|

市场调查报告书

商品编码

1833681

睡眠呼吸中止症植入物市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Sleep Apnea Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

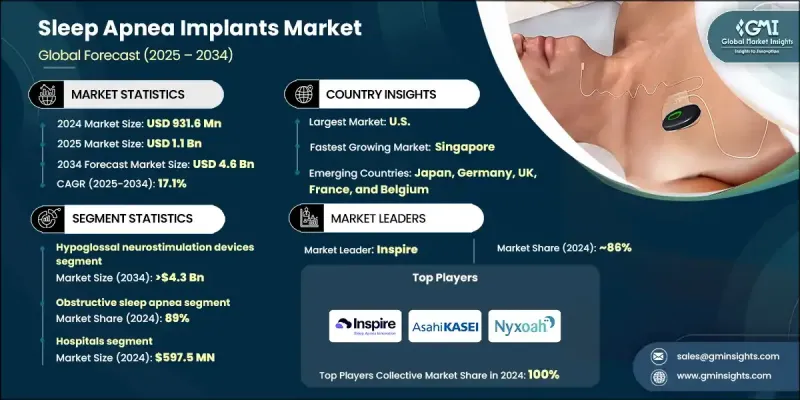

2024 年全球睡眠呼吸中止症植入物市场价值为 9.316 亿美元,预计到 2034 年将以 17.1% 的复合年增长率增长至 46 亿美元。

这项快速成长的动力源自于阻塞性睡眠呼吸中止症(OSA)盛行率的上升、持续性正压呼吸器(CPAP)疗法依从性有限以及人们对睡眠相关健康状况日益增长的认识。睡眠呼吸中止症植入物提供了一种替代面罩式治疗的方案,它提供微创、无需面罩的解决方案,刺激气道肌肉,防止睡眠期间出现阻塞。由于许多患者在使用传统疗法时感到不适、不耐受或不便,这些设备正日益受到关注。随着临床创新和对患者友善设备的日益关注,植入物正成为寻求长期有效解决方案的患者的关键选择。由于医生支持力度的增加、技术进步以及人们对未治疗的阻塞性睡眠呼吸中止症(OSA)与心血管、代谢和神经系统风险之间联繫的认识不断加深,市场也在不断扩大。 Inspire、Nyxoah 和旭化成等主要参与者正在塑造竞争格局,大型公司利用广泛的产品组合和全球影响力,而小型企业则透过利基技术和专注的研究工作来推动成长。这些动态共同推动着全球睡眠呼吸中止症治疗的变革性转变。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 9.316亿美元 |

| 预测值 | 46亿美元 |

| 复合年增长率 | 17.1% |

2024年,舌下神经刺激装置市场占据了86.7%的市场份额,这得益于其成熟的临床疗效、医生的偏好以及对传统疗法不耐受的患者群体的广泛采用。 CPAP的长期依从性有限,只有约三分之一的患者能够持续使用,这进一步增强了人们对可改善生活品质、带来便利的植入式治疗方案的需求。

阻塞性睡眠呼吸中止症(OSA)领域在2024年占据了89%的市场份额,这主要得益于OSA的高盛行率和传统治疗方法的不足。数百万患者仍未得到诊断,但人们越来越意识到该疾病与心臟病、糖尿病和认知能力下降之间的联繫,这推动了能够带来长期益处的植入疗法的发展。

2024年,医院植入手术市场收入达5.975亿美元,主要得益于植入手术。医院植入手术的主导地位源于其先进的基础设施、经验丰富的专业外科医生以及全面的术后护理,这些因素确保了植入手术的安全,并持续监测舌下神经刺激器和膈神经刺激器等器械。多学科团队和先进的诊断工具进一步提升了医院植入手术的采用率。

2024年,美国睡眠呼吸中止症植入物市场规模达8.4亿美元。该地区的成长得益于大量的阻塞性睡眠呼吸中止症(OSA)患者、优惠的报销框架以及早期植入式设备的普及。强大的医疗保健基础设施、积极的临床研究以及旭化成、Inspire Medical Systems和Nyxoah等公司的参与,将继续推动美国在该领域的领先地位。

睡眠呼吸中止症植入物产业的知名企业包括Inspire、Nyxoah和旭化成。为了巩固在睡眠呼吸中止症植入物市场的立足点,各公司正在实施以产品创新、临床研究和区域扩张为中心的策略。各公司正大力投资开发微创、患者友善设备,这些设备与传统疗法相比,可提高患者的依从性。扩大临床试验计画对于验证疗效、获得监管部门批准和建立医生信心也至关重要。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 阻塞性睡眠呼吸中止症盛行率不断上升

- 对 CPAP 的依从性和坚持性较低

- 技术进步

- 提高对睡眠呼吸中止症的认识

- 产业陷阱与挑战

- 睡眠呼吸中止症植入物成本高昂

- 与睡眠呼吸中止症植入物相关的併发症

- 市场机会

- 确诊 OSA 患者数量不断增加

- 向新兴市场扩张

- 成长动力

- 成长潜力分析

- 报销场景

- 监管格局

- 我们

- 欧洲

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 未来市场趋势

- 新兴国家的采用

- 2021-2024 年 OSA 发生率和盛行率

- 产品线分析

- 启动场景

- 2024年定价分析

- 投资前景

- 消费者行为分析

- 患者旅程图

- 波特的分析

- PESTEL分析

- 差距分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 我们

- 欧洲

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 舌下神经刺激装置

- 膈神经刺激器

第六章:市场估计与预测:按适应症,2021 - 2034 年

- 主要趋势

- 阻塞性睡眠呼吸中止症

- 中枢性睡眠呼吸中止症

第七章:市场估计与预测:依最终用途,2021 - 2034

- 主要趋势

- 医院

- 门诊手术中心

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 我们

- 欧洲

- 德国

- 英国

- 瑞士

- 法国

- 西班牙

- 义大利

- 荷兰

- 比利时

- 奥地利

- 芬兰

- 日本

- 新加坡

第九章:公司简介

- Asahi Kasei

- Inspire

- Nyxoah

The Global Sleep Apnea Implants Market was valued at USD 931.6 million in 2024 and is estimated to grow at a CAGR of 17.1% to reach USD 4.6 billion by 2034.

This rapid growth is being propelled by the rising prevalence of obstructive sleep apnea, limited compliance with CPAP therapy, and increasing awareness of sleep-related health conditions. Sleep apnea implants provide an alternative to mask-based treatments, offering minimally invasive, mask-free solutions that stimulate airway muscles to prevent obstruction during sleep. These devices are gaining traction as many patients experience discomfort, intolerance, or inconvenience with conventional therapies. With clinical innovations and a growing focus on patient-friendly devices, implants are becoming a critical option for individuals seeking long-term, effective solutions. The market is also expanding due to growing physician support, technological advancements, and heightened recognition of the link between untreated OSA and cardiovascular, metabolic, and neurological risks. Major players such as Inspire, Nyxoah, and Asahi Kasei are shaping the competitive landscape, with larger companies leveraging extensive product portfolios and global reach while smaller firms drive growth through niche technologies and focused research efforts. Collectively, these dynamics are driving a transformative shift in sleep apnea treatment worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $931.6 Million |

| Forecast Value | $4.6 Billion |

| CAGR | 17.1% |

The hypoglossal neurostimulation devices segment held 86.7% share in 2024, supported by proven clinical outcomes, physician preference, and widespread adoption among patients intolerant to traditional therapies. The limited long-term adherence to CPAP, with only about one-third of patients maintaining consistent use, has further reinforced demand for implantable options that offer improved quality of life and convenience.

The obstructive sleep apnea segment held an 89% share in 2024, driven by the high prevalence of OSA and the shortcomings of conventional treatment methods. Millions of individuals remain undiagnosed, yet awareness of the condition's connection to heart disease, diabetes, and cognitive decline is rising, driving the push for implant-based therapies that can deliver long-term benefits.

The hospitals segment generated USD 597.5 million in 2024, driven by the implant procedures. Their dominance stems from advanced infrastructure, availability of expert surgeons, and comprehensive post-operative care, ensuring safe implantation and ongoing monitoring of devices such as hypoglossal and phrenic nerve stimulators. Multidisciplinary teams and advanced diagnostic tools further strengthen hospital adoption rates.

United States Sleep Apnea Implants Market was valued at USD 840 million in 2024. Growth in the region is fueled by the high number of OSA patients, favorable reimbursement frameworks, and early adoption of implantable devices. A robust healthcare infrastructure, combined with active clinical research and the presence of companies like Asahi Kasei, Inspire Medical Systems, and Nyxoah, continues to drive the country's leadership in this space.

Prominent players in the Sleep Apnea Implants Industry include Inspire, Nyxoah, and Asahi Kasei. To strengthen their foothold in the sleep apnea implants market, companies are implementing strategies centered on product innovation, clinical research, and regional expansion. Firms are investing heavily in developing minimally invasive, patient-friendly devices that improve adherence compared to traditional therapies. Expanding clinical trial programs is also critical to validate efficacy, secure regulatory approvals, and build physician confidence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Indication channel trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of obstructive sleep apnea

- 3.2.1.2 Low compliance and adherence towards CPAP

- 3.2.1.3 Technological advancements

- 3.2.1.4 Rising awareness regarding sleep apnea

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of sleep apnea implants

- 3.2.2.2 Complications associated with sleep apnea implants

- 3.2.3 Market opportunities

- 3.2.3.1 Increasing number of diagnosed OSA patients

- 3.2.3.2 Expansion into emerging markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.5 Regulatory landscape

- 3.5.1 U.S.

- 3.5.2 Europe

- 3.6 Technology and innovation landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Future market trends

- 3.8 Adoption in emerging countries

- 3.9 Hypoglossal neurostimulation devices market, 2021 - 2034 (Units)

- 3.10 Incidence and prevalence of OSA, 2021-2024

- 3.11 Product pipeline analysis

- 3.12 Start-up scenario

- 3.13 Pricing analysis, 2024

- 3.14 Investment landscape

- 3.15 Consumer behaviour analysis

- 3.16 Patient journey map

- 3.17 Porter's analysis

- 3.18 PESTEL analysis

- 3.19 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 U.S.

- 4.2.2 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hypoglossal neurostimulation devices

- 5.3 Phrenic nerve stimulators

Chapter 6 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Obstructive sleep apnea

- 6.3 Central sleep apnea

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 U.S.

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 Switzerland

- 8.3.4 France

- 8.3.5 Spain

- 8.3.6 Italy

- 8.3.7 Netherlands

- 8.3.8 Belgium

- 8.3.9 Austria

- 8.3.10 Finland

- 8.4 Japan

- 8.5 Singapore

Chapter 9 Company Profiles

- 9.1 Asahi Kasei

- 9.2 Inspire

- 9.3 Nyxoah

2026年全球睡眠呼吸中止症植入市场报告

2026年全球睡眠呼吸中止症植入市场报告 睡眠呼吸植入市场规模、份额和成长分析(按产品、适应症、最终用户和地区划分):产业预测(2026-2033 年)

睡眠呼吸植入市场规模、份额和成长分析(按产品、适应症、最终用户和地区划分):产业预测(2026-2033 年) 全球睡眠呼吸植入市场

全球睡眠呼吸植入市场 2025-2029年全球睡眠呼吸植入市场

2025-2029年全球睡眠呼吸植入市场