|

市场调查报告书

商品编码

1833641

子宫内避孕器市场机会、成长动力、产业趋势分析及2025-2034年预测Intrauterine Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

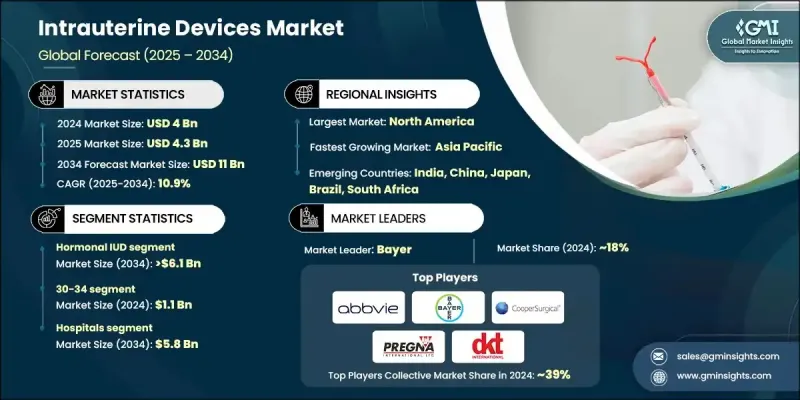

2024 年全球子宫内避孕器市场价值为 40 亿美元,预计到 2034 年将以 10.9% 的复合年增长率成长至 110 亿美元。

强劲的成长势头得益于支持性监管政策、女性对子宫内避孕器多种用途认识的提高以及意外怀孕的高发生率。子宫内避孕器不仅因其在避孕方面的作用而日益受到认可,还因其更广泛的健康应用而受到认可,包括管理月经过多、子宫内膜异位症和围绝经期症状。随着教育倡议、数位健康平台的兴起以及生殖保健资讯获取管道的改善,女性现在能够就长期避孕选择做出更明智的决定。医疗保健专业人员在为患者提供有关子宫内避孕器的安全性、有效性和其他健康益处的咨询方面发挥着重要作用,这在全球范围内提高了其接受度。子宫内避孕器是一种小型、灵活的T形避孕工具,旨在提供可靠、可逆且长效的避孕措施。诸如铁基非荷尔蒙节育器等新兴创新产品正在开发中,旨在最大限度地减少副作用并提供无激素解决方案。这些技术进步正在改变子宫内避孕器的格局,增强女性的选择,并加强长期的市场扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 40亿美元 |

| 预测值 | 110亿美元 |

| 复合年增长率 | 10.9% |

2024年,激素类子宫内避孕器市场占据53.8%的市场份额,这得益于其在避孕和改善月经健康方面的功效。荷尔蒙类子宫内避孕器,尤其是释放左炔诺孕酮的子宫内避孕器,因其持久保护、维护成本低以及诸如减少月经出血和缓解子宫内膜异位症症状等附加治疗优势而被广泛采用。由于其双重功效,医疗保健提供者经常推荐这些节育器,从而巩固了其在市场上的主导地位。

2024年,医院市场占据53.2%的份额,预计到2034年将创造58亿美元的市场价值。医院在提供长效可逆避孕措施方面仍然至关重要,因为它们能够提供经验丰富的妇产科医生进行安全放置子宫内避孕器。一些地区已采用产后子宫内避孕器放置方案,扩大了可近性,并有助于减少意外怀孕,尤其是在孕产妇保健系统健全的地区。

2024年,美国子宫内避孕器市场规模达14.4亿美元,预计2025年至2034年期间的复合年增长率将达到10.3%。公共卫生倡议和宣传活动的不断加强,推动了子宫内避孕器作为一种安全、有效且便捷的避孕方式的使用。相较于每日服用避孕药等短期避孕方式,长效可逆避孕法的受欢迎程度日益提升,进一步加速了美国和加拿大不同族群对子宫内避孕器的采用。

活跃于子宫内避孕器产业的知名公司包括 MONA LISA、Meril、Sebela Pharmaceuticals、DKT、PREGNA、SMB、AbbVie、Prosan、GIMA、Bayer、Medicines360、eurogine、GYNO CARE、CooperSurgical、HLL Lifecare Limited 等。为了巩固在子宫内避孕器市场的领先地位,这些公司正致力于扩大产品组合,涵盖荷尔蒙和非荷尔蒙产品,包括开发旨在最大程度减少副作用和提高用户舒适度的创新材料。此外,它们还与医疗保健组织和政府计画进行策略合作,以扩大子宫内避孕器的可及性和采用率。许多公司也投资宣传活动,向女性宣传子宫内避孕器除了避孕之外的益处,例如月经健康管理。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 有利的监管环境

- 女性对各种子宫内避孕器应用的认识不断提高

- 意外怀孕数量高

- 政府预防意外堕胎和怀孕的倡议

- 计划性延迟妊娠的倾向日益增强

- 产业陷阱与挑战

- 设备成本高

- 存在多种健康问题的风险

- 保险覆盖范围和获取途径的差异

- 市场机会

- 长期避孕需求不断增加

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 现有技术

- 新兴技术

- 未来市场趋势

- 报销场景

- 消费者行为和趋势

- 品牌分析

- 管道分析

- 避孕以外的治疗应用

- 2024年定价分析

- 波特的分析

- PESTEL分析

- 差距分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 铜子宫内避孕器

- 荷尔蒙子宫内避孕器

第六章:市场估计与预测:按年龄组,2021 - 2034 年

- 主要趋势

- 15-19

- 20-24

- 25-29

- 30-34

- 35-39

- 40-44

- 45岁以上

第七章:市场估计与预测:依最终用途,2021 - 2034

- 主要趋势

- 医院

- 妇科诊所

- 社区健康照护中心

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- AbbVie

- Bayer

- CooperSurgical

- DKT

- eurogine

- GIMA

- GYNO CARE

- HLL Lifecare Limited

- Medicines360

- Meril

- MONA LISA

- PREGNA

- Prosan

- Sebela Pharmaceuticals

- SMB

The Global Intrauterine Devices Market was valued at USD 4 billion in 2024 and is estimated to grow at a CAGR of 10.9% to reach USD 11 billion by 2034.

The strong growth trajectory is driven by supportive regulatory policies, greater awareness among women about the diverse uses of IUDs, and the high incidence of unintended pregnancies. IUDs are increasingly acknowledged not only for their role in birth control but also for wider health applications, including the management of heavy menstrual bleeding, endometriosis, and perimenopausal symptoms. With the rise of educational initiatives, digital health platforms, and improved access to reproductive care information, women are now empowered to make more informed decisions about long-term contraceptive options. Healthcare professionals play a significant role by counseling patients on the safety, effectiveness, and additional health benefits of IUDs, which has boosted acceptance globally. Intrauterine devices are small, flexible, T-shaped contraceptive tools designed to provide reliable, reversible, and long-acting pregnancy prevention. Emerging innovations, such as iron-based non-hormonal devices, are being developed to minimize side effects and provide hormone-free solutions. These technological advancements are transforming the IUD landscape, enhancing choices for women, and reinforcing long-term market expansion.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4 Billion |

| Forecast Value | $11 Billion |

| CAGR | 10.9% |

The hormonal IUD segment held 53.8% share in 2024, supported by its effectiveness in preventing pregnancy and improving menstrual health. Hormonal IUDs, particularly those releasing levonorgestrel, are widely adopted for their long-lasting protection, low maintenance, and added therapeutic advantages, such as reduced menstrual bleeding and relief from endometriosis symptoms. Healthcare providers frequently recommend them due to their dual benefits, strengthening their dominance in the market.

The hospitals segment held 53.2% share in 2024 and is forecasted to generate USD 5.8 billion by 2034. Hospitals remain vital in delivering long-acting reversible contraception, as they provide access to skilled gynecologists and obstetricians for safe insertion procedures. The adoption of postpartum IUD insertion protocols in several regions has broadened access and contributed to a decline in unplanned pregnancies, particularly in areas with robust maternal healthcare systems.

U.S. Intrauterine Devices Market was valued at USD 1.44 billion in 2024 and is estimated to grow at a CAGR of 10.3% between 2025 and 2034. Increased public health initiatives and awareness campaigns have encouraged the use of IUDs as a safe, effective, and convenient contraceptive option. Growing preference for long-acting reversible contraception over short-term alternatives, such as daily pills, has further accelerated adoption across diverse demographics in the U.S. and Canada.

Prominent companies active in the Intrauterine Devices Industry include MONA LISA, Meril, Sebela Pharmaceuticals, DKT, PREGNA, SMB, AbbVie, Prosan, GIMA, Bayer, Medicines360, eurogine, GYNO CARE, CooperSurgical, HLL Lifecare Limited, and others. To strengthen their foothold in the intrauterine devices market, leading companies are focusing on expanding product portfolios with both hormonal and non-hormonal options, including the development of innovative materials designed to minimize side effects and improve user comfort. Strategic collaborations with healthcare organizations and government programs are being pursued to broaden access and adoption rates. Many players are also investing in awareness campaigns to educate women on the benefits of IUDs beyond contraception, such as menstrual health management.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Age group trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Favorable regulatory scenario

- 3.2.1.2 Rising awareness among women regarding various IUD applications

- 3.2.1.3 High number of unintended pregnancies

- 3.2.1.4 Government initiatives for the prevention of unwanted abortions and pregnancies

- 3.2.1.5 Growing inclination towards planned delayed pregnancy

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the device

- 3.2.2.2 Risk of several health issues

- 3.2.2.3 Variability in insurance coverage and access

- 3.2.3 Market opportunities

- 3.2.3.1 Rising demand for long-term contraception

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technological landscape

- 3.5.1 Current technologies

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Reimbursement scenario

- 3.8 Consumer behaviour and trends

- 3.9 Brand analysis

- 3.10 Pipeline analysis

- 3.11 Therapeutic applications beyond contraception

- 3.12 Pricing analysis, 2024

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

- 3.15 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Copper IUD

- 5.3 Hormonal IUD

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 15-19

- 6.3 20-24

- 6.4 25-29

- 6.5 30-34

- 6.6 35-39

- 6.7 40-44

- 6.8 45+

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Gynecology clinics

- 7.4 Community health care centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 AbbVie

- 9.2 Bayer

- 9.3 CooperSurgical

- 9.4 DKT

- 9.5 eurogine

- 9.6 GIMA

- 9.7 GYNO CARE

- 9.8 HLL Lifecare Limited

- 9.9 Medicines360

- 9.10 Meril

- 9.11 MONA LISA

- 9.12 PREGNA

- 9.13 Prosan

- 9.14 Sebela Pharmaceuticals

- 9.15 SMB

2026年全球子宫内避孕器市场报告2026年全球荷尔蒙子宫内避孕器(IUD)市场报告2026年全球避孕器市场报告

2026年全球子宫内避孕器市场报告2026年全球荷尔蒙子宫内避孕器(IUD)市场报告2026年全球避孕器市场报告 全球皮下避孕植入市场规模、份额、趋势和成长分析报告(2026-2034)

全球皮下避孕植入市场规模、份额、趋势和成长分析报告(2026-2034) 妇科避孕植入市场(按产品、最终用户和分销管道划分),全球预测,2026-2032年

妇科避孕植入市场(按产品、最终用户和分销管道划分),全球预测,2026-2032年 避孕器材市场-全球产业规模、份额、趋势、机会和预测,依产品类型、配销通路、最终用户、地区和竞争格局划分,2021-2031年预测

避孕器材市场-全球产业规模、份额、趋势、机会和预测,依产品类型、配销通路、最终用户、地区和竞争格局划分,2021-2031年预测 日本避孕器械市场报告(按类型(保险套、隔膜、子宫颈帽、海绵、阴道环、子宫内避孕器(IUD)及其他)、性别(男性、女性)和地区划分,2026-2034年)

日本避孕器械市场报告(按类型(保险套、隔膜、子宫颈帽、海绵、阴道环、子宫内避孕器(IUD)及其他)、性别(男性、女性)和地区划分,2026-2034年) 子宫内避孕器市场规模、份额和成长分析(按类型、产品类型、年龄层、应用和地区划分)—产业预测(2026-2033 年)

子宫内避孕器市场规模、份额和成长分析(按类型、产品类型、年龄层、应用和地区划分)—产业预测(2026-2033 年) 子宫内避孕器(IUD)市场规模、份额及成长分析(按类型和地区划分)-2026-2033年产业预测

子宫内避孕器(IUD)市场规模、份额及成长分析(按类型和地区划分)-2026-2033年产业预测 避孕器市场规模、份额和成长分析(按产品类型、技术、分销管道和地区划分)-2026-2033年产业预测

避孕器市场规模、份额和成长分析(按产品类型、技术、分销管道和地区划分)-2026-2033年产业预测