|

市场调查报告书

商品编码

1801882

腹膜透析市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Peritoneal Dialysis Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

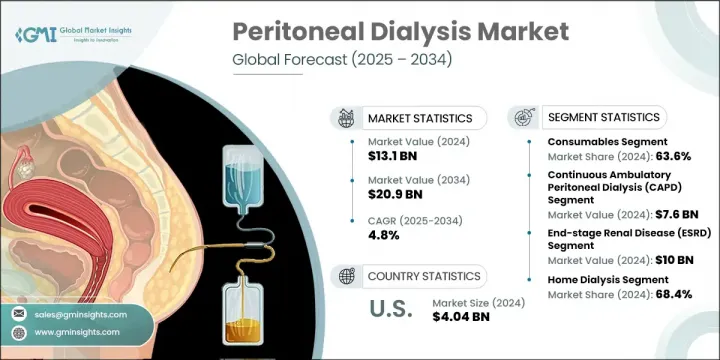

2024 年全球腹膜透析市场规模为 131 亿美元,预计到 2034 年将以 4.8% 的复合年增长率增长至 209 亿美元。推动这一增长的主要驱动因素包括肾臟相关疾病发病率的上升、居家透析解决方案的普及以及支持透析治疗的优惠报销结构。此外,与传统血液透析相比,腹膜透析的成本效益更高,再加上肾臟捐赠者的持续短缺,进一步刺激了市场需求。腹膜透析是针对末期肾病 (ESRD) 和急性肾损伤患者的一种维持生命的治疗方法,可在肾臟丧失功能时有效清除废物和多余液体。越来越多的人选择在家中进行病患管理的护理,这继续塑造着产业格局。此外,人口老化和受慢性肾臟疾病影响的患者数量不断增加,大大促进了全球 PD 解决方案的普及。

2024年,耗材市场占63.6%的市占率。这一主导地位主要归因于末期肾病(ESRD)病例数量的增加,以及对透析液、腹膜透析导管和其他相关耗材等腹膜透析必需组件的需求不断增长。向家庭疗法的转变显着影响了这一趋势,因为患者需要稳定的这些产品供应才能独立定期治疗。慢性和急性肾衰竭盛行率的上升,尤其是在老年人群体中,加剧了患者对耗材日益增长的依赖。这些人口结构变化持续推动对可靠、适用于家庭的透析解决方案的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 131亿美元 |

| 预测值 | 209亿美元 |

| 复合年增长率 | 4.8% |

持续性非卧床腹膜透析 (CAPD) 市场在 2024 年创造了 76 亿美元的收入,预计 2025-2034 年的复合年增长率将达到 4.6%。在自动化透析设备使用受限的地区,CAPD 仍然是首选。这种方法使患者能够每天多次进行手动换液,而无需依赖机器,价格实惠、易于使用,并能灵活地维持正常的日常护理。 CAPD 之所以越来越受欢迎,是因为它能够让患者更好地掌控自己的治疗,同时减少对透析中心的依赖。

2024年,美国腹膜透析市场规模达40.4亿美元,预计2025年至2034年期间的复合年增长率将达到3.5%。腹膜透析在美国日益普及,得益于其以患者为中心的优势,包括治疗灵活性、居家给药以及生活品质的提升。医疗保健提供者越来越多地推荐腹膜透析作为中心血液透析的可行替代方案,尤其是在医疗保健系统采用基于价值的医疗模式的背景下。越来越多的患者意识到腹膜透析的重要性,并接受更完善的培训项目,进一步推动了这一上升趋势。

积极影响全球腹膜透析市场的顶级公司包括 Terumo Corporation、Vantive(百特)、Diaverum(M42)、BD、B. Braun、Davita Kidney Care、Polymed、Utah Medical Products、Vivance、Fresenius Medical Care、medCOMP 和 Mozarc Medical。为了巩固市场地位并增强竞争力,腹膜透析领域的公司正积极推行多项策略性措施。

这些措施包括扩大产品组合,推出更先进、更便利的家用透析解决方案,并与医疗保健提供者建立合作关係,以加强服务网络。许多公司正大力投资研发,以开发效率更高、安全性更高的下一代腹膜透析设备。此外,公司还透过策略性併购来拓展地域覆盖范围并整合专业能力。此外,公司也进行培训计画和宣传活动,以提高病患(尤其是在发展中地区)的接受度和依从性。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 末期肾病(ESRD)患者数量不断增加

- 肾臟捐赠短缺

- 比血液透析的成本优势

- 透析治疗的优惠报销方案

- 糖尿病和高血压盛行率不断上升

- 产业陷阱与挑战

- 治疗併发症

- 市场机会

- 居家透析采用率的成长

- 新兴国家的需求不断成长

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 技术格局

- 历史时间表和行业演变

- 报销场景

- 报销政策对市场成长的影响

- 2024年各地区价格分析

- 透析机/循环仪

- 腹膜透析液/透析液

- 服务

- 差距分析

- 消费者行为分析

- 流行病学展望

- 波特的分析

- PESTEL分析

- 未来市场趋势

- 价值链分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 世界其他地区 (RoW)

- 按地区

- 竞争定位矩阵

- 主要市场参与者的竞争分析

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类别,2021 - 2034 年

- 主要趋势

- 透析机/循环器

- 耗材

- 腹膜透析液/透析液

- 葡萄糖

- 艾考糊精

- 胺基酸

- 导管

- 访问产品

- 其他耗材

- 腹膜透析液/透析液

- 服务

- 慢性透析

- 急性透析

- 耗材

第六章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 持续性非卧床腹膜透析(CAPD)

- 自动腹膜透析(APD)

第七章:市场估计与预测:依疾病状况,2021 - 2034 年

- 主要趋势

- 末期肾病(ESRD)

- 急性肾损伤(AKI)

- 其他条件

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 居家透析

- 中心透析

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- 全球参与者

- B. Braun

- BD

- Davita Kidney Care

- Diaverum (M42)

- Fresenius Medical Care

- medCOMP

- Mozarc Medical

- Polymed

- Terumo Corporation

- Utah Medical Products

- Vantive (Baxter)

- Vivance

- 区域参与者

- Apollo Dialysis

- Mitra Industries

- Newsol Technologies

- Northwest Kidney Centers

The Global Peritoneal Dialysis Market was valued at USD 13.1 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 20.9 billion by 2034. Key drivers fueling this expansion include the rising incidence of kidney-related conditions, increasing adoption of home-based dialysis solutions, and favorable reimbursement structures supporting dialysis treatment. Additionally, cost efficiency over traditional hemodialysis, combined with a persistent shortfall in kidney donors, further bolsters market demand. Peritoneal dialysis, a life-sustaining therapy for individuals facing end-stage renal disease (ESRD) and acute kidney injury, allows for the effective removal of waste and excess fluid when the kidneys lose function. A growing shift toward patient-managed care at home continues to shape the industry landscape. Moreover, the aging population and a growing number of patients affected by chronic kidney issues are contributing heavily to the uptake of PD solutions globally.

In 2024, the consumables segment held a 63.6% share. This dominance is largely attributed to a higher volume of ESRD cases and increasing demand for essential PD components such as dialysate solutions, PD catheters, and other related consumables. The shift toward home-based therapies has significantly influenced this trend, as patients require a steady supply of these products to conduct regular sessions independently. This growing patient reliance on consumables is magnified by the rising prevalence of both chronic and acute kidney failures, particularly within the elderly population. These demographic changes continue to push demand for dependable, home-compatible dialysis solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.1 Billion |

| Forecast Value | $20.9 Billion |

| CAGR | 4.8% |

The continuous ambulatory peritoneal dialysis (CAPD) segment generated USD 7.6 billion in 2024 and is forecasted to grow at a 4.6% CAGR during 2025-2034. CAPD remains a preferred choice in regions where access to automated dialysis equipment is limited. This approach enables patients to perform manual exchanges multiple times a day without relying on machines, offering affordability, ease of use, and the flexibility to maintain normal routines. Its growing popularity stems from its ability to empower patients with greater control over their treatment while reducing dependence on dialysis centers.

United States Peritoneal Dialysis Market was valued at USD 4.04 billion in 2024 and is expected to grow at a 3.5% CAGR from 2025 through 2034. The rising acceptance of PD in the country is due to its patient-centric benefits, including treatment flexibility, at-home administration, and improved quality of life. Healthcare providers are increasingly recommending PD as a viable alternative to center-based hemodialysis, especially as the healthcare system embraces value-based care models. This upward trend is further fueled by growing awareness and better training programs for patients opting for home dialysis.

The top-tier companies actively shaping the Global Peritoneal Dialysis Market are Terumo Corporation, Vantive (Baxter), Diaverum (M42), BD, B. Braun, Davita Kidney Care, Polymed, Utah Medical Products, Vivance, Fresenius Medical Care, medCOMP, and Mozarc Medical. To secure their market positions and enhance competitiveness, companies operating in the peritoneal dialysis sector are actively pursuing several strategic initiatives.

These include expanding their product portfolios with more advanced and user-friendly dialysis solutions tailored for home use, as well as forming partnerships with healthcare providers to strengthen service delivery networks. Many firms are investing heavily in R&D to develop next-generation PD devices with improved efficiency and safety profiles. Additionally, strategic mergers and acquisitions are being used to widen geographic reach and integrate specialized capabilities. Training programs and awareness campaigns are also being launched to boost patient adoption and adherence, particularly in developing regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Category trends

- 2.2.3 Type trends

- 2.2.4 Disease condition trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising number of end stage renal diseases (ESRD) patients

- 3.2.1.2 Shortage of donor kidneys

- 3.2.1.3 Cost advantages over hemodialysis

- 3.2.1.4 Favourable reimbursement scenario for dialysis treatment

- 3.2.1.5 Growing prevalence of diabetes and hypertension

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complications in the treatment

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in home dialysis adoption

- 3.2.3.2 Increasing demand in emerging countries

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Technology landscape

- 3.6 Historical timeline and industry evolution

- 3.7 Reimbursement scenario

- 3.7.1 Impact of reimbursement policies on market growth

- 3.8 Pricing analysis by region, 2024

- 3.8.1 Dialysis machines/cyclers

- 3.8.2 Peritoneal dialysis solution/Dialysate

- 3.8.3 Services

- 3.9 Gap analysis

- 3.10 Consumer behaviour analysis

- 3.11 Epidemiology outlook

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

- 3.14 Future market trends

- 3.15 Value chain analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 By Region

- 4.3.1.1 North America

- 4.3.1.2 Europe

- 4.3.1.3 Asia Pacific

- 4.3.1.4 Rest of the world (RoW)

- 4.3.1 By Region

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Category, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dialysis machines/Cyclers

- 5.2.1 Consumables

- 5.2.1.1 Peritoneal dialysis solution/Dialysate

- 5.2.1.1.1 Dextrose

- 5.2.1.1.2 Icodextrin

- 5.2.1.1.3 Amino Acid

- 5.2.1.2 Catheters

- 5.2.1.3 Access products

- 5.2.1.4 Other consumables

- 5.2.1.1 Peritoneal dialysis solution/Dialysate

- 5.2.2 Services

- 5.2.2.1 Chronic dialysis

- 5.2.2.2 Acute dialysis

- 5.2.1 Consumables

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Continuous ambulatory peritoneal dialysis (CAPD)

- 6.3 Automated peritoneal dialysis (APD)

Chapter 7 Market Estimates and Forecast, By Disease Condition, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 End-stage renal disease (ESRD)

- 7.3 Acute kidney injury (AKI)

- 7.4 Other conditions

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Home dialysis

- 8.3 In-center dialysis

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global players

- 10.1.1 B. Braun

- 10.1.2 BD

- 10.1.3 Davita Kidney Care

- 10.1.4 Diaverum (M42)

- 10.1.5 Fresenius Medical Care

- 10.1.6 medCOMP

- 10.1.7 Mozarc Medical

- 10.1.8 Polymed

- 10.1.9 Terumo Corporation

- 10.1.10 Utah Medical Products

- 10.1.11 Vantive (Baxter)

- 10.1.12 Vivance

- 10.2 Regional players

- 10.2.1 Apollo Dialysis

- 10.2.2 Mitra Industries

- 10.2.3 Newsol Technologies

- 10.2.4 Northwest Kidney Centers

血液透析和腹膜透析市场:按治疗类型、方法、技术、产品类型、患者类型和最终用户划分-2026年至2032年全球市场预测

血液透析和腹膜透析市场:按治疗类型、方法、技术、产品类型、患者类型和最终用户划分-2026年至2032年全球市场预测 2026年全球自动化腹膜透析市场报告

2026年全球自动化腹膜透析市场报告 连续性腹膜透析(CAPD)市场规模、份额和成长分析:按产品类型、透析方法、患者类型、最终用户、分销管道和地区划分-2026-2033年产业预测2026年全球血液透析及腹膜透析市场报告

连续性腹膜透析(CAPD)市场规模、份额和成长分析:按产品类型、透析方法、患者类型、最终用户、分销管道和地区划分-2026-2033年产业预测2026年全球血液透析及腹膜透析市场报告 全球血液透析和腹膜透析市场规模、份额、趋势和成长分析报告(2026-2034年)

全球血液透析和腹膜透析市场规模、份额、趋势和成长分析报告(2026-2034年) 血液透析和腹膜透析市场-全球产业规模、份额、趋势、机会、预测:按类型、产品、最终用户、地区和竞争格局划分,2021-2031年血液透析及腹膜透析市场-2026-2031年预测

血液透析和腹膜透析市场-全球产业规模、份额、趋势、机会、预测:按类型、产品、最终用户、地区和竞争格局划分,2021-2031年血液透析及腹膜透析市场-2026-2031年预测 血液透析和腹膜透析市场规模、份额和成长分析(按产品/服务、透析类型、年龄层、性别和地区划分)—产业预测(2026-2033年)2025年全球腹膜透析设备市场报告腹膜透析引流袋市场按产品类型、产品材质、产量、病患小组、最终用户和分销管道划分-2025-2030 年全球预测

血液透析和腹膜透析市场规模、份额和成长分析(按产品/服务、透析类型、年龄层、性别和地区划分)—产业预测(2026-2033年)2025年全球腹膜透析设备市场报告腹膜透析引流袋市场按产品类型、产品材质、产量、病患小组、最终用户和分销管道划分-2025-2030 年全球预测