|

市场调查报告书

商品编码

1797781

小型运载火箭 (SLV) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Small Launch Vehicle (SLV) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

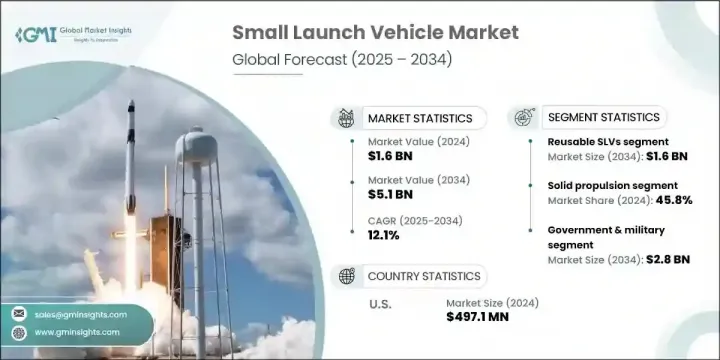

2024 年全球小型运载火箭市场规模达 16 亿美元,预计到 2034 年将以 12.1% 的复合年增长率成长,达到 51 亿美元。该市场扩张的主要动力来自航太商业化的不断推进以及向低成本、更灵活的发射解决方案的转变。随着私人实体深入参与卫星部署、分析和天基服务,该产业正经历创新、可负担性和服务客製化的快速转变。不断发展的商业航太格局催生了电信、地球成像和物联网系统等领域更专业化的商业模式,进一步刺激了小型运载火箭的需求。从共享发射有效载荷到客製化发射计画和客製化轨道交付的转变,推动了对响应迅速且针对特定任务的运载火箭设计的需求。

随着对更快部署週期和更高发射频率的需求日益增长,营运商必须打造低成本、适应性强的系统,以支援快速週转和更强大的任务控制。随着商业和政府航太任务越来越重视按需进入轨道,对可扩展、模组化发射解决方案的需求变得至关重要。营运商正在转向精益製造、增材製造方法和简化的设计架构,以缩短开发时间并简化整合流程。这些灵活的系统旨在适应各种有效载荷,同时支援在最后一刻调整轨道参数,这对于对地观测、国防通讯和灾难响应等时间敏感的应用至关重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 16亿美元 |

| 预测值 | 51亿美元 |

| 复合年增长率 | 12.1% |

2024年,固体推进系统市场以45.8%的市占率领先市场。固体推进系统凭藉其可靠性、易于整合和储存优势,仍然是快速反应、亚轨道和国防相关任务的首选。新进入者倾向于采用固体基运载火箭(SLV),以最大限度地降低设计复杂性并简化发射准备。供应商将固体燃料运载火箭定位于策略性用例,在这些用例中,简单性和可靠性是首要考虑因素。

可重复使用发射系统正日益被采用,以降低单次发射成本并缩短週转时间。预计到2034年,可重复使用运载火箭(SLV)市场规模将达16亿美元。许多参与者正专注于可重复使用性,开发用于回收、翻新和重新发射的可扩展硬体。事实证明,这些技术对于减少浪费、降低营运成本以及支援频繁轨道存取的长期环境和经济永续性至关重要。

2024年,北美小型运载火箭 (SLV) 市场占据34.6%的市场份额,预计到2034年将以11.1%的复合年增长率成长。凭藉雄厚的资金支持、日益加强的政府与私营部门合作,以及由小型卫星製造商和营运商组成的强大生态系统,该地区在全球SLV产业中处于领先地位。为了满足国家安全和商业需求,该地区正大幅转向更快速、更灵活的发射方式。

影响全球小型运载火箭 (SLV) 市场的关键参与者包括 C6 Launch、Astra Space、Agnikul Cosmos、Interstellar Technologies、Galactic Energy、Firefly 航太、CAS Space、ABL Space Systems、HyImpulse 和 Dawn 航太。活跃于小型运载火箭市场的公司正在加强在创新、可重复使用性和特定任务配置方面的力度。许多公司正在投资模组化发射系统和可重复使用的阶段开发,以提供具有成本效益和频繁的部署週期。与卫星製造商和航太机构的策略合作有助于扩大客户范围并增强信誉。越来越多的公司也专注于垂直整合,控制从零件製造到发射后资料服务的每个步骤,确保品质、降低成本并加快产品上市时间。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 对小型卫星和卫星星座的需求不断增长

- 太空商业化程度不断提高

- 对经济高效且专用的发射服务的需求

- 国防和国家安全应用的成长

- 低成本发射基础设施的扩展

- 产业陷阱与挑战

- 新进入者的开发和发布成本高昂

- SLV的酬载容量限制

- 市场机会

- 基于星座的卫星部署需求激增

- 新兴航太国家越来越多地采用SLV

- 整合可重复使用科技以提高成本效率

- 扩展按需和快速启动服务

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 科技与创新格局

- 当前的技术趋势

- 新兴技术

- 新兴商业模式

- 合规性要求

- 国防预算分析

- 全球国防开支趋势

- 区域国防预算分配

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 重点国防现代化项目

- 预算预测(2025-2034)

- 对产业成长的影响

- 各国国防预算

- 供应链弹性

- 地缘政治分析

- 劳动力分析

- 数位转型

- 合併、收购和策略伙伴关係格局

- 风险评估与管理

- 主要合约授予(2021-2024)

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 关键参与者的竞争基准

- 财务绩效比较

- 收入

- 利润率

- 研发

- 产品组合比较

- 产品范围广度

- 科技

- 创新

- 地理位置比较

- 全球足迹分析

- 服务网路覆盖

- 各区域市场渗透率

- 竞争定位矩阵

- 领导者

- 挑战者

- 追踪者

- 利基市场参与者

- 战略展望矩阵

- 财务绩效比较

- 2021-2024 年关键发展

- 併购

- 伙伴关係和合作

- 技术进步

- 扩张和投资策略

- 永续发展倡议

- 数位转型倡议

- 新兴/新创企业竞争对手格局

第五章:市场估计与预测:按推进类型,2021 - 2034 年

- 主要趋势

- 固体推进

- 液态推进

- 混合动力推进

第六章:市场估计与预测:按产能,2021 - 2034 年

- 主要趋势

- 最多 100 公斤

- 100-500公斤

- 500-1000公斤

- 1000 -2000公斤

第七章:市场估计与预测:依可重复使用性,2021 - 2034 年

- 主要趋势

- 可重复使用的 SLV

- 不可重复使用的 SLV

第八章:市场估计与预测:按发布平台,2021 - 2034 年

- 主要趋势

- 陆基

- 海基

- 空基

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 政府与军队

- 国防机构

- 民用航太机构

- 国家安全组织

- 公共研究机构和大学

- 其他的

- 商业的

- 卫星营运商

- 太空新创公司和技术演示者

- 其他的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Global Key Players

- Regional Key Players

- 利基市场参与者/颠覆者

- 黎明航太

- 银河能量

The Global Small Launch Vehicle Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 12.1% to reach USD 5.1 billion by 2034. Expansion in this market is largely driven by the increasing commercialization of space and a shift toward lower-cost and more agile launch solutions. As private entities deepen their involvement in satellite deployment, analytics, and space-based services, the industry is witnessing rapid shifts in innovation, affordability, and service customization. This evolving commercial space landscape is giving rise to more specialized business models across telecommunications, Earth imaging, and IoT-enabled systems, further fueling SLV demand. The shift from shared launch payloads to tailored schedules and customized orbital delivery is pushing the need for responsive and mission-specific vehicle design.

Growing demand for faster deployment cycles and greater launch frequency is compelling operators to create low-cost, adaptable systems that support rapid turnaround and increased mission control. As commercial and governmental space missions increasingly prioritize on-demand access to orbit, the need for scalable, modular launch solutions has become critical. Operators are shifting toward lean manufacturing, additive production methods, and simplified design architectures to reduce development timelines and streamline integration. These agile systems are built to accommodate a wide variety of payloads while enabling last-minute adjustments to orbital parameters, which is essential for time-sensitive applications such as Earth observation, defense communication, and disaster response.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $5.1 Billion |

| CAGR | 12.1% |

The solid propulsion segment led the market in 2024 with a 45.8% share. Solid propulsion systems remain a preferred choice for rapid-response, suborbital, and defense-related missions due to their reliability, ease of integration, and storage benefits. New entrants are leaning on solid-based SLVs to minimize design complexity and streamline launch readiness. Providers are positioning solid-fueled vehicles for strategic use cases where simplicity and dependability are top priorities.

The reusable launch systems are increasingly being adopted to cut per-launch expenses and increase turnaround times. The reusable SLV segment is projected to reach USD 1.6 billion by 2034. Many players are focusing on reusability by developing scalable hardware for recovery, refurbishment, and relaunch. These technologies are proving essential in reducing waste, lowering operational costs, and supporting long-term environmental and economic sustainability for frequent orbital access.

North America Small Launch Vehicle (SLV) Market held 34.6% share in 2024 and is projected to grow at a CAGR of 11.1% through 2034. With strong financial backing, increasing government-private sector collaboration, and a robust ecosystem of small satellite manufacturers and operators, the region is at the forefront of the global SLV industry. There's a marked shift toward faster, more flexible launch options catering to national security and commercial demands alike.

Key players shaping the Global Small Launch Vehicle (SLV) Market include C6 Launch, Astra Space, Agnikul Cosmos, Interstellar Technologies, Galactic Energy, Firefly Aerospace, CAS Space, ABL Space Systems, HyImpulse, and Dawn Aerospace. Companies active in the small launch vehicle market are intensifying their efforts around innovation, reusability, and mission-specific configurations. Many are investing in modular launch systems and reusable stage development to offer cost-effective and frequent deployment cycles. Strategic collaborations with satellite manufacturers and space agencies help extend their client reach and bolster credibility. A growing number of firms are also focusing on vertical integration, controlling every step from component fabrication to post-launch data services, ensuring quality, reducing costs, and speeding up time-to-market.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Propulsion type trends

- 2.2.2 Capacity trends

- 2.2.3 Reusability trends

- 2.2.4 Launch platform trends

- 2.2.5 End use trends

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for small satellites and satellite constellations

- 3.2.1.2 Increasing commercialization of space

- 3.2.1.3 Demand for cost-effective and dedicated launch services

- 3.2.1.4 Growth in defense and national security applications

- 3.2.1.5 Expansion of low-cost launch infrastructure

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High development and launch costs for new entrants

- 3.2.2.2 Payload capacity limitations of SLVs

- 3.2.3 Market opportunities

- 3.2.3.1 Surge in demand for constellation-based satellite deployments

- 3.2.3.2 Growing adoption of SLVs in emerging space nations

- 3.2.3.3 Integration of reusable technologies to enhance cost efficiency

- 3.2.3.4 Expansion of on-demand and rapid launch services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Emerging business models

- 3.9 Compliance requirements

- 3.10 Defense budget analysis

- 3.11 Global defense spending trends

- 3.12 Regional defense budget allocation

- 3.12.1 North America

- 3.12.2 Europe

- 3.12.3 Asia Pacific

- 3.12.4 Middle East and Africa

- 3.12.5 Latin America

- 3.13 Key defense modernization programs

- 3.14 Budget forecast (2025-2034)

- 3.14.1 Impact on industry growth

- 3.14.2 Defense budgets by country

- 3.15 Supply chain resilience

- 3.16 Geopolitical analysis

- 3.17 Workforce analysis

- 3.18 Digital transformation

- 3.19 Mergers, acquisitions, and strategic partnerships landscape

- 3.20 Risk assessment and management

- 3.21 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.5 Strategic outlook matrix

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2021-2024

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Sustainability initiatives

- 4.4.6 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Propulsion Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Solid propulsion

- 5.3 Liquid propulsion

- 5.4 Hybrid propulsion

Chapter 6 Market Estimates and Forecast, By Capacity, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Upto 100 kg

- 6.3 100-500 kg

- 6.4 500-1000 kg

- 6.5 1000 -2000 kg

Chapter 7 Market Estimates and Forecast, By Reusability, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Reusable SLVs

- 7.3 Non-reusable SLVs

Chapter 8 Market Estimates and Forecast, By Launch Platform, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Land-based

- 8.3 Sea-based

- 8.4 Air-based

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.1.1 Government & Military

- 9.1.2 Defense agencies

- 9.1.3 Civil space agencies

- 9.1.4 National security organizations

- 9.1.5 Public research institutions & universities

- 9.1.6 Others

- 9.2 Commercial

- 9.2.1 Satellite operators

- 9.2.2 Space startups & technology demonstrators

- 9.2.3 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 Rocket Lab

- 11.1.2 Virgin

- 11.1.3 Relativity Space

- 11.1.4 Firefly Aerospace

- 11.1.5 Isar Aerospace

- 11.2 Regional Key Players

- 11.2.1 North America

- 11.2.1.1 ABL Space Systems

- 11.2.1.2 Astra Space

- 11.2.1.3 X-Bow Systems

- 11.2.2 Europe

- 11.2.2.1 Rocket Factory Augsburg

- 11.2.2.2 Orbex

- 11.2.2.3 Skyrora Limited

- 11.2.2.4 HyImpulse

- 11.2.2.5 PLD Space

- 11.2.3 APAC

- 11.2.3.1 Agnikul Cosmos

- 11.2.3.2 Skyroot Aerospace

- 11.2.3.3 CAS Space

- 11.2.3.4 Interstellar Technologies

- 11.2.1 North America

- 11.3 Niche Players / Disruptors

- 11.3.1 Dawn Aerospace

- 11.3.2 Galactic Energy

北京建源科技有限公司(太空时代):竞争分析

北京建源科技有限公司(太空时代):竞争分析 全球卫星运载火箭市场规模、份额、趋势和成长分析报告(2026-2034年)北京大航跃迁科技有限公司(Cosmoleap)竞争格局分析

全球卫星运载火箭市场规模、份额、趋势和成长分析报告(2026-2034年)北京大航跃迁科技有限公司(Cosmoleap)竞争格局分析 卫星运载火箭市场-全球产业规模、份额、趋势、机会及预测(依轨道类型、应用类型、运载火箭类型、地区及竞争格局划分,2021-2031年)中国航太科工火箭技术有限公司(原中国航太科工火箭技术有限公司)竞争格局分析中国长征火箭股份有限公司(中国火箭公司):竞争格局分析北京天兵科技有限公司/太空先锋(SSPI)竞争分析

卫星运载火箭市场-全球产业规模、份额、趋势、机会及预测(依轨道类型、应用类型、运载火箭类型、地区及竞争格局划分,2021-2031年)中国航太科工火箭技术有限公司(原中国航太科工火箭技术有限公司)竞争格局分析中国长征火箭股份有限公司(中国火箭公司):竞争格局分析北京天兵科技有限公司/太空先锋(SSPI)竞争分析 上海航太技术研究院(SAST)竞争分析

上海航太技术研究院(SAST)竞争分析 中国运载火箭技术研究院(CALT)竞争格局分析

中国运载火箭技术研究院(CALT)竞争格局分析 海南国际商业航太发射中心(海信航太)竞争格局分析

海南国际商业航太发射中心(海信航太)竞争格局分析