|

市场调查报告书

商品编码

1801933

黏合剂和密封剂市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Adhesives and Sealants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

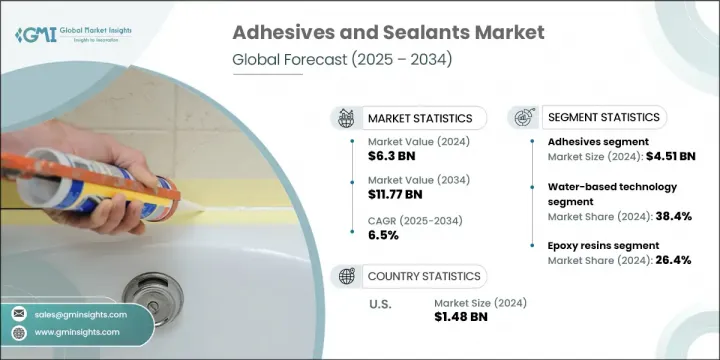

2024年,全球黏合剂和密封剂市场规模达63亿美元,预计到2034年将以6.5%的复合年增长率成长,达到117.7亿美元。该市场专注于黏合和密封材料的开发和使用,这些材料可增强各行各业产品的强度、使用寿命和耐用性。这些材料在建筑、汽车、电子和包装应用中发挥关键作用,能够有效防止产品受到天气、洩漏和外部污染物的侵害。随着全球基础设施现代化和轻量化节能汽车的推动,对黏合剂和密封剂的需求持续增长。

专注于性能、环保合规性和材料多功能性的创新正在帮助製造商满足不断发展的行业标准,同时提高产品的可靠性和效率。各公司正在不断开发先进的黏合剂和密封剂配方,以在极端条件下提供更强的黏合力,抵抗化学物质和温度波动,并缩短固化时间以支援更快的组装流程。这些改进不仅提高了营运效率,也延长了最终用途产品的生命週期。同时,对环保解决方案的追求正在推动人们转向符合全球永续发展目标的低挥发性有机化合物 (VOC)、生物基和可回收材料。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 63亿美元 |

| 预测值 | 117.7亿美元 |

| 复合年增长率 | 6.5% |

2024年,黏合剂市场规模达45.1亿美元,预计2034年将维持6.5%的强劲复合年增长率。环氧树脂和聚氨酯等结构胶粘剂因其在汽车和航太应用中的卓越粘合性能而引领市场。黏合剂市场包括压敏胶、热熔胶以及溶剂型和水性黏合剂。

在各类技术中,受可持续低挥发性有机化合物 (VOC) 产品兴起的推动,水性黏合剂在 2024 年占据了 38.4% 的市场。水性黏合剂更安全的应用和环保特性使其在家具、汽车、包装和建筑业的应用日益广泛。随着製造商致力于遵守空气品质法规,水性黏合剂在工业和商业应用中的普及度持续提升。

美国黏合剂和密封剂市场占据88.5%的市场份额,2024年市场规模达14.8亿美元。由于对先进製造业、电动车生产和国家基础设施升级的强劲投资,美国市场预计将持续成长至2034年。针对交通网络和公共建筑的联邦资助计划正在刺激对高性能黏合剂和密封产品的需求。此外,航太、电子和永续建筑的兴起,也巩固了美国作为黏合剂技术关键市场的地位。

全球黏合剂和密封剂市场的知名企业包括巴斯夫、陶氏、汉高股份公司、西卡公司和3M公司。黏合剂和密封剂行业的主要公司正在透过有针对性的研发投资、环保产品开发和区域扩张来提升其市场地位。为了满足环境法规和消费者的永续需求,企业正向低挥发性有机化合物 (VOC) 和生物基黏合剂进行策略转变。各公司正在加强供应链,并扩大高成长地区的製造能力,以缩短交货时间并提高营运效率。策略性併购和合作伙伴关係正在扩大产品组合和市场准入。针对电动车、电子产品和智慧基础设施量身定制的黏合剂解决方案也是重点,有助于满足下一代工业需求。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 转向轻量化製造

- 绿建筑与环保配方

- 电动交通和电子产品的成长

- 包装创新和安全要求

- 产业陷阱与挑战

- 环境和监管压力

- 原物料价格波动

- 市场机会

- 对永续和生物基替代品的需求

- 模组化和预製建筑的兴起

- 不断扩大的医疗保健和医疗器材市场

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 黏合剂市场

- 结构胶合剂

- 环氧胶黏剂

- 聚氨酯黏合剂

- 丙烯酸黏合剂

- 甲基丙烯酸甲酯黏合剂

- 氰基丙烯酸酯黏合剂

- 压敏胶

- 丙烯酸压敏胶

- 橡胶基压敏胶

- 硅胶压敏胶

- 热熔胶

- EVA热熔胶

- 聚酰胺热熔胶

- 聚烯烃热熔胶

- 反应性热熔胶

- 水性黏合剂

- 溶剂型黏合剂

- 其他黏合剂类型

- 结构胶合剂

- 密封剂市场

- 硅酮密封胶

- RTV硅酮密封胶

- 结构玻璃密封胶

- 聚氨酯密封胶

- 丙烯酸密封胶

- 聚硫密封胶

- 丁基密封胶

- 其他密封胶类型

- 硅酮密封胶

第六章:市场估计与预测:依技术分类,2021 - 2034 年

- 主要趋势

- 水性技术

- 溶剂型技术

- 热熔技术

- 反应技术

- UV/光固化技术

- 压力感应技术

- 其他的

第七章:市场估计与预测:按树脂类型,2021 - 2034

- 主要趋势

- 环氧树脂

- 聚氨酯树脂

- 丙烯酸树脂

- 硅树脂

- 聚醋酸乙烯酯(PVA)

- 乙烯醋酸乙烯酯 (EVA)

- 苯乙烯嵌段共聚物

- 其他的

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 结构黏合

- 组装操作

- 密封和衬垫

- 表面保护

- 电绝缘

- 热管理

- 避震

- 其他的

第九章:市场估计与预测:按最终用途产业,2021 - 2034 年

- 主要趋势

- 建筑和施工

- 住宅建筑

- 商业建筑

- 基础设施项目

- 汽车和运输

- 搭乘用车

- 商用车

- 电动车

- 售后市场

- 包装

- 软包装

- 硬质包装

- 标籤和胶带

- 电子和电气

- 消费性电子产品

- 半导体封装

- PCB组装

- 显示技术

- 航太和国防

- 商业航空

- 军事应用

- 空间应用

- 医疗保健

- 医疗器材

- 外科手术应用

- 医药包装

- 鞋类和皮革

- 木工和家具

- 船舶应用

- 其他的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 中东和非洲其他地区

第 11 章:公司简介

- 3M Company

- Arkema Group (Bostik)

- Ashland Global Holdings Inc.

- Avery Dennison Corporation

- BASF SE

- Dow Inc.

- DuPont de Nemours, Inc.

- HB Fuller Company

- Henkel AG & Co. KGaA

- Huntsman Corporation

- Illinois Tool Works Inc. (ITW)

- Momentive Performance Materials Inc.

- RPM International Inc.

- Sika AG

- Wacker Chemie AG

The Global Adhesives and Sealants Market was valued at USD 6.3 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 11.77 billion by 2034. This market revolves around the development and use of bonding and sealing materials that enhance the strength, longevity, and resistance of products across multiple industries. These materials play a key role in construction, automotive, electronics, and packaging applications, where they provide protection against weather, leakage, and external contaminants. With the global push toward infrastructure modernization and lightweight, energy-efficient vehicles, demand continues to accelerate.

Innovations focused on performance, eco-compliance, and material versatility are helping manufacturers meet evolving industry standards while improving product reliability and efficiency. Companies are increasingly developing advanced adhesive and sealant formulations that deliver stronger bonding under extreme conditions, resist chemicals and temperature fluctuations, and reduce cure times to support faster assembly processes. These improvements not only boost operational efficiency but also extend the lifecycle of end-use products. Simultaneously, the push for eco-friendly solutions is driving the shift toward low-VOC, bio-based, and recyclable materials that align with global sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.3 Billion |

| Forecast Value | $11.77 Billion |

| CAGR | 6.5% |

The adhesives segment accounted for USD 4.51 billion in 2024 and is expected to maintain a strong CAGR of 6.5% through 2034. Structural adhesives such as epoxy and polyurethane lead the market due to their superior bonding in automotive and aerospace applications. The adhesives segment includes pressure-sensitive adhesives, hot melts, and both solvent- and water-based variants.

Among technologies, the water-based adhesives segment held 38.4% share in 2024, driven by the rise of sustainable, low-VOC products. Their safer application and environmental compatibility have increased adoption across furniture, automotive, packaging, and construction sectors. As manufacturers aim to align with air quality regulations, water-based adhesives continue to gain popularity for both industrial and commercial applications.

United States Adhesives and Sealants Market held an 88.5% share and generated USD 1.48 billion in 2024. The U.S. market is set for continued growth through 2034, supported by robust investments in advanced manufacturing, EV production, and national infrastructure upgrades. Federal funding initiatives targeting transportation networks and public buildings are boosting the demand for high-performance adhesive and sealing products. Additionally, the rise of aerospace, electronics, and sustainable construction is reinforcing the country's role as a key market for adhesive technologies.

Prominent players in the Global Adhesives and Sealants Market include BASF SE, Dow Inc., Henkel AG & Co. KGaA, Sika AG, and 3M Company. Major companies in the adhesives and sealants industry are enhancing their market position through targeted R&D investments, eco-friendly product development, and regional expansion. There's a strategic shift toward low-VOC and bio-based adhesives to address environmental regulations and consumer sustainability demands. Companies are strengthening supply chains and expanding manufacturing capabilities in high-growth regions to reduce lead times and boost operational efficiency. Strategic mergers, acquisitions, and partnerships are enabling broader product portfolios and market access. Custom adhesive solutions tailored for electric vehicles, electronics, and smart infrastructure are also a focus, helping meet next-gen industrial demands.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Technology

- 2.2.4 Resin type

- 2.2.5 Application

- 2.2.6 End Use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward lightweight manufacturing

- 3.2.1.2 Green building and eco-friendly formulations

- 3.2.1.3 Growth of e-mobility and electronics

- 3.2.1.4 Packaging innovation and safety requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Environmental and regulatory pressure

- 3.2.2.2 Raw material price volatility

- 3.2.3 Market opportunities

- 3.2.3.1 Demand for sustainable and bio-based alternatives

- 3.2.3.2 Rise in modular and prefabricated construction

- 3.2.3.3 Expanding healthcare and medical devices market

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product type

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and environmental aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly Initiatives

- 3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Adhesives market

- 5.2.1 Structural adhesives

- 5.2.1.1 Epoxy adhesives

- 5.2.1.2 Polyurethane adhesives

- 5.2.1.3 Acrylic adhesives

- 5.2.1.4 Methyl methacrylate adhesives

- 5.2.1.5 Cyanoacrylate adhesives

- 5.2.2 Pressure sensitive adhesives

- 5.2.2.1 Acrylic PSA

- 5.2.2.2 Rubber-based PSA

- 5.2.2.3 Silicone PSA

- 5.2.3 Hot melt adhesives

- 5.2.3.1 EVA hot melts

- 5.2.3.2 Polyamide hot melts

- 5.2.3.3 Polyolefin hot melts

- 5.2.3.4 Reactive hot melts

- 5.2.4 Water-based adhesives

- 5.2.5 Solvent-based adhesives

- 5.2.6 Other adhesive types

- 5.2.1 Structural adhesives

- 5.3 Sealants market

- 5.3.1 Silicone sealants

- 5.3.1.1 RTV silicone sealants

- 5.3.1.2 Structural glazing sealants

- 5.3.2 Polyurethane sealants

- 5.3.3 Acrylic sealants

- 5.3.4 Polysulfide sealants

- 5.3.5 Butyl sealants

- 5.3.6 Other sealant types

- 5.3.1 Silicone sealants

Chapter 6 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Water-based technology

- 6.3 Solvent-based technology

- 6.4 Hot melt technology

- 6.5 Reactive technology

- 6.6 UV/light curable technology

- 6.7 Pressure sensitive technology

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Resin Type, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Epoxy resins

- 7.3 Polyurethane resins

- 7.4 Acrylic resins

- 7.5 Silicone resins

- 7.6 Polyvinyl acetate (PVA)

- 7.7 Ethylene vinyl acetate (EVA)

- 7.8 Styrenic block copolymers

- 7.9 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

- 8.1 Key trends

- 8.2 Structural bonding

- 8.3 Assembly operations

- 8.4 Sealing and gasketing

- 8.5 Surface protection

- 8.6 Electrical insulation

- 8.7 Thermal management

- 8.8 Vibration damping

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 (USD Billion, Kilo Tons)

- 9.1 Key trends

- 9.2 Building and construction

- 9.2.1 Residential construction

- 9.2.2 Commercial construction

- 9.2.3 Infrastructure projects

- 9.3 Automotive and transportation

- 9.3.1 Passenger vehicles

- 9.3.2 Commercial vehicles

- 9.3.3 Electric vehicles

- 9.3.4 Aftermarket

- 9.4 Packaging

- 9.4.1 Flexible packaging

- 9.4.2 Rigid packaging

- 9.4.3 Labels and tapes

- 9.5 Electronics and electrical

- 9.5.1 Consumer electronics

- 9.5.2 Semiconductor packaging

- 9.5.3 PCB assembly

- 9.5.4 Display technologies

- 9.6 Aerospace and defense

- 9.6.1 Commercial aviation

- 9.6.2 Military applications

- 9.6.3 Space applications

- 9.7 Medical and healthcare

- 9.7.1 Medical devices

- 9.7.2 Surgical applications

- 9.7.3 Pharmaceutical packaging

- 9.8 Footwear and leather

- 9.9 Woodworking and furniture

- 9.10 Marine applications

- 9.11 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion, Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 3M Company

- 11.2 Arkema Group (Bostik)

- 11.3 Ashland Global Holdings Inc.

- 11.4 Avery Dennison Corporation

- 11.5 BASF SE

- 11.6 Dow Inc.

- 11.7 DuPont de Nemours, Inc.

- 11.8 H.B. Fuller Company

- 11.9 Henkel AG & Co. KGaA

- 11.10 Huntsman Corporation

- 11.11 Illinois Tool Works Inc. (ITW)

- 11.12 Momentive Performance Materials Inc.

- 11.13 RPM International Inc.

- 11.14 Sika AG

- 11.15 Wacker Chemie AG

黏合剂市场:按产品类型、包装、应用、终端用户产业和销售管道- 全球预测(2026-2032年)

黏合剂市场:按产品类型、包装、应用、终端用户产业和销售管道- 全球预测(2026-2032年) 日本黏合剂和密封剂市场规模、份额、趋势和预测(按黏合剂类型、密封剂类型、技术、应用和地区划分),2026-2034年外墙建筑黏合剂和密封剂市场:按分销管道、产品类型、技术、配方、最终用途产业和应用划分-2025-2032年全球预测弹性黏合剂和密封剂市场(按树脂类型、包装类型、应用方法、最终用户产业和分销管道)—全球预测 2025-2032防水胶黏剂和密封剂市场(按产品类型、技术、形式、最终用途和应用)—2025-2032 年全球预测黏合剂和密封剂市场(按产品类型、最终用途产业、技术、应用、形式和分销管道)—2025-2032 年全球预测

日本黏合剂和密封剂市场规模、份额、趋势和预测(按黏合剂类型、密封剂类型、技术、应用和地区划分),2026-2034年外墙建筑黏合剂和密封剂市场:按分销管道、产品类型、技术、配方、最终用途产业和应用划分-2025-2032年全球预测弹性黏合剂和密封剂市场(按树脂类型、包装类型、应用方法、最终用户产业和分销管道)—全球预测 2025-2032防水胶黏剂和密封剂市场(按产品类型、技术、形式、最终用途和应用)—2025-2032 年全球预测黏合剂和密封剂市场(按产品类型、最终用途产业、技术、应用、形式和分销管道)—2025-2032 年全球预测 全球黏合剂和密封剂市场(按类型、技术、应用、树脂类型和地区划分)- 预测至 2030 年2025 年至 2033 年黏合剂和密封剂市场报告(按黏合剂类型、密封剂类型、技术、应用和地区划分)

全球黏合剂和密封剂市场(按类型、技术、应用、树脂类型和地区划分)- 预测至 2030 年2025 年至 2033 年黏合剂和密封剂市场报告(按黏合剂类型、密封剂类型、技术、应用和地区划分) 全球防水胶黏剂及密封剂市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球防水胶黏剂及密封剂市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测 黏合剂和密封剂市场规模、份额和趋势分析报告:按技术、产品、应用、地区和细分市场预测,2025 年至 2033 年

黏合剂和密封剂市场规模、份额和趋势分析报告:按技术、产品、应用、地区和细分市场预测,2025 年至 2033 年