|

市场调查报告书

商品编码

1797888

包裹分类系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Parcel Sorting System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

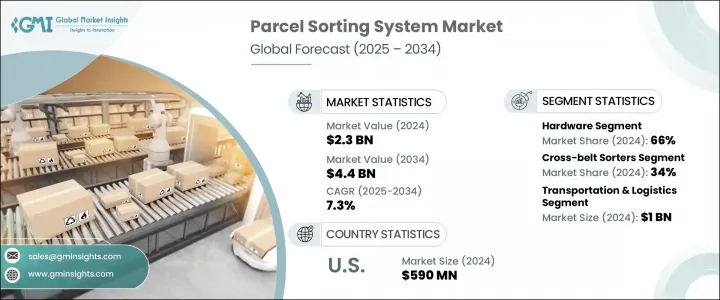

2024 年全球包裹分拣系统市场规模达 23 亿美元,预计到 2034 年将以 7.3% 的复合年增长率成长,达到 44 亿美元。这一稳定成长主要得益于物流和电商领域对更快、更聪明、更具成本效益的解决方案日益增长的需求。随着包裹数量持续增长和客户期望值不断提高,物流业者正在从过时的手动方法转向先进的自动化技术。人工智慧、机器学习和云端平台的整合正在改变分类流程,从而提高速度、减少错误并提升整体营运效率。即时适应性和跨配送中心的无缝处理已成为核心优先事项,使得智慧自动化成为现代包裹处理策略的核心特征。

自动化移动机器人和人工智慧驱动的系统正在缩短处理时间,提升整个物流运作的效率。企业也利用物联网和数位孪生技术实现预测性维护,进而提高设备的正常运作时间和可靠性。性能追踪和主动系统警报方面的创新正在不断推出,以避免营运延误并最大限度地提高吞吐量。这些技术驱动的进步反映了物流自动化如何从辅助任务演变为高度协作的智慧生态系统。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 23亿美元 |

| 预测值 | 44亿美元 |

| 复合年增长率 | 7.3% |

硬体领域在2024年占据了66%的市场份额,预计到2034年将以7%的复合年增长率成长。为了处理不断增长的包裹量,对模组化、可扩展硬体的需求不断增长,这推动了对实体基础设施的大量投资。这些系统专为高速、高精度操作而设计,随着全球订单规模和频率的持续增长,它们对于保持高效的物流性能至关重要。

在各类分类系统中,交叉带式分类系统在2024年的市占率为34%,预计到2034年将以8%的复合年增长率成长。交叉带式分类系统能够精确分类各种形状和尺寸的包裹,同时也能轻柔地处理易碎物品,使其成为高吞吐量物流中心的首选。交叉带式分类系统的多功能性使物流供应商能够处理全球电子商务成长带来的日益多样化的包裹类型,确保长期的适应性。

美国包裹分类系统市场占80%的市场份额,2024年市场规模达5.9亿美元。美国之所以能占据市场领先地位,得益于其积极采用物流自动化技术、建构强大的电商生态系统,以及持续投资智慧仓库基础设施。各大公司正在部署先进的设备以及智慧软体平台,以提高产量、管理分类能力,并优化庞大配送网路中的配送。

全球包裹分拣系统市场的领导者包括伯曼集团 (BEUMER Group)、范德兰德 (Vanderlande)、柯柏 (Korber)、霍尼韦尔智能 (Honeywell Intelligrated)、大福 (Daifuku)、英特诺集团 (Interroll Group) 和德马泰克 (Dematic)。为了巩固市场地位,包裹分拣系统产业的企业正在部署以创新、扩张和协作为重点的策略性倡议。他们正在透过基于人工智慧的自动化、云端整合和即时监控功能来增强产品线。此外,各企业也正在建立全球合作伙伴关係,拓展新兴市场,并投资于下一代技术,例如自主移动机器人 (AMR)、数位孪生和物联网诊断技术。许多公司正在扩展其模组化硬体产品,并为电商、零售和第三方物流客户量身定制解决方案,以确保更广泛的应用。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 原料生产商

- 包裹分类系统製造商

- 技术供应商和开发商

- 系统整合商和顾问

- 分销合作伙伴和通路

- 最终用途

- 成本结构

- 利润率

- 每个阶段的增值

- 影响供应链的因素

- 破坏者

- 供应商格局

- 对部队的影响

- 成长动力

- 电子商务成长和最后一哩配送需求

- 劳动成本上升和劳动力优化需求

- 物流营运中的自动化和人工智慧集成

- 永续性要求和环境法规

- 产业陷阱与挑战

- 高初始资本投资和投资报酬率考虑

- 实施和维护成本高

- 市场机会

- 电子商务推动高阶分类需求

- 对灵活系统进行不同尺寸包裹分类的需求日益增长

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

- 技术与创新格局

- 现有技术

- 新兴技术

- 专利分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 价格趋势

- 按地区

- 按类型

- 成本細項分析

- 可持续性分析

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 软体

- 服务

第六章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 推盘式分类机

- 倾斜托盘分类机

- 交叉带式分类机

- 鞋子分类器

- 其他的

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 运输与物流

- 零售与电子商务

- 食品和饮料

- 製药

- 其他的

第八章:市场估计与预测:按地区,2021 - 2034 年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Amazon

- Alstef Group's

- Bastian Solutions (Toyota Advanced Logistics)

- BEUMER Group

- BOWE INTRALOGISTICS

- Daifuku

- Dematic (KION Group)

- Equinox MHE

- Falcon Autotech

- Five Group

- GBI Intralogistics

- GreyOrange

- Honeywell Intelligrated

- Interroll Group

- Korber Supply Chain (formerly Consoveyo)

- Kuecker Pulse Integration (KPI)

- MHS Global

- Okura Yusoki

- Schaefer Systems International (SSI SCHAFER)

- Vanderlande

The Global Parcel Sorting System Market was valued at USD 2.3 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 4.4 billion by 2034. This steady growth is largely driven by the increasing demand for faster, smarter, and more cost-effective solutions in the logistics and e-commerce sectors. As the volume of parcels continues to rise and customer expectations tighten, logistics operators are shifting away from outdated manual methods toward advanced automation technologies. The integration of artificial intelligence, machine learning, and cloud-powered platforms is transforming sorting operations by improving speed, minimizing errors, and enhancing overall operational efficiency. Real-time adaptability and seamless processing across distribution hubs have become core priorities, making intelligent automation a central feature in modern parcel handling strategies.

Automated mobile robots and AI-driven systems are reducing handling time and boosting efficiency across logistics operations. Companies are also leveraging IoT and digital twin technologies to enable predictive maintenance, helping to improve equipment uptime and reliability. Innovations in performance tracking and proactive system alerts are being rolled out to avoid operational delays and maximize throughput. These tech-driven advancements reflect how logistics automation is evolving from assisted tasks to highly collaborative, intelligent ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.3 Billion |

| Forecast Value | $4.4 Billion |

| CAGR | 7.3% |

The hardware segment held a 66% share in 2024 and is estimated to grow at 7% CAGR through 2034. The increased need for modular, scalable hardware to handle rising parcel volumes is driving heavy investment in physical infrastructure. These systems are engineered for high-speed, high-accuracy operations and are critical to maintaining efficient logistics performance as order sizes and frequencies continue to rise globally.

Among sorting types, the cross-belt segment held a 34% share in 2024 and is expected to grow at a CAGR of 8% through 2034. Their ability to sort packages of various shapes and sizes with precision, while maintaining gentle handling for delicate items, has made them a top choice for high-volume logistics centers. Their versatility allows logistics providers to handle the growing variety of parcel types driven by global e-commerce growth, ensuring long-term adaptability.

U.S. Parcel Sorting System Market held an 80% share and generated USD 590 million in 2024. The country's leadership stems from its aggressive adoption of logistics automation, a strong e-commerce ecosystem, and continued investments in smart warehouse infrastructure. Companies are deploying advanced equipment alongside intelligent software platforms to improve output, manage sorting capacity, and optimize distribution across vast fulfillment networks.

Leading players in the Global Parcel Sorting System Market include BEUMER Group, Vanderlande, Korber, Honeywell Intelligrated, Daifuku, Interroll Group, and Dematic. To secure a stronger market position, companies in the parcel sorting system industry are deploying strategic initiatives that focus on innovation, expansion, and collaboration. They are enhancing product lines with AI-based automation, cloud integration, and real-time monitoring features. Firms are also forming global partnerships, expanding into emerging markets, and investing in next-gen technologies like AMRs, digital twins, and IoT-enabled diagnostics. Many companies are scaling their modular hardware offerings and customizing solutions for e-commerce, retail, and third-party logistics clients to ensure broader adoption.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Data mining sources

- 1.2.1 Global

- 1.2.2 Regional/Country

- 1.3 Base estimates & calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Type

- 2.2.4 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw materials manufacturer

- 3.1.1.2 Parcel sorting system manufacturer

- 3.1.1.3 Technology vendors and developers

- 3.1.1.4 System integrators and consultants

- 3.1.1.5 Distribution partners and channels

- 3.1.1.6 End use

- 3.1.2 Cost structure

- 3.1.3 Profit margin

- 3.1.4 Value addition at each stage

- 3.1.5 Factors impacting the supply chain

- 3.1.6 Disruptors

- 3.1.1 Supplier landscape

- 3.2 Impact on forces

- 3.2.1 Growth drivers

- 3.2.1.1 E-commerce growth and last-mile delivery demands

- 3.2.1.2 Rising labor costs and workforce optimization needs

- 3.2.1.3 Automation and ai integration in logistics operations

- 3.2.1.4 Sustainability requirements and environmental regulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial capital investment and ROI considerations

- 3.2.2.2 High implementation and maintenance costs

- 3.2.3 Market opportunities

- 3.2.3.1 E-commerce driving advanced sorting needs

- 3.2.3.2 Growing need for flexible systems to sort varied parcel sizes

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Porter's analysis

- 3.5 PESTEL analysis

- 3.6 Technology & innovation landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Patent analysis

- 3.8 Regulatory landscape

- 3.8.1 North America

- 3.8.2 Europe

- 3.8.3 Asia Pacific

- 3.8.4 Latin America

- 3.8.5 Middle East & Africa

- 3.9 Price trends

- 3.9.1 By region

- 3.9.2 By type

- 3.10 Cost breakdown analysis

- 3.11 Sustainability analysis

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Push tray sorters

- 6.3 Tilt-tray sorter

- 6.4 Crossbelt sorter

- 6.5 Shoe sorter

- 6.6 Others

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Transportation & Logistics

- 7.3 Retail & E-commerce

- 7.4 Food & Beverage

- 7.5 Pharmaceutical

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 8.1 North America

- 8.1.1 U.S.

- 8.1.2 Canada

- 8.2 Europe

- 8.2.1 UK

- 8.2.2 Germany

- 8.2.3 France

- 8.2.4 Italy

- 8.2.5 Spain

- 8.2.6 Belgium

- 8.2.7 Netherlands

- 8.2.8 Sweden

- 8.3 Asia Pacific

- 8.3.1 China

- 8.3.2 India

- 8.3.3 Japan

- 8.3.4 Australia

- 8.3.5 Singapore

- 8.3.6 South Korea

- 8.3.7 Vietnam

- 8.3.8 Indonesia

- 8.4 Latin America

- 8.4.1 Brazil

- 8.4.2 Mexico

- 8.4.3 Argentina

- 8.5 MEA

- 8.5.1 South Africa

- 8.5.2 Saudi Arabia

- 8.5.3 UAE

Chapter 9 Company Profiles

- 9.1 Amazon

- 9.2 Alstef Group's

- 9.3 Bastian Solutions (Toyota Advanced Logistics)

- 9.4 BEUMER Group

- 9.5 BOWE INTRALOGISTICS

- 9.6 Daifuku

- 9.7 Dematic (KION Group)

- 9.8 Equinox MHE

- 9.9 Falcon Autotech

- 9.10 Five Group

- 9.11 GBI Intralogistics

- 9.12 GreyOrange

- 9.13 Honeywell Intelligrated

- 9.14 Interroll Group

- 9.15 Korber Supply Chain (formerly Consoveyo)

- 9.16 Kuecker Pulse Integration (KPI)

- 9.17 MHS Global

- 9.18 Okura Yusoki

- 9.19 Schaefer Systems International (SSI SCHAFER)

- 9.20 Vanderlande

2026年全球包裹分类系统市场报告

2026年全球包裹分类系统市场报告 小包裹分类系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及设备划分

小包裹分类系统市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户、功能及设备划分 包裹分类系统市场 - 全球产业规模、份额、趋势、机会及预测(按类型、产品、应用、地区和竞争格局划分),2021-2031年

包裹分类系统市场 - 全球产业规模、份额、趋势、机会及预测(按类型、产品、应用、地区和竞争格局划分),2021-2031年 2026-2030年全球小包裹分类市场

2026-2030年全球小包裹分类市场 EFEM 和分类机:2025-2031 年全球市场份额和排名、总收入和需求预测

EFEM 和分类机:2025-2031 年全球市场份额和排名、总收入和需求预测 小包裹分类系统市场:按系统类型、最终用户、吞吐量和自动化程度划分 - 2025 年至 2032 年全球预测物流包装和分类设备市场(按设备类型、自动化程度、营运环境、应用、最终用途和分销管道)—2025-2030 年全球预测

小包裹分类系统市场:按系统类型、最终用户、吞吐量和自动化程度划分 - 2025 年至 2032 年全球预测物流包装和分类设备市场(按设备类型、自动化程度、营运环境、应用、最终用途和分销管道)—2025-2030 年全球预测 小包裹分拣系统市场规模、份额及成长分析(按产品、类型、应用和地区)-2025 年至 2032 年产业预测

小包裹分拣系统市场规模、份额及成长分析(按产品、类型、应用和地区)-2025 年至 2032 年产业预测 AI 咖啡豆分类机市场报告:2030 年趋势、预测与竞争分析

AI 咖啡豆分类机市场报告:2030 年趋势、预测与竞争分析 全球包裹分拣系统市场规模:依产品类型、按组件、依最终用户、按地区、范围和预测

全球包裹分拣系统市场规模:依产品类型、按组件、依最终用户、按地区、范围和预测