024, the insulin therapy segment was valued at USD 1.2 billion, and it is expected to grow to USD 2.1 billion by 2034, registering a CAGR of 5.6%. The pivotal role of insulin in controlling blood glucose and stopping ketone accumulation underpins its dominance in the therapeutic landscape. Fast-acting insulin analogs are widely adopted in acute care settings due to their swift onset and consistent efficacy. A major development in this area is the integration of smart dosing systems that link continuous glucose monitors with automated insulin delivery. These intelligent systems optimize insulin administration in real time, lowering the risk of hypoglycemia and improving patient safety.

The adult population segment generated USD 2.3 billion in 2024. Adults represent the most affected age group due to the widespread occurrence of both type 1 and insulin-dependent type 2 diabetes. This population often faces additional health complications, delayed diagnoses, and inconsistent glycemic management, making them more susceptible to diabetic ketoacidosis. Such complexities require targeted therapeutic approaches, including advanced insulin treatments and close monitoring of electrolytes. Pharmaceutical companies focus their efforts heavily on this group, given the demand for tailored interventions and the high treatment volumes it commands.

United States Diabetic Ketoacidosis Treatment Market held a 90.1% share in 2024, driven by a combination of high diabetes prevalence and sophisticated healthcare infrastructure. The country continues to benefit from supportive regulatory environments, intensive R&D initiatives, and public awareness campaigns that promote early diagnosis and prompt treatment. Adoption of smart insulin devices integrated with AI and EHR platforms is becoming standard in many hospitals, helping streamline care protocols and reduce patient recovery times. The overall demand in the U.S. remains high across both emergency settings and long-term diabetes care.

Leading companies in the Global Diabetic Ketoacidosis Treatment Market include Sanofi, Merck & Co., Novo Nordisk, Eli Lilly and Company, Fresenius Kabi, Wockhardt, Baxter International, and Pfizer. Companies are prioritizing the development of AI-driven insulin delivery systems, next-gen analogs, and combination therapies to address emerging clinical needs. Strategic alliances with hospitals, research institutions, and digital health companies help accelerate tech integration and treatment personalization. Major firms are investing heavily in expanding their product portfolios through clinical trials and regulatory approvals in high-burden regions. Further, global pharmaceutical leaders are optimizing supply chains and bolstering distribution networks to ensure consistent access across developed and underserved markets, strengthening their competitive foothold.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global prevalence of type 1 and type 2 diabetes

- 3.2.1.2 Advancements in insulin delivery and glucose monitoring technologies

- 3.2.1.3 Increased awareness and early diagnosis of diabetic ketoacidosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of diabetic ketoacidosis treatment and insulin therapies

- 3.2.2.2 Limited access to advanced care in low-income and rural regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with rising diabetes burden

- 3.2.3.2 Integration of telemedicine and digital health tools for remote management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Clinical trials landscape

- 3.8 Future market trends

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Fluid replacement therapy

- 5.3 Electrolyte replacement therapy

- 5.4 Insulin therapy

- 5.5 Other therapies

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pediatric

- 6.3 Adults

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Parenteral

- 7.3 Subcutaneous

- 7.4 Oral

- 7.5 Other routes of administration

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Homecare settings

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Baxter International

- 10.1.2 Eli Lilly and Company

- 10.1.3 Fresenius Kabi

- 10.1.4 Merck & Co.

- 10.1.5 Novo Nordisk

- 10.1.6 Pfizer

- 10.1.7 Sanofi

- 10.1.8 Wockhardt

- 10.2 Regional Players

- 10.2.1 Biocon

- 10.2.2 Julphar

- 10.2.3 Otsuka Pharmaceutical

- 10.2.4 Tonghua Dongbao

- 10.2.5 Yuria-Pharm

- 10.3 Emerging Players

- 10.3.1 Adocia

- 10.3.2 Cipla

- 10.3.3 Gufic Biosciences

- 10.3.4 Hanmi Pharmaceuticals

- 10.3.5 Yiling Pharmaceutical

糖尿病酮酸症治疗市场分析及预测(至2035年):按类型、产品类型、服务、技术、应用、剂型、设备、最终用户、解决方案和阶段划分

糖尿病酮酸症治疗市场分析及预测(至2035年):按类型、产品类型、服务、技术、应用、剂型、设备、最终用户、解决方案和阶段划分 糖尿病酮酸症市场-全球产业规模、份额、趋势、机会及预测(依疗法、最终用户、地区及竞争格局划分,2021-2031年)糖尿病酮酸中毒治疗市场-全球产业规模、份额、趋势、机会和预测,按治疗类型、最终用户(医院、门诊手术中心、家庭护理机构)、地区和竞争情况细分,2020 年至 2030 年预测

糖尿病酮酸症市场-全球产业规模、份额、趋势、机会及预测(依疗法、最终用户、地区及竞争格局划分,2021-2031年)糖尿病酮酸中毒治疗市场-全球产业规模、份额、趋势、机会和预测,按治疗类型、最终用户(医院、门诊手术中心、家庭护理机构)、地区和竞争情况细分,2020 年至 2030 年预测 美国糖尿病酮酸症治疗市场规模、份额和趋势分析报告:按疗法、最终用途、地区和细分市场预测,2025 年至 2033 年

美国糖尿病酮酸症治疗市场规模、份额和趋势分析报告:按疗法、最终用途、地区和细分市场预测,2025 年至 2033 年 糖尿病酮酸症(DKA)治疗的全球市场,规模,占有率,趋势,产业分析报告:各治疗类型,各用途,各终端用户,各地区 - 市场预测,2025年~2034年糖尿病酮酸症治疗市场规模、份额和趋势分析报告:按治疗类型、最终用途、地区和细分市场预测,2025 年至 2033 年

糖尿病酮酸症(DKA)治疗的全球市场,规模,占有率,趋势,产业分析报告:各治疗类型,各用途,各终端用户,各地区 - 市场预测,2025年~2034年糖尿病酮酸症治疗市场规模、份额和趋势分析报告:按治疗类型、最终用途、地区和细分市场预测,2025 年至 2033 年