|

市场调查报告书

商品编码

1801860

表面处理市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Surface Treatments Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

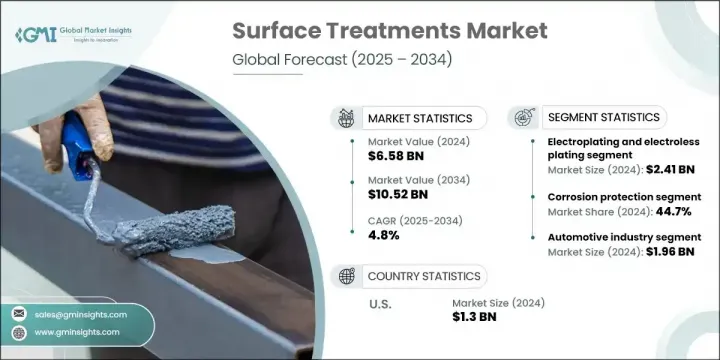

2024 年全球表面处理市场价值为 65.8 亿美元,预计到 2034 年将以 4.8% 的复合年增长率成长,达到 105.2 亿美元。这一增长得益于汽车、航太、建筑和电子等领域对增强表面性能的需求不断增长。表面处理可改善各种材料(包括金属、复合材料和聚合物)的耐磨性、防腐性、附着力和美观性等性能。由于结构材料面临湿气、紫外线和化学降解等环境压力的影响,表面处理是保持其功能性和使用寿命的重要屏障。这些处理形式包括密封剂、疏水涂层或在混凝土、钢材和木材等基材上涂覆环保保护层。

向永续建筑实践的转变也促进了水基和生物基处理解决方案的采用,从而符合绿色建筑标准。随着各行各业对在更严苛条件下实现更高性能的要求,客製化处理技术正发挥越来越重要的作用。从提高效率到减少维护需求,表面处理市场正快速朝向更具客製化和环保的解决方案发展,为各行各业带来长期营运优势。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 65.8亿美元 |

| 预测值 | 105.2亿美元 |

| 复合年增长率 | 4.8% |

雷射纹理处理、等离子处理和奈米涂层等技术的投资正日益受到关注,尤其是在电子和航太等注重精密製造的行业。这些先进的处理技术能够在表面层面进行高度精准的性能改进,即使是微小的差异也可能影响整体功能。製造商不断开发满足严格工业规范的解决方案,并提供可客製化的表面处理,以提高产品的耐用性。

2024年,电镀和化学镀领域产值达24.1亿美元。这些被广泛采用的方法能够提供经济高效的防腐保护,尤其适用于注重表面一致性和耐磨性的製造环境。此外,阳极氧化和化学转化膜等其他成熟技术在註重耐用性和环境相容性的产业中也持续广泛应用。这些方法能够形成保护性氧化层,增强表面弹性,并提供长期性能。

2024年,防蚀领域占了44.7%的市场。该应用在船舶、汽车和基础设施领域至关重要,这些领域的恶劣环境使得持久的表面保护成为必要。涂装系统、转化处理和电镀製程有助于延长零件寿命、降低更换成本并提高安全性。同样重要的是注重耐磨性,尤其是对于高摩擦、高负荷条件下的航太机械和工具。增强的表面强度可确保在极端操作环境下的稳定性能和结构可靠性。

2024年,美国表面处理市场产值达13亿美元。其领先地位得益于强大的製造生态系统和先进材料的广泛应用。创新仍然是美国经济成长的核心支柱,国防、航太和电子等高风险产业强大的研发项目为其提供了有力支持。该市场也日益重视永续性,推动了人们对环保处理技术的兴趣,并将表面处理技术融入性能关键型应用中。

推动表面处理市场的关键参与者包括 Jotun A/S、BASF SE(表面技术部门)、关西涂料株式会社、RPM International Inc.、Axalta Coating Systems Ltd.、日本涂料控股株式会社、宣伟公司、汉高股份公司、PPG Industries Inc. 和阿克苏诺贝尔 NV。在表面处理市场运营的公司正专注于开发先进的环保技术,以增强产品功能,同时满足法规遵循。策略性研发投资使公司能够在奈米涂层、生物基表面改质剂和低 VOC(挥发性有机化合物)配方等领域进行创新。与航太、电子和汽车製造商的合作使他们能够创建客製化的、以性能为导向的解决方案。市场领导者也透过合併、收购和合资企业扩大其全球影响力,以进入新兴市场并拓宽其产品组合。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 未来市场趋势

- 专利格局

- 贸易统计(HS编码)

(註:仅提供重点国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按技术类型,2021-2034 年

- 主要趋势

- 电镀和化学镀

- 阳极处理和化学转化涂层

- 热喷涂技术

- 物理气相沉积(PVD)

- 化学气相沉积(CVD)

- 等离子表面处理

- 雷射表面工程

- 新兴技术

第六章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 防腐蚀

- 耐磨性增强

- 装饰性和美观性

- 电气和电子特性

- 生物相容性和医疗应用

- 热管理

- 光学特性增强

第七章:市场估计与预测:按最终用户,2021-2034 年

- 主要趋势

- 汽车产业

- 航太和国防

- 电子和半导体

- 工业机械设备

- 医疗器材和医疗保健

- 能源和发电

- 建筑与建筑

- 海洋和近海

第八章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

- 哥伦比亚

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- PPG Industries Inc.

- The Sherwin-Williams Company

- AkzoNobel NV

- BASF SE (Surface Technologies Division)

- Henkel AG & Co. KGaA

- Axalta Coating Systems Ltd.

- RPM International Inc.

- Jotun A/S

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

The Global Surface Treatments Market was valued at USD 6.58 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 10.52 billion by 2034. This growth is fueled by rising demand for enhanced surface performance in sectors like automotive, aerospace, construction, and electronics. Surface treatments improve properties like wear resistance, corrosion protection, adhesion, and aesthetics for a variety of materials, including metals, composites, and polymers. As structural materials face exposure to environmental stressors like moisture, UV rays, and chemical degradation, surface treatments act as essential barriers that preserve functionality and longevity. These treatments come in forms such as sealants, hydrophobic coatings, or eco-conscious protective layers on substrates like concrete, steel, and timber.

The shift toward sustainable building practices has also encouraged the adoption of water-based and bio-sourced treatment solutions, aligning with green construction standards. With industries demanding better performance in harsher conditions, customized treatment technologies are playing a more prominent role. From increasing efficiency to reducing maintenance needs, the surface treatment market is quickly evolving toward more tailored and environmentally sound solutions that deliver long-term operational advantages across various industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.58 Billion |

| Forecast Value | $10.52 Billion |

| CAGR | 4.8% |

Technological investments in methods like laser texturing, plasma treatment, and nanocoatings are gaining traction, especially in precision-focused industries such as electronics and aerospace. These advanced treatments allow for highly specific performance modifications at the surface level, where even microscopic inconsistencies can impact overall functionality. Manufacturers continue to develop solutions that meet exacting industrial specifications with customizable finishes that promote product durability.

The electroplating and electroless plating segment generated USD 2.41 billion in 2024. These widely adopted methods deliver cost-effective corrosion protection and are especially useful in manufacturing environments where consistent finish and wear resistance are vital. Alongside these, other mature technologies such as anodizing and chemical conversion coatings continue to see extensive usage in industries that value durability and environmental compatibility. These methods create protective oxide layers that enhance surface resilience while offering long-term performance.

The corrosion protection segment held a 44.7% share in 2024. This application is vital across marine, automotive, and infrastructure sectors where harsh environmental exposure makes long-lasting surface protection a necessity. Coating systems, conversion treatments, and plating processes help extend component life, limit replacement costs, and boost safety. Equally critical is the focus on wear resistance, particularly for aerospace machinery and tools under high-friction, high-load conditions. Enhanced surface strength ensures steady performance and structural reliability in extreme operating environments.

U.S. Surface Treatments Market generated USD 1.3 billion in 2024. Its leadership is backed by a robust manufacturing ecosystem and the widespread use of advanced materials. Innovation remains a central pillar of growth in the U.S., supported by strong research programs across high-stakes industries like defense, aerospace, and electronics. This market also places increasing emphasis on sustainability, driving interest in environmentally responsible treatment technologies and the integration of surface treatments into performance-critical applications.

Key players driving the Surface Treatments Market include Jotun A/S, BASF SE (Surface Technologies Division), Kansai Paint Co., Ltd., RPM International Inc., Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., The Sherwin-Williams Company, Henkel AG & Co. KGaA, PPG Industries Inc., and AkzoNobel N.V. Companies operating in the surface treatments market are focusing on developing advanced, eco-friendly technologies to enhance product functionality while meeting regulatory compliance. Strategic R&D investments are enabling firms to innovate in areas such as nanocoatings, bio-based surface modifiers, and low-VOC (volatile organic compound) formulations. Collaborations with aerospace, electronics, and automotive manufacturers allow them to create customized, performance-oriented solutions. Market leaders are also expanding their global presence through mergers, acquisitions, and joint ventures to gain access to emerging markets and broaden their product portfolios.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Technology type trends

- 2.2.2 Application trends

- 2.2.3 End user trends

- 2.2.4 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.9 Future market trends

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code)

(Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021-2034 (USD Million) (Kilo tons)

- 5.1 Key trends

- 5.2 Electroplating and electroless plating

- 5.3 Anodizing and chemical conversion coatings

- 5.4 Thermal spraying technologies

- 5.5 Physical vapor deposition (PVD)

- 5.6 Chemical vapor deposition (CVD)

- 5.7 Plasma surface treatment

- 5.8 Laser surface engineering

- 5.9 Emerging technologies

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Kilo tons)

- 6.1 Key trends

- 6.2 Corrosion protection

- 6.3 Wear resistance enhancement

- 6.4 Decorative and aesthetic finishes

- 6.5 Electrical and electronic properties

- 6.6 Biocompatibility and medical applications

- 6.7 Thermal management

- 6.8 Optical properties enhancement

Chapter 7 Market Estimates and Forecast, By End User, 2021-2034 (USD Million) (Kilo tons)

- 7.1 Key trends

- 7.2 Automotive industry

- 7.3 Aerospace and defense

- 7.4 Electronics and semiconductors

- 7.5 Industrial machinery and equipment

- 7.6 Medical devices and healthcare

- 7.7 Energy and power generation

- 7.8 Construction and architecture

- 7.9 Marine and offshore

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Kilo tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Argentina

- 8.5.3 Chile

- 8.5.4 Colombia

- 8.5.5 Mexico

- 8.5.6 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 PPG Industries Inc.

- 9.2 The Sherwin-Williams Company

- 9.3 AkzoNobel N.V.

- 9.4 BASF SE (Surface Technologies Division)

- 9.5 Henkel AG & Co. KGaA

- 9.6 Axalta Coating Systems Ltd.

- 9.7 RPM International Inc.

- 9.8 Jotun A/S

- 9.9 Kansai Paint Co., Ltd.

- 9.10 Nippon Paint Holdings Co., Ltd.

船舶隔音材料市场按材料类型、船舶类型、应用领域、安装类型和供应来源划分-全球预测,2026-2032年

船舶隔音材料市场按材料类型、船舶类型、应用领域、安装类型和供应来源划分-全球预测,2026-2032年 表面处理化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

表面处理化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026-2034年全球交通运输路面材料市场规模、份额、趋势和成长分析报告全球成品生产线市场规模、份额、趋势及成长分析报告(2026-2034)

2026-2034年全球交通运输路面材料市场规模、份额、趋势和成长分析报告全球成品生产线市场规模、份额、趋势及成长分析报告(2026-2034) 全球工业低摩擦表面材料市场:预测(至2034年)-按材料类型、涂层技术、功能、应用、最终用户和地区进行分析

全球工业低摩擦表面材料市场:预测(至2034年)-按材料类型、涂层技术、功能、应用、最终用户和地区进行分析 2026年全球化学表面处理市场报告2026年全球成品生产线市场报告

2026年全球化学表面处理市场报告2026年全球成品生产线市场报告 表面处理化学品市场-全球产业规模、份额、趋势、机会、预测:按化学品、最终用户、地区和竞争对手划分,2021-2031年表面处理市场-全球产业规模、份额、趋势、机会及预测(依化学类型、基材、最终用途产业、地区及竞争格局划分,2021-2031年)

表面处理化学品市场-全球产业规模、份额、趋势、机会、预测:按化学品、最终用户、地区和竞争对手划分,2021-2031年表面处理市场-全球产业规模、份额、趋势、机会及预测(依化学类型、基材、最终用途产业、地区及竞争格局划分,2021-2031年) 表面处理化学品市场规模、份额和成长分析(按类型、基材、应用、最终用户和地区划分)-2026-2033年产业预测

表面处理化学品市场规模、份额和成长分析(按类型、基材、应用、最终用户和地区划分)-2026-2033年产业预测