|

市场调查报告书

商品编码

1822654

汽油直喷 (GDI) 系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Gasoline Direct Injection (GDI) System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

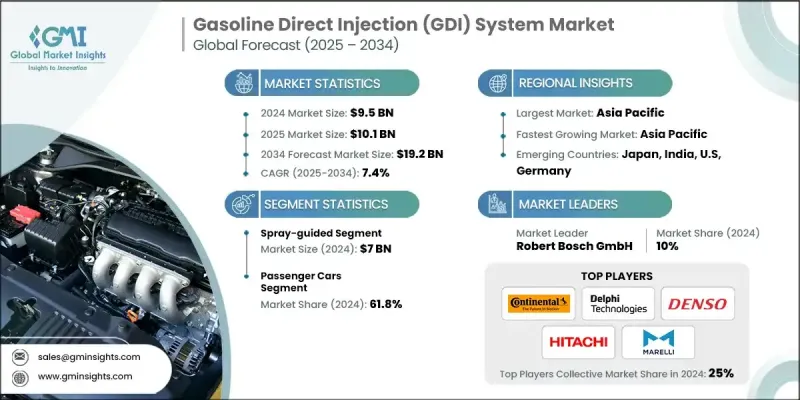

2024 年全球汽油直喷 (GDI) 系统市场价值为 95 亿美元,预计在 GDI 技术的持续创新和消费者对高性能汽车日益增长的推动下,该市场将以 7.4% 的复合年增长率增长,到 2034 年达到 192 亿美元。 GDI 系统的进步,例如增强的燃油喷射器和改进的燃烧控制,正在提高引擎效率和性能。同时,消费者越来越优先考虑具有卓越动力、反应能力和燃油经济性的汽车。对高性能、高效能汽车的这种日益增长的需求推动了 GDI 系统的采用。 2024 年 1 月,GB Remanufacturing, Inc. 透过推出 17 个新零件(包括密封套件、多件装、喷射器和高级密封件更换工具包)增强了其汽油直喷计划。此举凸显了该产业对维护和升级 GDI 系统的日益重视。

汽油直喷系统产业份额按组件、应用和地区细分。到 2032 年,燃油喷射器市场有望实现显着成长,这得益于其在提高引擎性能和燃油效率方面的关键作用。燃油喷射器确保将燃油精确输送到燃烧室,从而实现更好的燃烧控制并最大限度地减少排放。随着汽车製造商越来越多地采用 GDI 技术来遵守严格的燃油效率和排放标准,对先进燃油喷射器的需求正在上升。商用车市场将为 GDI 系统产业带来可观的收益,这得益于重型应用中对省油、高性能引擎日益增长的需求。 GDI 系统以其更高的燃油经济性和更低的排放而闻名,非常适合需要强劲引擎并遵守严格环保标准的商用车。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 95亿美元 |

| 预测值 | 192亿美元 |

| 复合年增长率 | 7.4% |

随着全球物流和运输业的扩张,商用车对先进引擎技术的追求进一步扩大了汽油直喷 (GDI) 系统的采用。预计到2032年,亚太地区汽油直喷系统市场将保持显着份额,这得益于该地区蓬勃发展的汽车产业以及对节能汽车日益增长的需求。主要汽车製造商的入驻以及尖端引擎技术的迅速采用推动了这一增长。此外,政府倡议的燃油效率和减排措施进一步促进了GDI系统的普及。凭藉其强大的製造业基础和快速的技术进步,亚太地区在全球汽油直喷 (GDI) 系统领域占据着举足轻重的地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 节能高性能汽车的普及率不断提高

- 严格的排放法规

- 技术进步

- 产业陷阱与挑战

- 积碳问题

- 排放问题

- 机会

- 先进控制系统的集成

- 与替代燃料的兼容性

- 成长动力

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按类型

- 监管格局

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 - 2034

- 主要趋势

- 壁面引导

- 喷雾引导

第六章:市场估计与预测:按组件,2021 - 2034

- 主要趋势

- 燃油帮浦

- 燃油喷射器

- 电子控制单元

- 燃油导轨

- 其他的

第七章:市场估计与预测:按车辆类型,2021 - 2034 年

- 主要趋势

- 传统汽油动力汽车

- 油电混合车

第 8 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 轻型商用车

第九章:市场估计与预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Aisin Seiki Co Ltd

- BorgWarner Inc

- Continental AG

- Delphi Technologies

- Denso

- Hitachi

- Infineon Technologies AG

- Keihin Corporation

- Marelli

- Park Ohio Holdings Corp

- PHINIA

- Robert Bosch GmbH

- Stanadyne LLC

- Standard Ignition

- TI Fluid Systems

The Global Gasoline Direct Injection (GDI) System Market was valued at USD 9.5 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 19.2 billion by 2034 driven by continuous innovations in GDI technology and rising consumer preference for high-performance vehicles. Advancements in GDI systems, such as enhanced fuel injectors and improved combustion control, are driving greater engine efficiency and performance. Concurrently, consumers are increasingly prioritizing vehicles that deliver superior power, responsiveness, and fuel economy. This heightened demand for high-performance, efficient vehicles is propelling the adoption of GDI systems. In January 2024, GB Remanufacturing, Inc. bolstered its Gasoline Direct Injection program by introducing 17 new parts, including seal kits, multi-packs, injectors, and a premium seal replacement tool kit. This move underscores the industry's growing emphasis on maintaining and upgrading GDI systems.

The gasoline direct injection system industry share is segmented by component, application, and region. By 2032, the fuel injectors segment is poised for significant growth, thanks to their pivotal role in enhancing engine performance and fuel efficiency. Fuel injectors ensure precise fuel delivery into the combustion chamber, leading to better combustion control and minimized emissions. With automakers increasingly turning to GDI technology to adhere to stringent fuel efficiency and emission standards, the demand for advanced fuel injectors is on the rise. The commercial vehicle segment is set to offer substantial gains to the GDI system industry, driven by the escalating demand for fuel-efficient, high-performance engines in heavy-duty applications. GDI systems, known for their enhanced fuel economy and lower emissions, are perfectly suited for commercial vehicles that need robust engines while adhering to strict environmental standards.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.5 Billion |

| Forecast Value | $19.2 Billion |

| CAGR | 7.4% |

As global logistics and transportation sectors expand, the push for advanced engine technologies in commercial vehicles amplifies the adoption of GDI systems. Through 2032, the Asia Pacific gasoline direct injection system market is expected to maintain a significant share, fueled by the region's thriving automotive sector and a growing appetite for fuel-efficient vehicles. The growth is driven by the presence of major automotive manufacturers and the swift adoption of cutting-edge engine technologies. Additionally, government initiatives championing fuel efficiency and emissions reduction further catalyze the uptake of GDI systems. With its robust manufacturing foundation and rapid technological advancements, Asia Pacific stands as a pivotal player in the global gasoline direct injection (GDI) system arena.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Component

- 2.2.4 Vehicle type

- 2.2.5 Application

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of energy-efficient and high-performance vehicles

- 3.2.1.2 Stringent emission regulations

- 3.2.1.3 Technological advancements

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 Carbon buildup concerns

- 3.2.2.2 Emission concerns

- 3.2.3 Opportunities

- 3.2.3.1 Integration of advanced control systems

- 3.2.3.2 Compatibility with alternative fuels

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Units)

- 5.1 Key trends

- 5.2 Wall-guided

- 5.3 Spray-guided

Chapter 6 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Billion) (Units)

- 6.1 Key trends

- 6.2 Fuel pump

- 6.3 Fuel injector

- 6.4 Electronic control unit

- 6.5 Fuel rail

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Vehicle Type, 2021 - 2034 (USD Billion) (Units)

- 7.1 Key trends

- 7.2 Conventional gasoline-powered vehicles

- 7.3 Hybrid vehicles

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Units)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.3 Light commercial vehicles

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Aisin Seiki Co Ltd

- 10.2 BorgWarner Inc

- 10.3 Continental AG

- 10.4 Delphi Technologies

- 10.5 Denso

- 10.6 Hitachi

- 10.7 Infineon Technologies AG

- 10.8 Keihin Corporation

- 10.9 Marelli

- 10.10 Park Ohio Holdings Corp

- 10.11 PHINIA

- 10.12 Robert Bosch GmbH

- 10.13 Stanadyne LLC

- 10.14 Standard Ignition

- 10.15 TI Fluid Systems

汽油缸内直喷系统市场:2026-2032年全球市场预测(依车辆类型、引擎排气量、喷射压力范围、喷射方式及销售管道)

汽油缸内直喷系统市场:2026-2032年全球市场预测(依车辆类型、引擎排气量、喷射压力范围、喷射方式及销售管道) 汽油缸内直喷市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测

汽油缸内直喷市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测 2026年全球缸内喷油(GDI)设备市场报告

2026年全球缸内喷油(GDI)设备市场报告 GDI系统市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、类型、销售管道、地区和竞争格局划分,2021-2031年)

GDI系统市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、类型、销售管道、地区和竞争格局划分,2021-2031年) 2026-2030年全球缸内喷油(GDI)系统市场缸内喷油管市场依产品类型、材料、压力范围、车辆类型及销售管道,全球预测,2026-2032年

2026-2030年全球缸内喷油(GDI)系统市场缸内喷油管市场依产品类型、材料、压力范围、车辆类型及销售管道,全球预测,2026-2032年 缸内喷油系统市场规模、份额和成长分析(按衝程、引擎类型、零件、车辆类型和地区划分)-2026-2033年产业预测汽油直喷市场-全球产业规模、份额、趋势、机会和预测,按组件、支援技术、车辆类型、地区和竞争格局划分,2020-2030年预测

缸内喷油系统市场规模、份额和成长分析(按衝程、引擎类型、零件、车辆类型和地区划分)-2026-2033年产业预测汽油直喷市场-全球产业规模、份额、趋势、机会和预测,按组件、支援技术、车辆类型、地区和竞争格局划分,2020-2030年预测 全球缸内喷油系统市场

全球缸内喷油系统市场 汽油直喷市场,按组件、按车辆、按支援技术、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测

汽油直喷市场,按组件、按车辆、按支援技术、按国家和地区划分 - 2024-2032 年行业分析、市场规模、市场份额和预测