|

市场调查报告书

商品编码

1833407

胰岛素笔市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Insulin Pen Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

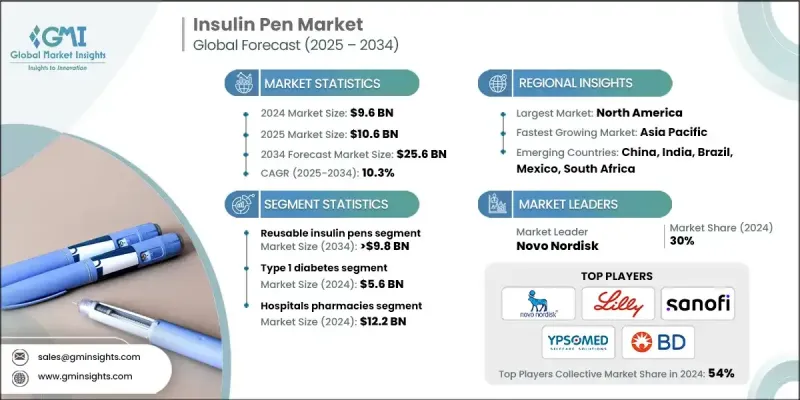

2024 年全球胰岛素笔市场价值为 96 亿美元,预计到 2034 年将以 10.3% 的复合年增长率增长至 256 亿美元。

在全球范围内,1型和第2型糖尿病患者数量的不断增加是胰岛素笔需求成长的主要驱动力。随着糖尿病患者人数的持续增长,尤其是在城市地区和老龄化人口中,对便捷可靠的胰岛素注射方法的需求也日益增长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 96亿美元 |

| 预测值 | 256亿美元 |

| 复合年增长率 | 10.3% |

可重复使用胰岛素笔部分

由于对经济高效、可持续且用户友好的胰岛素注射装置的需求不断增长,可重复使用胰岛素笔市场正经历强劲增长。与一次性胰岛素注射装置相比,可重复使用胰岛素笔具有长期经济效益,推动了这一成长。这些注射笔深受需要每日多次注射的患者的青睐,因为它们支持精准剂量,并且相容于多种胰岛素笔芯。

1 型糖尿病盛行率不断上升

2024年,第1型糖尿病市场占了强劲的份额。由于第1型糖尿病患者需要终生胰岛素治疗,因此对高效、便携且隐藏的胰岛素给药方法的需求持续增长。胰岛素笔,尤其是具有智慧剂量功能的胰岛素笔,由于使用方便且训练需求低,非常适合这类族群。

医院药局采用率不断上升

2024年,医院药局在急诊和新诊断患者中占据了相当大的份额。标准化剂量、感染控制和易于员工培训推动了这一成长。医院更青睐胰岛素笔,因为它安全可靠,并能降低剂量错误的风险。製造商正透过提供大包装解决方案、医院员工培训模组和延长保质期的产品来满足机构需求。

北美胰岛素笔市场

2024年,北美胰岛素笔市场保持了可持续的份额。高糖尿病盛行率、先进的医疗基础设施以及广泛的保险覆盖是支持该地区市场主导地位的关键因素。美国正大力推广智慧胰岛素笔和简化糖尿病管理的数位健康平台。为了巩固市场地位,各公司正利用直接面向消费者的行销方式,扩大透过零售药局的分销管道,并加强病患支援计画。

胰岛素笔市场的主要参与者包括Medmix、Julphar、东宝药业、赛诺菲、甘李药业、诺和诺德、Owen Mumford、Haselmeier、Ypsomed、Biocon Biologics、礼来公司、美敦力、Wockhardt、Becton、Dickinson and Company和苏州鹏业医疗器材。

为了巩固市场地位,胰岛素笔市场的领先公司高度重视创新、策略合作伙伴关係以及以患者为中心的解决方案。许多公司正在投资智慧胰岛素笔技术,整合蓝牙连接、剂量记忆和行动应用程式同步功能,以提供更优质的糖尿病管理工具。与数位健康平台和血糖监测公司的合作也有助于建立更一体化的医疗生态系统。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 糖尿病盛行率上升

- 胰岛素笔的技术进步

- 增强糖尿病自我管理意识

- 产业陷阱与挑战

- 胰岛素笔成本高

- 低收入地区渗透率有限

- 市场机会

- 智慧功能与数位平台的整合

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 当前的技术趋势

- 新兴技术

- 未来市场趋势

- 定价分析

- 按类型

- 按地区

- 报销情况

- 专利分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 亚太地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 - 2034

- 主要趋势

- 可重复使用的胰岛素笔

- 一次性胰岛素笔

第六章:市场估计与预测:按适应症,2021 - 2034 年

- 主要趋势

- 1型糖尿病

- 2型糖尿病

- 妊娠糖尿病

第七章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 电子商务

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Becton, Dickinson and Company

- Biocon Biologics

- Dongbao Pharmaceutical

- Eli Lilly and Co

- Gan & Lee Pharmaceuticals

- Haselmeier

- Julphar

- Medmix

- Medtronic

- Novo Nordisk

- Owen Mumford

- Sanofi

- Suzhou Peng Ye Medical Devices

- Wockhardt

- Ypsomed

The Global Insulin Pen Market was valued at USD 9.6 billion in 2024 and is estimated to grow at a CAGR of 10.3% to reach USD 25.6 billion by 2034.

The increasing number of people diagnosed with both Type 1 and Type 2 diabetes worldwide is a primary driver of insulin pen demand. As the diabetic population continues to grow, particularly in urban areas and among aging demographics, the need for convenient and reliable insulin delivery methods is escalating.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.6 Billion |

| Forecast Value | $25.6 Billion |

| CAGR | 10.3% |

Reusable Insulin Pens Segment

The reusable insulin pens segment is experiencing robust growth due to rising demand for cost-effective, sustainable, and user-friendly insulin delivery devices. The growth is driven by the long-term economic benefits reusable pens offer compared to disposable models. These pens are favored by patients requiring multiple daily injections, as they support dose precision and are compatible with a wide range of insulin cartridges.

Increasing Prevalence of Type 1 Diabetes Segment

The Type 1 diabetes segment held a robust share in 2024. As individuals with Type 1 diabetes require lifelong insulin therapy, there is a continuous need for efficient, portable, and discreet insulin delivery methods. Insulin pens, particularly those with smart dosing capabilities, are well-suited to this population due to their convenience and minimal training requirements.

Rising Adoption in Hospital Pharmacies

The hospital pharmacies segment held a sizeable share in 2024 in acute care settings and for newly diagnosed patients. The growth is driven by standardized dosing, infection control, and ease of staff training. Hospitals prefer insulin pens for their safety features and reduced risk of dosage errors. Manufacturers are responding by offering bulk packaging solutions, training modules for hospital staff, and extended shelf-life products to meet institutional needs.

North America Insulin Pen Market

North America insulin pen market held a sustainable share in 2024. High diabetes prevalence, advanced healthcare infrastructure, and widespread insurance coverage are key factors supporting this region's dominance. The U.S. is witnessing strong adoption of smart insulin pens and digital health platforms that streamline diabetes management. To reinforce their market position, companies are leveraging direct-to-consumer marketing, expanding distribution through retail pharmacies, and enhancing patient support programs.

Major players in the insulin pen market are Medmix, Julphar, Dongbao Pharmaceutical, Sanofi, Gan & Lee Pharmaceuticals, Novo Nordisk, Owen Mumford, Haselmeier, Ypsomed, Biocon Biologics, Eli Lilly and Co., Medtronic, Wockhardt, Becton, Dickinson and Company, and Suzhou Peng Ye Medical Devices.

To strengthen their foothold, leading companies in the insulin pen market are heavily focused on innovation, strategic partnerships, and patient-centric solutions. Many are investing in smart insulin pen technology, integrating Bluetooth connectivity, dose memory, and mobile app synchronization to offer better diabetes management tools. Collaborations with digital health platforms and glucose monitoring companies are also helping create more integrated care ecosystems.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Type trends

- 2.2.3 Indication trends

- 2.2.4 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of diabetes

- 3.2.1.2 Technological advancements in insulin pens

- 3.2.1.3 Enhanced awareness of self-management of diabetes

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of insulin pens

- 3.2.2.2 Limited penetration in low-income regions

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of smart features and digital platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.7.1 By type

- 3.7.2 By region

- 3.8 Reimbursement landscape

- 3.9 Patent analysis

- 3.10 Porter’s analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.2.4 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Reusable insulin pens

- 5.3 Disposable insulin pens

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Type 1 diabetes

- 6.3 Type 2 diabetes

- 6.4 Gestational diabetes

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospital pharmacies

- 7.3 Retail pharmacies

- 7.4 E-commerce

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Becton, Dickinson and Company

- 9.2 Biocon Biologics

- 9.3 Dongbao Pharmaceutical

- 9.4 Eli Lilly and Co

- 9.5 Gan & Lee Pharmaceuticals

- 9.6 Haselmeier

- 9.7 Julphar

- 9.8 Medmix

- 9.9 Medtronic

- 9.10 Novo Nordisk

- 9.11 Owen Mumford

- 9.12 Sanofi

- 9.13 Suzhou Peng Ye Medical Devices

- 9.14 Wockhardt

- 9.15 Ypsomed

2026年全球胰岛素笔、注射器、帮浦和注射器市场报告

2026年全球胰岛素笔、注射器、帮浦和注射器市场报告 胰岛素笔针市场按产品类型、可重复使用性、涂层、包装、材质、规格、针长、最终用户和分销管道划分-2026年至2032年全球预测

胰岛素笔针市场按产品类型、可重复使用性、涂层、包装、材质、规格、针长、最终用户和分销管道划分-2026年至2032年全球预测 胰岛素笔市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测

胰岛素笔市场规模、份额及成长分析(按类型、应用和地区划分)-2026-2033年产业预测 全球胰岛素笔市场-2025-2030年预测

全球胰岛素笔市场-2025-2030年预测 胰岛素笔:全球市占率和排名、总收入和需求预测(2025-2031年)胰岛素笔针:全球市占率和排名、总收入和需求预测(2025-2031年)

胰岛素笔:全球市占率和排名、总收入和需求预测(2025-2031年)胰岛素笔针:全球市占率和排名、总收入和需求预测(2025-2031年) 胰岛素笔市场:按产品类型、按技术、按应用、按年龄组、按性别、按最终用户、按分销管道、按地区

胰岛素笔市场:按产品类型、按技术、按应用、按年龄组、按性别、按最终用户、按分销管道、按地区 胰岛素笔市场规模、份额和趋势分析报告:按类型、最终用途、地区、细分市场预测,2024-2030 年

胰岛素笔市场规模、份额和趋势分析报告:按类型、最终用途、地区、细分市场预测,2024-2030 年 胰岛素笔针的市场规模,占有率,预测,趋势:各类型,各糖尿病类型,不同流通管道,医疗保健环境-2031年为止的世界预测

胰岛素笔针的市场规模,占有率,预测,趋势:各类型,各糖尿病类型,不同流通管道,医疗保健环境-2031年为止的世界预测