|

市场调查报告书

商品编码

1797799

量子通讯市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Quantum Communications Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

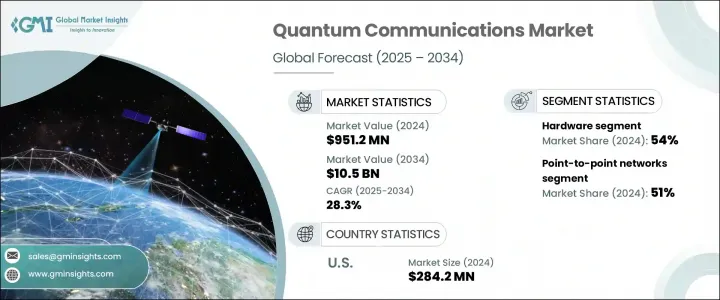

2024 年全球量子通讯市场价值为 9.512 亿美元,预计到 2034 年将以 28.3% 的复合年增长率成长,达到 105 亿美元。人们对网路安全日益增长的担忧以及对高度安全的资料传输系统日益增长的需求,在该市场的快速扩张中发挥着至关重要的作用。世界各国政府都在策略性地投资量子技术的发展,特别注重建立强大的量子通讯网路。各国正在启动国家计画并拨出大量资金来加强研究基础设施,以建构面向未来的量子通讯系统。这些全球性努力旨在保护关键基础设施和敏感资料,并希望在公共和私营部门部署先进的量子解决方案。

量子通讯技术,尤其是量子金钥分发 (QKD),因其能够检测窃听行为并确保资讯安全传输,从而提供高水准的资料安全性,正日益受到关注。网路威胁事件的增多,以及政府机构和企业保护敏感通讯的压力日益增大,正促使量子解决方案得到更广泛的应用。国防、金融和电信等关键产业对量子通讯的需求日益旺盛,这些产业的安全资料传输至关重要。在这些领域,量子技术正被部署到面向未来的基础设施中,并在日益严苛的数位环境中保持资料完整性。卫星量子网路的普及和光纤系统的演进,正在为市场成长创造额外的动力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 9.512亿美元 |

| 预测值 | 105亿美元 |

| 复合年增长率 | 28.3% |

就组件而言,硬体在2024年占据全球量子通讯市场的最大份额,约占整个市场的54%。预计该细分市场在预测期内的复合年增长率将超过26%。该领域的成长主要归功于专用设备的开发和部署,包括光子源、侦测器和其他对确保量子金钥分发可靠性至关重要的关键元件。这些组件对于需要最高保密性的行动尤其有价值,例如情报服务、安全金融交易和政府通讯。

根据网路类型,点对点网路在2024年占据了51%的市场份额,预计到2034年将以超过27%的复合年增长率成长。这种网路模式被认为是短距离通讯的最佳选择,通常在100公里半径内,因此非常适合办公室间或城市内的通讯需求。此设计确保了高保真度并最大限度地减少了资料遗失,使机构能够自信地进行安全的资料交换。光纤技术的进步也有助于减少传输损耗并提高金钥产生机制的可靠性。这些发展对于确保量子通讯系统的稳定性和运作效率至关重要。

从最终用途来看,政府和国防部门正在成为量子通讯市场成长最快的领域之一。国家级量子基础设施和安全通讯骨干网路的投资正成为优先事项,以防御网路战并保护敏感资讯安全。各国政府越来越依赖量子通讯来加强国家安全,确保其关键行动免受潜在网路攻击的影响。

从地区来看,美国引领北美量子通讯市场,占据约82%的地区份额,2024年创造了2.842亿美元的收入。联邦政府的倡议以及能源部(DOE)、国家科学基金会(NSF)和国防部(DoD)等主要机构的资金投入不断增加,正在推动美国的技术进步和商业部署。投资的激增使美国成为量子研发的主要枢纽,促进了公共和私营部门的创新。

量子通讯产业的领先公司包括东芝、泰雷兹、QuantumCTek、MagiQ Technologies、Arqit Quantum、Qubitekk、Aliro Quantum、ID Quantique、KETS Quantum Security 和 Quintessence Labs。这些公司正在为量子金钥分发、安全网路和下一代加密技术领域的尖端解决方案的开发做出贡献,在塑造全球安全通讯的未来方面发挥关键作用。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 对资料安全的担忧日益加剧

- 量子网路的技术进步

- 关键产业的采用率不断提高

- 政府措施和资金

- 产业陷阱与挑战

- 实施成本高且基础设施复杂

- 没有量子中继器,范围和网路可扩展性有限

- 市场机会

- 与传统通讯基础设施集成

- 量子通讯卫星的发展

- 关键领域的安全通信

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 案例研究

- 用例

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 量子金钥分发(QKD)设备

- 量子中继器

- 单光子侦测器

- 量子储存设备

- 软体

- 量子网路管理

- 加密金钥管理

- 安全协议软体

- 服务

- 咨询与整合

- 支援与维护

- 培训与教育

第六章:市场估计与预测:按网络,2021 - 2034 年

- 主要趋势

- 点对点网络

- 点对多点网络

- 网状网路

- 卫星网路

- 混合网路

第七章:市场估计与预测:按部署模式,2021 - 2034 年

- 主要趋势

- 本地

- 基于云端

- 杂交种

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 政府和国防

- 银行、金融服务和保险(BFSI)

- 医疗保健和生命科学

- 电信

- 能源和公用事业

- 研究与学术

- 企业和商业

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

- 以色列

第十章:公司简介

- 成熟玩家

- Cisco

- Huawei Technologies

- ID Quantique

- Mitsubishi

- NEC

- Nokia

- Toshiba

- 专营公司

- MagiQ Technologies,

- Quantum Communications Hub

- Quantum Xchange

- QuantumCTek Co.

- QuantumCTek Europe

- Qubitekk

- QuintessenceLabs

- SeQure Quantum

- 电信和基础设施公司

- AT&T

- BT Group

- China Telecom

- Deutsche Telekom

- Verizon

- Vodafone

- 硬体製造商

- Aurea Technology

- Excelitas Technologies

- Newport Corp.

- Photon Spot

- Single Quantum

The Global Quantum Communications Market was valued at USD 951.2 million in 2024 and is estimated to grow at a CAGR of 28.3% to reach USD 10.5 billion by 2034. Growing concerns about cybersecurity and the increasing need for highly secure data transfer systems are playing a crucial role in the rapid expansion of this market. Governments across the globe are strategically investing in the development of quantum technologies, with a particular focus on creating robust quantum communication networks. Countries are launching national initiatives and allocating substantial funds to enhance research infrastructure to build future-ready quantum communication systems. These global efforts are aimed at safeguarding critical infrastructure and sensitive data, with a vision of deploying advanced quantum solutions across both public and private sectors.

Quantum communication technologies, especially quantum key distribution (QKD), are gaining traction as they offer high-level data security by detecting eavesdropping attempts and ensuring safe transmission of information. Rising incidents of cyber threats and increased pressure on government agencies and enterprises to protect sensitive communications are encouraging broader adoption of quantum solutions. The market is witnessing high demand from key industries such as defense, finance, and telecom, where secure data transmission is a priority. In these sectors, quantum technologies are being deployed to future-proof infrastructure and maintain data integrity in increasingly hostile digital environments. The adoption of satellite-based quantum networks and the evolution of fiber-based systems are creating additional momentum for market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $951.2 Million |

| Forecast Value | $10.5 Billion |

| CAGR | 28.3% |

In terms of components, hardware accounted for the largest share of the global quantum communications market in 2024, representing around 54% of the total market. This segment is anticipated to grow at a CAGR of over 26% during the forecast period. Growth in this area is largely attributed to the development and deployment of specialized equipment, including photon sources, detectors, and other critical elements that are essential to ensure the reliability of quantum key distribution. These components are particularly valuable for operations that demand maximum confidentiality, such as intelligence services, secure financial transactions, and government communications.

Based on network type, the point-to-point networks segment held a dominant 51% market share in 2024 and is projected to grow at a CAGR exceeding 27% through 2034. This network model is considered optimal for short-distance communication, typically within a 100-kilometer radius, making it suitable for inter-office or intra-city communication needs. The design ensures high fidelity and minimizes data loss, allowing institutions to confidently perform secure data exchange. Advances in fiber optic technologies are also helping reduce transmission losses and enhance the reliability of key generation mechanisms. These developments are critical in ensuring the stability and operational efficiency of quantum communication systems.

On the basis of end use, the government and defense segment is emerging as one of the fastest-growing sectors in the quantum communications market. Investments in national-level quantum infrastructure and secure communication backbones are being prioritized to defend against cyber warfare and secure sensitive information. Governments are increasingly relying on quantum communication to bolster national security, ensuring their critical operations remain insulated from potential cyber breaches.

Regionally, the United States led the North American quantum communications market, capturing approximately 82% of the regional share and generating USD 284.2 million in revenue in 2024. Federal initiatives and increased funding from key agencies such as the Department of Energy (DOE), National Science Foundation (NSF), and Department of Defense (DoD) are driving technological advancements and commercial deployment across the country. This surge in investment has positioned the US as a major hub for quantum R&D, fostering innovation across both the public and private sectors.

Leading companies in the quantum communications industry include Toshiba, Thales, QuantumCTek, MagiQ Technologies, Arqit Quantum, Qubitekk, Aliro Quantum, ID Quantique, KETS Quantum Security, and Quintessence Labs. These firms are contributing to the development of cutting-edge solutions in quantum key distribution, secure networking, and next-gen encryption technologies, playing a key role in shaping the future of secure global communications.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Network type

- 2.2.4 Deployment mode

- 2.2.5 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising concerns over data security

- 3.2.1.2 Technological advancements in quantum networks

- 3.2.1.3 Increasing adoption across critical industries

- 3.2.1.4 Government initiatives and funding

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation costs and infrastructure complexity

- 3.2.2.2 Limited range and network scalability without quantum repeaters

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with classical communication infrastructure

- 3.2.3.2 Development of quantum communication satellites

- 3.2.3.3 Secure communication for critical sectors

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Case studies

- 3.9 Use cases

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million, Units)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Quantum key distribution (QKD) devices

- 5.2.2 Quantum repeaters

- 5.2.3 Single photon detectors

- 5.2.4 Quantum memory devices

- 5.3 Software

- 5.3.1 Quantum network management

- 5.3.2 Cryptographic key management

- 5.3.3 Security protocol software

- 5.4 Services

- 5.4.1 Consulting & integration

- 5.4.2 Support & maintenance

- 5.4.3 Training & education

Chapter 6 Market Estimates & Forecast, By Network, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Point-to-point networks

- 6.3 Point-to-multipoint networks

- 6.4 Mesh networks

- 6.5 Satellite-based networks

- 6.6 Hybrid networks

Chapter 7 Market Estimates & Forecast, By Deployment mode, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud-based

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Million, Units)

- 8.1 Key trends

- 8.2 Government and defense

- 8.3 Banking, financial services & insurance (BFSI)

- 8.4 Healthcare and life sciences

- 8.5 Telecommunications

- 8.6 Energy and utilities

- 8.7 Research and academia

- 8.8 Enterprise and commercial

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

- 9.6.4 Israel

Chapter 10 Company Profiles

- 10.1 Established players

- 10.1.1 Cisco

- 10.1.2 Huawei Technologies

- 10.1.3 ID Quantique

- 10.1.4 Mitsubishi

- 10.1.5 NEC

- 10.1.6 Nokia

- 10.1.7 Toshiba

- 10.2 Pure-play companies

- 10.2.1 MagiQ Technologies,

- 10.2.2 Quantum Communications Hub

- 10.2.3 Quantum Xchange

- 10.2.4 QuantumCTek Co.

- 10.2.5 QuantumCTek Europe

- 10.2.6 Qubitekk

- 10.2.7 QuintessenceLabs

- 10.2.8 SeQure Quantum

- 10.3 Telecom and infrastructure companies

- 10.3.1 AT&T

- 10.3.2 BT Group

- 10.3.3 China Telecom

- 10.3.4 Deutsche Telekom

- 10.3.5 Verizon

- 10.3.6 Vodafone

- 10.4 Hardware manufacturer

- 10.4.1 Aurea Technology

- 10.4.2 Excelitas Technologies

- 10.4.3 Newport Corp.

- 10.4.4 Photon Spot

- 10.4.5 Single Quantum

量子安全通讯晶片市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户及功能划分

量子安全通讯晶片市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户及功能划分 全球量子技术市场规模、份额、趋势和成长分析报告(2026-2034)

全球量子技术市场规模、份额、趋势和成长分析报告(2026-2034) 量子网路安全解决方案市场:2026-2032年全球预测(按解决方案类型、部署模式、传输介质、组织规模和应用划分)高速随机数晶片市场:按类型、应用、最终用户和销售管道,全球预测(2026-2032年)

量子网路安全解决方案市场:2026-2032年全球预测(按解决方案类型、部署模式、传输介质、组织规模和应用划分)高速随机数晶片市场:按类型、应用、最终用户和销售管道,全球预测(2026-2032年) 2025年全球卫星量子互联网市场报告

2025年全球卫星量子互联网市场报告 量子技术的全球市场(2026年~2046年)

量子技术的全球市场(2026年~2046年) 量子电子感测设备市场预测(至 2032 年):按类型、部署平台、公司规模、技术、应用、最终用户和地区进行的全球分析

量子电子感测设备市场预测(至 2032 年):按类型、部署平台、公司规模、技术、应用、最终用户和地区进行的全球分析 量子技术市场 (2025~2035年):运算·通讯·成像·保全·感测·建模·模拟

量子技术市场 (2025~2035年):运算·通讯·成像·保全·感测·建模·模拟 印度的量子通讯的发展:International Quantum Communication Conclave 2025的考察:政府、学术界和产业界携手合作,利用量子金钥分发 (QKD)、光量子通讯 (PQC) 和光子晶片等本土技术,为印度的量子未来铺路2032 年量子技术市场预测:按组件类型、投资类型、技术类型、应用、最终用户和地区进行的全球分析

印度的量子通讯的发展:International Quantum Communication Conclave 2025的考察:政府、学术界和产业界携手合作,利用量子金钥分发 (QKD)、光量子通讯 (PQC) 和光子晶片等本土技术,为印度的量子未来铺路2032 年量子技术市场预测:按组件类型、投资类型、技术类型、应用、最终用户和地区进行的全球分析