|

市场调查报告书

商品编码

1797845

AMI 瓦斯表市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测AMI Gas Meter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

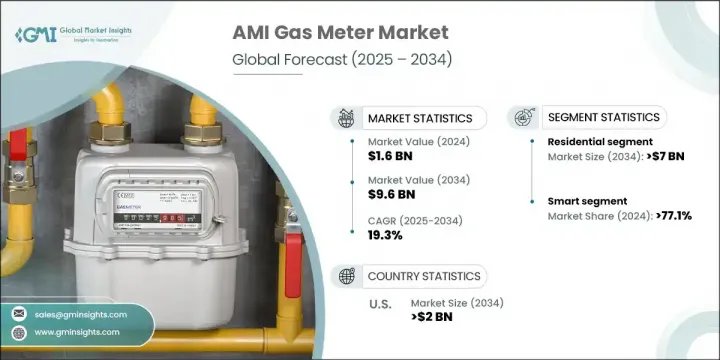

2024年,全球先进计量基础设施 (AMI) 瓦斯表市场规模达16亿美元,预计到2034年将以19.3%的复合年增长率成长,达到96亿美元。受新兴技术、不断变化的监管规定以及对智慧能源管理系统日益增长的需求的推动,该市场正在经历快速转型。先进计量基础设施 (AMI) 燃气表支援即时能耗追踪、远端监控和双向通信,与传统计量系统相比,显着提升了营运能力。

不断增长的需求与全球在节能减排和转型为智慧城市基础设施方面的努力密切相关。各国正在升级其公用事业框架,以减少能源浪费并实现永续发展目标。物联网技术的融入,透过实现远端诊断和预测分析,正在彻底改变AMI燃气表。这种智慧连接提高了系统效率,减少了服务中断,并提供了更准确的计费。公用事业提供者可以透过改善资产管理并最大限度地减少停机时间,从这些升级中受益。随着客户寻求更高的能源使用透明度,并受到能够促进更高效能耗控制的工具的激励,AMI燃气表在工业、商业和住宅环境中的日益普及,这继续加速了市场发展势头。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 16亿美元 |

| 预测值 | 96亿美元 |

| 复合年增长率 | 19.3% |

随着终端用户领域需求的成长,预计到 2034 年,住宅市场规模将达到 70 亿美元。这一增长主要得益于旨在提高家庭能源效率的现代化基础设施政策和措施。随着 AMI 瓦斯表在家庭中的普及率不断提高,监测用量、检测异常并及时提供洞察的能力已成为住宅市场成长的关键驱动力。按应用领域(包括住宅、商业和公用事业)进行细分,凸显了 AMI 解决方案如何根据不同的营运需求进行客製化。

智慧电錶市场在2024年占据了77.1%的市场份额,预计到2034年将以19%的复合年增长率成长。这一增长源于政府不断加大的压力,要求用能够提供双向资料交换、增强客户控制并符合环境法规的数位智慧电錶取代过时的类比系统。大众对节能和智慧解决方案的理解不断加深,也推动了关键地区的智慧电錶应用。

预计到2034年,美国AMI瓦斯表市场规模将达到20亿美元,这得益于强劲的基础建设和成熟能源公司的布局。技术进步、严格的能源法规以及对智慧公用事业项目的大量投资,为市场奠定了坚实的基础。美国持续扩大其在能源创新领域的布局,石油和天然气等领域的大型专案进一步推动了智慧燃气表系统的发展。由于全球15%的清洁能源支出集中在美国,美国在智慧燃气基础建设中发挥重要作用。

引领 AMI 瓦斯表市场的领先公司包括施耐德电气、Aclara Technologies、Landis+Gyr、Itron 和霍尼韦尔国际。 AMI 瓦斯表市场的主要参与者致力于透过技术创新、策略联盟和全球扩张来扩大其市场份额。各公司正大力投资研发,以开发具有增强连接性、资料分析和自我诊断功能的燃气表。与公用事业供应商和智慧电网专案的合作有助于推动大规模部署。各公司也与电信和物联网公司建立合作伙伴关係,以增强即时资料通讯能力。在地化策略,包括针对特定区域的产品设计和法规遵从性,进一步支持了新兴市场的扩张。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 原物料供应情况

- 影响价值链的因素

- 中断

- 监管格局

- 进出口贸易分析

- 各地区价格趋势分析(美元/单位)

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

- 新兴机会和趋势

- 数位化和物联网集成

- 新兴市场渗透

- 投资分析及未来展望

第四章:竞争格局

- 介绍

- 公司市占率(按地区)

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 策略倡议

- 竞争性基准描述

- 策略仪表板

- 创新与技术格局

第五章:市场规模及预测:依应用,2021 - 2034

- 主要趋势

- 住宅

- 商业的

- 公用事业

第六章:市场规模及预测:依类型,2021 - 2034

- 主要趋势

- 基本的

- 聪明的

第七章:市场规模及预测:依地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 瑞典

- 义大利

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 中东和非洲

- 阿联酋

- 沙乌地阿拉伯

- 南非

- 埃及

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

第八章:公司简介

- Aclara Technologies

- Ameresco

- Apator

- Azbil Kimmon

- Chint Group

- Core & Main

- Diehl Stiftung & Co. KG

- Holly technology

- Honeywell International

- Itron

- Landis+Gyr

- Neptune Technology Group

- Osaki Electric

- Raychem RPG

- Schneider Electric

- Sensus

- Siemens

- Waltero

- Wasion Group

- Zenner International

The Global AMI Gas Meter Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 19.3% to reach USD 9.6 billion by 2034. The market is undergoing rapid transformation, powered by emerging technologies, evolving regulatory mandates, and the surging need for intelligent energy management systems. Advanced metering infrastructure (AMI) gas meters enable real-time consumption tracking, remote monitoring, and two-way communication, which significantly enhance operational capabilities compared to conventional metering systems.

The expanding demand is strongly linked to global efforts around energy conservation and the transition to smart urban infrastructure. Countries are upgrading their utility frameworks to cut energy waste and meet sustainability goals. The incorporation of IoT technologies is revolutionizing AMI gas meters by enabling remote diagnostics and predictive analytics. This smart connectivity enhances system efficiency, reduces service interruptions, and delivers more accurate billing. Utility providers benefit from these upgrades by improving asset management and minimizing downtime. The growing acceptance of AMI gas meters across industrial, commercial, and residential environments continues to accelerate market momentum, as customers seek greater transparency in their energy usage and are motivated by tools that promote better consumption control.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $9.6 Billion |

| CAGR | 19.3% |

With demand rising across end-use segments, the residential sector is forecasted to reach USD 7 billion by 2034. This surge is being driven by modern infrastructure policies and initiatives aimed at increasing energy efficiency in households. As AMI gas meter adoption grows in homes, the ability to monitor consumption, detect anomalies, and provide timely insights has become a key driver of residential market growth. Segmentation by application-including residential, commercial, and utility sectors-highlights how AMI solutions are being tailored to meet different operational needs.

The smart meter segment held 77.1% share in 2024 and is expected to grow at a CAGR of 19% through 2034. This growth stems from increased government pressure to replace outdated analog systems with digital smart meters capable of providing two-way data exchange, enhancing customer control, and meeting environmental regulations. Enhanced public understanding around energy savings and smart solutions is also bolstering adoption across key regions.

U.S. AMI Gas Meter Market is projected to reach USD 2 billion by 2034, supported by robust infrastructure development and the presence of well-established energy companies. Technological advancement, strict energy regulations, and heavy investment in smart utility projects contribute to the market's solid foundation. The country continues to expand its footprint in energy innovation, with large-scale projects across sectors like oil and gas reinforcing the push for smart gas metering systems. With 15% of global clean energy spending concentrated in the U.S., the country plays a significant role in the advancement of smart gas infrastructure.

Leading companies steering the AMI Gas Meter Market include Schneider Electric, Aclara Technologies, Landis+Gyr, Itron, and Honeywell International. Major players in the AMI Gas Meter Market are focused on expanding their market presence through technological innovation, strategic alliances, and global expansion. Companies are investing heavily in R&D to develop meters with enhanced connectivity, data analytics, and self-diagnostic capabilities. Collaborations with utility providers and smart grid projects help boost deployment at scale. Firms are also forming partnerships with telecom and IoT companies to strengthen real-time data communication capabilities. Localization strategies, including region-specific product design and regulatory compliance, further support expansion in emerging markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material availability landscape

- 3.1.2 Factors affecting the value chain

- 3.1.3 Disruptions

- 3.2 Regulatory landscape

- 3.3 Import/Export trade analysis

- 3.4 Price trend analysis, by region (USD/Unit)

- 3.5 Industry impact forces

- 3.5.1 Growth drivers

- 3.5.2 Industry pitfalls & challenges

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

- 3.9 Emerging opportunities & trends

- 3.9.1 Digitalization & IoT integration

- 3.9.2 Emerging market penetration

- 3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic initiatives

- 4.4 Competitive benchmarking depictions

- 4.5 Strategy dashboard

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 (USD Million & '000 Units)

- 5.1 Key trends

- 5.2 Residential

- 5.3 Commercial

- 5.4 Utility

Chapter 6 Market Size and Forecast, By Type, 2021 - 2034 (USD Million & '000 Units)

- 6.1 Key trends

- 6.2 Basic

- 6.3 Smart

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & '000 Units)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Sweden

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 UAE

- 7.5.2 Saudi Arabia

- 7.5.3 South Africa

- 7.5.4 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

- 7.6.3 Argentina

Chapter 8 Company Profiles

- 8.1 Aclara Technologies

- 8.2 Ameresco

- 8.3 Apator

- 8.4 Azbil Kimmon

- 8.5 Chint Group

- 8.6 Core & Main

- 8.7 Diehl Stiftung & Co. KG

- 8.8 Holly technology

- 8.9 Honeywell International

- 8.10 Itron

- 8.11 Landis+Gyr

- 8.12 Neptune Technology Group

- 8.13 Osaki Electric

- 8.14 Raychem RPG

- 8.15 Schneider Electric

- 8.16 Sensus

- 8.17 Siemens

- 8.18 Waltero

- 8.19 Wasion Group

- 8.20 Zenner International

旋转式燃气表市场:2026-2032年全球市场预测(按应用、最终用户、功能、仪表类型、压力等级、流量、安装方式和精度等级划分)涡轮燃气表市场:2026-2032年全球市场预测(按应用、最终用途、技术类型、安装方式和通路划分)

旋转式燃气表市场:2026-2032年全球市场预测(按应用、最终用户、功能、仪表类型、压力等级、流量、安装方式和精度等级划分)涡轮燃气表市场:2026-2032年全球市场预测(按应用、最终用途、技术类型、安装方式和通路划分) 2026年全球旋转式燃气表市场报告2026年全球燃气表市场报告

2026年全球旋转式燃气表市场报告2026年全球燃气表市场报告 燃气表市场机会、成长要素、产业趋势分析及预测(2026年至2035年)

燃气表市场机会、成长要素、产业趋势分析及预测(2026年至2035年) 全球湿式气体流量计市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考量、未来预测(2026-2034)

全球湿式气体流量计市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考量、未来预测(2026-2034) 瓦斯表市场 - 全球产业规模、份额、趋势、机会和预测(按技术、应用、类型、地区和竞争格局划分,2021-2031 年预测)

瓦斯表市场 - 全球产业规模、份额、趋势、机会和预测(按技术、应用、类型、地区和竞争格局划分,2021-2031 年预测) 燃气表市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测

燃气表市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测 燃气表:全球市场占有率和排名、总销售量和需求预测(2025-2031年)

燃气表:全球市场占有率和排名、总销售量和需求预测(2025-2031年) AMI燃气表的全球市场

AMI燃气表的全球市场