|

市场调查报告书

商品编码

1844261

环境管理系统市场机会、成长动力、产业趋势分析及2025-2034年预测Environmental Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

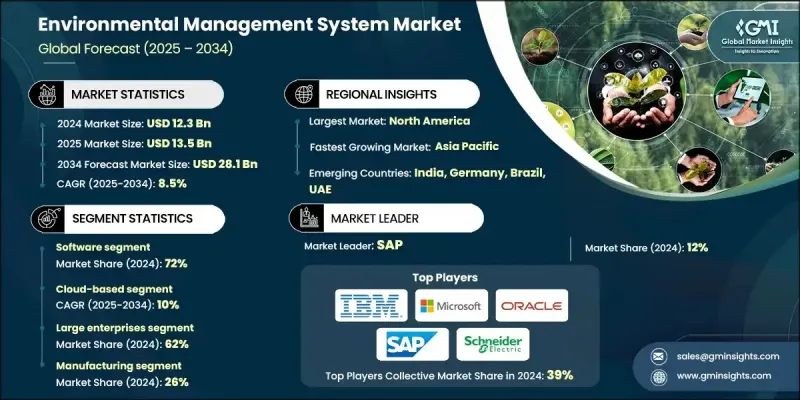

2024 年全球环境管理系统市场价值为 123 亿美元,预计将以 8.5% 的复合年增长率成长,到 2034 年达到 281 亿美元。

随着企业致力于加强环境责任制和合规性,环境管理系统 (EMS) 解决方案的采用率日益提升。这些系统提供结构化的框架和数位化平台,以高效管理环境责任。 EMS 解决方案基于 ISO 14001 和 EMAS 等全球标准,可协助企业制定政策、规划和实施营运控制、监控绩效并进行审查,以确保合规性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 123亿美元 |

| 预测值 | 281亿美元 |

| 复合年增长率 | 8.5% |

市场成长的动力源自于日益严格的合规要求、企业永续发展目标以及追踪各产业环境绩效的数位化解决方案日益增长的需求。企业正在利用环境管理系统 (EMS) 来展现透明度、管理环境风险,并将环境、社会和治理 (ESG) 优先事项融入其营运中。从能源和建筑业到製造业和公共服务业,企业纷纷部署环境管理系统 (EMS) 工具,以标准化流程并减少各职能部门的环境影响。随着监管机构和利害关係人对实现严格环境目标的压力日益增大,企业正在将环境管理体系与更广泛的业务策略相结合,从而提高效率并实现长期永续性。

2024年,软体部门占了72%的份额。这些平台旨在简化环境资料收集,自动化合规报告,并集中关键指标,以便更好地做出决策。与企业软体、物联网感测器和云端系统的集成,可实现跨多个地点的即时效能监控。以软体为基础的环境管理系统 (EMS) 可协助组织遵守环境法规,同时优化其资源使用和营运工作流程。遵循ISO 14001和其他标准的公司高度依赖EMS软体来维护记录、预测潜在问题,并协调复杂营运中的永续发展计画。

预计2025年至2034年,基于云端的EMS解决方案细分市场的复合年增长率将达到10%。这些平台提供可扩展的互联网託管环境,支援快速部署和从任何位置进行远端存取。云端EMS无需巨额前期投资,并支援与物联网设备无缝整合以实现即时追踪。订阅有助于降低资本成本,而集中式系统则支援跨站点协作、分析和自动更新。云端基础架构还增强了灾难復原、维护和版本控制功能,使团队能够在不同区域跨不同区域以更高的敏捷性和回应速度开展工作。

2024年,美国环境管理系统市场规模达38亿美元。受联邦和州两级环境政策执行和永续发展承诺的推动,美国环境管理系统平台的采用率持续上升。各机构致力于减少排放、改善废弃物控制并增强环境公平,这催生了对结构化系统的需求,以确保合规性。公用事业、製造业和能源等行业越来越多地采用环境管理系统来监控排放、管理资源并简化合规报告。

影响全球环境管理系统市场的关键参与者包括赛默飞世尔科技、SAP、IBM、威立雅环境、施耐德电机、甲骨文、微软、西门子、霍尼韦尔国际和艾默生电气。环境管理系统市场的领先公司正专注于产品创新、云端整合和数据驱动的洞察,以巩固其市场地位。许多公司正在开发基于人工智慧的平台,以实现预测分析、即时报告和自动合规性追踪。与 ERP 和物联网供应商的合作使得 EMS 解决方案能够更顺畅地整合到企业营运中。企业也透过区域办事处、基于云端的服务和多语言支援系统扩大全球影响力。持续的网路安全投资确保了资料的安全处理,而可扩展的订阅模式则吸引了更广泛的客户。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预报

- 研究假设和局限性

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 日益严格的监管合规要求

- 扩大企业永续发展与 ESG 计划

- 数位平台在环境资料管理的应用日益增多

- 公共部门环境监督体系的发展

- 采用 ISO 14001 和 EMAS 等国际标准

- 产业陷阱与挑战

- 与现有企业系统的复杂集成

- 组织内部缺乏专业知识

- 市场机会

- 与物联网、云端和分析平台集成

- 越来越关註生命週期资源效率

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- Pestel分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 成本分解分析

- 软体授权和订阅费用

- 硬体和感测器投资

- 实施和整合费用

- 培训和变更管理成本

- 持续维护和支持

- 合规与审计成本

- 专利分析

- 永续性和环境方面

- 绿色IT实施

- 碳中和技术运营

- 永续软体开发

- 科技对环境的影响

- 循环经济原则

- 净零技术目标

- 用例和应用

- 最佳情况

- 风险评估框架

- 环境合规风险

- 技术实施风险

- 资料安全和隐私风险

- 供应商依赖风险

- 监理变化风险

- 营运中断风险

- 声誉和品牌风险

- 投资格局分析

- 环境技术领域的创投

- 企业永续发展投资

- 政府环境资金

- 绿色债券与永续金融

- ESG投资趋势

- 以投资类型进行的投资报酬率分析

- 气候科技资金

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 多边环境协定

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:依组件划分,2021 - 2034 年

- 主要趋势

- 软体

- 服务

第六章:市场估计与预测:依部署,2021 - 2034 年

- 主要趋势

- 本地部署

- 基于云端

第七章:市场估计与预测:依企业规模,2021 - 2034

- 主要趋势

- 大型企业

- 中小企业

第 8 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 製造业

- 建造

- 能源和公用事业

- 化学品

- 汽车

- 製药

- 食品和饮料

- 政府和公共部门

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧人

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- 全球参与者

- Emerson Electric

- Honeywell

- IBM

- Microsoft

- Oracle

- SAP

- Schneider Electric

- Siemens

- Thermo Fisher Scientific

- Veolia Environnement

- 区域参与者

- ABB

- APEVA

- AspenTech

- Bentley Systems

- Dassault Systemes

- GE Digital

- Hexagon

- Rockwell Automation

- Trimble

- Yokogawa Electric

- 新兴企业和创新者

- EcoOnline

- Enablon

- Gensuite

- Intelex Technologies

- ProcessMAP

- Quentic

- SafetySync

- SHE Software

- Sphera Solutions

- VelocityEHS

The Global Environmental Management System Market was valued at USD 12.3 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 28.1 billion by 2034.

Environmental Management System solutions are seeing increased adoption as businesses work toward stronger environmental accountability and regulatory compliance. These systems provide structured frameworks and digital platforms to manage environmental responsibilities efficiently. Built on global standards such as ISO 14001 and EMAS, EMS solutions help organizations develop policies, plan and implement operational controls, monitor performance, and conduct reviews to maintain regulatory alignment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.3 Billion |

| Forecast Value | $28.1 Billion |

| CAGR | 8.5% |

Market growth is fueled by tightening compliance demands, corporate sustainability objectives, and the rising need for digital solutions that track environmental performance across sectors. Businesses are leveraging EMS to demonstrate transparency, manage environmental risks, and integrate ESG priorities into their operations. From energy and construction to manufacturing and public sector services, EMS tools are deployed to standardize procedures and reduce environmental impact across various functions. With mounting pressure from regulators and stakeholders to meet strict environmental goals, companies are aligning EMS with wider business strategies, improving efficiency and long-term sustainability in the process.

In 2024, the software segment held a 72% share. These platforms are designed to streamline environmental data collection, automate compliance reporting, and centralize key metrics for better decision-making. Integration with enterprise software, IoT sensors, and cloud systems enables real-time performance monitoring across multiple locations. Software-based EMS helps organizations adhere to environmental regulations while optimizing their resource usage and operational workflows. Companies following ISO 14001 and other standards rely heavily on EMS software to maintain records, predict potential issues, and coordinate sustainability initiatives across complex operations.

The cloud-based EMS solutions segment is forecasted to grow at a CAGR of 10% from 2025 to 2034. These platforms offer scalable, internet-hosted environments that enable rapid deployment and remote access from any location. Cloud EMS eliminates the need for heavy upfront investment and supports seamless integration with IoT devices for real-time tracking. Subscriptions help reduce capital costs, while centralized systems support cross-site collaboration, analytics, and automated updates. Cloud infrastructure also enhances disaster recovery, maintenance, and version control, allowing teams to operate with greater agility and responsiveness across different regions.

United States Environmental Management System Market generated USD 3.8 billion in 2024. Adoption of EMS platforms in the US continues to rise, driven by environmental policy enforcement and sustainability commitments across federal and state levels. Agencies promote reducing emissions, improving waste control, and enhancing environmental equity, creating demand for structured systems to ensure compliance. Industries such as utilities, manufacturing, and energy are increasingly turning to EMS to monitor emissions, manage resources, and streamline compliance reporting.

Key players shaping the Global Environmental Management System Market include Thermo Fisher Scientific, SAP, IBM, Veolia Environnement, Schneider Electric, Oracle, Microsoft, Siemens, Honeywell International, and Emerson Electric. Leading companies in the Environmental Management System Market are focusing on product innovation, cloud integration, and data-driven insights to strengthen their market position. Many are developing AI-powered platforms that enable predictive analytics, real-time reporting, and automated compliance tracking. Partnerships with ERP and IoT vendors allow for smoother integration of EMS solutions into enterprise operations. Businesses are also expanding global reach through regional offices, cloud-based services, and multilingual support systems. Ongoing investment in cybersecurity ensures secure data handling, while scalable subscription models attract a wider range of clients.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Deployment

- 2.2.4 Enterprise Size

- 2.2.5 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing regulatory compliance requirements

- 3.2.1.2 Expansion of corporate sustainability and ESG programs

- 3.2.1.3 Rising use of digital platforms for environmental data management

- 3.2.1.4 Growth in public sector environmental oversight systems

- 3.2.1.5 Adoption of international standards like ISO 14001 and EMAS

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex integration with existing enterprise systems

- 3.2.2.2 Lack of specialized expertise within organizations

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with IoT, cloud, and analytics platforms

- 3.2.3.2 Rising focus on lifecycle resource efficiency

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.8.1 Software licensing & subscription costs

- 3.8.2 Hardware & sensor investment

- 3.8.3 Implementation & integration expenses

- 3.8.4 Training & change management costs

- 3.8.5 Ongoing maintenance & support

- 3.8.6 Compliance & audit costs

- 3.9 Patent analysis

- 3.10 Sustainability & environmental aspects

- 3.10.1 Green IT implementation

- 3.10.2 Carbon neutral technology operations

- 3.10.3 Sustainable software development

- 3.10.4 Environmental impact of technology

- 3.10.5 Circular economy principles

- 3.10.6 Net-zero technology goals

- 3.11 Use cases and applications

- 3.12 Best-case scenario

- 3.13 Risk assessment framework

- 3.13.1 Environmental compliance risks

- 3.13.2 Technology implementation risks

- 3.13.3 Data security & privacy risks

- 3.13.4 Vendor dependency risks

- 3.13.5 Regulatory change risks

- 3.13.6 Operational disruption risks

- 3.13.7 Reputation & brand risks

- 3.14 Investment landscape analysis

- 3.14.1 Venture capital in environmental technology

- 3.14.2 Corporate sustainability investment

- 3.14.3 Government environmental funding

- 3.14.4 Green bond & sustainable finance

- 3.14.5 ESG investment trends

- 3.14.6 ROI analysis by investment type

- 3.14.7 Climate technology funding

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

Chapter 6 Market Estimates & Forecast, By Deployment, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 On-Premises

- 6.3 Cloud-Based

Chapter 7 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Large Enterprises

- 7.3 Small and Medium Enterprises

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Manufacturing

- 8.3 Construction

- 8.4 Energy and utilities

- 8.5 Chemicals

- 8.6 Automotive

- 8.7 Pharmaceuticals

- 8.8 Food and Beverage

- 8.9 Government & public sector

- 8.10 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Emerson Electric

- 10.1.2 Honeywell

- 10.1.3 IBM

- 10.1.4 Microsoft

- 10.1.5 Oracle

- 10.1.6 SAP

- 10.1.7 Schneider Electric

- 10.1.8 Siemens

- 10.1.9 Thermo Fisher Scientific

- 10.1.10 Veolia Environnement

- 10.2 Regional Players

- 10.2.1 ABB

- 10.2.2 APEVA

- 10.2.3 AspenTech

- 10.2.4 Bentley Systems

- 10.2.5 Dassault Systemes

- 10.2.6 GE Digital

- 10.2.7 Hexagon

- 10.2.8 Rockwell Automation

- 10.2.9 Trimble

- 10.2.10 Yokogawa Electric

- 10.3 Emerging Players & Innovators

- 10.3.1 EcoOnline

- 10.3.2 Enablon

- 10.3.3 Gensuite

- 10.3.4 Intelex Technologies

- 10.3.5 ProcessMAP

- 10.3.6 Quentic

- 10.3.7 SafetySync

- 10.3.8 SHE Software

- 10.3.9 Sphera Solutions

- 10.3.10 VelocityEHS

全球国防环境控制系统 (ECS) 市场 (2026–2036)

全球国防环境控制系统 (ECS) 市场 (2026–2036) 2026年全球自动化气候控制市场报告

2026年全球自动化气候控制市场报告 环境智慧平台市场 - 全球产业规模、份额、趋势、机会和预测(按部署方式、服务、最终用户、地区和竞争格局划分,2021-2031 年)

环境智慧平台市场 - 全球产业规模、份额、趋势、机会和预测(按部署方式、服务、最终用户、地区和竞争格局划分,2021-2031 年) 环境控制系统市场规模、份额和成长分析(按系统类型、组件、平台、最终用户、应用、技术和地区划分)-2026-2033年产业预测

环境控制系统市场规模、份额和成长分析(按系统类型、组件、平台、最终用户、应用、技术和地区划分)-2026-2033年产业预测 环境管理系统市场规模、份额和趋势分析报告:按组件、部署、公司规模、最终用途、地区和细分市场预测,2025 年至 2033 年

环境管理系统市场规模、份额和趋势分析报告:按组件、部署、公司规模、最终用途、地区和细分市场预测,2025 年至 2033 年 全球环境控制系统市场:市场规模、份额、趋势分析(按产品、组件、最终用途和地区)、展望和未来预测(2024-2031 年)环境控制系统市场规模、份额、趋势分析报告:按组件、最终用途、产品、地区、细分市场预测,2025-2030 年

全球环境控制系统市场:市场规模、份额、趋势分析(按产品、组件、最终用途和地区)、展望和未来预测(2024-2031 年)环境控制系统市场规模、份额、趋势分析报告:按组件、最终用途、产品、地区、细分市场预测,2025-2030 年 环境智慧平台市场:依产品类型、最终用户、地区 - 全球产业分析、规模、占有率、成长、趋势、预测,2024-2031 年

环境智慧平台市场:依产品类型、最终用户、地区 - 全球产业分析、规模、占有率、成长、趋势、预测,2024-2031 年