|

市场调查报告书

商品编码

1833411

结合疫苗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Conjugate Vaccine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

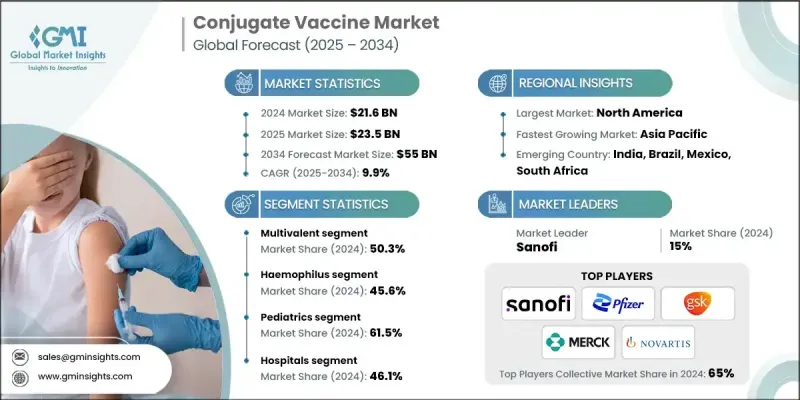

2024 年全球结合疫苗市场价值为 216 亿美元,预计将以 9.9% 的复合年增长率成长,到 2034 年达到 550 亿美元。

随着这些疾病的持续发病率,对有效预防措施的需求变得更加迫切。结合疫苗已成为一种强有力的解决方案,与传统的多醣疫苗相比,它具有更强的免疫原性和更持久的保护作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 216亿美元 |

| 预测值 | 550亿美元 |

| 复合年增长率 | 9.9% |

多价领域采用率不断提高

多价疫苗由于其能够透过单一剂型针对多种病原体菌株,在结合疫苗市场中发展势头强劲。这种方法可以增强广谱免疫力,这在多种血清型同时流行的地区尤其重要。透过减少所需的注射次数,多价疫苗可以提高患者的依从性并简化免疫接种程序。製造商正在积极投资研发下一代多价结合疫苗,以更少的剂量提供更强的保护。随着医疗保健行业日益重视效率和覆盖率,预计该领域将在未来市场成长中占据重要地位,尤其是在儿科和公共卫生疫苗接种计划中。

嗜血桿菌感染率上升

2024年,嗜血桿菌(Hib)疫苗市场占有相当大的份额。 Hib感染是幼儿细菌性脑膜炎和肺炎的主要原因,广泛的免疫接种已显着降低了全球许多地区Hib的发生率。 Hib结合疫苗即使在婴儿时期也能有效引发强烈的免疫反应,使其成为儿童早期免疫接种计画的基石。随着各国努力消除疫苗可预防疾病并扩大免疫覆盖率,Hib结合疫苗的需求维持稳定。

儿科需求不断成长

2024年,儿科疫苗市场占据了强劲的份额,这要归功于婴幼儿在最脆弱的时期迫切需要保护他们免受危及生命的细菌感染。全球各国的国家免疫计画都优先考虑在儿童早期接种结合疫苗,因为其安全性、免疫原性以及诱发持久免疫力的能力都已得到证实。结合疫苗易于与联合注射液结合使用,这进一步提高了儿科族群的接种率。

北美将成为推动力地区

2024年,北美结合疫苗市场收入可观,这得益于先进的医疗基础设施、积极的免疫接种计划以及高度的公共卫生意识。美国疾病管制与预防中心(CDC)和美国食品药物管理局(FDA)等机构的监管支持,确保了结合疫苗能够及时获得批准并纳入常规免疫接种计画。大型製药公司的入驻以及持续的研究投入,促进了创新和市场竞争力的提升。

结合疫苗市场的主要参与者包括印度血清研究所、默克、SK Bioscience、辉瑞、Bio-Med、诺华、泰姬製药、葛兰素史克、赛诺菲和巴拉特生物技术。

为了巩固在结合疫苗市场的地位,各公司正致力于多管齐下的策略,包括扩大疫苗组合、提高生产可扩展性以及建立策略伙伴关係。领先的製造商正在开发多价疫苗和联合疫苗,以增强疾病覆盖率并简化免疫接种计划。此外,他们还在投资新的给药平台,例如预充式註射器和单剂量小瓶,以提高用户便利性并减少浪费。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 传染病日益流行

- 老年人和儿科人口不断增长

- 增强临床意识和免疫指南

- 数位健康和远距医疗平台的扩展

- 产业陷阱与挑战

- 品牌疗法和生物疗法成本高昂

- 安全性问题和副作用

- 市场机会

- 新兴市场需求不断成长

- 转向个人化和联合治疗

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 未来市场趋势

- 管道分析

- 技术和创新格局

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

第五章:市场估计与预测:按类型,2021 - 2034

- 主要趋势

- 多价

- 单价

- 五价

第六章:市场估计与预测:按适应症,2021 - 2034 年

- 主要趋势

- 肺炎球菌

- 嗜血桿菌

- 脑膜炎球菌

- 其他适应症

第七章:市场估计与预测:按年龄组,2021 - 2034 年

- 主要趋势

- 儿科

- 成年人

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院

- 儿科诊所

- 公共卫生机构

- 其他最终用途

第九章:市场估计与预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Bharat Biotech

- Bio-Med

- GlaxoSmithKline

- Merck

- Novartis

- Pfizer

- Sanofi

- Serum Institute of India

- SK Bioscience

- Taj Pharmaceuticals

The Global Conjugate Vaccine Market was valued at USD 21.6 billion in 2024 and is estimated to grow at a CAGR of 9.9% to reach USD 55 billion by 2034.

As the incidence of these diseases persists, the need for effective, preventive measures has become more urgent. Conjugate vaccines have emerged as a powerful solution, offering enhanced immunogenicity and longer-lasting protection compared to traditional polysaccharide vaccines.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.6 Billion |

| Forecast Value | $55 Billion |

| CAGR | 9.9% |

Increasing Adoption Multivalent Sector

The multivalent segment is gaining significant momentum in the conjugate vaccine market due to its ability to target multiple strains of pathogens within a single formulation. This approach enhances broad-spectrum immunity, which is especially valuable in regions where multiple serotypes circulate simultaneously. By reducing the number of injections required, multivalent vaccines improve patient compliance and streamline immunization schedules. Manufacturers are actively investing in R&D to develop next-generation multivalent conjugate vaccines that provide stronger protection with fewer doses. As the healthcare industry increasingly emphasizes efficiency and coverage, this segment is expected to drive a substantial portion of future market growth, particularly in pediatric and public health vaccination programs.

Rising Prevalence of Haemophilus

The Haemophilus segment held a significant share in 2024. Hib infection is a leading cause of bacterial meningitis and pneumonia in young children, and widespread immunization has dramatically reduced its incidence in many parts of the world. The effectiveness of Hib conjugate vaccines in triggering strong immune responses, even in infants, has made them a cornerstone of early childhood immunization programs. As countries work to eliminate vaccine-preventable diseases and expand immunization coverage, the demand for Hib conjugate vaccines remains steady.

Increasing Demand in Pediatrics

The pediatrics segment held a robust share in 2024, driven by the critical need to protect infants and young children from life-threatening bacterial infections during their most vulnerable years. National immunization schedules across the globe prioritize conjugate vaccines in early childhood due to their proven safety, immunogenicity, and ability to induce long-lasting immunity. The convenience of integrating conjugate vaccines into combination shots further boosts uptake among pediatric populations.

North America to Emerge as a Propelling Region

North America conjugate vaccine market generated substantial revenues in 2024, supported by advanced healthcare infrastructure, proactive immunization programs, and a high level of public health awareness. Regulatory support from agencies like the CDC and FDA ensures timely approval and inclusion of conjugate vaccines in routine immunization schedules. The presence of major pharmaceutical companies and continued investment in research fuel innovation and market competitiveness.

Major players in the conjugate vaccine market are Serum Institute of India, Merck, SK Bioscience, Pfizer, Bio-Med, Novartis, Taj Pharmaceuticals, GlaxoSmithKline, Sanofi, and Bharat Biotech.

To strengthen their presence in the conjugate vaccine market, companies are focusing on a multi-pronged strategy that includes expanding vaccine portfolios, improving manufacturing scalability, and entering strategic partnerships. Leading manufacturers are developing multivalent and combination vaccines to enhance disease coverage and streamline immunization programs. Investments in new delivery platforms, such as pre-filled syringes and single-dose vials, are being made to improve user convenience and reduce wastage.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Indication

- 2.2.4 Age group

- 2.2.5 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of infectious diseases

- 3.2.1.2 Growing geriatric and paediatric populations

- 3.2.1.3 Enhanced clinical awareness and immunization guidelines

- 3.2.1.4 Expansion of digital health and telemedicine platforms

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of branded and biologic therapies

- 3.2.2.2 Safety concerns and side effects

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand in emerging markets

- 3.2.3.2 Shift toward personalized and combination therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Pipeline analysis

- 3.7 Technology and innovation landscape

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Multivalent

- 5.3 Monovalent

- 5.4 Pentavalent

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pneumococcal

- 6.3 Haemophilus

- 6.4 Meningococcal

- 6.5 Other indications

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Pediatrics

- 7.3 Adults

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Pediatric clinics

- 8.4 Public health agencies

- 8.5 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bharat Biotech

- 10.2 Bio-Med

- 10.3 GlaxoSmithKline

- 10.4 Merck

- 10.5 Novartis

- 10.6 Pfizer

- 10.7 Sanofi

- 10.8 Serum Institute of India

- 10.9 SK Bioscience

- 10.10 Taj Pharmaceuticals

结合疫苗市场:依产品类型、技术、通路和最终用户划分-2026-2032年全球市场预测

结合疫苗市场:依产品类型、技术、通路和最终用户划分-2026-2032年全球市场预测 结合疫苗市场:按产品类型、适应症、病原体类型、患者类型和地区划分

结合疫苗市场:按产品类型、适应症、病原体类型、患者类型和地区划分 结合疫苗市场-全球产业规模、份额、趋势、机会、预测:按产品类型、疾病适应症、最终用户、地区和竞争格局划分,2021-2031年

结合疫苗市场-全球产业规模、份额、趋势、机会、预测:按产品类型、疾病适应症、最终用户、地区和竞争格局划分,2021-2031年 结合疫苗:全球市场份额和排名、总收入和需求预测(2025-2031年)

结合疫苗:全球市场份额和排名、总收入和需求预测(2025-2031年) 全球结合疫苗市场规模(按类型、适应症、病原体、患者类型、地区、范围和预测)

全球结合疫苗市场规模(按类型、适应症、病原体、患者类型、地区、范围和预测) 结合疫苗市场规模、份额、趋势分析报告:按产品、品牌、疾病、病原体、患者、地区、细分市场预测,2024-2030年

结合疫苗市场规模、份额、趋势分析报告:按产品、品牌、疾病、病原体、患者、地区、细分市场预测,2024-2030年