|

市场调查报告书

商品编码

1797724

数位乳房 X 光摄影市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Digital Mammography Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

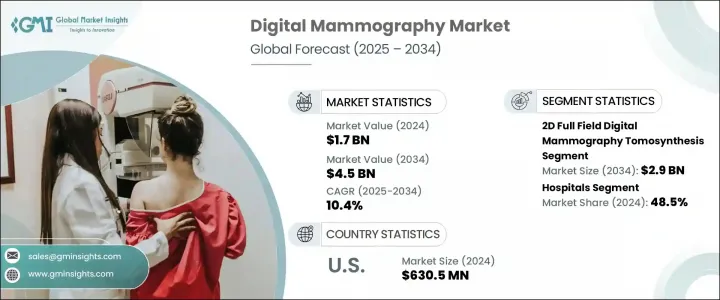

2024 年全球数位乳房 X 光摄影市场价值 17 亿美元,预计到 2034 年将以 10.4% 的复合年增长率增长至 45 亿美元。受全球乳癌发病率上升、早期发现意识增强、政府积极倡议以及影像技术进步的推动,该市场正在快速成长。数位乳房 X 光摄影使医疗保健提供者能够捕捉乳房组织的高解析度影像,有助于乳癌的早期发现和诊断。此技术广泛应用于医院、诊断中心和专科诊所等临床环境。该领域的领先公司包括 GE 医疗、Hologic、西门子医疗、富士胶片控股和荷兰皇家飞利浦电子公司。市场主要专注于全视野数位乳房 X 光摄影 (FFDM) 和 3D 断层合成系统等设备,这些设备可提高诊断准确性、减少辐射暴露并改善患者预后。

由于政府支持的筛检计画和影像技术的持续进步,数位化和人工智慧乳房钼靶X光检查系统的普及率显着提升。随着医疗保健行业日益重视以患者为中心的诊疗,数位化乳房钼靶X光检查因其更高的影像精度、更少的诊断错误以及更高的患者舒适度而成为首选。此外,乳癌发生率的上升凸显了早期精准检测以改善临床疗效的必要性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 17亿美元 |

| 预测值 | 45亿美元 |

| 复合年增长率 | 10.4% |

2024年,二维全视野数位乳房断层摄影(2D Full-field Digital Molecular X-ray, DTMS)市场价值11亿美元,预计复合年增长率为10.2%,到2034年将达到29亿美元。该技术是乳癌诊断不可或缺的一部分,它提供高解析度数位影像,帮助放射科医生检测细微异常,例如微钙化和小肿块。整合影像解决方案、人工智慧驱动的诊断和全面的乳癌筛检计划的使用日益增多,正在促进该领域的成长。影像清晰度的提高有助于发现早期乳癌,从而提高成功干预的几率并改善患者预后。

2024年,医院领域占了48.5%的市场。医院领域占最大份额,得益于其先进的影像基础设施以及在乳癌筛检和诊断中发挥关键作用的熟练放射科医生。医院是乳癌治疗的核心,这推动了对多模式影像系统和人工智慧整合数位乳房钼靶X光摄影的需求。此外,新兴市场(尤其是亚太、中东和非洲等地区)医疗基础设施的发展,正在加速先进乳房钼靶X光摄影技术在医院环境中的应用,包括二维和三维断层合成系统。

2024年,美国数位乳房X光检查市场规模达6.305亿美元,其成长主要源自于美国乳癌发生率的上升。随着对早期精准乳癌检测的需求不断增长,对数位乳房X光检查等先进诊断工具的需求也日益增长。这一趋势极大地促进了美国市场的成长。

数位乳房 X 光摄影市场的主要参与者包括西门子医疗、通用电气医疗、荷兰皇家飞利浦、富士胶片控股和豪洛捷。为了巩固市场地位,数位乳房 X 光摄影产业的公司正专注于几项关键策略。一种方法是不断创新影像技术,例如将人工智慧 (AI) 整合到乳房 X 光摄影系统中,以提高诊断准确性和速度。另一项策略是与医疗保健提供者和组织建立合作伙伴关係,以扩大其产品和服务的覆盖范围。许多公司也正在投资开发更用户友好、以患者为中心的解决方案,以减少筛检过程中的不适感,这是患者日益关注的问题。此外,公司正致力于透过瞄准新兴市场来扩大市场份额,特别是在医疗基础设施快速发展的地区。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球乳癌发生率不断上升

- 对早期乳癌检测的认识不断提高

- 政府措施和筛选项目不断增加

- 数位乳房X光检查的技术进步

- 产业陷阱与挑战

- 设备和维护成本高

- 辐射暴露问题

- 市场机会

- 人工智慧预测监控工具和人工智慧整合的采用率不断上升

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 技术进步

- 当前的技术趋势

- 新兴技术

- 供应链分析

- 未来市场趋势

- 定价分析

- 依产品类型

- 专利分析

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 二维全视野数位化乳房断层摄影

- 3D全视野数位化乳房断层摄影

第六章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 专科诊所

- 诊断中心

第七章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第八章:公司简介

- Allengers

- Canon

- Carestream

- Fujifilm Holdings

- GE Healthcare

- Genoray

- Hologic

- IDETEC Medical Imaging

- IMS Giotto

- Koninklijke Philips

- Planmed

- Siemens Healthineers

- SINO MDT

- SternMed

- Trivitron Healthcare

- Vannin Healthcare

The Global Digital Mammography Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 10.4% to reach USD 4.5 billion by 2034. This market is growing rapidly, driven by the increasing incidence of breast cancer worldwide, heightened awareness about early detection, proactive government initiatives, and advancements in imaging technology. Digital mammography allows healthcare providers to capture high-resolution images of breast tissue, which aids in early detection and diagnosis of breast cancer. This technology is widely used in clinical environments such as hospitals, diagnostic centers, and specialty clinics. Leading companies in the sector include GE Healthcare, Hologic, Siemens Healthineers, Fujifilm Holdings, and Koninklijke Philips. The market primarily focuses on devices such as full-field digital mammography (FFDM) and 3D tomosynthesis systems, which improve diagnostic accuracy, reduce radiation exposure, and enhance patient outcomes.

The adoption of digital and AI-powered mammography systems has seen a significant rise, aided by government-supported screening programs and continuous advancements in imaging technology. With a growing emphasis on patient-centered care in the healthcare industry, digital mammography is becoming the preferred choice due to its higher image accuracy, reduced diagnostic errors, and enhanced patient comfort. Additionally, the rising prevalence of breast cancer underscores the need for early and accurate detection to improve clinical outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 10.4% |

In 2024, 2D full-field digital mammography tomosynthesis segment was valued at USD 1.1 billion and is expected to grow at a CAGR of 10.2%, to reach USD 2.9 billion by 2034. This technology is integral to breast cancer diagnosis, providing high-resolution digital images that help radiologists detect subtle abnormalities such as microcalcifications and small masses. The increased use of integrated imaging solutions, AI-driven diagnostics, and comprehensive breast cancer screening programs is contributing to the growth of this segment. Enhanced clarity of images helps detect early-stage breast cancer, improving the chances of successful intervention and patient outcomes.

The hospitals segment held 48.5% share in 2024. The hospital segment holds the largest share due to its advanced imaging infrastructure and the presence of skilled radiologists who play a vital role in breast cancer screening and diagnosis. Hospitals are central to breast cancer treatment, which drives the demand for multimodal imaging systems and AI-integrated digital mammography. Furthermore, the development of healthcare infrastructure in emerging markets, especially in regions like Asia-Pacific, the Middle East, and Africa, is accelerating the adoption of advanced mammography technologies within hospital settings, including both 2D and 3D tomosynthesis systems.

U.S. Digital Mammography Market was valued at USD 630.5 million in 2024, with growth largely driven by the increasing prevalence of breast cancer in the country. As the demand for early and accurate breast cancer detection rises, the need for advanced diagnostic tools like digital mammography is growing. This trend significantly contributes to the market's expansion in the U.S.

The key players in the Digital Mammography Market include Siemens Healthineers, GE Healthcare, Koninklijke Philips, Fujifilm Holdings, and Hologic. To strengthen their market position, companies in the digital mammography industry are focusing on a few key strategies. One approach is the continuous innovation of imaging technologies, such as the integration of artificial intelligence (AI) into mammography systems to enhance diagnostic accuracy and speed. Another strategy involves forming partnerships with healthcare providers and organizations to expand the reach of their products and services. Many companies are also investing in developing more user-friendly, patient-centric solutions that reduce discomfort during screenings, which is a growing concern for patients. Additionally, companies are working on expanding their market share by targeting emerging markets, particularly in regions where healthcare infrastructure is rapidly developing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence of breast cancer across the globe

- 3.2.1.2 Growing awareness regarding early breast cancer detection

- 3.2.1.3 Rising government initiatives and screening programs

- 3.2.1.4 Technological advancements in digital mammography

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of equipment and maintenance

- 3.2.2.2 Radiation exposure concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of AI-powered predictive monitoring tools and AI integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Future market trends

- 3.8 Pricing analysis

- 3.8.1 By product type

- 3.9 Patent analysis

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 2D full field digital mammography tomosynthesis

- 5.3 3D full field digital mammography tomosynthesis

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Specialty clinics

- 6.4 Diagnostic centers

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Allengers

- 8.2 Canon

- 8.3 Carestream

- 8.4 Fujifilm Holdings

- 8.5 GE Healthcare

- 8.6 Genoray

- 8.7 Hologic

- 8.8 IDETEC Medical Imaging

- 8.9 IMS Giotto

- 8.10 Koninklijke Philips

- 8.11 Planmed

- 8.12 Siemens Healthineers

- 8.13 SINO MDT

- 8.14 SternMed

- 8.15 Trivitron Healthcare

- 8.16 Vannin Healthcare