|

市场调查报告书

商品编码

1797703

外用药物包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Topical Drugs Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

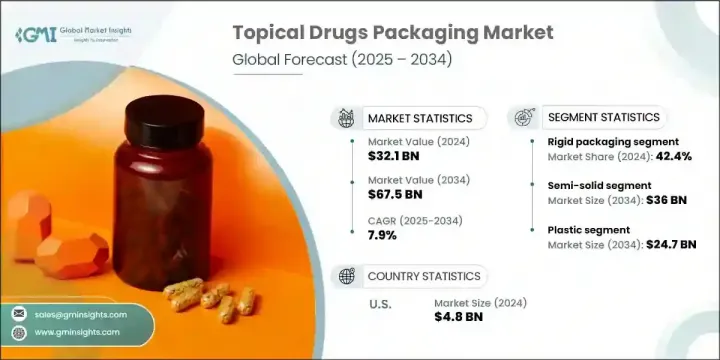

2024年,全球外用药物包装市场规模达321亿美元,预计到2034年将以7.9%的复合年增长率成长,达到675亿美元。日益严重的皮肤问题以及日益增长的直销管道(尤其是线上管道)是主要的成长动力。电子商务的蓬勃发展为製药公司(尤其是提供外用解决方案的公司)开闢了新的途径,使其能够直接接触更广泛的受众。

随着痤疮、湿疹和牛皮癣等皮肤病日益普遍,製药公司更加重视便利有效的局部治疗,这反过来又刺激了对安全创新包装的需求。二维码验证、防篡改密封和追踪追踪等数位技术在包装中的应用,在高价值和非处方皮肤病产品中越来越受欢迎。永续性持续重塑包装选择。市场参与者正在整合环保解决方案,包括可回收塑胶、补充装系统和可生物降解薄膜,这反映了製药业消费者和监管部门不断变化的期望。这些永续包装创新不仅有助于减少环境影响,还能提升品牌声誉和消费者信任。企业越来越多地投资于轻质、资源高效的材料开发,以最大限度地减少整个产品生命週期中的浪费。使用单一材料结构以便于回收,并减少碳足迹的包装工艺,在整个行业中变得越来越普遍。此外,对闭环系统的需求日益增长,该系统将废旧包装收集起来并重新加工成新产品。这些措施符合全球永续发展目标,同时满足了对符合道德和环境责任的医疗保健解决方案日益增长的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 321亿美元 |

| 预测值 | 675亿美元 |

| 复合年增长率 | 7.9% |

2024年,硬质包装占了42.4%的市场。瓶子、玻璃容器和罐子广泛用于高端和处方护肤品,因为它们能够提供保护、保持产品品质并支持储存稳定性。这些容器尤其受到青睐,因为它们能够处理黏稠的配方,并在敏感应用领域保持结构完整性。

预计 2025 年至 2034 年期间液体产品领域的复合年增长率为 7.9%。液体(包括防腐剂和药用喷雾)需要精确、安全的包装,以防止溢出和污染,同时支持活性成分的保存和剂量准确性。

2024年,北美外用药物包装市场占据37.6%的市场份额,预计在2025-2034年期间的复合年增长率将达到6.9%。强大的医药基础设施、对非处方药的偏好以及日益增长的自我照护习惯,正在推动该地区的包装创新。对电子商务的依赖程度不断提高,以及确保安全性和合规性的用户友好型包装,将继续塑造美国和加拿大的需求格局。

外用药品包装市场的领导公司包括 West Pharmaceutical Services、Schott、AptarGroup、Gerresheimer 和 Amcor。外用药品包装公司正在大力投资永续材料、数位安全和先进的配药系统,以满足消费者和製药客户不断变化的需求。各大品牌正透过可再填充容器、可生物降解包装膜和低碳製造进行创新,以符合环境法规和消费者偏好。产品差异化正在透过防篡改封盖、人体工学设计和序列化技术来增强,这些技术可以提高可追溯性和消费者信心。各公司也正在与製药商建立策略伙伴关係,共同开发针对特定皮肤病产品的包装形式。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 皮肤病和皮肤病盛行率不断上升

- 对便捷、用户友好的包装形式的需求不断增长

- 非处方外用药品的扩张

- 电子商务和直接面向消费者的药品销售成长

- 单位剂量和控制分配系统的创新

- 产业陷阱与挑战

- 严格的监管合规和审批流程

- 设计儿童安全且老年人友善的包装的复杂性

- 市场机会

- 向皮肤病学需求尚未充分满足的新兴市场扩张。

- 整合智慧包装技术,用于身份验证和患者参与。

- 对永续和可生物降解包装解决方案的投资不断增加。

- 零售药局连锁店的自有品牌外用产品线不断成长。

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 科技与创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 历史价格分析(2021-2024)

- 价格趋势驱动因素

- 区域价格差异

- 价格预测(2025-2034)

- 定价策略

- 新兴商业模式

- 合规性要求

- 永续性措施

- 永续材料评估

- 碳足迹分析

- 循环经济实施

- 永续性认证和标准

- 永续性投资报酬率分析

- 全球消费者情绪分析

- 专利分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 关键参与者的竞争基准

- 财务绩效比较

- 收入

- 利润率

- 研发

- 产品组合比较

- 产品范围广度

- 科技

- 创新

- 地理位置比较

- 全球足迹分析

- 服务网路覆盖

- 各地区市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 利基市场参与者

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年关键发展

- 併购

- 伙伴关係和合作

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型倡议

- 新兴/新创企业竞争对手格局

第五章:市场估计与预测:按包装类型,2021 - 2034 年

- 主要趋势

- 软包装

- 硬质包装

- 半硬质包装

第六章:市场估计与预测:按包装材料,2021 - 2034 年

- 主要趋势

- 塑胶

- 玻璃

- 金属

- 纸

- 铝

- 其他的

第七章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 瓶子

- 瓶盖和封口

- 吸入器

- 管

- 罐子

- 其他的

第 8 章:市场估计与预测:按药物类型,2021 - 2034 年

- 主要趋势

- 液体

- 半固体

- 坚硬的

- 透皮

第九章:市场估计与预测:按关闭类型,2021 - 2034 年

- 主要趋势

- 螺旋盖

- 翻盖

- 泵浦式分配器

- 滴管

- 喷嘴

第十章:市场估计与预测:按管理模式,2021 - 2034 年

- 主要趋势

- 眼科用途

- 鼻腔使用

- 皮肤使用

第 11 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 皮肤科

- 眼科

- 其他的

第 12 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十三章:公司简介

- Global Key Players

- Regional Key Players

- 利基市场参与者/颠覆者

- CCL工业公司

- LOG Pharma 初级包装

- 尼利帕克

The Global Topical Drugs Packaging Market was valued at USD 32.1 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 67.5 billion by 2034. Rising skin conditions and growing direct-to-consumer sales channels, particularly online, are among the primary growth drivers. The boom in e-commerce has opened new pathways for pharmaceutical companies, especially those offering topical solutions, to reach broader audiences directly.

With skin conditions like acne, eczema, and psoriasis becoming increasingly prevalent, pharmaceutical firms are focusing more on accessible and effective topical treatments, which in turn boosts demand for safe and innovative packaging. Digital tech adoption in packaging-such as QR verification, tamper-proof seals, and track-and-trace capabilities-is gaining traction in high-value and OTC dermatology products. Sustainability continues to reshape packaging choices. Market players are integrating eco-conscious solutions, including recyclable plastics, refill systems, and biodegradable films, reflecting shifting consumer and regulatory expectations in the pharmaceutical sector. These sustainable packaging innovations are not only helping reduce environmental impact but also enhancing brand reputation and consumer trust. Companies are increasingly investing in the development of lightweight, resource-efficient materials that minimize waste throughout the product lifecycle. The use of mono-material structures for easier recyclability, along with reduced carbon footprint packaging processes, is becoming more common across the industry. Additionally, there's a growing push for closed-loop systems, where used packaging is collected and reprocessed into new products. Such initiatives align with global sustainability goals while meeting the rising demand for ethical and environmentally responsible healthcare solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $32.1 Billion |

| Forecast Value | $67.5 Billion |

| CAGR | 7.9% |

In 2024, the rigid formats segment held a 42.4% share. Bottles, glass containers, and jars are widely used for premium and prescription skin treatments as they offer protection, preserve product quality, and support storage stability. These containers are particularly favored for their ability to handle viscous formulations and maintain structural integrity for sensitive applications.

The liquid product segment is forecasted to grow at a CAGR of 7.9% from 2025 to 2034. Liquids, including antiseptics and medicated sprays, demand precise, secure packaging that prevents spills and contamination while supporting active ingredient preservation and dosing accuracy.

North America Topical Drugs Packaging Market held 37.6% share in 2024 and is set to grow at a CAGR of 6.9% throughout 2025-2034. Strong pharmaceutical infrastructure, a preference for OTC medication, and growing self-care habits are advancing packaging innovation in this region. Increased reliance on e-commerce and user-friendly packaging that ensures safety and compliance continues to shape the demand landscape in the US and Canada.

Leading companies in Topical Drugs Packaging Market include West Pharmaceutical Services, Schott, AptarGroup, Gerresheimer, and Amcor. Topical drug packaging companies are investing heavily in sustainable materials, digital security, and advanced dispensing systems to cater to the evolving needs of both consumers and pharmaceutical clients. Brands are innovating with refillable containers, biodegradable packaging films, and low-carbon manufacturing to align with environmental regulations and consumer preferences. Product differentiation is being enhanced through tamper-proof closures, ergonomic design, and serialization technologies that add traceability and consumer confidence. Companies are also forming strategic partnerships with pharmaceutical manufacturers to co-develop packaging formats tailored to specialized dermatological products.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Packaging type trends

- 2.2.2 Packaging material trends

- 2.2.3 Product types trends

- 2.2.4 Drug type trends

- 2.2.5 Closure type trends

- 2.2.6 Mode of administration trends

- 2.2.7 Application trends

- 2.2.8 Regional trends

- 2.3 TAM Analysis, 2025-2034 (USD Million)

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of skin diseases and dermatological disorders

- 3.2.1.2 Growing demand for convenient and user-friendly packaging formats

- 3.2.1.3 Expansion of over-the-counter (OTC) topical drug products

- 3.2.1.4 Growth of e-commerce and direct-to-consumer pharmaceutical sales

- 3.2.1.5 Innovation in unit dose and controlled-dispensing systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory compliance and approval processes

- 3.2.2.2 Complexities in designing child-resistant yet senior-friendly packaging

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with underserved dermatological needs.

- 3.2.3.2 Integration of smart packaging technologies for authentication and patient engagement.

- 3.2.3.3 Rising investment in sustainable and biodegradable packaging solutions.

- 3.2.3.4 Growth of private-label topical product lines by retail pharmacy chains.

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 Historical price analysis (2021-2024)

- 3.8.2 Price trend drivers

- 3.8.3 Regional price variations

- 3.8.4 Price Forecast (2025-2034)

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Sustainability measures

- 3.12.1 Sustainable materials assessment

- 3.12.2 Carbon footprint analysis

- 3.12.3 Circular economy implementation

- 3.12.4 Sustainability certifications and standards

- 3.12.5 Sustainability ROI Analysis

- 3.13 Global consumer sentiment analysis

- 3.14 Patent analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Flexible packaging

- 5.3 Rigid packaging

- 5.4 Semi-rigid packaging

Chapter 6 Market Estimates and Forecast, By Packaging Material, 2021 - 2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Plastic

- 6.3 Glass

- 6.4 Metal

- 6.5 Paper

- 6.6 Aluminium

- 6.7 Others

Chapter 7 Market Estimates and Forecast, By Product Types, 2021 - 2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Bottles

- 7.3 Caps & closures

- 7.4 Inhalers

- 7.5 Tubes

- 7.6 Jars

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Drug Type, 2021 - 2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 Liquid

- 8.3 Semi-solid

- 8.4 Solid

- 8.5 Transdermal

Chapter 9 Market Estimates and Forecast, By Closure Type, 2021 - 2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 Screw cap

- 9.3 Flip-top cap

- 9.4 Pump dispenser

- 9.5 Dropper

- 9.6 Nozzle

Chapter 10 Market Estimates and Forecast, By Mode of Administration, 2021 - 2034 (USD Million & Kilo Tons)

- 10.1 Key trends

- 10.2 Ophthalmic usage

- 10.3 Nasal usage

- 10.4 Dermal usage

Chapter 11 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Kilo Tons)

- 11.1 Key trends

- 11.2 Dermatology

- 11.3 Ophthalmology

- 11.4 Others

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Kilo Tons)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Italy

- 12.3.5 Spain

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 MEA

- 12.6.1 South Africa

- 12.6.2 Saudi Arabia

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Global Key Players

- 13.1.1 Amcor

- 13.1.2 AptarGroup

- 13.1.3 Gerresheimer

- 13.1.4 Schott

- 13.1.5 West Pharmaceutical Services

- 13.2 Regional Key Players

- 13.2.1 North America

- 13.2.1.1 Catalent

- 13.2.1.2 WestRock

- 13.2.1.3 Sonoco Products

- 13.2.1.4 ProAmpac

- 13.2.1.5 Silgan Holdings

- 13.2.2 Europe

- 13.2.2.1 Bormioli Pharma

- 13.2.2.2 Constantia Flexibles

- 13.2.2.3 Mondi

- 13.2.2.4 SGD Pharma

- 13.2.3 APAC

- 13.2.3.1 Huhtamaki

- 13.2.3.2 Nipro

- 13.2.3.3 EPL Limited

- 13.2.1 North America

- 13.3 Niche Players / Disruptors

- 13.3.1 CCL Industries

- 13.3.2 LOG Pharma Primary Packaging

- 13.3.3 Nelipak

合约开发和生产组织 (CDMO) 市场分析及至 2035 年预测:按类型、产品、服务、技术、应用、最终用户、材料类型、阶段、工艺和实施类型划分

合约开发和生产组织 (CDMO) 市场分析及至 2035 年预测:按类型、产品、服务、技术、应用、最终用户、材料类型、阶段、工艺和实施类型划分 抗体合约开发和生产组织 (CDMO) 市场规模、份额和趋势分析报告:按产品、服务、原材料、工作流程、治疗领域、最终用途、地区和细分市场预测 (2025-2033)小分子创新 API CDMO 市场分析与预测(至 2034 年):类型、产品、服务、技术、应用、形式、材料类型、流程、最终用户、阶段生物製剂合约开发和生产组织 (CDMO) 市场规模、份额和趋势分析报告:按产品、服务、原材料来源、工作流程、治疗领域、最终用途和地区分類的细分市场预测(2025-2033 年)

抗体合约开发和生产组织 (CDMO) 市场规模、份额和趋势分析报告:按产品、服务、原材料、工作流程、治疗领域、最终用途、地区和细分市场预测 (2025-2033)小分子创新 API CDMO 市场分析与预测(至 2034 年):类型、产品、服务、技术、应用、形式、材料类型、流程、最终用户、阶段生物製剂合约开发和生产组织 (CDMO) 市场规模、份额和趋势分析报告:按产品、服务、原材料来源、工作流程、治疗领域、最终用途和地区分類的细分市场预测(2025-2033 年) 生技药品开发和受託製造厂商市场按服务类型、表现系统、治疗类别、开发阶段和最终用户划分 - 全球预测 2025-2032美国活性药物原料药CDMO 市场:市场规模、份额、趋势分析(按产品、合成、药物、应用和工作流程)、细分市场预测(2025-2033 年)全球活性药物成分CDMO市场:市场规模、份额和趋势分析(按产品、合成、药物、应用、工作流程和地区划分),细分市场预测(2025-2033年)美国临床实验CDMO 市场规模、份额和趋势分析报告:按服务、最终用途和细分市场预测,2025 年至 2033 年全球临床实验药物CDMO市场:市场规模、份额和趋势分析(按服务、最终用途和地区划分),细分市场预测(2025-2033年)电子化学品 CDMO 和 CRO 市场(按服务类型、化学品类别、化学品类型、应用和最终用途行业)- 2025-2030 年全球预测

生技药品开发和受託製造厂商市场按服务类型、表现系统、治疗类别、开发阶段和最终用户划分 - 全球预测 2025-2032美国活性药物原料药CDMO 市场:市场规模、份额、趋势分析(按产品、合成、药物、应用和工作流程)、细分市场预测(2025-2033 年)全球活性药物成分CDMO市场:市场规模、份额和趋势分析(按产品、合成、药物、应用、工作流程和地区划分),细分市场预测(2025-2033年)美国临床实验CDMO 市场规模、份额和趋势分析报告:按服务、最终用途和细分市场预测,2025 年至 2033 年全球临床实验药物CDMO市场:市场规模、份额和趋势分析(按服务、最终用途和地区划分),细分市场预测(2025-2033年)电子化学品 CDMO 和 CRO 市场(按服务类型、化学品类别、化学品类型、应用和最终用途行业)- 2025-2030 年全球预测