|

市场调查报告书

商品编码

1797736

机器人作业系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Robot Operating System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

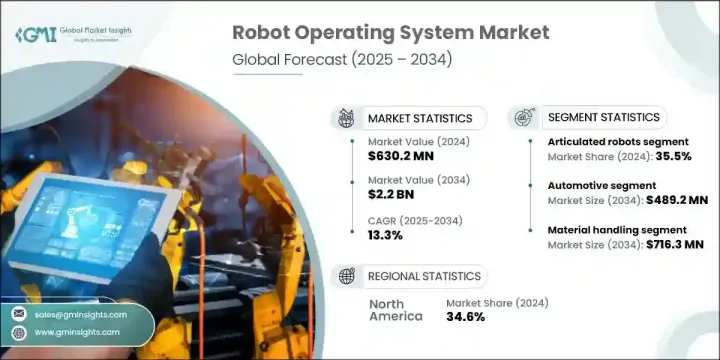

2024 年全球机器人作业系统市场规模达 6.302 亿美元,预计到 2034 年将以 13.3% 的复合年增长率成长,达到 22 亿美元。推动这一成长的主要因素包括:各行各业协作机器人和移动机器人的部署日益增多、物流和仓储自动化程度不断提高,以及与工业 4.0 相关的智慧製造系统投资不断增加。随着机器人技术成为製造业、医疗保健和物流等领域不可或缺的一部分,对 ROS 等灵活平台的需求也随之激增。这些系统能够无缝整合物联网、人工智慧和巨量资料,从而促进即时监控、预测性维护和智慧生产工作流程。因此,企业正在利用 ROS 扩大机器人计画的规模,以适应不断发展的自动化目标,从而提高多个垂直领域的营运敏捷性和效率。

协作机器人 (cobot) 和自主移动机器人的普及是市场扩张的主要动力。这些类型的机器人支援物料搬运、生产协作和物流运营等领域的自适应自动化。电子商务的快速发展加速了订单处理和仓库履行领域对复杂机器人的需求。同时,与产业数位化相关的倡议正在将机器人技术与人工智慧和感测器网路相结合,以实现动态、智慧的工厂环境。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 6.302亿美元 |

| 预测值 | 22亿美元 |

| 复合年增长率 | 13.3% |

2024年,关节型机器人占最大份额,达35.5%。关节型机器人以其强大的工作范围、高负载能力和灵活性而闻名,广泛应用于各种工业环境中的组装、焊接、喷漆和搬运任务。当与ROS结合使用时,它们能够提供高度的适应性和成本效益。製造商正在利用人工智慧驱动的视觉工具、力感测器和预测分析技术进行创新,使这些机器人更加智慧、更加模组化,并创建针对不同工业用例量身定制的ROS相容系统。

随着电动车电池生产、焊接流程和检测系统自动化程度的提高,预计到2034年,汽车产业的市场规模将达到4.892亿美元。支援ROS的机器人对于精确的感测器校准、大批量组装和生产线末端测试至关重要。供应商正致力于开发模组化、符合ROS 2标准的机器人解决方案,以满足电动车製造、轻量化物料搬运和多阶段品质控制的需求,以应对全球汽车生产的电气化趋势。

2024年,美国机器人作业系统市场规模达1.92亿美元,这得益于汽车、电子和物流产业的强劲成长。机器人作业系统与云端机器人技术、人工智慧增强协调和智慧仓储的融合,正在推动整个工业营运效率的提升。强大的合作伙伴关係和对行业标准的遵循,推动了美国机器人技术的进步,为其持续扩张奠定了坚实的基础。

塑造机器人作业系统产业的领导者包括发那科、欧姆龙、ABB 有限公司、安川电机和库卡股份公司。 ROS 市场的顶尖企业正专注于 ROS 2 相容解决方案,以确保协作机器人的可扩展性和安全性,从而巩固其市场地位。他们正在投资支援 AI 增强感知和自主导航的模组化机器人平台。与自动化供应商、系统整合商和行业协会建立的策略合作伙伴关係正在加速其在物流和智慧工厂的部署。持续的研发正致力于嵌入式视觉、力感和预测分析,以增强机器人智慧。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 协作机器人和移动机器人在各行各业的快速应用

- 与 ROS 平台整合的 AI 和电脑视觉的进步

- 仓库自动化和物流机器人的需求不断增长

- 智慧製造和工业 4.0 计划的投资不断增加

- 扩大 ROS 在医疗保健和服务机器人领域的应用

- 产业陷阱与挑战

- 初始整合和部署成本高

- 与传统工业系统互通性的复杂性

- 市场机会

- ROS 2 在自动驾驶汽车和 AMR 的应用

- 中小企业对低成本模组化机器人解决方案的需求不断增长

- 向新兴市场和非工业领域扩张

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品

- 定价策略

- 新兴商业模式

- 合规性要求

- 专利和智慧财产权分析

- 地缘政治与贸易动态

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 关键参与者的竞争基准

- 财务绩效比较

- 收入

- 利润率

- 研发

- 产品组合比较

- 产品范围广度

- 科技

- 创新

- 地理位置比较

- 全球足迹分析

- 服务网路覆盖

- 各区域市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 利基市场参与者

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年关键发展

- 併购

- 伙伴关係和合作

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型倡议

- 新兴/新创企业竞争对手格局

第五章:市场估计与预测:按机器人类型,2021 - 2034 年

- 主要趋势

- 关节型机器人

- SCARA机器人

- 笛卡儿/龙门机器人

- Delta/并联机器人

- 协作机器人(Cobots)

- 移动机器人/AMR

- 其他的

第六章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 物料处理

- 测试和品质检验

- 地图和导航

- 库存和仓库管理

- 家庭自动化和安全

- 共同包装和生产线末端包装

- 其他的

第七章:市场估计与预测:按最终用途产业,2021 - 2034 年

- 主要趋势

- 汽车

- 电学

- 医疗保健与生命科学

- 金属和机械

- 食品和饮料

- 仓储和物流

- 塑胶、橡胶和化学品

- 其他的

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Global Key Players

- Regional Key Players

- 利基市场参与者/颠覆者

- Apex.AI

- 移动工业机器人(MiR)

- Husarion sp. z oo

- 艾克德有限公司

- 万德尔博茨有限公司

The Global Robot Operating System Market was valued at USD 630.2 million in 2024 and is estimated to grow at a CAGR of 13.3% to reach USD 2.2 billion by 2034. This growth is being fueled by increasing deployment of collaborative and mobile robots across industries, escalating automation in logistics and warehousing, and rising investment in smart manufacturing systems linked to Industry 4.0. As robotics becomes integral to sectors like manufacturing, healthcare, and logistics, demand for flexible platforms like ROS is surging. These systems enable seamless integration of IoT, AI, and big data to facilitate real-time monitoring, predictive maintenance, and smart production workflows. As a result, businesses are leveraging ROS to scale up robotics initiatives in alignment with evolving automation objectives, improving operational agility and efficiency across multiple verticals.

Adoption of collaborative robots (cobots) and autonomous mobile robots is a major contributor to market expansion. These types of robots support adaptive automation in areas such as material handling, production cooperation, and logistics operations. The sharp uptick in e-commerce has accelerated demand for sophisticated robotics in order processing and warehouse fulfillment. Meanwhile, initiatives tied to industry digitalization are integrating robotics with AI and sensor networks to enable dynamic, intelligent factory settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $630.2 Million |

| Forecast Value | $2.2 Billion |

| CAGR | 13.3% |

In 2024, the articulated robots segment held the largest share at 35.5%. Known for their reach, payload capacity, and flexibility, articulated robots are widely used in assembly, welding, painting, and handling tasks across diverse industrial environments. When paired with ROS, they offer high adaptability and cost efficiency. Manufacturers are innovating with AI-driven vision tools, force sensors, and predictive analytics to make these robots smarter and more modular, creating ROS-compatible systems customized for distinct industrial use cases.

The automotive segment is expected to reach USD 489.2 million by 2034, thanks to increasing automation in EV battery production, welding processes, and inspection systems. ROS-enabled robots are central to precise sensor calibration, high-volume assembly, and end-of-line testing. Suppliers are focusing on developing modular, ROS 2-compliant robotics solutions tailored to electric vehicle manufacturing, lightweight material handling, and multi-stage quality control, addressing the electrification trend in global automotive production.

U.S. Robot Operating System Market generated USD 192 million in 2024, driven by solid uptake in automotive, electronics, and logistics sectors. The convergence of ROS with cloud robotics, AI-enhanced coordination, and smart warehousing is driving efficiency gains across industrial operations. U.S.-based robotics initiatives are boosted by strong partnerships and compliance with industry standards, providing a solid base for continued expansion.

Leading organizations shaping the Robot Operating System Industry include Fanuc, Omron Corporation, ABB Ltd., Yaskawa Electric Corporation, and KUKA AG. Top players in the ROS market are strengthening their foothold by focusing on ROS 2 compatible solutions, ensuring scalability and security in collaborative robotics. They're investing in modular robotic platforms that support AI-enhanced perception and autonomous navigation. Strategic partnerships with automation vendors, system integrators, and industry associations are accelerating deployment in logistics and smart factories. Continuous R&D is being channeled toward embedded vision, force sensing, and predictive analytics to enhance robot intelligence.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Robot type trends

- 2.2.2 Application trends

- 2.2.3 End use industry trends

- 2.2.4 Regional trends

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid adoption of collaborative and mobile robots across industries

- 3.2.1.2 Advancements in AI and computer vision integrated with ROS platforms

- 3.2.1.3 Increasing demand for warehouse automation and logistics robots

- 3.2.1.4 Rising investment in smart manufacturing and Industry 4.0 initiatives

- 3.2.1.5 Expanding use of ROS in healthcare and service robotics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial integration and deployment costs

- 3.2.2.2 Complexity in interoperability with legacy industrial systems

- 3.2.3 Market opportunities

- 3.2.3.1 Adoption of ROS 2 in autonomous vehicles and AMRs

- 3.2.3.2 Growing SME demand for low-cost modular robotic solutions

- 3.2.3.3 Expansion into emerging markets and non-industrial sectors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing strategies

- 3.10 Emerging business models

- 3.11 Compliance requirements

- 3.12 Patent and IP analysis

- 3.13 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Robot Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Articulated robots

- 5.3 SCARA robots

- 5.4 Cartesian/gantry robots

- 5.5 Delta/parallel robots

- 5.6 Collaborative robots (Cobots)

- 5.7 Mobile robots / AMRs

- 5.8 Others

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Material handling

- 6.3 Testing & quality inspection

- 6.4 Mapping & navigation

- 6.5 Inventory & warehouse management

- 6.6 Home automation and safety

- 6.7 Co-packaging & end-of-line packaging

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Electronics & electrical

- 7.4 Healthcare & life sciences

- 7.5 Metal & machinery

- 7.6 Food & beverages

- 7.7 Warehousing & logistics

- 7.8 Plastic, rubber, and chemicals

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Key Players

- 9.1.1 ABB Ltd.

- 9.1.2 Fanuc

- 9.1.3 KUKA AG

- 9.1.4 Microsoft Corporation

- 9.1.5 Yaskawa Electric Corporation

- 9.2 Regional Key Players

- 9.2.1 North America

- 9.2.1.1 iRobot Corporation

- 9.2.1.2 Clearpath Robotics

- 9.2.1.3 Locus Robotics

- 9.2.2 Europe

- 9.2.2.1 Universal Robots (UR)

- 9.2.2.2 Staubli Robotics

- 9.2.2.3 Acceleration Robotics

- 9.2.2.4 Neobotix

- 9.2.3 Asia Pacific

- 9.2.3.1 Denso Corporation

- 9.2.3.2 Kawasaki Heavy Industries

- 9.2.3.3 Omron Corporation

- 9.2.3.4 Seiko Epson Corporation

- 9.2.1 North America

- 9.3 Niche Players / Disruptors

- 9.3.1 Apex.AI

- 9.3.2 Mobile Industrial Robots (MiR)

- 9.3.3 Husarion sp. z o.o.

- 9.3.4 acceed GmbH

- 9.3.5 Wandelbots GmbH

机器人作业系统市场(按机器人类型、组件、最终用户产业和部署模式)—全球预测 2025-2032

机器人作业系统市场(按机器人类型、组件、最终用户产业和部署模式)—全球预测 2025-2032 2025年全球基于ROS的机器人市场报告

2025年全球基于ROS的机器人市场报告 机器人作业系统市场,按机器人类型、按应用、按最终用户、按国家和地区 - 行业分析、市场规模、市场份额及预测(2025 年至 2032 年)行动机械手市场,按类型、按应用、按最终用户、按国家和地区 - 行业分析、市场规模、市场份额及预测(2025 年至 2032 年)

机器人作业系统市场,按机器人类型、按应用、按最终用户、按国家和地区 - 行业分析、市场规模、市场份额及预测(2025 年至 2032 年)行动机械手市场,按类型、按应用、按最终用户、按国家和地区 - 行业分析、市场规模、市场份额及预测(2025 年至 2032 年) 机器人作业系统市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、最终用途、地区和竞争细分,2020-2030 年预测)

机器人作业系统市场-全球产业规模、份额、趋势、机会和预测(按产品、应用、最终用途、地区和竞争细分,2020-2030 年预测) 机器人作业系统:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

机器人作业系统:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 机器人作业系统市场规模、份额、趋势分析报告(按机器人类型、应用、最终用途、地区、细分市场预测,2025 年至 2033 年)

机器人作业系统市场规模、份额、趋势分析报告(按机器人类型、应用、最终用途、地区、细分市场预测,2025 年至 2033 年) 机器人作业系统的全球市场,规模,占有率,趋势,产业分析报告:各机器人类型,各用途,各最终用途,各地区 - 市场预测,2025年~2034年开放原始码组成架构ROS (机器人作业系统)

机器人作业系统的全球市场,规模,占有率,趋势,产业分析报告:各机器人类型,各用途,各最终用途,各地区 - 市场预测,2025年~2034年开放原始码组成架构ROS (机器人作业系统)