|

市场调查报告书

商品编码

1833635

汽车电动真空帮浦市场机会、成长动力、产业趋势分析及2025-2034年预测Automotive Electric Vacuum Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

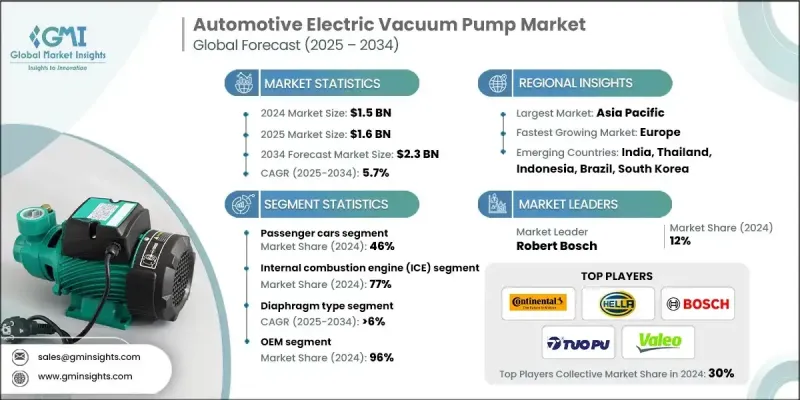

2024 年全球汽车电动真空帮浦市场价值为 15 亿美元,预计将以 5.7% 的复合年增长率成长,到 2034 年达到 23 亿美元。

该市场在帮助汽车製造商提高车辆效率、遵守不断变化的排放标准以及支持动力总成电气化方面发挥关键作用。原始设备製造商越来越依赖电动真空帮浦 (EVP) 为关键车辆系统提供稳定且独立的真空源,尤其是在缺乏引擎真空源的混合动力和电动车中。向环保出行的转变以及消费者对节能安全汽车的偏好,正在加速电动真空帮浦 (EVP) 在现代汽车中的整合。旨在降低碳足迹的严格政府法规进一步刺激了需求。随着製造商努力实现永续发展目标和营运效率,EVP 正在被设计为支援再生煞车、启动停止系统和 ECU 驱动的车辆动力学等先进功能。随着汽车产业在疫情后復苏,对可靠减排技术的需求正在推动全球所有主要汽车市场对电动真空帮浦的创新和应用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 15亿美元 |

| 预测值 | 23亿美元 |

| 复合年增长率 | 5.7% |

乘用车市场占了46%的市场份额,预计2025年至2034年的复合年增长率为7%。乘用车继续成为EVP的主要应用领域,因为它们广泛应用于SUV、掀背车和紧凑型轿车等各种车型。这些泵浦可确保稳定的煞车性能,提高车辆整体安全性,并在缺乏传统引擎真空源的情况下满足真空需求,尤其是在电动和混合动力车型中。 EVP易于整合且经济高效,是汽车製造商青睐的真空泵,使其成为无需进行大规模重新设计即可提高车辆效率的实用解决方案。

2024年,内燃机 (ICE) 市场占据了77%的市场份额,预计到2034年将以4.5%的复合年增长率成长。即使电气化发展势头强劲,内燃机汽车仍将在全球汽车市场中占据主导地位,尤其是在新兴经济体。随着全球范围内更严格的排放和燃油效率法规的生效,内燃机汽车製造商越来越多地采用EVP系统,以减少对引擎的依赖并提高营运效率。这些系统在怠速阶段、启动停止循环和交通拥堵期间,在增强煞车辅助器功能和辅助系统性能方面发挥关键作用。

2024年,亚太地区汽车电动真空帮浦市场占54%的市场份额,这得益于中国、日本和韩国等主要经济体汽车电气化进程的加速以及日益严格的排放法规。随着该地区电动车和混合动力车的快速普及,汽车製造商面临着整合符合现行和未来监管标准的节能部件的压力。因此,电动真空帮浦已成为现代汽车架构的重要组成部分。该地区强大的汽车产能、优惠的政策框架以及对电动车创新不断增加的投资,使亚太地区成为汽车技术进步的堡垒。

影响全球汽车电动真空帮浦市场的关键参与者包括法雷奥、永信精密、大陆集团、爱信、拓普、罗伯特博世、采埃孚、莱茵金属汽车、麦格纳国际和海拉。汽车电动真空帮浦市场的领导企业正致力于开发轻量化、紧凑化、节能的EVP系统,这些系统相容于所有动力系统类型,例如内燃机、混合动力和纯电动。马达效率、泵壳材料和电子控制单元的创新是产品差异化的关键。许多製造商正在高成长地区扩大产能,以满足日益增长的需求并减少对供应链的依赖。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 严格的排放和燃油经济法规

- 混合动力汽车和电动车的普及率不断上升

- 电动机和感测器的技术进步

- 消费者对增强安全性和效率的需求

- 政府对电气化和绿色交通的激励措施

- 产业陷阱与挑战

- 极端条件下的可靠性

- 与车辆系统的整合复杂性

- 市场机会

- 与混合动力和电动动力系统的集成

- 电动机和泵浦技术的进步

- 与先进的煞车和安全系统集成

- 越来越重视法规遵循和减排

- 成长潜力分析

- 监管格局

- 全球安全标准和测试要求

- 区域监管框架和审批流程

- 环境法规和排放合规性

- 品质管理系统和 ISO 标准

- 汽车产业标准(IATF 16949、ISO/TS)

- 功能安全要求(ISO 26262)

- 电磁相容性(EMC)标准

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 下一代电动机技术

- 智慧帮浦整合和物联网连接

- 预测性维护和状态监测

- 能源效率优化和电源管理

- 新兴技术

- 降噪与声学工程

- 小型化和轻量化技术

- 与先进驾驶辅助系统集成

- 人工智慧和机器学习应用

- 无线通讯和远端诊断

- 永续材料与循环经济设计

- 当前的技术趋势

- 价格趋势

- 按地区

- 按产品

- 生产统计

- 生产中心

- 消费中心

- 汇出和汇入

- 成本分解分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

- 风险评估与市场情报

- 供应链风险分析及缓解策略

- 技术过时和创新风险

- 监理合规风险与管理

- 市场需求波动与情境规划

- 竞争威胁与策略应变计划

- 经济和货币风险评估

- 地缘政治风险与贸易政策影响

- 环境与永续性风险

- 未来市场展望及策略机会

- 电动车市场成长的影响与机会

- 自动驾驶汽车整合要求

- 新兴市场扩张与在地化策略

- 科技融合与跨产业应用

- 永续发展趋势与绿色科技采用

- 投资机会和市场进入策略

- 伙伴关係和合作机会

- 长期市场演变与颠覆情景

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 多边环境协定

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- Expansion Plans and funding

第五章:市场估计与预测:依车型,2021 - 2034

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车

- 轻型商用车

- 中型商用车

- 重型商用车

第六章:市场估计与预测:以推进方式,2021 - 2034 年

- 主要趋势

- 内燃机(ICE)

- 电动车(EV)

- 纯电动车(BEV)

- 插电式混合动力电动车(PHEV)

- 混合动力电动车(HEV)

第七章:市场估计与预测:按应用,2021 - 2034

- 主要趋势

- 煞车系统

- 排放控制系统

- 暖通空调和气候控制系统

- 引擎管理系统

- 其他的

第八章:市场估计与预测:按类型,2021 - 2034

- 主要趋势

- 摆动活塞

- 隔膜

- 叶子

第九章:市场估计与预测:依销售管道,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第 10 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧人

- 俄罗斯

- 葡萄牙

- 克罗埃西亚

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- 全球参与者

- Aptiv

- BorgWarner

- Continental

- DENSO

- Magna International

- Mahle

- Rheinmetall Automotive

- Robert Bosch

- Schaeffler

- Valeo

- ZF Friedrichshafen

- 区域参与者

- Aisin

- Faurecia (Forvia)

- Hella

- Hitachi Astemo

- Hyundai Mobis

- Marelli

- Nexteer Automotive

- Pierburg

- Plastic Omnium

- Tenneco

- Tuopu

- Youngshin Precision

- 新兴玩家

- Aeromotive

- Classic Performance

- NAVAC

- Pfeiffer Vacuum Technology

- Thomas Magnete

The Global Automotive Electric Vacuum Pump Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 2.3 billion by 2034.

This market plays a critical role in enabling automotive manufacturers to enhance vehicle efficiency, comply with evolving emission norms, and support powertrain electrification. OEMs are increasingly relying on EVPs to provide a consistent and independent vacuum source for essential vehicle systems, particularly in hybrid and electric vehicles where engine-based vacuum sources are absent. The shift toward eco-friendly mobility and consumer preference for vehicles that are both energy-efficient and safe is accelerating the integration of EVPs into modern vehicles. Stringent government regulations focused on lowering carbon footprints have further fueled demand. As manufacturers strive to meet sustainability targets and operational efficiency, EVPs are being engineered to support advanced features such as regenerative braking, start-stop systems, and ECU-driven vehicle dynamics. With the automotive industry rebounding post-pandemic, the need for reliable, emission-reducing technologies is driving both innovation and adoption of electric vacuum pumps across all major automotive markets worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 5.7% |

The passenger car segment held a 46% share and is projected to grow at a CAGR of 7% from 2025 to 2034. Passenger cars continue to serve as the primary application area for EVPs due to their wide deployment in various vehicle categories, including SUVs, hatchbacks, and compact cars. These pumps ensure consistent braking performance, improve overall vehicle safety, and support vacuum needs in the absence of traditional engine vacuum sources, especially in electric and hybrid variants. Automakers prefer EVPs for their easy integration and cost-effectiveness, making them a practical solution for enhancing vehicle efficiency without extensive redesigns.

The internal combustion engine (ICE) segment held a 77% share in 2024 and is set to grow at a CAGR of 4.5% through 2034. Even as electrification gains momentum, ICE-powered vehicles continue to dominate global fleets, particularly in emerging economies. With stricter emissions and fuel efficiency mandates coming into effect globally, ICE vehicle manufacturers are increasingly implementing EVPs to reduce engine dependency and improve operational efficiency. These systems play a key role in enhancing brake booster functionality and auxiliary system performance during idle phases, start-stop cycles, and traffic congestion.

Asia Pacific Automotive Electric Vacuum Pump Market held 54% share in 2024, driven by the accelerating electrification of vehicles and increasingly stringent emissions regulations in major economies such as China, Japan, and South Korea. With EV and hybrid adoption growing rapidly across this region, automakers are under pressure to integrate energy-efficient components that comply with current and upcoming regulatory benchmarks. As a result, EVPs have become a critical part of modern vehicle architecture. The region's robust automotive production capacity, favorable policy frameworks, and increasing investments in electric mobility innovation have positioned Asia Pacific as a stronghold for automotive technology advancement.

Key players shaping the Global Automotive Electric Vacuum Pump Market include Valeo, Youngshin Precision, Continental, Aisin, Tuopu, Robert Bosch, ZF Friedrichshafen, Rheinmetall Automotive, Magna International, and Hella. Leading companies in the automotive electric vacuum pump market are focusing on developing lightweight, compact, and energy-efficient EVP systems compatible with all powertrain types such as ICE, hybrid, and electric. Innovation in motor efficiency, pump housing materials, and electronic control units is central to product differentiation. Many manufacturers are expanding production capabilities in high-growth regions to meet increasing demand and reduce supply chain dependencies.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicles

- 2.2.3 Propulsion

- 2.2.4 Application

- 2.2.5 Type

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Stringent emission and fuel economy regulations

- 3.2.1.3 Rising adoption of hybrid and electric vehicles

- 3.2.1.4 Technological advancements in electric motors and sensors

- 3.2.1.5 Consumer demand for enhanced safety and efficiency

- 3.2.1.6 Government incentives for electrification and green mobility

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Reliability under extreme conditions

- 3.2.2.2 Integration complexity with vehicle systems

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with hybrid and electric powertrains

- 3.2.3.2 Advancements in electric motor and pump technology

- 3.2.3.3 Integration with advanced braking and safety systems

- 3.2.3.4 Growing focus on regulatory compliance and emission reduction

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global safety standards & testing requirements

- 3.4.2 Regional regulatory frameworks & approval processes

- 3.4.3 Environmental regulations & emission compliance

- 3.4.4 Quality management systems & ISO standards

- 3.4.5 Automotive industry standards (IATF 16949, ISO/TS)

- 3.4.6 Functional safety requirements (ISO 26262)

- 3.4.7 Electromagnetic compatibility (EMC) standards

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Next-generation electric motor technologies

- 3.7.1.2 Smart pump integration & IoT connectivity

- 3.7.1.3 Predictive maintenance & condition monitoring

- 3.7.1.4 Energy efficiency optimization & power management

- 3.7.2 Emerging technologies

- 3.7.2.1 Noise reduction & acoustic engineering

- 3.7.2.2 Miniaturization & weight reduction technologies

- 3.7.2.3 Integration with advanced driver assistance systems

- 3.7.2.4 Artificial intelligence & machine learning applications

- 3.7.2.5 Wireless communication & remote diagnostics

- 3.7.2.6 Sustainable materials & circular economy design

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Risk assessment & market intelligence

- 3.13.1 Supply chain risk analysis & mitigation strategies

- 3.13.2 Technology obsolescence & innovation risks

- 3.13.3 Regulatory compliance risks & management

- 3.13.4 Market demand volatility & scenario planning

- 3.13.5 Competitive threats & strategic response planning

- 3.13.6 Economic & currency risk assessment

- 3.13.7 Geopolitical risks & trade policy impact

- 3.13.8 Environmental & sustainability Risks

- 3.14 Future market outlook & strategic opportunities

- 3.14.1 Electric vehicle market growth impact & opportunities

- 3.14.2 Autonomous vehicle integration requirements

- 3.14.3 Emerging market expansion & localization strategies

- 3.14.4 Technology convergence & cross-industry applications

- 3.14.5 Sustainability trends & green technology adoption

- 3.14.6 Investment opportunities & market entry strategies

- 3.14.7 Partnership & collaboration opportunities

- 3.14.8 Long-term market evolution & disruption scenarios

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicle

- 5.3.2 Medium commercial vehicle

- 5.3.3 Heavy commercial vehicle

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Internal combustion engine (ICE)

- 6.3 Electric vehicles (EVs)

- 6.3.1 Battery electric vehicles (BEVs)

- 6.3.2 Plug-in hybrid electric vehicles (PHEVs)

- 6.3.3 Hybrid electric vehicles (HEVs)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Braking systems

- 7.3 Emission control systems

- 7.4 HVAC & climate control systems

- 7.5 Engine management systems

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Swing piston

- 8.3 Diaphragm

- 8.4 Leaf

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 (USD Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Portugal

- 10.3.9 Croatia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aptiv

- 11.1.2 BorgWarner

- 11.1.3 Continental

- 11.1.4 DENSO

- 11.1.5 Magna International

- 11.1.6 Mahle

- 11.1.7 Rheinmetall Automotive

- 11.1.8 Robert Bosch

- 11.1.9 Schaeffler

- 11.1.10 Valeo

- 11.1.11 ZF Friedrichshafen

- 11.2 Regional Players

- 11.2.1 Aisin

- 11.2.2 Faurecia (Forvia)

- 11.2.3 Hella

- 11.2.4 Hitachi Astemo

- 11.2.5 Hyundai Mobis

- 11.2.6 Marelli

- 11.2.7 Nexteer Automotive

- 11.2.8 Pierburg

- 11.2.9 Plastic Omnium

- 11.2.10 Tenneco

- 11.2.11 Tuopu

- 11.2.12 Youngshin Precision

- 11.3 Emerging Players

- 11.3.1 Aeromotive

- 11.3.2 Classic Performance

- 11.3.3 NAVAC

- 11.3.4 Pfeiffer Vacuum Technology

- 11.3.5 Thomas Magnete

汽车电动真空帮浦市场 - 全球产业规模、份额、趋势、机会及预测(按电动车类型、车辆类型、地区和竞争格局划分,2021-2031年)

汽车电动真空帮浦市场 - 全球产业规模、份额、趋势、机会及预测(按电动车类型、车辆类型、地区和竞争格局划分,2021-2031年) 汽车电动真空帮浦市场规模、份额及成长分析(按电动车类型、车辆类型及地区划分)-2026-2033年产业预测

汽车电动真空帮浦市场规模、份额及成长分析(按电动车类型、车辆类型及地区划分)-2026-2033年产业预测 全球汽车电动真空帮浦(EVP)市场:产业分析、规模、份额、成长、趋势与预测(2025-2032)

全球汽车电动真空帮浦(EVP)市场:产业分析、规模、份额、成长、趋势与预测(2025-2032) 全球汽车电动真空帮浦市场

全球汽车电动真空帮浦市场 全球汽车电动真空帮浦市场:依车型、推进系统类型、销售通路、地区、机会及预测,2018-2032

全球汽车电动真空帮浦市场:依车型、推进系统类型、销售通路、地区、机会及预测,2018-2032 汽车电动真空帮浦市场,按推进类型、按应用、按车辆类型、按国家和地区 - 2025 年至 2032 年的行业分析、市场规模、市场份额和预测

汽车电动真空帮浦市场,按推进类型、按应用、按车辆类型、按国家和地区 - 2025 年至 2032 年的行业分析、市场规模、市场份额和预测