|

市场调查报告书

商品编码

1833625

露天采矿设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Surface Mining Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

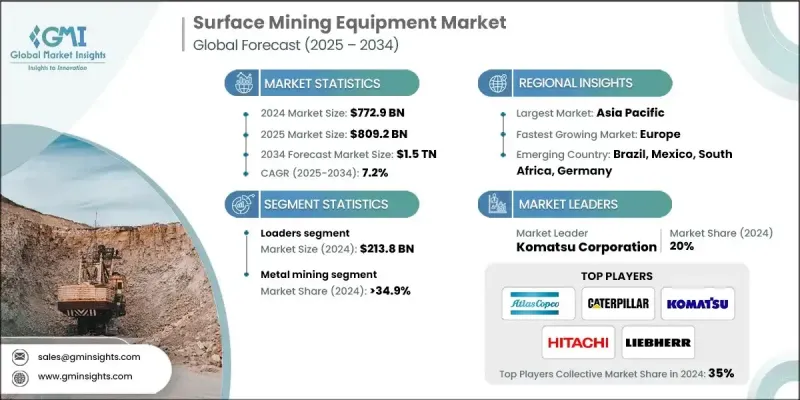

2024 年全球露天采矿设备市场价值为 7,729 亿美元,预计到 2034 年将以 7.2% 的复合年增长率成长,达到 1.5 兆美元。

这一成长的动力源于建筑、电子和汽车等主要终端产业对矿产和金属需求的不断增长。由于这些产业严重依赖原料,采矿企业正在增加对技术先进设备的投资,以提高产量、提升营运可靠性并简化流程。企业正在迅速将自动化和数位化平台整合到其采矿业务中,以提高效率、降低人为风险并最大限度地减少停机时间。配备即时监控系统和人工智慧分析功能的智慧机械正在改变营运商管理生产力和资源配置的方式。透过集中控制系统做出明智决策的能力,使采矿作业更快、更安全、更具成本效益。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 7729亿美元 |

| 预测值 | 1.5兆美元 |

| 复合年增长率 | 7.2% |

市场也正向永续和环保的实践转变。随着严格法规的出台,製造商正在引入混合动力和电动采矿机械,以减少排放。更清洁的引擎技术、生物燃料相容性和节能设计正在成为标准。此外,节水系统和除尘解决方案正在实施,以帮助营运达到环境基准。先进的安全系统,包括基于光达和雷达的防撞系统,正在提高现场安全性,而远端控制机器使操作员能够在场外安全地工作,从而降低现场风险。

2024年,装载机市场规模达2,138亿美元,在露天采矿活动中仍扮演着至关重要的角色。装载机在运输、装载和堆料等作业中功能多样,是各种规模采矿作业不可或缺的装备。更高的燃油效率和在各种地形条件下的坚固耐用性能继续推动装载机的普及,尤其是在企业寻求能够在恶劣条件下运行的可靠设备的情况下。

2024年,金属矿业板块占据了34.9%的市场份额,这得益于对铁、铝、铜和金等金属需求的成长。电子、建筑和运输等行业的消费成长正在推动矿业项目的扩张。露天采矿仍然是首选方法,因为它具有更高的开采能力和成本优势,有助于企业在控製成本的同时扩大营运规模。

2024年,美国露天采矿设备市场占76%的市场份额,为区域成长做出了重大贡献。随着先进技术的快速应用以及对数位化工具和自动化的日益依赖,美国的采矿作业正变得更加有效率和安全。支持性立法、税收优惠以及商品价格的上涨正在鼓励设备升级和新设备的采购。注重永续发展的政府政策和创新激励措施也有助于刺激对现代环保设备的需求。

影响全球露天采矿设备市场的关键公司包括必和必拓、美卓、巴里克黄金、小松、利勃海尔、力拓、英美资源集团、日立建机、自由港麦克莫兰铜金公司、山特维克、阿特拉斯·科普柯、JC Bamford Excavators、淡水河谷、Boart Longyear、卡特彼勒和沃尔沃。为了巩固其在露天采矿设备市场的竞争地位,领先企业正优先考虑创新、策略合作伙伴关係和永续性。许多公司正在扩展其产品线,包括电动和混合动力机械,以符合全球排放目标。对自动化、人工智慧整合和数位监控工具的投资使公司能够提供具有更高效率和预测性维护能力的智慧型设备。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 工业领域对金属的需求不断增长

- 发展中国家城市化进程加速

- 有利的政府法规

- 产业陷阱与挑战

- 初始成本高

- 更严格的环境法规

- 机会

- 采用自动化和智慧製造

- 新兴市场的扩张

- 成长动力

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 监管格局

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021-2034

- 主要趋势

- 装载机

- 挖土机

- 破碎、粉碎和筛选设备

- 钻孔机和破碎机

- 自卸车

- 铲子

- 平地机

- 其他的

第六章:市场估计与预测:依方法,2021-2034 年

- 主要趋势

- 露天开采

- 梯田采矿

- 露天采矿

第七章:市场估计与预测:按应用 2021-2034

- 主要趋势

- 采煤

- 金属矿业

- 矿产开采

- 其他(铝土矿开采)

第 8 章:市场估计与预测:按配销通路,2021-2034 年

- 主要趋势

- 直销

- 间接销售

第九章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 沙乌地阿拉伯

- 阿联酋

- 南非

第十章:公司简介

- Anglo American

- Atlas Copco

- Barrick Gold

- BHP Billiton

- Boart Longyear

- Caterpillar

- Freeport-McMoRan

- Hitachi Construction Machinery

- JC Bamford Excavators

- Komatsu

- Liebherr

- Metso

- Rio Tinto

- Sandvik

- Vale

- Volvo

The Global Surface Mining Equipment Market was valued at USD 772.9 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 1.5 trillion by 2034.

The growth is fueled by rising demand for minerals and metals across major end-use industries, including construction, electronics, and automotive. As these sectors rely heavily on raw materials, mining operations are increasingly investing in technologically advanced equipment to boost output, improve operational reliability, and streamline processes. Companies are rapidly integrating automation and digital platforms into their mining operations to enhance efficiency, reduce human risk, and minimize downtime. Intelligent machinery equipped with real-time monitoring systems and AI-based analytics is transforming how operators manage productivity and resource allocation. The ability to make informed decisions through centralized control systems is making mining operations faster, safer, and more cost-effective.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $772.9 Billion |

| Forecast Value | $1.5 Trillion |

| CAGR | 7.2% |

The market is also seeing a shift toward sustainable and eco-conscious practices. With strict regulations in place, manufacturers are introducing hybrid and electric-powered mining machinery to reduce emissions. Cleaner engine technologies, biofuel compatibility, and energy-saving designs are becoming standard. Additionally, water conservation systems and dust control solutions are being implemented to help operations meet environmental benchmarks. Advanced safety systems, including LiDAR- and radar-based collision prevention, are enhancing site safety while remote-controlled machines allow operators to work safely from off-site locations, lowering on-site risk.

In 2024, the loaders segment generated USD 213.8 billion, maintaining a vital role in surface mining activities. Their versatility in handling tasks such as transporting, loading, and stockpiling makes them indispensable for mining operations of all scales. Enhanced fuel efficiency and rugged performance across varied terrains continue to drive their popularity, especially as companies seek reliable equipment that performs under harsh conditions.

The metal mining segment captured a 34.9% share in 2024, supported by heightened demand for metals like iron, aluminum, copper, and gold. Increased consumption from sectors like electronics, building, and transportation is driving expansion in mining projects. Surface mining remains a preferred method due to its higher extraction capacity and cost advantages, which are helping companies scale operations while managing expenses.

United States Surface Mining Equipment Market held a 76% share in 2024, contributing significantly to regional growth. With the rapid adoption of advanced technologies and increasing reliance on digital tools and automation, mining operations in the U.S. are becoming more efficient and safer. Supportive legislation, tax benefits, and higher commodity prices are encouraging upgrades and new equipment purchases. Sustainability-focused government policies and innovation incentives are also helping fuel demand for modern, environmentally friendly equipment.

Key companies shaping the Global Surface Mining Equipment Market include BHP Billiton, Metso, Barrick Gold, Komatsu, Liebherr, Rio Tinto, Anglo American, Hitachi Construction Machinery, Freeport-McMoRan, Sandvik, Atlas Copco, J.C. Bamford Excavators, Vale, Boart Longyear, Caterpillar, and Volvo. To reinforce their competitive position in the surface mining equipment market, leading players are prioritizing innovation, strategic partnerships, and sustainability. Many are expanding their product lines with electric and hybrid machinery to align with global emission targets. Investment in automation, AI integration, and digital monitoring tools is enabling companies to offer intelligent equipment with enhanced efficiency and predictive maintenance capabilities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type trends

- 2.2.3 Method trends

- 2.2.4 Application trends

- 2.2.5 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for metals in industries

- 3.2.1.2 Increasing urbanization in developing countries

- 3.2.1.3 Favorable government regulations

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost

- 3.2.2.2 Stricter environmental regulations

- 3.2.3 Opportunities

- 3.2.3.1 Adoption of automation and smart manufacturing

- 3.2.3.2 Expansion in emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Loaders

- 5.3 Excavators

- 5.4 Crushing, pulverizing and screen equipment

- 5.5 Drills & breakers

- 5.6 Dumper

- 5.7 Shovels

- 5.8 Motor graders

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Method, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Strip mining

- 6.3 Terrace mining

- 6.4 Open-pit mining

Chapter 7 Market Estimates and Forecast, By Application 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Coal mining

- 7.3 Metal mining

- 7.4 Mineral mining

- 7.5 Other (bauxite mining)

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 Saudi Arabia

- 9.6.2 UAE

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Anglo American

- 10.2 Atlas Copco

- 10.3 Barrick Gold

- 10.4 BHP Billiton

- 10.5 Boart Longyear

- 10.6 Caterpillar

- 10.7 Freeport-McMoRan

- 10.8 Hitachi Construction Machinery

- 10.9 J.C. Bamford Excavators

- 10.10 Komatsu

- 10.11 Liebherr

- 10.12 Metso

- 10.13 Rio Tinto

- 10.14 Sandvik

- 10.15 Vale

- 10.16 Volvo