|

市场调查报告书

商品编码

1833652

汽车启动停止系统市场机会、成长动力、产业趋势分析及2025-2034年预测Automotive Start-Stop System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

根据 Global Market Insights Inc. 发布的最新报告,全球汽车启动/停止系统市场规模在 2024 年估计为 437 亿美元,预计将从 2025 年的 480 亿美元增长到 2034 年的 1,218 亿美元,复合年增长率为 13.7%。

全球各国政府正在实施更严格的排放标准和燃油经济性标准,迫使汽车製造商整合启停系统等节油技术。这些系统有助于减少怠速排放并提高整体燃油效率,使其成为合规的首选解决方案。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 437亿美元 |

| 预测值 | 1218亿美元 |

| 复合年增长率 | 13.7% |

乘用车需求不断成长

2024年,乘用车市场将占据显着份额,这得益于日常用车对节油环保解决方案的强劲需求。汽车製造商正在将启动/停止系统作为各种车型(包括紧凑型、中型和高端车型)的标准配置,以符合排放法规并满足消费者对更高燃油经济性的期望。

柴油使用量上升

由于柴油动力系统在乘用车和轻型商用车中仍然占据主导地位,柴油市场在2024年占据了相当大的份额。柴油引擎以其高扭力和燃油效率而闻名,启动停止系统可显着降低怠速时的油耗和排放,使其受益匪浅。儘管电气化进程正在逐步推进,但配备启动停止技术的柴油车仍然受到车队营运商和注重成本的消费者的青睐。

OEM获得发展动力

2024年,原始设备製造商(OEM)市场占据了相当大的份额,这得益于新车平台内建功能的推动。原始设备製造商(OEM)认为这项技术是一种经济高效的解决方案,无需完全过渡到混合动力或电动传动系统即可满足燃油经济性目标和排放要求。 OEM正在与一级供应商紧密合作,共同开发更紧凑、更耐用、更有效率的系统,并可扩展应用于所有车型。

欧洲将崛起成为推手地区

2024年,欧洲汽车启动停止系统市场收入强劲,这得益于严格的欧盟排放法规、高昂的燃油价格以及对永续发展的高度重视。包括德国、法国和英国在内的主要欧洲国家都实施了积极的碳减排政策,推动了启停系统等节油技术的广泛应用。此外,成熟的汽车製造基础和消费者对环保功能的认知度也推动了该地区OEM的强劲成长。

汽车启停系统市场的主要参与者包括法雷奥、日立汽车、罗伯特博世、麦格纳、博格华纳、大陆集团、采埃孚、江森自控、爱信精机和电装。

为了巩固市场地位,汽车启动停止系统领域的企业正专注于创新、合作和成本优化。领先的供应商正在开发更强大的电池管理系统、再生煞车整合系统和静音启动电机,以提升系统性能和耐用性。原始设备製造商 (OEM) 和技术供应商之间的合作正在加快针对特定动力系统配置客製化的先进系统的上市时间。同时,企业正在扩大其全球生产布局,以确保供应链的弹性和成本效率。透过平衡性能、可靠性和价格承受能力,这些策略倡议正在帮助企业与汽车製造商签订长期合同,并在日益严格的行业监管中保持竞争优势。

目录

第一章:方法论

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- GMI 专有 AI 系统

- 人工智慧驱动的研究增强

- 来源一致性协议

- 人工智慧准确度指标

- 预测模型

- 初步研究和验证

- 市场估计的主要趋势

- 量化市场影响分析

- 生长参数对预测的数学影响

- 情境分析框架

- 一些主要来源(但不限于)

- 资料探勘来源

- 次要

- 付费来源

- 公共资源

- 来源(按地区)

- 次要

- 研究路径和信心评分

- 研究路径组成部分:

- 评分组件

- 研究透明度附录

- 来源归因框架

- 品质保证指标

- 我们对信任的承诺

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 严格的排放和燃油经济法规

- 燃料价格上涨和消费者对效率的需求

- 起动马达和电池的技术进步

- 混合动力和轻度混合动力汽车产量激增

- 政府对环保技术的奖励措施

- 产业陷阱与挑战

- 系统和组件成本高

- 电池磨损和更换频率

- 市场机会

- 与混合动力和电动动力系统的集成

- 电池技术与能量回收的进步

- 拓展新兴汽车市场

- 与 ADAS 和智慧行动平台集成

- 成长动力

- 成长潜力分析

- 监管格局

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

- 用例和应用分析

- 城市驾驶应用

- 城市交通走走停停场景

- 配送车辆优化

- 计程车和共乘应用程式

- 大众运输整合

- 高速公路和混合驾驶条件

- 长途旅行应用

- 商业船队运营

- 紧急车辆应用

- 休閒车集成

- 特殊用例

- 建筑和工业车辆

- 农业设备应用

- 船舶和非公路应用

- 城市驾驶应用

- 成本效益和投资报酬率分析框架

- 总拥有成本分析

- 初始系统成本明细

- 维护和更换成本

- 燃料节省量化

- 生命週期成本建模

- 投资报酬率指标

- 依车辆类型分析投资回收期

- 净现值计算

- 内部报酬率评估

- 敏感度分析框架

- 总拥有成本分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 多边环境协定

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:依车型,2021 - 2034

- 主要趋势

- 两轮车

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车

- 轻型商用车

- 中型商用车

- 重型商用车

第六章:市场估计与预测:按燃料,2021 - 2034 年

- 主要趋势

- 柴油引擎

- 汽油

- 天然气

- 杂交种

第七章:市场估计与预测:依技术分类,2021 - 2034 年

- 主要趋势

- 增强型启动器

- 常规启动器

- 双联电磁启动器

- 皮带驱动交流发电机起动器(BAS)

- 直喷引擎系统

- 整合起动发电机(ISG)

第八章:市场估计与预测:按组件,2021 - 2034

- 主要趋势

- 引擎控制单元(ECU)

- 电池

- 交流发电机

- 起动马达

- DC/DC转换器

- 感应器

- 其他的

第九章:市场估计与预测:按配销通路,2021 - 2034

- 主要趋势

- OEM

- 售后市场

第 10 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧人

- 俄罗斯

- 葡萄牙

- 克罗埃西亚

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- 全球参与者

- Aisin Seiki

- BorgWarner

- Continental

- Denso

- Exide Technologies

- GS Yuasa

- Hitachi

- Infineon Technologies

- Johnson Controls

- Magna International Inc.

- Mahle

- NXP Semiconductors

- Panasonic

- Robert Bosch

- Schaeffler

- Valeo

- ZF Friedrichshafen

- 区域参与者

- Calsonic Kansei

- Eaton Corporation

- Faurecia

- Hella GmbH & Co.

- Hyundai Mobis

- JTEKT Corporation

- Lear Corporation

- Schaeffler AG

- Visteon Corporation

- 新兴玩家

- ABB Ltd.

- Aptiv PLC

- Infineon Technologies

- LEM Holding

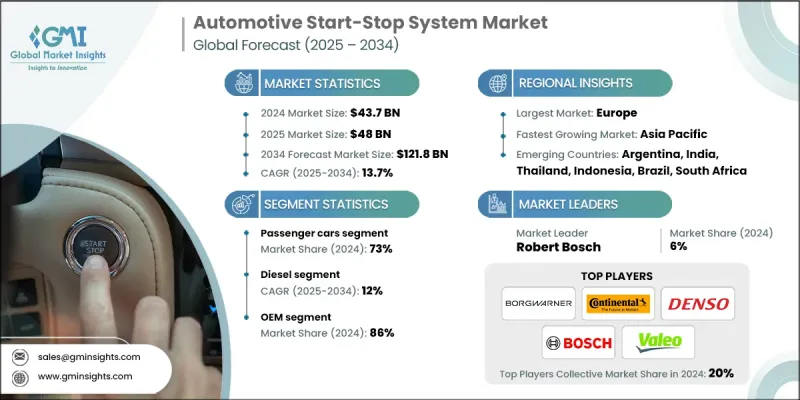

The global automotive start-stop system market was estimated at USD 43.7 billion in 2024 and is expected to grow from USD 48 billion in 2025 to USD 121.8 billion by 2034, at a CAGR of 13.7%, according to the latest report published by Global Market Insights Inc.

Governments across the globe are enforcing stricter emission norms and fuel economy standards, compelling automakers to integrate fuel-saving technologies like start-stop systems. These systems help reduce idling emissions and improve overall fuel efficiency, making them a go-to solution for compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $43.7 Billion |

| Forecast Value | $121.8 Billion |

| CAGR | 13.7% |

Growing Demand for Passenger Cars

The passenger cars segment held a notable share in 2024, driven by strong demand for fuel-efficient and environmentally friendly solutions in daily-use vehicles. Automakers are integrating start-stop systems as a standard feature across a wide range of car models, including compact, midsize, and premium offerings, to comply with emissions regulations and meet consumer expectations for improved fuel economy.

Rising Usage of Diesel

The diesel segment generated a significant share in 2024, as diesel powertrains remain prevalent in the passenger and light commercial vehicles. Diesel engines, known for their high torque and fuel efficiency, benefit significantly from start-stop systems that further reduce idle-time fuel consumption and emissions. Despite a gradual shift toward electrification, diesel vehicles equipped with start-stop technology continue to appeal to fleet operators and cost-conscious consumers.

OEM to Gain Traction

The OEM segment held a sizeable share in 2024, driven by built-in features across new vehicle platforms. Original Equipment Manufacturers view this technology as a cost-effective solution to meet fuel economy targets and emission mandates without fully transitioning to hybrid or electric drivetrains. OEMs are partnering closely with tier-1 suppliers to co-develop more compact, durable, and efficient systems that can be scaled across vehicle lineups.

Europe to Emerge as a Propelling Region

Europe automotive start-stop system market generated robust revenues in 2024, backed by stringent EU emission regulations, high fuel prices, and a strong emphasis on sustainability. Major European countries, including Germany, France, and the UK, have implemented aggressive carbon reduction policies, prompting widespread adoption of fuel-saving technologies like start-stop systems. Additionally, a mature automotive manufacturing base and consumer awareness around eco-friendly features are driving strong OEM uptake in the region.

Major players in the automotive start-stop system market are Valeo, Hitachi Automotive, Robert Bosch, Magna, BorgWarner, Continental, ZF Friedrichshafen, Johnson Controls, Aisin Seiki, and Denso.

To strengthen their market position, companies in the automotive start-stop system space are focusing on innovation, partnerships, and cost optimization. Leading suppliers are developing more robust battery management systems, regenerative braking integration, and silent start motors to enhance system performance and durability. Collaborations between OEMs and technology providers are accelerating time-to-market for advanced systems tailored to specific powertrain configurations. At the same time, firms are expanding their global production footprints to ensure supply chain resilience and cost efficiency. By balancing performance, reliability, and affordability, these strategic moves are helping companies secure long-term contracts with automakers and maintain a competitive edge in an increasingly regulated industry.

Table of Contents

Chapter 1 Methodology

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.1.3 Base estimates and calculations

- 1.1.4 Base year calculation

- 1.1.5 Key trends for market estimates

- 1.1.6 GMI proprietary AI system

- 1.1.6.1 AI-Powered research enhancement

- 1.1.6.2 Source consistency protocol

- 1.1.6.3 AI accuracy metrics

- 1.2 Forecast model

- 1.3 Primary research and validation

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario Analysis Framework

- 1.4 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Secondary

- 1.5.1.1 Paid Sources

- 1.5.1.2 Public Sources

- 1.5.1.3 Sources, by region

- 1.5.1 Secondary

- 1.6 Research Trail & Confidence Scoring

- 1.6.1 Research Trail Components:

- 1.6.2 Scoring Components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicles

- 2.2.3 Fuel

- 2.2.4 Technology

- 2.2.5 Component

- 2.2.6 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.1.1 Stringent emission and fuel economy regulations

- 3.2.1.1.2 Rising fuel prices and consumer demand for efficiency

- 3.2.1.1.3 Technological advancements in starter motors and batteries

- 3.2.1.1.4 Surge in hybrid and mild-hybrid vehicle production

- 3.2.1.1.5 Government incentives for eco-friendly technologies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High system and component costs

- 3.2.2.2 Battery wear and replacement frequency

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with hybrid and electric powertrains

- 3.2.3.2 Advancements in battery technology and energy recovery

- 3.2.3.3 Expansion into emerging automotive markets

- 3.2.3.4 Integration with ADAS and smart mobility platforms

- 3.2.1.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.8 Patent analysis

- 3.9 Sustainability and environmental aspects

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly Initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Use cases and application analysis

- 3.10.1 Urban driving applications

- 3.10.1.1 City traffic stop-start scenarios

- 3.10.1.2 Delivery vehicle optimization

- 3.10.1.3 Taxi & ride-sharing applications

- 3.10.1.4 Public transportation integration

- 3.10.2 Highway and mixed driving conditions

- 3.10.2.1 Long-distance travel applications

- 3.10.2.2 Commercial fleet operations

- 3.10.2.3 Emergency vehicle applications

- 3.10.2.4 Recreational vehicle integration

- 3.10.3 Specialized use cases

- 3.10.3.1 Construction & industrial vehicles

- 3.10.3.2 Agricultural equipment applications

- 3.10.3.3 Marine & off-road applications

- 3.10.1 Urban driving applications

- 3.11 Cost-benefit and ROI analysis framework

- 3.11.1 Total cost of ownership analysis

- 3.11.1.1 Initial system cost breakdown

- 3.11.1.2 Maintenance & replacement costs

- 3.11.1.3 Fuel savings quantification

- 3.11.1.4 Lifecycle cost modeling

- 3.11.2 Return on investment metrics

- 3.11.2.1 Payback period analysis by vehicle type

- 3.11.2.2 Net present value calculations

- 3.11.2.3 Internal rate of return assessment

- 3.11.2.4 Sensitivity analysis framework

- 3.11.1 Total cost of ownership analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 (USD Mn)

- 5.1 Key trends

- 5.2 Two wheelers

- 5.3 Passenger cars

- 5.3.1 Hatchbacks

- 5.3.2 Sedans

- 5.3.3 SUVs

- 5.4 Commercial vehicles

- 5.4.1 Light commercial vehicle

- 5.4.2 Medium commercial vehicle

- 5.4.3 Heavy commercial vehicle

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 (USD Mn)

- 6.1 Key trends

- 6.2 Diesel

- 6.3 Gasoline

- 6.4 CNG

- 6.5 Hybrid

Chapter 7 Market Estimates & Forecast, By Technology, 2021 - 2034 (USD Mn)

- 7.1 Key trends

- 7.2 Enhanced starter

- 7.2.1 Conventional starter

- 7.2.2 Tandem solenoid starter

- 7.3 Belt-driven alternator starter (BAS)

- 7.4 Direct injection engine systems

- 7.5 Integrated starter generator (ISG)

Chapter 8 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Mn)

- 8.1 Key trends

- 8.2 Engine control unit (ECU)

- 8.3 Battery

- 8.4 Alternator

- 8.5 Starter Motor

- 8.6 DC/DC converter

- 8.7 Sensors

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 (USD Mn)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.3.8 Portugal

- 10.3.9 Croatia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aisin Seiki

- 11.1.2 BorgWarner

- 11.1.3 Continental

- 11.1.4 Denso

- 11.1.5 Exide Technologies

- 11.1.6 GS Yuasa

- 11.1.7 Hitachi

- 11.1.8 Infineon Technologies

- 11.1.9 Johnson Controls

- 11.1.10 Magna International Inc.

- 11.1.11 Mahle

- 11.1.12 NXP Semiconductors

- 11.1.13 Panasonic

- 11.1.14 Robert Bosch

- 11.1.15 Schaeffler

- 11.1.16 Valeo

- 11.1.17 ZF Friedrichshafen

- 11.2 Regional Players

- 11.2.1 Calsonic Kansei

- 11.2.2 Eaton Corporation

- 11.2.3 Faurecia

- 11.2.4 Hella GmbH & Co.

- 11.2.5 Hyundai Mobis

- 11.2.6 JTEKT Corporation

- 11.2.7 Lear Corporation

- 11.2.8 Schaeffler AG

- 11.2.9 Visteon Corporation

- 11.3 Emerging Players

- 11.3.1 ABB Ltd.

- 11.3.2 Aptiv PLC

- 11.3.3 Infineon Technologies

- 11.3.4 LEM Holding

全球汽车怠速熄火系统市场

全球汽车怠速熄火系统市场 启停电池市场-全球产业规模、份额、趋势、机会及预测(按类型、车辆类型、最终用途、地区及竞争情况细分,2020-2030 年)

启停电池市场-全球产业规模、份额、趋势、机会及预测(按类型、车辆类型、最终用途、地区及竞争情况细分,2020-2030 年) 汽车启停电池市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

汽车启停电池市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2025-2033 年汽车启动停止系统市场(按组件、燃料类型、车辆类型、配销通路(原始设备製造商、售后市场)和地区)

2025-2033 年汽车启动停止系统市场(按组件、燃料类型、车辆类型、配销通路(原始设备製造商、售后市场)和地区) 到 2030 年汽车启动电池市场预测:按电池类型、车辆类型、组件类型、销售管道、技术、最终用户和地区进行的全球分析

到 2030 年汽车启动电池市场预测:按电池类型、车辆类型、组件类型、销售管道、技术、最终用户和地区进行的全球分析 汽车怠速熄火系统市场规模、份额、趋势分析报告:按车型、推进类型、销售管道、地区、细分市场预测,2024-2030年

汽车怠速熄火系统市场规模、份额、趋势分析报告:按车型、推进类型、销售管道、地区、细分市场预测,2024-2030年