|

市场调查报告书

商品编码

1844276

DTP 疫苗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测DTP Vaccines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

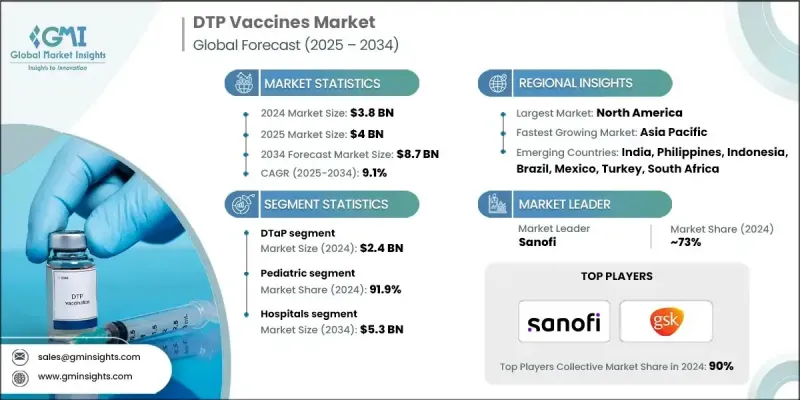

2024 年全球 DTP 疫苗市场价值为 38 亿美元,预计到 2034 年将以 9.1% 的复合年增长率增长至 87 亿美元。

这一显着增长得益于全球免疫接种力度的加大,尤其是在传染病仍构成严重威胁的发展中国家。人们对疫苗可预防疾病的认识不断提高以及医疗基础设施的改善,在促进疫苗接种方面发挥关键作用。此外,疫苗技术的创新,尤其是更安全、更有效的联合疫苗的研发,正在增强公众信心,并推动疫苗接种率的提高。在全球卫生组织和国家医疗保健计画的支持下,儿童免疫接种仍然是主要的需求驱动因素。预防婴儿白喉、破伤风和百日咳的需求日益增长,这促使人们增加对疫苗研发和分发的投资。随着免疫覆盖率的扩大,将百白破疫苗纳入更大规模的联合方案,正在提高依从性、简化接种程序并提高可及性。世界各国政府正投入更多资源加强免疫网络,同时公私合作也正在扩大覆盖范围和推广范围。这些因素,加上不断上升的出生率和更广泛的医疗保健可近性,预计将在预测期内支撑全球百白破疫苗市场的发展。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 38亿美元 |

| 预测值 | 87亿美元 |

| 复合年增长率 | 9.1% |

2024年,百日咳疫苗(DTaP)市场规模达24亿美元。由于在常规儿科免疫接种计划中被广泛采用,该市场仍占据主导地位。 DTaP疫苗采用无细胞百日咳成分,与先前的全细胞疫苗相比,其安全性更高,副作用更少。全球卫生机构和国家免疫规划积极推广DTaP疫苗的使用,进一步推动了需求成长。对联合疫苗的偏好日益增长以及加强针接种的增加是该市场增长的关键因素,尤其是在医疗基础设施和政府疫苗接种项目覆盖面更广的地区。

2024年,儿科疫苗市占率达91.9%。这得归功于全球高出生率以及百白破疫苗被纳入儿童早期免疫接种计划。各国政府和卫生组织持续重视儿科疫苗接种,从而增加了资金投入,改善了疫苗接种系统,并提高了儿童疾病预防意识。随着百白破疫苗成分越来越多地融入五价和六价疫苗等多价疫苗配方,儿科疫苗覆盖率进一步提高。这些疫苗配方简化了疫苗接种程序,简化了物流,并提高了医护人员和家长的遵从性。

2024年,北美百白破疫苗市场占据41.3%的市占率。其领先地位得益于高额的医疗保健投入、完善的免疫框架以及持续的公众教育工作。赛诺菲、默克和葛兰素史克等主要製药公司强大的分销网络确保了疫苗在美国和加拿大的广泛供应。全面的报销政策和全国性的宣传措施有助于维持稳定的疫苗接种率。公共卫生机构积极推广儿童免疫接种,巩固了该地区在疫苗覆盖率和普及率方面的领先地位。

积极参与全球 DTP 疫苗市场的主要参与者包括 LG Chem、Biological E、Walvax、Finlay Institute、Indian Immunologicals、HLL Lifecare Limited (HLL)、Bilthoven Biologicals、葛兰素史克 (GSK)、赛诺菲、默克、Microgen、Panacea Biotectec、PTA、AakA. Biomed、Boryung、印度血清研究所、北京民海生物技术和 ST Pharma。为了巩固其在 DTP 疫苗市场的地位,领先公司正在采取策略性倡议,包括扩大生产能力和扩大生产规模,以满足全球市场日益增长的需求。企业越来越多地与公共卫生机构和政府合作,以确保供应合约并加强疫苗分发。许多公司也投资研究,开发副作用更少、免疫原性更好的下一代製剂。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 日益重视预防性医疗保健

- 扩大免疫接种计划

- 政府措施和支持措施

- 不断进步的技术

- 产业陷阱与挑战

- 严格的监管审批流程

- 开发和生产成本高

- 市场机会

- 加强疫苗分发的公私伙伴关係

- 扩大成人疫苗接种计划

- 成长动力

- 成长潜力分析

- 监管格局

- 管道分析

- 技术格局

- 投资和融资格局

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 公司矩阵分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按疫苗类型,2021 - 2034 年

- 主要趋势

- 百时美施贵宝

- DTwP

- 经皮/经皮穿刺

第六章:市场估计与预测:按年龄组,2021 - 2034 年

- 主要趋势

- 儿科

- 成人

第七章:市场估计与预测:依最终用途,2021 - 2034

- 主要趋势

- 医院

- 民众

- 私人的

- 专科诊所

- 其他最终用途

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Arab Company for Pharmaceutical Products (Arabio)

- Beijing Minhai Biological Technology

- Bilthoven Biologicals

- Biological E

- Boryung

- Finlay Institute

- GlaxoSmithKline (GSK)

- HLL Lifecare Limited (HLL)

- IBSS Biomed

- Indian Immunologicals

- LG Chem

- Merck

- Microgen

- Panacea Biotec

- PT Bio Farma

- Sanofi

- Serum Institute of India

- Walvax

The Global DTP Vaccines Market was valued at USD 3.8 billion in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 8.7 billion by 2034.

This significant growth is driven by increasing immunization efforts worldwide, especially across developing countries where infectious diseases remain a serious threat. Enhanced awareness of vaccine-preventable diseases and improvements in healthcare infrastructure are playing a key role in boosting vaccine uptake. Further, innovation in vaccine technology, especially the development of safer and more effective combination vaccines, is increasing public confidence and driving higher adoption rates. Pediatric immunization continues to be a major demand driver, supported by global health organizations and national healthcare programs. The growing need to prevent diphtheria, tetanus, and pertussis among infants is encouraging greater investment in vaccine research and distribution. As immunization coverage expands, the integration of DTP vaccines into larger combination schedules is improving compliance, simplifying administration, and increasing accessibility. Governments across the globe are allocating more resources to strengthen their immunization networks, while public-private collaborations are enhancing outreach and coverage. These factors, combined with rising birth rates and broader healthcare access, are expected to support the global DTP vaccines market over the forecast period.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.8 Billion |

| Forecast Value | $8.7 Billion |

| CAGR | 9.1% |

In 2024, the DTaP segment generated USD 2.4 billion. This segment remains dominant due to its broad adoption in routine pediatric immunization schedules. DTaP vaccines utilize acellular pertussis components, which offer a safer profile and fewer adverse effects compared to earlier whole-cell options. Global health bodies and national immunization programs actively promote DTaP's use, further driving demand. The rising preference for combination vaccines and increased administration of booster shots are key growth factors for the segment, especially in regions with better access to healthcare infrastructure and government vaccination programs.

The pediatric segment held a 91.9% share in 2024. This is due to high global birth rates and the inclusion of DTP vaccines in early childhood immunization schedules. Governments and health organizations continue to prioritize pediatric vaccinations, leading to increased funding, improved vaccine delivery systems, and heightened awareness of disease prevention in children. With the growing integration of DTP components into multivalent formulations, such as pentavalent and hexavalent vaccines, pediatric coverage is further strengthened. These formulations streamline vaccine schedules, simplify logistics, and increase compliance from both healthcare providers and parents.

North America DTP Vaccines Market held a 41.3% share in 2024. The leading position is supported by high healthcare investments, established immunization frameworks, and continuous public education efforts. Robust distribution networks of key pharmaceutical companies like Sanofi, Merck, and GSK ensure broad vaccine availability across the U.S. and Canada. Comprehensive reimbursement policies and national awareness initiatives help sustain consistent vaccination rates. Public health agencies actively promote childhood immunizations, reinforcing the region's leadership in vaccine coverage and adoption.

Key players actively involved in the Global DTP Vaccines Market include LG Chem, Biological E, Walvax, Finlay Institute, Indian Immunologicals, HLL Lifecare Limited (HLL), Bilthoven Biologicals, GlaxoSmithKline (GSK), Sanofi, Merck, Microgen, Panacea Biotec, PT Bio Farma, Arab Company for Pharmaceutical Products (Arabio), IBSS Biomed, Boryung, Serum Institute of India, Beijing Minhai Biological Technology, and ST Pharma. To strengthen their position in the DTP vaccines market, leading companies are adopting strategic initiatives that include expanding production capacity and scaling manufacturing operations to meet growing demand across global markets. Firms are increasingly collaborating with public health bodies and governments to secure supply contracts and enhance vaccine distribution. Many are also investing in research to develop next-generation formulations with fewer side effects and better immunogenicity.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Vaccine type trends

- 2.2.3 Age group trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising emphasis on preventive healthcare

- 3.2.1.2 Expanding immunization programs

- 3.2.1.3 Government initiatives and supportive measures

- 3.2.1.4 Growing technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory approval processes

- 3.2.2.2 High development and production costs

- 3.2.3 Market opportunities

- 3.2.3.1 Growing public-private partnerships for vaccine distribution

- 3.2.3.2 Expanding adult vaccination programs

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Pipeline analysis

- 3.6 Technology landscape

- 3.7 Investment and funding landscape

- 3.8 Future market trends

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Company matrix analysis

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Vaccine Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 DTaP

- 5.3 DTwP

- 5.4 Td/TdaP

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pediatric

- 6.3 Adult

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.2.1 Public

- 7.2.2 Private

- 7.3 Specialty clinics

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Arab Company for Pharmaceutical Products (Arabio)

- 9.2 Beijing Minhai Biological Technology

- 9.3 Bilthoven Biologicals

- 9.4 Biological E

- 9.5 Boryung

- 9.6 Finlay Institute

- 9.7 GlaxoSmithKline (GSK)

- 9.8 HLL Lifecare Limited (HLL)

- 9.9 IBSS Biomed

- 9.10 Indian Immunologicals

- 9.11 LG Chem

- 9.12 Merck

- 9.13 Microgen

- 9.14 Panacea Biotec

- 9.15 PT Bio Farma

- 9.16 Sanofi

- 9.17 Serum Institute of India

- 9.18 Walvax

儿童疫苗市场报告:按类型、技术、应用和地区划分(2026-2034年)

儿童疫苗市场报告:按类型、技术、应用和地区划分(2026-2034年) 麻疹-德国麻疹疫苗市场:依疫苗品牌、通路和地区划分

麻疹-德国麻疹疫苗市场:依疫苗品牌、通路和地区划分 儿科吸入糖皮质激素市场按产品、适应症、分销管道、最终用户和年龄组别划分-全球预测,2026-2032年

儿科吸入糖皮质激素市场按产品、适应症、分销管道、最终用户和年龄组别划分-全球预测,2026-2032年 全球儿童疫苗市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考察、未来预测(2026-2034)全球儿科疫苗开发市场规模(按类型、技术、应用、区域范围和预测)IPV 疫苗市场(按疫苗品牌、分销管道和地区)—市场规模、份额、前景和机会分析(2025-2032)

全球儿童疫苗市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的考察、未来预测(2026-2034)全球儿科疫苗开发市场规模(按类型、技术、应用、区域范围和预测)IPV 疫苗市场(按疫苗品牌、分销管道和地区)—市场规模、份额、前景和机会分析(2025-2032) 儿科疫苗市场规模、份额、趋势分析报告:按类型、技术、应用、地区、细分市场预测,2024-2030 年

儿科疫苗市场规模、份额、趋势分析报告:按类型、技术、应用、地区、细分市场预测,2024-2030 年 儿科疫苗市场、机会、成长动力、产业趋势分析与预测,2024-2032全球儿科疫苗市场-2024年至2029年预测

儿科疫苗市场、机会、成长动力、产业趋势分析与预测,2024-2032全球儿科疫苗市场-2024年至2029年预测 IPV 疫苗市场,按疫苗类型、年龄层、分布、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测

IPV 疫苗市场,按疫苗类型、年龄层、分布、最终用户、国家和地区 - 2024-2032 年行业分析、市场规模、市场份额和预测