|

市场调查报告书

商品编码

1797847

智慧植入物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Smart Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

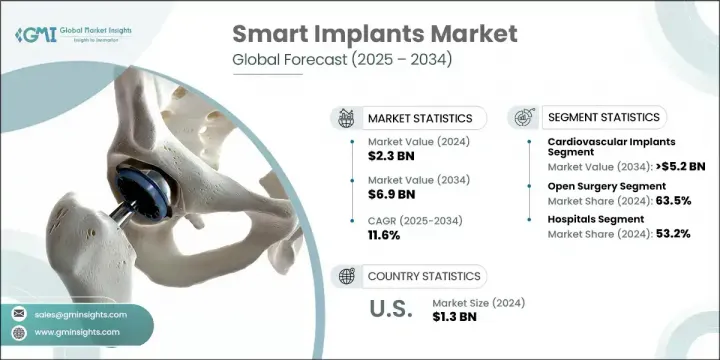

2024 年全球智慧植入物市场规模达 23 亿美元,预计到 2034 年将以 11.6% 的复合年增长率成长至 69 亿美元。心血管疾病盛行率上升、智慧医疗技术快速发展以及对即时患者监测设备需求不断增长等因素共同推动了这一市场的大幅扩张。智慧植入物不仅提供治疗支持,还能收集即时生理资料,帮助诊断和优化治疗方案,在现代医学中发挥变革性作用。随着医疗体系转向个人化和主动护理,这些技术的发展势头强劲。随着全球老龄化人口的成长以及一些已开发经济体可支配收入的提高,市场对能够适应各种健康状况、技术先进的植入物的需求稳步增长。骨科手术的持续成长、神经刺激设备的广泛应用以及对下一代植入物研发活动投资的不断增加,也加速了多个临床领域的成长。

2024年,心血管植入物市场占78.1%的市占率。这一主导地位得益于对起搏系统、可植入式监视器和其他植入式设备的广泛需求,这些设备旨在管理日益增多的心臟病患者。随着这些智慧型心臟设备的治疗和诊断能力不断提升,它们的部署速度也越来越快,能够帮助医生即时了解患者的健康状况,并制定更有针对性的治疗策略。大量患有慢性心血管疾病的患者是推动其发展的因素之一,而植入物功能的不断进步也不断增强其在日常心臟病学实践中的临床价值。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 23亿美元 |

| 预测值 | 69亿美元 |

| 复合年增长率 | 11.6% |

2024年,开放手术占据63.5%的市场份额,预计未来几年将保持稳定成长。在需要增强解剖可视性和精准度的手术中,尤其是在复杂的心血管和骨科手术中,这种手术方法仍然是首选。开放性手术也广泛应用于创伤护理以及微创技术应用有限的地区。骨科和神经内科的外科医生通常更青睐开放性手术,因为它可靠,尤其是在治疗患有多种合併症或解剖学挑战的患者时。

美国智慧植入物市场规模在2024年达到13亿美元,预计2034年将以11.5%的复合年增长率成长。该地区的成长得益于其强大的医疗基础设施、活跃的研发活动以及门诊和门诊手术中心日益增多的外科手术量。随着患者越来越倾向于缩短住院时间和当天即可完成手术,智慧植入设备的采用率正在飙升。此外,神经系统和心血管疾病的发生率不断上升,也持续推动了对能够提供持续监测和标靶治疗的先进植入技术的需求。

智慧植入物市场的主要参与者包括 NeuroPace、波士顿科学、DirectSync Surgical、Zimmer Biomet、Intelligent Implants、Biotronik、雅培和美敦力。这些公司正透过技术创新和以患者为中心的产品设计,积极推动产业发展方向。智慧植入物市场的公司正在实施以产品创新、临床验证和市场渗透为重点的策略性倡议,以增强竞争优势。领先的公司正在大力投资研发,以设计整合人工智慧、无线通讯和感测器技术的设备,用于即时健康追踪。与学术机构和研究机构的合作有助于加速针对特定疾病的植入物的开发。为了扩大地理覆盖范围,公司正在建立策略分销合作伙伴关係,并扩大关键地区的製造能力。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 即时健康监测需求激增

- 心血管疾病发生率不断上升

- 事故和运动伤害数量上升

- 智慧植入物的技术进步

- 产业陷阱与挑战

- 严格的监管框架

- 植入物成本高昂

- 市场机会

- 微创手术日益受到青睐

- 越来越关注能量收集和无电池植入物的开发

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 不同植体类型的价格趋势

- 未来市场趋势

- 网路安全在智慧植入物中的作用

- 比较分析:智慧植入物与传统植入物

- 消费者行为分析

- 报销场景

- 波特的分析

- PESTEL分析

- 差距分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 世界其他地区 (RoW)

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按植入物类型,2021 - 2034 年

- 主要趋势

- 心血管植入物

- 骨科植入物

- 神经刺激植入物

第六章:市场估计与预测:按手术,2021 - 2034 年

- 主要趋势

- 开放性手术

- 微创手术

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 心臟护理中心

- 门诊手术中心

- 其他最终用途

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Abbott

- Biotronik

- Boston Scientific

- DirectSync Surgical

- Intelligent Implants

- Medtronic

- NeuroPace

- Zimmer Biomet

The Global Smart Implants Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 11.6% to reach USD 6.9 billion by 2034. This significant expansion is being propelled by a combination of rising cardiovascular disease prevalence, rapid advancements in smart medical technology, and increasing demand for devices that offer real-time patient monitoring. Smart implants play a transformative role in modern medicine by not only offering therapeutic support but also collecting real-time physiological data that aids in diagnosis and treatment optimization. These technologies are gaining momentum as healthcare systems shift toward personalized and proactive care. With the global aging population growing and disposable income rising in several developed economies, the market is experiencing a steady increase in demand for technologically advanced implants that can adapt to various health conditions. The consistent increase in orthopedic surgeries, expanding adoption of neurostimulation devices, and growing investment in R&D activities for next-generation implantable devices are also accelerating growth across multiple clinical segments.

In 2024, the cardiovascular implants segment held 78.1% share. This dominance is fueled by the widespread need for pacing systems, insertable monitors, and other implantable devices aimed at managing the increasing number of individuals with cardiac conditions. These smart cardiac devices are being deployed at a higher rate as their therapeutic and diagnostic capabilities continue to improve, offering physicians real-time insight into patient health and facilitating more targeted treatment strategies. The large number of patients dealing with chronic cardiovascular disorders is a driving factor, and ongoing advancements in implant functionality continue to strengthen their clinical value in everyday cardiology practice.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $6.9 Billion |

| CAGR | 11.6% |

The open surgery segment held a 63.5% share in 2024 and is projected to maintain steady growth over the coming years. This surgical approach remains the preferred method in cases where enhanced anatomical visibility and precision are critical, especially in complex cardiovascular and orthopedic procedures. Open surgery is also widely used in trauma care and in regions where access to minimally invasive techniques is limited. Surgeons in orthopedic and neurology disciplines often favor open procedures for their reliability, particularly when treating patients with multiple comorbidities or anatomical challenges.

United States Smart Implants Market reached USD 1.3 billion in 2024 and is set to grow at a CAGR of 11.5% through 2034. Growth in this region is fueled by the presence of a robust healthcare infrastructure, high research and development activity, and an increasing volume of surgical procedures conducted in outpatient and ambulatory surgical centers. As patient preference shifts toward shorter hospital stays and same-day surgical interventions, the adoption of intelligent implantable devices is surging. Additionally, the growing prevalence of neurological and cardiovascular conditions continues to increase the demand for advanced implant technologies that offer continuous monitoring and targeted therapy delivery.

Key players in the Smart Implants Market include NeuroPace, Boston Scientific, DirectSync Surgical, Zimmer Biomet, Intelligent Implants, Biotronik, Abbott, and Medtronic. These companies are actively contributing to shaping the direction of the industry through technological innovation and patient-centric product design. Companies operating in the smart implants market are implementing strategic initiatives focused on product innovation, clinical validation, and market penetration to enhance their competitive edge. Leading players are investing heavily in R&D to design devices that integrate AI, wireless communication, and sensor technology for real-time health tracking. Collaborations with academic institutions and research bodies are helping to accelerate the development of implants tailored to specific diseases. To expand their geographic footprint, companies are entering into strategic distribution partnerships and expanding manufacturing capabilities in key regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Implant type trends

- 2.2.3 Surgery trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surging demand for real-time health monitoring

- 3.2.1.2 Growing incidence of cardiovascular disorders

- 3.2.1.3 Rise in number of accidents and sport injuries

- 3.2.1.4 Technological advancements in smart implants

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory framework

- 3.2.2.2 High cost of implants

- 3.2.3 Market opportunities

- 3.2.3.1 Rising preference for minimally invasive surgery

- 3.2.3.2 Growing focus towards development of energy-harvesting and battery-less implants

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends, by implant type

- 3.7 Future market trends

- 3.8 Role of cybersecurity in smart implants

- 3.9 Comparative analysis: Smart vs. conventional implants

- 3.10 Consumer behaviour analysis

- 3.11 Reimbursement scenario

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Rest of the world (RoW)

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Implant Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Cardiovascular implants

- 5.3 Orthopedic implants

- 5.4 Neurostimulation implants

Chapter 6 Market Estimates and Forecast, By Surgery, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Open surgery

- 6.3 Minimally invasive surgery

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Cardiac care centers

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 Biotronik

- 9.3 Boston Scientific

- 9.4 DirectSync Surgical

- 9.5 Intelligent Implants

- 9.6 Medtronic

- 9.7 NeuroPace

- 9.8 Zimmer Biomet