|

市场调查报告书

商品编码

1801906

医用胶带市场机会、成长动力、产业趋势分析及2025-2034年预测Medical Adhesive Tapes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

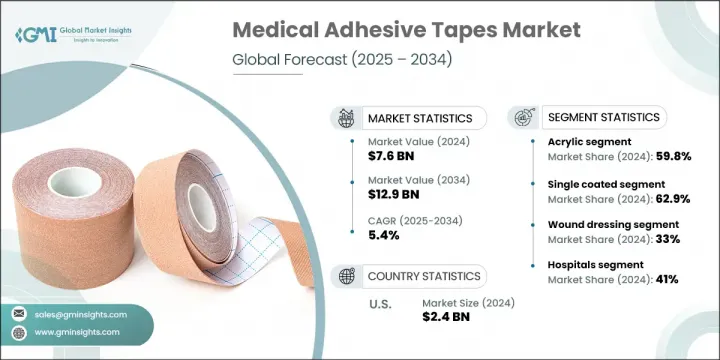

2024年,全球医用胶带市场规模达76亿美元,预计到2034年将以5.4%的复合年增长率成长,达到129亿美元。对高效伤口护理解决方案的需求不断增长,主要源于慢性病发病率的上升、外科手术的激增以及创伤相关病例的显着增加。医用胶带在现代医疗保健中发挥关键作用,用于固定绷带、静脉输液管和医疗器械,在需要快速伤口处理的紧急治疗中也发挥着重要作用。市场不断发展,更加重视舒适性、皮肤相容性和客製化。

製造商正在开发先进的亲肤低敏产品,以减少刺激并改善癒合效果。包括硅基和生物相容性材料在内的黏合剂创新正在重塑产品标准。患者个人化照护的转变进一步影响了购买行为,其中考虑了敏感性、活动性和伤口部位等因素。 Flexcon Company、Paul Hartmann、Berry Global Group、Solventum 和 Lohmann GmbH 等主要参与者正透过优先考虑产品创新和临床疗效来塑造市场格局。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 76亿美元 |

| 预测值 | 129亿美元 |

| 复合年增长率 | 5.4% |

2024年,丙烯酸类医用胶带占了59.8%的市场。其吸引力在于透气性、耐热防潮性以及短期和长期应用的兼容性。丙烯酸类胶黏剂能够有效控制水汽渗透,有助于降低皮肤破损的风险,并创造更好的癒合环境。这种兼具舒适性和耐用性的胶带使其成为伤口护理和外科手术的理想选择。

2024年,单面胶带占据最大份额,达62.9%,因其易于使用且在不同表面具有一致的黏合性而备受青睐。这些胶带适用于各种临床用途,从固定导管、敷料到医疗器械,使其成为医院和家庭护理环境中的可靠选择。其透气亲肤的特性,加上防潮性能,使其能够更安全、更快速地处理患者,这在快节奏的护理环境中至关重要。

2024年,美国医用胶带市场规模达24亿美元。这一市场主导地位得益于其先进的医疗基础设施和对可靠伤口护理产品日益增长的需求。老龄人口的成长以及糖尿病等疾病的高发生率是医用胶带使用量上升的主要原因。美国广泛的医疗保健网络持续推动高性能胶带的使用,这些胶带能够增强伤口癒合并提高患者舒适度。

积极参与全球医用胶带市场的主要公司包括强生、施乐辉、日东电工株式会社、麦克森公司、Dermarite Industries、Medline Industries、美敦力、艾利丹尼森公司、DermaMed Coatings Company、Nichiban、琳得科公司和康德乐。为了巩固市场地位,医用胶带市场的公司正在采取各种成长策略。他们正在投资研发,以设计更先进、更安全、更透气的黏合剂解决方案,以满足不同的肤质和临床需求。与医疗保健提供者的合作以及向高成长地区的扩张,可以扩大产品的覆盖范围。许多公司正专注于扩大製造能力和供应链,以满足日益增长的全球需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 道路交通事故和其他创伤事件激增

- 慢性病盛行率不断上升

- 外科手术数量不断增加

- 新兴经济体医疗保健产业蓬勃发展

- 成长动力

产业陷阱与挑战

- 原料成本高

- 严格的监管情景

- 市场机会

- 医用胶带技术创新不断涌现

- 成长潜力分析

- 监管格局

- 技术进步

- 供应链分析

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 丙烯酸纤维

- 硅酮

- 橡皮

第六章:市场估计与预测:按黏合剂,2021 - 2034 年

- 主要趋势

- 单面涂敷

- 双面涂层

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 手术

- 伤口敷料

- 设备固定

- 其他应用

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 专科诊所

- 门诊手术中心

- 其他最终用途

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- Avery Dennison Corporation

- Berry Global Group

- Cardinal Health

- DermaMed Coatings Company

- Dermarite Industries

- Flexcon Company

- Johnson & Johnson

- Lintec Corporation

- Lohmann GmbH

- McKesson Corporation

- Medline Industries

- Medtronic

- Nichiban

- Nitto Denko Corporation

- Paul Hartmann

- Smith & Nephew

- Solventum

The Global Medical Adhesive Tapes Market was valued at USD 7.6 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 12.9 billion by 2034. Rising demand for efficient wound care solutions is largely fueled by the growing incidence of chronic diseases, a surge in surgical interventions, and a notable increase in trauma-related cases. Medical adhesive tapes play a critical role in modern healthcare for securing bandages, IV lines, and medical devices, and are essential in emergency treatments requiring prompt wound management. The market continues to evolve, with greater emphasis on comfort, skin compatibility, and customization.

Manufacturers are developing advanced skin-friendly and hypoallergenic options that reduce irritation and improve healing outcomes. Innovations in adhesives, including silicone-based and biocompatible materials, are reshaping product standards. The shift toward patient-specific care further influences purchasing behavior, with sensitivity, mobility, and wound site factors considered. Major players such as Flexcon Company, Paul Hartmann, Berry Global Group, Solventum, and Lohmann GmbH are helping shape the market landscape by prioritizing product innovation and clinical efficacy.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.6 Billion |

| Forecast Value | $12.9 Billion |

| CAGR | 5.4% |

In 2024, the acrylic-based medical adhesive tapes accounted for a 59.8% share. Their appeal lies in their breathability, resistance to heat and moisture, and compatibility with both short-term and extended applications. The ability of acrylic adhesives to manage moisture vapor transmission helps reduce the risk of skin breakdown and supports better healing environments. This balance of comfort and durability makes them ideal for use in wound care and surgical settings.

The single-coated tapes held the largest share at 62.9% in 2024, favored for their easy application and consistent adhesion across different surfaces. These tapes are designed for a range of clinical uses, from securing tubing and dressings to medical devices, making them a reliable option in both hospital and home care settings. Their breathable and skin-friendly properties, combined with moisture resistance, allow for safer and quicker patient handling, which is critical in fast-paced care environments.

U.S. Medical Adhesive Tapes Market generated USD 2.4 billion in 2024. This dominance is driven by its advanced healthcare infrastructure and increasing demand for reliable wound care products. A growing elderly population and the high prevalence of conditions like diabetes are major contributors to rising usage. The country's extensive healthcare network continues to promote the use of high-performance tapes that offer enhanced healing and patient comfort.

Key companies actively involved in the Global Medical Adhesive Tapes Market include Johnson & Johnson, Smith & Nephew, Nitto Denko Corporation, McKesson Corporation, Dermarite Industries, Medline Industries, Medtronic, Avery Dennison Corporation, DermaMed Coatings Company, Nichiban, Lintec Corporation, and Cardinal Health. To strengthen their position, companies operating in the medical adhesive tapes market are adopting a variety of growth strategies. They are investing in R&D to engineer more advanced, skin-safe, and breathable adhesive solutions tailored to different skin types and clinical needs. Partnerships with healthcare providers and expansion into high-growth regions allow for improved product reach. Many are focusing on expanding manufacturing capabilities and supply chains to meet increasing global demand.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Adhesive trends

- 2.2.4 Application trends

- 2.2.5 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in road accidents and other traumatic incidents

- 3.2.1.2 Increasing prevalence of chronic disorders

- 3.2.1.3 Rising number of surgical procedures

- 3.2.1.4 Growing healthcare sector in emerging economies

- 3.2.1 Growth drivers

Industry pitfalls and challenges

- 3.2.1.5 High cost of raw material

- 3.2.1.6 Stringent regulatory scenario

- 3.2.2 Market opportunities

- 3.2.2.1 Rising technological innovations in medical tapes

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological advancements

- 3.6 Supply chain analysis

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

- 4.7 Key developments

- 4.7.1 Mergers and acquisitions

- 4.7.2 Partnerships and collaborations

- 4.7.3 New product launches

- 4.7.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn, Units)

- 5.1 Key trends

- 5.2 Acrylic

- 5.3 Silicone

- 5.4 Rubber

Chapter 6 Market Estimates and Forecast, By Adhesive, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Single coated

- 6.3 Double coated

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Surgery

- 7.3 Wound dressing

- 7.4 Device fixation

- 7.5 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Ambulatory surgical centers

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Avery Dennison Corporation

- 10.2 Berry Global Group

- 10.3 Cardinal Health

- 10.4 DermaMed Coatings Company

- 10.5 Dermarite Industries

- 10.6 Flexcon Company

- 10.7 Johnson & Johnson

- 10.8 Lintec Corporation

- 10.9 Lohmann GmbH

- 10.10 McKesson Corporation

- 10.11 Medline Industries

- 10.12 Medtronic

- 10.13 Nichiban

- 10.14 Nitto Denko Corporation

- 10.15 Paul Hartmann

- 10.16 Smith & Nephew

- 10.17 Solventum

医用胶带市场:2026-2032年全球市场预测(按产品类型、黏合剂类型、基材、应用、最终用户和分销管道划分)

医用胶带市场:2026-2032年全球市场预测(按产品类型、黏合剂类型、基材、应用、最终用户和分销管道划分) 2026年全球医用胶带市场报告

2026年全球医用胶带市场报告 全球医用胶带市场规模、份额、趋势及成长分析报告(2026-2034年)2026年全球医用胶带市场报告

全球医用胶带市场规模、份额、趋势及成长分析报告(2026-2034年)2026年全球医用胶带市场报告 运动胶带市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、分销管道、地区和竞争格局划分,2021-2031年包装胶带市场-2026-2031年预测客製化包装胶带市场:按黏合剂、材料、胶带宽度、应用、最终用户和分销管道划分,全球预测,2026-2032年

运动胶带市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、分销管道、地区和竞争格局划分,2021-2031年包装胶带市场-2026-2031年预测客製化包装胶带市场:按黏合剂、材料、胶带宽度、应用、最终用户和分销管道划分,全球预测,2026-2032年 医用胶带市场规模、份额及成长分析(按基材、树脂类型、应用和地区划分)-2026-2033年产业预测医疗保健胶带市场-全球产业规模、份额、趋势、机会和预测,按背衬材料、树脂类型、应用、地区和竞争情况细分,2020-2030 年预测运动胶带市场按类型、形式、材料成分、黏合剂类型、应用、分销管道和最终用户划分——2025-2030 年全球预测

医用胶带市场规模、份额及成长分析(按基材、树脂类型、应用和地区划分)-2026-2033年产业预测医疗保健胶带市场-全球产业规模、份额、趋势、机会和预测,按背衬材料、树脂类型、应用、地区和竞争情况细分,2020-2030 年预测运动胶带市场按类型、形式、材料成分、黏合剂类型、应用、分销管道和最终用户划分——2025-2030 年全球预测