|

市场调查报告书

商品编码

1801953

住宅太阳能光电逆变器市场机会、成长动力、产业趋势分析及2025-2034年预测Residential Solar PV Inverter Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

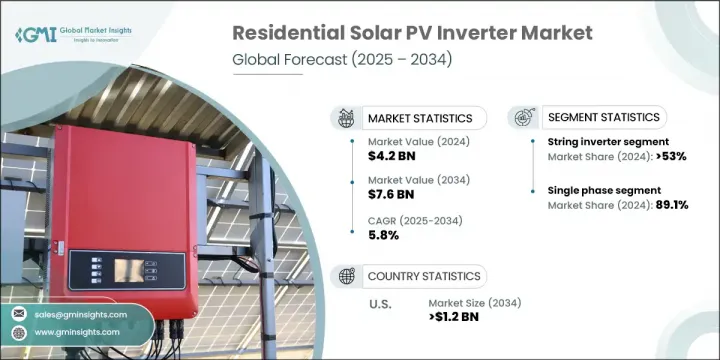

2024年,全球住宅太阳能光电逆变器市场规模达42亿美元,预计年复合成长率将达5.8%,2034年将达76亿美元。太阳能光电模组及相关技术价格的下降,以及政府透过补贴、回馈和税收优惠等方式提供的财政支持,推动了太阳能应用的稳定成长。与传统电网相关的公用事业成本不断上涨,促使房主探索替代能源,从而推高了对太阳能係统及光伏逆变器等配套产品的需求。

这些逆变器在将太阳能板的直流电转换为住宅电网使用的交流电方面发挥关键作用,同时也提供必要的安全性和监控功能。推广清洁能源的监管框架以及展示长期节能效益的宣传活动,进一步鼓励了住宅安装逆变器。产业领导者越来越多地采用尖端逆变器技术,以满足追求永续发展和能源独立的家庭日益增长的能源需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 42亿美元 |

| 预测值 | 76亿美元 |

| 复合年增长率 | 5.8% |

微型逆变器市场预计在2034年实现6%的复合年增长率,这得益于其面板级优化,即使在部分遮光的环境下也能确保更高的性能。简化的安装、低压设计和可扩展的架构使微型逆变器成为中小型住宅的理想选择,从而推动其更广泛的市场应用。

单相逆变器在2024年占了89.1%的市场份额,预计到2034年将以5.6%的复合年增长率成长。这些设备因其紧凑的设计、易于安装以及与普通住宅用电需求的兼容性而广受青睐。它们与储能係统和智慧能源平台的整合也满足了那些希望减少水电费并最大程度减少碳足迹的家庭日益增长的需求。随着太阳能+储能解决方案的普及,对能够在现代智慧家庭中无缝运行的单相逆变器的需求持续增长。

2024年,美国住宅太阳能光电逆变器市场占99.3%的市场份额,预计2034年将达到12亿美元。美国强劲的发展势头得益于再生能源强制令、税收优惠、净计量计划以及公用事业级补贴等优惠政策。这些措施正在鼓励大规模安装住宅太阳能係统。主要市场参与者对先进产品开发的投入,进一步支持了美国家庭向再生能源解决方案转型的长期成长。

住宅太阳能光电逆变器市场的知名公司包括阳光电源、Solar Edge Technologies, Inc.、西门子、施耐德电气、松下公司、INVERGY、华为技术有限公司、日立 Hi-Rel 电力电子私人有限公司、固德威、Goldi Solar、锦浪科技、通用电气、Fronius International GmbH、Fimer Group、伊顿电角、Enphase 电图、通用电气公司。领先的企业正在透过推动产品创新来巩固其市场地位,专注于与储存和物联网应用相容的紧凑、高效和智慧逆变器。企业正在积极投资研发,以增强安全功能、整合基于人工智慧的监控并提高每块面板的能量产量。与电池製造商和智慧家庭平台的合作正在创造符合不断变化的住宅能源需求的增值产品。企业也透过区域製造部门、分销合作伙伴关係和数位销售网络扩大其地理覆盖范围。

目录

第一章:方法论与范围

第二章:行业洞察

- 2021 - 2034 年产业概要

- 商业趋势

- 产品趋势

- 阶段趋势

- 区域趋势

第三章:行业洞察

- 产业生态系统分析

- 原料和零件供应商

- 逆变器製造商

- EPC和系统整合商

- 专案开发商和独立发电厂

- 2021-2034年价格趋势分析

- 按产品

- 按地区

- 成本结构分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- 供应商的议价能力

- 买家的议价能力

- 新进入者的威胁

- 替代品的威胁

- PESTEL分析

第四章:竞争格局

- 介绍

- 按地区分析公司市场份额

- 北美洲

- 欧洲

- 亚太地区

- 中东和非洲

- 拉丁美洲

- 战略仪表板

- 策略倡议

- 公司标竿分析

- 创新与技术格局

第五章:市场规模及预测:依产品,2021 - 2034

- 主要趋势

- 细绳

- 微

第六章:市场规模及预测:依阶段,2021 - 2034

- 主要趋势

- 单相

- 三相

第七章:市场规模及预测:依地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 义大利

- 波兰

- 荷兰

- 奥地利

- 英国

- 法国

- 亚太地区

- 中国

- 澳洲

- 印度

- 日本

- 韩国

- 中东和非洲

- 以色列

- 沙乌地阿拉伯

- 阿联酋

- 南非

- 埃及

- 奈及利亚

- 拉丁美洲

- 巴西

- 墨西哥

- 智利

第八章:公司简介

- Canadian Solar

- Darfon Electronics Corp.

- Delta Electronics, Inc.

- Enphase Energy

- Eaton

- Fimer Group

- Fronius International GmbH

- General Electric

- Ginlong Technologies

- Goldi Solar

- GoodWe

- Hitachi Hi-Rel Power Electronics Private Limited

- Huawei Technologies Co., Ltd.

- INVERGY

- Panasonic Corporation

- Schneider Electric

- Siemens

- SMA Solar Technology AG

- Servotech Power Systems

- Solar Edge Technologies, Inc.

- Sungrow

The Global Residential Solar PV Inverter Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 7.6 billion by 2034. A steady rise in solar energy adoption is being fueled by declining prices of panels and associated technologies, along with increasing availability of financial support through grants, rebates, and tax incentives. Escalating utility costs tied to conventional power grids are motivating homeowners to explore energy alternatives, pushing up demand for solar-powered systems and supporting products like PV inverters.

These inverters play a critical role in converting direct current from solar panels into alternating current used by residential electrical grids, while also providing essential safety and monitoring features. Regulatory frameworks promoting cleaner energy and awareness campaigns that showcase long-term savings are further encouraging residential installations. Industry leaders are increasingly adopting cutting-edge inverter technologies to meet the growing energy demands of households aiming for sustainability and energy independence.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $7.6 Billion |

| CAGR | 5.8% |

The micro inverter segment is poised for a CAGR of 6% through 2034, driven by its panel-level optimization, which ensures enhanced performance even in partially shaded installations. The simplified installation, low-voltage design, and scalable architecture make micro inverters ideal for small and mid-size homes, promoting wider market adoption.

The single-phase inverters captured 89.1% share in 2024 and is projected to grow at a CAGR of 5.6% through 2034. These units are widely favored due to their compact design, ease of installation, and compatibility with average residential power demands. Their integration with energy storage systems and intelligent energy platforms also supports growing interest from households looking to reduce utility bills and minimize their carbon footprint. As solar-plus-storage solutions gain traction, the demand for single-phase inverters that seamlessly operate within modern smart homes continues to rise.

United States Residential Solar PV Inverter Market held a 99.3% share in 2024 and is anticipated to reach USD 1.2 billion by 2034. The country's strong momentum is driven by favorable policies such as renewable energy mandates, tax incentives, net metering programs, and utility-level rebate offerings. These measures are encouraging the installation of residential solar systems at scale. The presence of major market players investing in advanced product development further supports long-term growth across US households transitioning toward renewable power solutions.

Prominent companies operating in the Residential Solar PV Inverter Market include Sungrow, Solar Edge Technologies, Inc., Siemens, Schneider Electric, Panasonic Corporation, INVERGY, Huawei Technologies Co., Ltd., Hitachi Hi-Rel Power Electronics Private Limited, GoodWe, Goldi Solar, Ginlong Technologies, General Electric, Fronius International GmbH, Fimer Group, Eaton, Enphase Energy, Delta Electronics, Inc., Darfon Electronics Corp., Canadian Solar, and Servotech Power Systems. Leading players are strengthening their market foothold by advancing product innovation, focusing on compact, high-efficiency, and smart inverters compatible with storage and IoT applications. Firms are actively investing in R&D to enhance safety features, integrate AI-based monitoring, and increase energy yield per panel. Collaborations with battery manufacturers and smart home platforms are creating value-added offerings that align with evolving residential energy needs. Companies are also expanding their geographic footprint through regional manufacturing units, distribution partnerships, and digital sales networks.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market Definitions

Chapter 2 Industry Insights

- 2.1 Industry synopsis, 2021 - 2034

- 2.2 Business trends

- 2.3 Product trends

- 2.4 Phase trends

- 2.5 Regional trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw materials & component suppliers

- 3.1.2 Inverter manufacturers

- 3.1.3 EPC & system integrators

- 3.1.4 Project developers & IPPs

- 3.2 Price trend analysis, 2021-2034

- 3.2.1 By product

- 3.2.2 By region

- 3.3 Cost structure analysis

- 3.4 Regulatory landscape

- 3.5 Industry impact forces

- 3.5.1 Growth drivers

- 3.5.2 Industry pitfalls & challenges

- 3.6 Growth potential analysis

- 3.7 Porter's analysis

- 3.7.1 Bargaining power of suppliers

- 3.7.2 Bargaining power of buyers

- 3.7.3 Threat of new entrants

- 3.7.4 Threat of substitutes

- 3.8 PESTEL analysis

- 3.8.1 Political factors

- 3.8.2 Economic factors

- 3.8.3 Social factors

- 3.8.4 Technological factors

- 3.8.5 Legal factors

- 3.8.6 Environmental factors

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, by region, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Middle East & Africa

- 4.2.5 Latin America

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.5 Company benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Billion & MW)

- 5.1 Key trends

- 5.2 String

- 5.3 Micro

Chapter 6 Market Size and Forecast, By Phase, 2021 - 2034 (USD Billion & MW)

- 6.1 Key trends

- 6.2 Single phase

- 6.3 Three phase

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Poland

- 7.3.4 Netherlands

- 7.3.5 Austria

- 7.3.6 UK

- 7.3.7 France

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Israel

- 7.5.2 Saudi Arabia

- 7.5.3 UAE

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.5.6 Nigeria

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Mexico

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 Canadian Solar

- 8.2 Darfon Electronics Corp.

- 8.3 Delta Electronics, Inc.

- 8.4 Enphase Energy

- 8.5 Eaton

- 8.6 Fimer Group

- 8.7 Fronius International GmbH

- 8.8 General Electric

- 8.9 Ginlong Technologies

- 8.10 Goldi Solar

- 8.11 GoodWe

- 8.12 Hitachi Hi-Rel Power Electronics Private Limited

- 8.13 Huawei Technologies Co., Ltd.

- 8.14 INVERGY

- 8.15 Panasonic Corporation

- 8.16 Schneider Electric

- 8.17 Siemens

- 8.18 SMA Solar Technology AG

- 8.19 Servotech Power Systems

- 8.20 Solar Edge Technologies, Inc.

- 8.21 Sungrow

太阳能逆变器市场:按产品、组件、类型、相数、输出、销售管道和应用划分-2026-2032年全球市场预测太阳能逆变器市场:2026-2032年全球市场预测(依逆变器类型、相数、额定输出、系统类型、输出电压、应用、安装方式及销售管道)太阳能逆变器测试解决方案市场:按应用、逆变器类型、输出额定值和测试类型划分,全球预测(2026-2032年)

太阳能逆变器市场:按产品、组件、类型、相数、输出、销售管道和应用划分-2026-2032年全球市场预测太阳能逆变器市场:2026-2032年全球市场预测(依逆变器类型、相数、额定输出、系统类型、输出电压、应用、安装方式及销售管道)太阳能逆变器测试解决方案市场:按应用、逆变器类型、输出额定值和测试类型划分,全球预测(2026-2032年) 太阳能逆变器市场机会、成长要素、产业趋势分析及2026年至2035年预测。

太阳能逆变器市场机会、成长要素、产业趋势分析及2026年至2035年预测。 太阳能逆变器:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

太阳能逆变器:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 2026-2034年全球商用和工业用太阳能逆变器市场规模、份额、趋势和成长分析报告2026-2034年全球独立式太阳能逆变器市场规模、份额、趋势和成长分析报告全球太阳能微型逆变器市场规模、份额、趋势和成长分析报告(2026-2034年)全球太阳能逆变器市场规模、份额、趋势和成长分析报告(2026-2034)

2026-2034年全球商用和工业用太阳能逆变器市场规模、份额、趋势和成长分析报告2026-2034年全球独立式太阳能逆变器市场规模、份额、趋势和成长分析报告全球太阳能微型逆变器市场规模、份额、趋势和成长分析报告(2026-2034年)全球太阳能逆变器市场规模、份额、趋势和成长分析报告(2026-2034) 日本太阳能逆变器市场规模、份额、趋势和预测:按逆变器类型、应用和地区划分,2026-2034年

日本太阳能逆变器市场规模、份额、趋势和预测:按逆变器类型、应用和地区划分,2026-2034年