|

市场调查报告书

商品编码

1797775

电火花加工机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Electrical Discharge Machine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

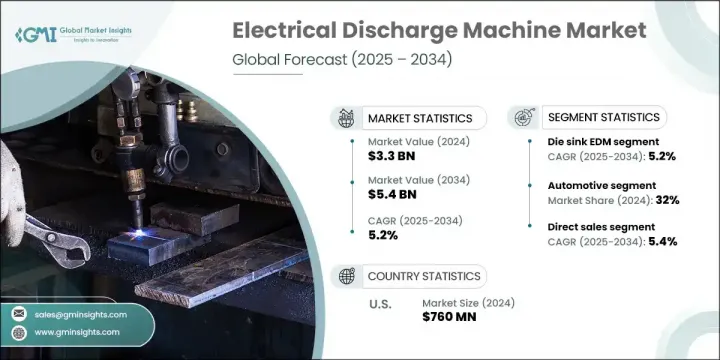

2024 年全球电火花加工工具机市场价值为 33 亿美元,预计到 2034 年将以 5.2% 的复合年增长率成长至 54 亿美元。该市场的成长主要得益于医疗设备、航太和汽车製造等高科技产业对超精密加工日益增长的需求。随着製造业越来越重视尺寸精度、复杂零件几何形状和卓越表面光洁度,电火花加工系统已成为关键解决方案。对高性能涡轮叶片、注塑模具、骨科植入物和精密模具的需求持续成长,使得电火花加工不可或缺。技术进步和智慧系统的整合进一步加速了市场采用,使电火花加工成为先进製造趋势的关键贡献者。随着越来越多地采用传统方法难以加工的复杂合金和材料,电火花加工的非接触式加工作为一种高度可靠和高效的方法脱颖而出。数位转型和自动化加工系统的投资进一步推动了市场发展势头,这些投资有助于优化产量并减少人为错误。

电火花加工系统技术的进步持续提升着各行各业的需求。最新的电火花加工工具机旨在提供更高的精度、更低的电极损耗和更佳的切割速度——这些正是製造商追求成本效益和生产力提升的关键特性。人工智慧控制系统和即时监控功能等连网技术的使用正日益普及,有助于加快决策速度并减少停机时间。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 33亿美元 |

| 预测值 | 54亿美元 |

| 复合年增长率 | 5.2% |

2024年,电火花成型加工系统占据最大市场份额,产值达15亿美元,预计到2034年将以5.2%的复合年增长率成长。该领域凭藉其能够加工极硬且复杂的材料并保持顶级精度的优势,继续保持领先地位。电火花成型加工设备特别适用于加工精细的模腔和复杂的零件几何形状,而这些形状难以透过机械刀具加工。其独特的优势在于能够减少材料浪费,同时提高零件质量,使其在精度至关重要且表面光洁度不容妥协的应用中越来越受欢迎。此外,其环保特性和更低的模具成本有助于在製造营运中推动更广泛的永续发展。

汽车领域在2024年占据了32%的市场份额,预计在2025-2034年期间的复合年增长率将达到5.6%。电火花加工系统在复杂汽车零件的设计和生产中发挥关键作用,尤其是在汽车产业转型为电气化和自动驾驶技术的背景下。使用铝、复合材料和其他难加工材料进行轻量化结构的发展趋势,进一步增强了电火花加工的吸引力。汽车製造商越来越多地采用电火花加工来製造高精度齿轮、动力总成零件和模具,这有助于加快生产进度并保持严格的公差。汽车产业对流程优化和缩短上市时间的关注,可能会使电火花加工的使用率保持上升趋势。

美国电火花加工工具机市场占据77%的市场份额,2024年市场规模达7.6亿美元,这得益于航太、汽车和国防製造业的持续扩张。对复杂零件製造和精密加工解决方案的旺盛需求推动了电火花加工机床的广泛应用。此外,美国正受惠于工业4.0战略的推出,电火花加工机床正被整合到智慧工厂和数位化控制环境中。产业顶尖企业的涌现和不断增加的研发投入进一步增强了该产业的发展动力。政府支持国内生产和先进製造业的政策也增强了该产业的长期前景。

全球电火花加工工具机市场的领导者包括Sparkonix、Fanuc、牧野、ONA EDM、Sodick、三菱电机、AccuteX、Agie、CHMER、Seibu、Zimmer & Kreim、FEOB、Oscar EDM Company、Excetek和GF Machining Solutions。为了巩固市场地位,主要的电火花加工工具机製造商正在投资产品创新,重点是人工智慧驱动的自动化、更高的能源效率和即时性能分析。各企业正与精密工程和航太公司结盟,共同开发符合新兴应用需求的专用电火花加工系统。此外,他们也正在向发展中市场进行策略性扩张,以挖掘汽车和医疗器材产业的新需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按机器类型

- 监管格局

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 贸易统计(HS编码)

- 主要进口国

- 主要出口国

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按机器类型,2021 - 2034 年

- 主要趋势

- 电火花成型机

- 线切割

- 钻孔电火花加工

第六章:市场估计与预测:按工作量,2021 - 2034 年

- 主要趋势

- 低于2000磅

- 2000至4000磅

- 4000至8000磅

- 8000磅以上

第七章:市场估计与预测:按最终用途产业,2021 - 2034 年

- 主要趋势

- 汽车

- 航太和国防

- 电气和电子

- 卫生保健

- 其他(消费品等)

第八章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 直销

- 间接销售

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- AccuteX

- Agie

- CHMER

- Excetek

- Zimmer & Kreim

- FEOB

- Fanuc

- GF Machining Solutions

- Makino

- Mitsubishi Electric

- ONA EDM

- Oscar EDM Company

- Seibu

- Sodick

- Sparkonix

The Global Electrical Discharge Machine Market was valued at USD 3.3 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 5.4 billion by 2034. Growth in this market is primarily driven by rising demand for ultra-precise machining across high-tech industries such as medical devices, aerospace, and automotive manufacturing. As manufacturing sectors increasingly prioritize dimensional accuracy, complex part geometries, and superior surface finishes, EDM systems have emerged as a key solution. The need for high-performance turbine blades, injection molds, orthopedic implants, and precision dies continues to rise, making EDM indispensable. Technological improvements and the integration of smart systems have further accelerated market adoption, positioning EDM as a key contributor to advanced manufacturing trends. With increasing adoption of complex alloys and materials that are hard to machine using traditional methods, EDM's contact-free processing stands out as a highly reliable and efficient approach. Market momentum is further fueled by investments in digital transformation and automated machining systems that help optimize throughput while reducing human error.

The technological evolution of EDM systems continues to elevate demand across industries. The newest EDM machines are designed to offer higher precision, reduced electrode wear, and superior cutting speeds-key features that manufacturers seek for cost efficiency and productivity enhancement. The use of connected technologies such as AI-driven control systems and real-time monitoring features is becoming more common, supporting faster decision-making and reducing downtime.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.3 Billion |

| Forecast Value | $5.4 Billion |

| CAGR | 5.2% |

The Die sink EDM systems segment held the largest market share in 2024, generating USD 1.5 billion and projected to grow at a CAGR of 5.2% through 2034. This segment continues to lead due to its ability to work with extremely hard and complex materials while maintaining top-level precision. Die sinker EDM machines are especially effective for detailed mold cavities and intricate part geometries that are difficult to process using mechanical tools. Their unique capability to reduce material waste while improving component quality makes them increasingly favored in applications where precision is critical and surface finish cannot be compromised. Furthermore, their eco-friendliness and reduced tooling costs contribute to broader sustainability initiatives within manufacturing operations.

The automotive segment held a 32% share in 2024 and is forecasted to grow at a CAGR of 5.6% during 2025-2034. EDM systems play a pivotal role in enabling the design and production of intricate automotive components, especially as the industry shifts toward electrification and autonomous technologies. The push toward lightweight construction using aluminum, composites, and other hard-to-machine materials continues to reinforce EDM's appeal. Automakers are increasingly adopting EDM to manufacture high-precision gears, powertrain components, and mold tools, helping to accelerate production timelines and maintain tight tolerances. The industry's focus on process optimization and time-to-market reductions is likely to keep EDM usage on an upward trend.

United States Electrical Discharge Machine Market held a 77% share and generated USD 760 million in 2024, supported by continued expansion in aerospace, automotive, and defense manufacturing. High demand for complex part fabrication and precision machining solutions has contributed to EDM's wide adoption. Additionally, the U.S. is benefiting from the rollout of Industry 4.0 strategies, with EDM machines integrated into smart factories and digitally controlled environments. The presence of top industry players and increasing R&D initiatives adds further momentum. Government policies supporting domestic production and advanced manufacturing are also enhancing the sector's long-term outlook.

Leading companies operating in the Global Electrical Discharge Machine Market include Sparkonix, Fanuc, Makino, ONA EDM, Sodick, Mitsubishi Electric, AccuteX, Agie, CHMER, Seibu, Zimmer & Kreim, FEOB, Oscar E.D.M. Company, Excetek, and GF Machining Solutions. To strengthen their market presence, major EDM manufacturers are investing in product innovation with a focus on AI-driven automation, improved energy efficiency, and real-time performance analytics. Firms are forming alliances with precision engineering and aerospace companies to co-develop specialized EDM systems that address emerging application needs. Strategic expansion into developing markets is also being pursued to tap new demand from the automotive and medical device industries.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 By regional

- 2.2.2 By machine type

- 2.2.3 By workload

- 2.2.4 By end use industry

- 2.2.5 By distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By machine type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics (HS code)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machine Type, 2021 - 2034 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Die sink EDM

- 5.3 Wire EDM

- 5.4 Hole drilling EDM

Chapter 6 Market Estimates & Forecast, By Workload, 2021 - 2034 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 Below 2000 lbs

- 6.3 2000 to 4000 lbs

- 6.4 4000 to 8000 lbs

- 6.5 Above 8000 lbs

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Aerospace and Defense

- 7.4 Electrical and electronics

- 7.5 Healthcare

- 7.6 Others (consumer goods etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AccuteX

- 10.2 Agie

- 10.3 CHMER

- 10.4 Excetek

- 10.5 Zimmer & Kreim

- 10.6 FEOB

- 10.7 Fanuc

- 10.8 GF Machining Solutions

- 10.9 Makino

- 10.10 Mitsubishi Electric

- 10.11 ONA EDM

- 10.12 Oscar E.D.M. Company

- 10.13 Seibu

- 10.14 Sodick

- 10.15 Sparkonix

电火花加工机(EDM)的全球市场(2025年)- 产品,终端用户,竞争企业:2024年~2030年的分析与预测

电火花加工机(EDM)的全球市场(2025年)- 产品,终端用户,竞争企业:2024年~2030年的分析与预测 电火花加工市场:按类型、组件、切削材料、销售管道、应用和产业划分-2026-2032年全球预测电火花加工丝市场按材料、线径、应用、最终用户和分销管道划分,全球预测(2026-2032年)

电火花加工市场:按类型、组件、切削材料、销售管道、应用和产业划分-2026-2032年全球预测电火花加工丝市场按材料、线径、应用、最终用户和分销管道划分,全球预测(2026-2032年) 电火花加工 (EDM) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、材料类型、最终用户、製程和功能划分

电火花加工 (EDM) 市场分析及预测(至 2035 年):按类型、产品类型、服务、技术、组件、应用、材料类型、最终用户、製程和功能划分 2026年全球电火花线切割放电加工线材市场报告按机器类型、线材和最终用途产业分類的电火花加工线材市场-全球预测,2026-2032年铸铁电火花加工服务市场(按机器类型、最终用户产业、服务类型和应用划分)-全球预测,2026-2032年

2026年全球电火花线切割放电加工线材市场报告按机器类型、线材和最终用途产业分類的电火花加工线材市场-全球预测,2026-2032年铸铁电火花加工服务市场(按机器类型、最终用户产业、服务类型和应用划分)-全球预测,2026-2032年 电火花加工工具机市场规模、份额和趋势分析报告:按工作负载、工具机类型、最终用途、地区和细分市场预测(2025-2033 年)

电火花加工工具机市场规模、份额和趋势分析报告:按工作负载、工具机类型、最终用途、地区和细分市场预测(2025-2033 年) 电火花加工 (EDM) 市场:未来预测(2025-2030 年)

电火花加工 (EDM) 市场:未来预测(2025-2030 年) 电火花加工机市场,按产品类型、按服务类型、按应用、按最终用途、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

电火花加工机市场,按产品类型、按服务类型、按应用、按最终用途、按国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测