|

市场调查报告书

商品编码

1822645

乙太网路供电 (PoE) 解决方案市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Power over Ethernet (PoE) Solution Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

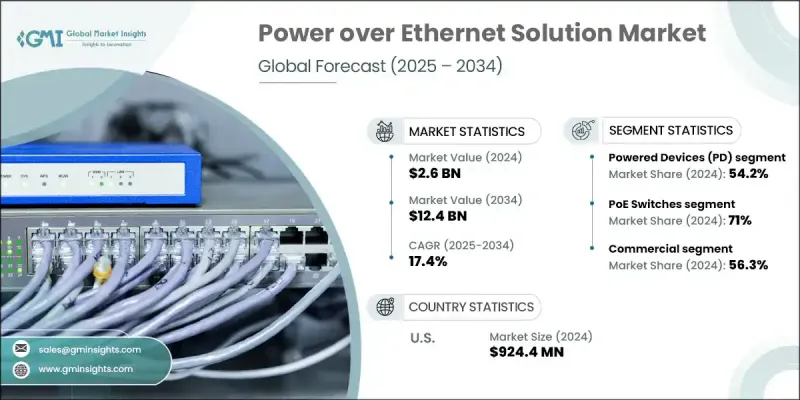

2024 年全球乙太网路网路供电解决方案市值为 26 亿美元,预计到 2034 年将以 17.4% 的复合年增长率成长,达到 124 亿美元。

这一强劲的成长前景主要源自于全球范围内对更智慧、更节能基础设施的日益追求。 PoE 已成为楼宇现代化的关键推动因素,它提供了一种经济高效且简化的方式,可透过单一乙太网路电缆传输电力和资料。这种方法使智慧型设备(例如照明系统、摄影机和感测器)无需传统电线即可运行,从而降低了复杂性和安装成本。各行各业的组织都开始将 PoE 作为一种灵活的解决方案,用于改造和新建智慧基础设施项目,尤其是在他们寻求简化营运和增强楼宇智慧化方面。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 26亿美元 |

| 预测值 | 124亿美元 |

| 复合年增长率 | 17.4% |

人们对安全和自动化日益增长的关注进一步加速了PoE的部署。基于PoE技术的IP监控解决方案的日益普及,简化了安装过程,并显着降低了部署成本。这些系统允许透过单线传输视讯资料和电力,从而减少了对劳动力和基础设施的需求。同时,在工业4.0实务的推动下,工业领域对物联网设备的需求显着成长。从生产车间到物流中心,工厂配备了智慧感测器和连网工具,这些都需要不间断的电力和资料流。 PoE如今在实现工业环境中无缝、低延迟的通讯和运作方面发挥着至关重要的作用,无需大量重新布线即可提供可靠性。

2024年,受电设备 (PD) 细分市场以 54.2% 的市占率领先乙太网路网路供电解决方案市场,预计到 2034 年复合年增长率将达到 19%。物联网技术在智慧建筑、互联城市基础设施和工业自动化领域的快速应用推动了这一成长。安防系统、智慧感测器和门禁单元等受电设备越来越多地采用 PoE 供电,不仅支援高效的能源传输,还支援稳定的资料通讯。製造商正在推动多功能产品设计,以支援时尚、节省空间的安装,同时满足现代科技需求。

PoE 交换器市场在 2024 年占据 71% 的市场份额,预计在 2025 年至 2034 年期间的复合年增长率将达到 10.4%。企业在扩展其智慧基础设施(尤其是在办公环境、安防系统和智慧设施管理方面)时,正积极采用 16 至 48 个连接埠的管理型交换器。这些交换器提供 VLAN 分段、服务品质 (QoS) 和远端诊断等进阶网路功能。对高功率设备日益增长的需求也推动了符合 IEEE 802.3bt 标准的交换器的采用,该标准支援集中电源控制,并可在广泛的设备生态系统中提高效率。

美国乙太网路供电 (PoE) 解决方案市场占 86.2% 的市场份额,2024 年市场规模达 9.244 亿美元。其领先地位得益于先进的数位基础设施、智慧技术的快速部署以及 VoIP、无线存取点和先进监控设备等 IP 供电系统的广泛应用。美国政府推动能源效率和智慧城市框架的倡议,进一步加速了 PoE 在住宅、商业和公共部门计画中的普及。此外,消费者的高认知度和对联网节能係统的强劲需求,使美国成为该地区的关键成长动力。

影响全球乙太网路供电 (PoE) 解决方案市场的关键参与者包括意法半导体 (STMicroelectronics)、博通 (Broadcom)、惠普企业 (HPE)、思科系统 (Cisco Systems)、百通 (Belden)、德州仪器 (Texas Instruments)、ADI 公司、Silicon Laboratories、康芯科技公司 (Commpance)。乙太网路解决方案市场的领导公司正透过创新、策略合作和全球扩张等方式巩固其地位。许多公司正在大力投资研发,以支援 IEEE 802.3bt 等不断发展的标准,并提高下一代智慧型装置的功率输出。扩展产品线以包括针对工业和商业应用量身定制的高端口数交换机和混合系统是另一个优先事项。各公司也正在配合智慧城市计划,并与物联网设备製造商合作,以确保无缝整合和互通性。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 供应链弹性分析

- 半导体依赖关係映射

- 关键部件短缺的影响

- 替代采购策略

- 通路伙伴生态系统

- 系统整合商格局

- VAR/经销商网路分析

- 直接与间接销售模式

- 产业衝击力

- 成长动力

- 物联网和智慧建筑应用激增

- 集中网路管理需求不断成长

- 扩充需要 PoE++ (802.3bt) 的高功率设备

- 安装和维护的成本效益

- 产业陷阱与挑战

- 电缆长度有限(乙太网路限制为 100 公尺)

- 设备相容性和功率限制

- 市场机会

- 进军高成长地区

- 远距和全球劳动力

- 进阶分析和人工智慧

- 雇主品牌服务

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 技术演进路线图

- 下一代 PoE 标准(超越 802.3bt)

- 电力传输效率的提高

- 与再生能源的整合

- 无线电力传输融合

- 区域创新中心分析

- 硅谷技术领导力

- 欧洲可持续发展标准的影响

- 亚洲製造业卓越中心

- 新兴市场的跨越式发展机会

- 关键参与者的创新管道分析

- 专利格局

- 专利集群和技术护城河

- 成本分解分析

- 客户获取成本分析

- 最终使用者情绪和采用障碍

- IT决策者调查洞察

- ROI计算方法

- 从遗留系统迁移的挑战

- 供应商选择标准分析

- 新兴商业模式

- PoE 即服务 (PaaS) 模型

- 託管 PoE 基础设施服务

- 基于订阅的电源管理

- 能源共享和併网机会

- 用例

- 最佳情况

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 多边环境协定

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重要新闻和倡议

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:依组件划分,2021 - 2034 年

- 主要趋势

- 电源设备 (PSE)

- 末端跨度

- 中跨

- 受电设备(PD)

- IP摄影机

- 网路电话

- 无线存取点

- 网路交换机

- 瘦客户端

- 智慧照明

第六章:市场估计与预测:按类型,2021 - 2034

- 主要趋势

- PoE交换机

- 未託管

- 託管

- PoE转换器

- PoE供电器

- PoE 扩展器/中继器

- PoE 分配器

第七章:市场估计与预测:依标准,2021 - 2034

- 主要趋势

- IEEE 802.3af (PoE) - 高达 15.4W

- IEEE 802.3at (PoE+) - 高达 30W

- IEEE 802.3bt (PoE++/4PPoE) - 高达 60-100W

第 8 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 商业的

- 住宅

- 工业的

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧人

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- 全球参与者

- Analog Devices

- Broadcom

- Cisco Systems

- Dell Technologies

- D-Link

- HPE (Hewlett Packard Enterprise)

- Huawei Technologies

- Juniper Networks

- Microchip Technology

- NETGEAR

- ON Semiconductor

- STMicroelectronics

- Texas Instruments

- TP-Link Technologies

- 关键参与者

- Axis Communications

- Belden

- CommScope Holding Company

- Hubbell

- Moxa

- Phihong Technology

- Signify Holding

- Ubiquiti

- Technology Innovators

- Analog Devices

- Kinetic Technologies Holdings

- Maxim Integrated Products

- Microchip Technology

- Monolithic Power Systems

- Silicon Laboratories

The Global Power over Ethernet Solution Market was valued at USD 2.6 billion in 2024 and is estimated to grow at a CAGR of 17.4% to reach USD 12.4 billion by 2034.

This strong growth outlook is primarily driven by the rising push toward smarter, energy-efficient infrastructure worldwide. PoE has become a key enabler in modernizing buildings by offering a cost-effective and simplified way to deliver both power and data over a single Ethernet cable. This method allows smart devices-like lighting systems, cameras, and sensors-to operate without the need for traditional electrical wiring, reducing complexity and installation costs. Organizations across sectors are turning to PoE as a flexible solution for both retrofit and new smart infrastructure projects, especially as they seek to streamline operations and enhance building intelligence.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.6 Billion |

| Forecast Value | $12.4 Billion |

| CAGR | 17.4% |

Growing attention to security and automation has further accelerated PoE deployment. The rising adoption of IP-based surveillance solutions that rely on PoE technology is simplifying installations while significantly lowering deployment expenses. These systems allow video data and power to be transmitted via a single line, cutting down on labor and infrastructure needs. In parallel, the industrial sector is seeing a notable rise in demand for IoT-enabled devices, fueled by Industry 4.0 practices. From manufacturing floors to logistics hubs, factories equip themselves with smart sensors and networked tools that require uninterrupted power and data flow. PoE is now playing a vital role in enabling seamless, low-latency communication and operation across industrial environments, offering reliability without extensive rewiring.

In 2024, the Powered Devices (PD) segment led the Power over Ethernet Solution Market with a 54.2% share and is projected to register a CAGR of 19% through 2034. The rapid adoption of IoT technologies across smart buildings, connected city infrastructure, and industrial automation is fueling this growth. Powered devices such as security systems, smart sensors, and access control units are increasingly designed to run on PoE, which supports not only efficient energy transfer but also consistent data communication. Manufacturers are pushing multifunctional product designs that support sleek, space-saving installations while aligning with modern tech preferences.

The PoE switches segment held a 71% share in 2024 and is forecast to grow at a CAGR of 10.4% between 2025 and 2034. Enterprises are embracing managed switches with 16 to 48 ports as they scale their smart infrastructure, particularly in office settings, security systems, and smart facility management. These switches offer advanced network features like VLAN segmentation, Quality of Service (QoS), and remote diagnostics. The growing demand for high-power devices is also pushing the adoption of switches compliant with the IEEE 802.3bt standard, which enables centralized power control and greater efficiency across expansive device ecosystems.

United States Power over Ethernet (PoE) Solution Market held an 86.2% share, generating USD 924.4 million in 2024. This leadership is supported by an advanced digital infrastructure, rapid deployment of smart technologies, and widespread use of IP-powered systems such as VoIP, wireless access points, and advanced surveillance devices. US government initiatives promoting energy efficiency and smart city frameworks are further accelerating PoE adoption across residential, commercial, and public sector projects. Additionally, high consumer awareness and strong demand for networked, power-efficient systems position the country as a key growth driver in the region.

Key players shaping the Global Power over Ethernet (PoE) Solution Market include STMicroelectronics, Broadcom, Hewlett Packard Enterprise (HPE), Cisco Systems, Belden, Texas Instruments, Analog Devices, Silicon Laboratories, CommScope, and Microchip Technology. Leading companies in the power over Ethernet solution market are strengthening their foothold through a combination of innovation, strategic collaborations, and global expansion. Many are investing heavily in R&D to support evolving standards like IEEE 802.3bt and to improve power output for next-gen smart devices. Expanding product lines to include high-port-count switches and hybrid systems tailored for industrial and commercial applications is another priority. Companies are also aligning with smart city initiatives and partnering with IoT device manufacturers to ensure seamless integration and interoperability.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Engagement model

- 2.2.3 Organization size

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Supply Chain Resilience Analysis

- 3.2.1 Semiconductor dependency mapping

- 3.2.2 Critical component shortage impact

- 3.2.3 Alternative sourcing strategies

- 3.3 Channel Partner Ecosystem

- 3.3.1 Systems integrators landscape

- 3.3.2 VAR/distributor network analysis

- 3.3.3 Direct vs. indirect sales models

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.1.1 Surge in IoT and Smart Building Adoption

- 3.4.1.2 Rising Demand for Centralized Network Management

- 3.4.1.3 Expansion of High-Power Devices Requiring PoE++ (802.3bt)

- 3.4.1.4 Cost Efficiency in Installation and Maintenance

- 3.4.2 Industry pitfalls and challenges

- 3.4.2.1 Limited Cable Length (100m Ethernet Limit)

- 3.4.2.2 Device Compatibility and Power Limitations

- 3.4.3 Market opportunities

- 3.4.3.1 Taps into high-growth regions

- 3.4.3.2 Remote & Global Workforce

- 3.4.3.3 Advanced Analytics & AI

- 3.4.3.4 Employer Branding Services

- 3.4.1 Growth drivers

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East & Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.9.3 Technology Evolution Roadmap

- 3.9.3.1 Next-Generation PoE Standards (Beyond 802.3bt)

- 3.9.3.2 Power Delivery Efficiency Improvements

- 3.9.3.3 Integration with Renewable Energy Sources

- 3.9.3.4 Wireless Power Transmission Convergence

- 3.9.4 Regional Innovation Hubs Analysis

- 3.9.4.1 Silicon Valley Technology Leadership

- 3.9.4.2 European Sustainability Standards Impact

- 3.9.4.3 Asian Manufacturing Excellence Centers

- 3.9.4.4 Emerging Market Leapfrog Opportunities

- 3.9.5 Innovation Pipeline Analysis by Key Players

- 3.10 Patent landscape

- 3.10.1 Patent Clustering and Technology Moats

- 3.11 Cost breakdown analysis

- 3.12 Customer Acquisition Cost Analysis

- 3.13 End Use Sentiment and Adoption Barriers

- 3.13.1 IT Decision Maker Survey Insights

- 3.13.2 ROI Calculation Methodologies

- 3.13.3 Migration from Legacy Systems Challenges

- 3.13.4 Vendor Selection Criteria Analysis

- 3.14 Emerging Business Models

- 3.14.1 PoE-as-a-Service (PaaS) Models

- 3.14.2 Managed PoE Infrastructure Services

- 3.14.3 Subscription-Based Power Management

- 3.14.4 Energy-Sharing and Grid-Tie Opportunities

- 3.15 Use cases

- 3.16 Best-case scenario

- 3.17 Sustainability and environmental aspects

- 3.17.1 Sustainable practices

- 3.17.2 Waste reduction strategies

- 3.17.3 Energy efficiency in production

- 3.17.4 Eco-friendly Initiatives

- 3.17.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Power sourcing equipment (PSE)

- 5.2.1 Endspan

- 5.2.2 Midspan

- 5.3 Powered devices (PD)

- 5.3.1 IP cameras

- 5.3.2 VOIP phones

- 5.3.3 Wireless access points

- 5.3.4 Network switches

- 5.3.5 Thin clients

- 5.3.6 Smart lighting

Chapter 6 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 PoE Switches

- 6.2.1 Unmanaged

- 6.2.2 Managed

- 6.3 PoE Converters

- 6.4 PoE Injectors

- 6.5 PoE Extenders/Repeaters

- 6.6 PoE Splitters

Chapter 7 Market Estimates & Forecast, By Standard, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 IEEE 802.3af (PoE) - Up to 15.4W

- 7.3 IEEE 802.3at (PoE+) - Up to 30W

- 7.4 IEEE 802.3bt (PoE++/4PPoE) - Up to 60-100W

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Commercial

- 8.3 Residential

- 8.4 Industrial

- 8.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Analog Devices

- 10.1.2 Broadcom

- 10.1.3 Cisco Systems

- 10.1.4 Dell Technologies

- 10.1.5 D-Link

- 10.1.6 HPE (Hewlett Packard Enterprise)

- 10.1.7 Huawei Technologies

- 10.1.8 Juniper Networks

- 10.1.9 Microchip Technology

- 10.1.10 NETGEAR

- 10.1.11 ON Semiconductor

- 10.1.12 STMicroelectronics

- 10.1.13 Texas Instruments

- 10.1.14 TP-Link Technologies

- 10.2 Key Players

- 10.2.1 Axis Communications

- 10.2.2 Belden

- 10.2.3 CommScope Holding Company

- 10.2.4 Hubbell

- 10.2.5 Moxa

- 10.2.6 Phihong Technology

- 10.2.7 Signify Holding

- 10.2.8 Ubiquiti

- 10.3 Technology Innovators

- 10.3.1 Analog Devices

- 10.3.2 Kinetic Technologies Holdings

- 10.3.3 Maxim Integrated Products

- 10.3.4 Microchip Technology

- 10.3.5 Monolithic Power Systems

- 10.3.6 Silicon Laboratories

电信级乙太网路接取设备市场:依产品类型、连接埠速度、部署模式、应用程式和最终用户划分-2026-2032年全球市场预测都会乙太网路市场:按连线类型、频宽、服务类型和产业划分 - 2026-2032 年全球预测LAN脉衝变压器市场按传输速率、产品类型、应用和最终用户划分,全球预测(2026-2032)

电信级乙太网路接取设备市场:依产品类型、连接埠速度、部署模式、应用程式和最终用户划分-2026-2032年全球市场预测都会乙太网路市场:按连线类型、频宽、服务类型和产业划分 - 2026-2032 年全球预测LAN脉衝变压器市场按传输速率、产品类型、应用和最终用户划分,全球预测(2026-2032) 乙太网路供电 (PoE) 市场 - 全球产业规模、份额、趋势、机会、预测:按产品类型、组件、最终用户、地区和竞争对手划分,2021-2031 年Thunderbolt 3 和 Thunderbolt 4 扩充座市场:按连接器类型、供电方式、显示支援、价格范围、外形规格、连接埠支援和最终用途划分-2026 年至 2032 年全球预测乙太网路磁性变压器市场按产品、传输速度、安装类型、整合类型和最终用户产业划分,全球预测,2026-2032年

乙太网路供电 (PoE) 市场 - 全球产业规模、份额、趋势、机会、预测:按产品类型、组件、最终用户、地区和竞争对手划分,2021-2031 年Thunderbolt 3 和 Thunderbolt 4 扩充座市场:按连接器类型、供电方式、显示支援、价格范围、外形规格、连接埠支援和最终用途划分-2026 年至 2032 年全球预测乙太网路磁性变压器市场按产品、传输速度、安装类型、整合类型和最终用户产业划分,全球预测,2026-2032年 都会乙太网路市场规模、份额和成长分析(按服务类型、企业规模、服务产品、频宽范围、应用、最终用户和地区划分)—产业预测(2026-2033 年)

都会乙太网路市场规模、份额和成长分析(按服务类型、企业规模、服务产品、频宽范围、应用、最终用户和地区划分)—产业预测(2026-2033 年) EtherCAT 全球市场规模、份额、行业分析报告:2025 年至 2032 年按组件、设备类型、最终用途和地区分類的展望和预测

EtherCAT 全球市场规模、份额、行业分析报告:2025 年至 2032 年按组件、设备类型、最终用途和地区分類的展望和预测 EtherCAT 市场规模、份额和趋势分析报告:按组件、设备类型、最终用途、地区和细分市场预测,2025 年至 2033 年

EtherCAT 市场规模、份额和趋势分析报告:按组件、设备类型、最终用途、地区和细分市场预测,2025 年至 2033 年 全球乙太网路隔离器市场

全球乙太网路隔离器市场