|

市场调查报告书

商品编码

1844301

羽毛加工设备市场机会、成长动力、产业趋势分析及2025-2034年预测Feather Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

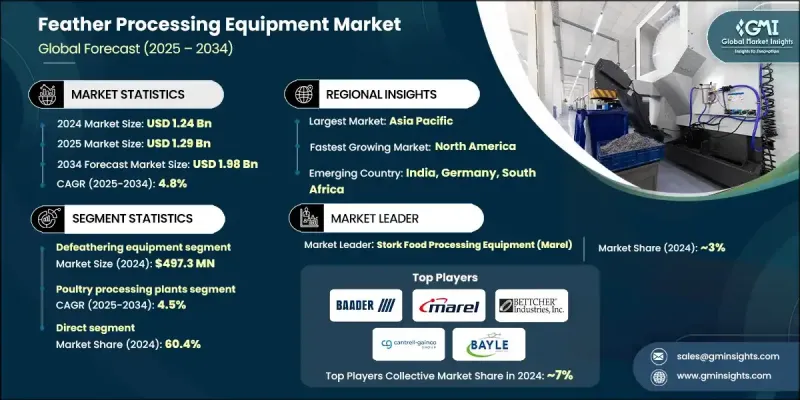

2024 年全球羽毛加工设备市场价值为 12.4 亿美元,预计将以 4.8% 的复合年增长率成长,到 2034 年达到 19.8 亿美元。

人们日益重视环保的废弃物管理实践,这大大推动了羽毛回收技术的应用。据估计,每年约有800万吨家禽羽毛产生,这为永续利用提供了重大机会。这些曾经被当作废物丢弃的羽毛,如今正被重新利用,製成肥料、纺织品和动物饲料等利润丰厚的产品。这种转变有助于减少环境影响,同时为企业开启新的收入来源。随着永续发展目标和更严格的环保合规标准日益凸显,製造商正在增加对下一代羽毛加工设备的投资。这些发展正在重塑市场格局,使永续性成为成长的核心驱动力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 12.4亿美元 |

| 预测值 | 19.8亿美元 |

| 复合年增长率 | 4.8% |

持续的技术进步正在改变羽毛加工方式。自动化程度的提高和节能机械的出现正在提升生产力、改善卫生标准并简化操作流程。日益严格的废弃物处理法规促使家禽加工企业采用更有效、更环保的解决方案。越来越多的家禽加工厂正在将羽毛加工单元与更广泛的提炼系统整合。这种转变推动了对模组化、易于安装的机器的需求,这些机器可以无缝融入现有的工作流程,从而提高操作灵活性和效率。

2024年,除毛设备市场规模达4.973亿美元,预计2025年至2034年期间的复合年增长率将达到4.4%。家禽产品需求激增,尤其是在新兴经济体,促使加工厂实现自动化运营,减少对人工的依赖。除毛机在禽肉加工早期阶段,对于实现高产量、保持清洁度和确保均匀性起着至关重要的作用。随着生产规模的扩大,对快速卫生的除毛解决方案的需求也日益迫切。

家禽加工设施领域在2024年占据52.9%的市场份额,预计到2034年将以4.5%的复合年增长率成长。随着全球禽肉消费量持续成长,加工商正在扩大产能并升级现有系统,以经济高效、卫生且永续的方式管理羽毛副产品。随着工厂致力于优化每个操作步骤,能够清洁、脱毛、干燥和包装羽毛的整合系统的需求日益增长。

2024年,美国羽毛加工设备市场规模达2.664亿美元,预计2025年至2034年的复合年增长率为4.7%。美国羽毛加工产业受益于强劲的国内家禽业,该产业由高消费率和严格的监管框架支撑。各企业正大力投资先进、节能和自动化设备,以符合食品安全法规、环境政策和生产力目标。这些发展使美国在现代羽毛加工技术的采用方面处于领先地位。

影响羽毛加工设备市场竞争格局的关键参与者包括 Kuiper & Zonen、Taizy Machinery、Bayle、TALSA、Bettcher Industries、Cantrell-Gainco、MAJA、LINCO、Baader Group、Meyn、Scott Automation、Banss、Stork (Marel)、Hubbard Systems 和 Ruvii。羽毛加工设备市场的公司正在采取多种策略来巩固其市场地位。主要重点是透过自动化和能源效率进行产品创新,以满足不断发展的永续性和监管标准。许多参与者正在透过模组化、即插即用的解决方案扩展其产品线,这些解决方案可轻鬆整合到现有的处理系统中。与家禽加工厂的合作和长期服务协议正在帮助公司获得经常性收入来源。策略性併购也被用来加强技术能力和扩大地理覆盖范围。

目录

第一章:方法论与范围

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 家禽业快速扩张

- 对永续废弃物管理的需求增加

- 羽毛副产品需求不断成长

- 产业陷阱与挑战

- 初期投资成本高

- 维护和技术专业知识

- 成长动力

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依设备类型

- 监管格局

- 标准和合规性要求

- 区域监理框架

- 认证标准

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依设备类型,2021 - 2034 年

- 主要趋势

- 除毛设备

- 清洗干燥设备

- 研磨和切割设备

- 分类和分级设备

- 压制和捆扎设备

- 干燥和脱水系统

- 包装和搬运设备

- 其他(灭菌消毒系统、鼓风机、除尘等)

第六章:市场估计与预测:按用途,2021 - 2034 年

- 主要趋势

- 回收羽毛

- 处女羽毛

第七章:市场估计与预测:依产能,2021 - 2034

- 主要趋势

- 高达 500 公斤/小时

- 500-2,500公斤/小时

- 高于2500公斤/小时

第 8 章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 家禽

- 鸡

- 鹅

- 鸭子

- 其他的

- 孔雀

- 其他(鸵鸟等)

第九章:市场估计与预测:依最终用途产业,2021 - 2034 年

- 主要趋势

- 家禽加工厂

- 家禽饲养

- 屠宰

- 羽绒和羽毛

- 衣服

- 寝具

- 羽毛粉生产商

- 艺术与手工艺

- 其他(肥料、建筑隔热、过滤系统等)

第 10 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 直接的

- 间接

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 马来西亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 沙乌地阿拉伯

- 阿联酋

- 南非

第十二章:公司简介

- Baader Group

- Banss

- Bayle

- Bettcher Industries

- Cantrell-Gainco

- Hubbard Systems

- Kuiper & Zonen

- LINCO

- MAJA

- Meyn

- Ruvii

- Scott Automation

- Stork (Marel)

- TALSA

- Taizy Machinery

The Global Feather Processing Equipment Market was valued at USD 1.24 billion in 2024 and is estimated to grow at a CAGR of 4.8% to reach USD 1.98 billion by 2034.

Growing emphasis on eco-friendly waste management practices is significantly driving the adoption of feather recycling technologies. According to estimates, around 8 million metric tons of poultry feathers are generated each year, presenting a major opportunity for sustainable utilization. These feathers, once discarded as waste, are now being repurposed into profitable products such as fertilizers, textiles, and animal feed. This shift is helping to cut down environmental impact while opening new revenue streams for businesses. As sustainability targets and stricter environmental compliance standards become more prominent, manufacturers are increasing investments in next-gen feather processing equipment. These developments are reshaping the market landscape, making sustainability a central driver of growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.24 Billion |

| Forecast Value | $1.98 Billion |

| CAGR | 4.8% |

Ongoing technological improvements are transforming how feather processing is carried out. Enhanced automation and energy-efficient machinery are boosting productivity, improving hygiene standards, and streamlining operations. Tighter regulations related to waste disposal are prompting poultry processors to adopt more effective and environmentally conscious solutions. A growing number of poultry processing plants are now integrating feather processing units with broader rendering systems. This shift is fueling demand for modular, easy-to-install machines that seamlessly fit into existing workflows, boosting operational flexibility and efficiency.

The defeathering equipment segment was valued at USD 497.3 million in 2024 and is forecasted to grow at a CAGR of 4.4% between 2025 and 2034. Surging demand for poultry products, particularly in emerging economies, is prompting processing facilities to automate their operations and reduce their reliance on manual labor. Defeathering machines play a critical role in achieving high throughput, maintaining cleanliness, and ensuring uniformity during the early stages of poultry processing. As production scales up, the need for fast and hygienic defeathering solutions becomes more essential.

The poultry processing facilities segment held a 52.9% share in 2024 and is projected to grow at a CAGR of 4.5% through 2034. With poultry meat consumption continuing to rise globally, processors are expanding capacity and upgrading existing systems to manage feather by-products in a cost-effective, sanitary, and sustainable manner. Integrated systems that can clean, defeather, dry, and package feathers are seeing rising demand as plants aim to optimize every step of the operation.

United States Feather Processing Equipment Market was valued at USD 266.4 million in 2024 and is expected to grow at a CAGR of 4.7% from 2025 to 2034. The U.S. feather processing industry benefits from a strong domestic poultry sector supported by high consumption rates and stringent regulatory frameworks. Companies are investing heavily in advanced, energy-efficient, and automated equipment to align with food safety mandates, environmental policies, and productivity goals. These developments are positioning the U.S. as a frontrunner in the adoption of modern feather processing technologies.

Key players shaping the competitive landscape of the Feather Processing Equipment Market include Kuiper & Zonen, Taizy Machinery, Bayle, TALSA, Bettcher Industries, Cantrell-Gainco, MAJA, LINCO, Baader Group, Meyn, Scott Automation, Banss, Stork (Marel), Hubbard Systems, and Ruvii. Companies in the Feather Processing Equipment Market are adopting several strategies to reinforce their market position. A primary focus is on product innovation through automation and energy efficiency to meet evolving sustainability and regulatory standards. Many players are expanding their product lines with modular, plug-and-play solutions that integrate easily into existing processing systems. Collaborations with poultry processing plants and long-term service agreements are helping companies secure recurring revenue streams. Strategic mergers and acquisitions are also being used to strengthen technical capabilities and broaden geographic reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Equipment type

- 2.2.3 Usage

- 2.2.4 Capacity

- 2.2.5 Application

- 2.2.6 End use industry

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid expansion of poultry industry

- 3.2.1.2 Increased demand for sustainable waste management

- 3.2.1.3 Rising demand for feather-based by-products

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Maintenance and technical expertise

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By Equipment type

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Equipment Type, 2021 - 2034, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Defeathering equipment

- 5.3 Cleaning and drying equipment

- 5.4 Grinding & cutting equipment

- 5.5 Sorting & grading equipment

- 5.6 Pressing & bunching equipment

- 5.7 Drying and dehydration systems

- 5.8 Packaging and handling equipment

- 5.9 Others (sterilization and disinfection systems, blowers, dusting, etc.)

Chapter 6 Market Estimates & Forecast, By Usage, 2021 - 2034, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Recycling feathers

- 6.3 Virgin feathers

Chapter 7 Market Estimates & Forecast, By Capacity, 2021 - 2034, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Upto 500 kg/hr

- 7.3 500-2,500 kg/hr

- 7.4 Above 2.500 kg/hr

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Poultry

- 8.3 Chicken

- 8.4 Goose

- 8.5 Duck

- 8.6 Others

- 8.7 Peacock

- 8.8 Others (ostrich, etc.)

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021 - 2034, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Poultry processing plants

- 9.3 Poultry rearing

- 9.4 Slaughtering

- 9.5 Down & feather

- 9.6 Clothing

- 9.7 Bedding products

- 9.8 Feather meal producers

- 9.9 Arts & crafts

- 9.10 Others (fertilizer, construction insulation, filtration system, etc.)

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.4.6 Indonesia

- 11.4.7 Malaysia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Baader Group

- 12.2 Banss

- 12.3 Bayle

- 12.4 Bettcher Industries

- 12.5 Cantrell-Gainco

- 12.6 Hubbard Systems

- 12.7 Kuiper & Zonen

- 12.8 LINCO

- 12.9 MAJA

- 12.10 Meyn

- 12.11 Ruvii

- 12.12 Scott Automation

- 12.13 Stork (Marel)

- 12.14 TALSA

- 12.15 Taizy Machinery

非接触式三维表面轮廓仪市场:按技术、产品类型、解析度、终端用户产业和应用划分-全球预测,2026-2032年表面轮廓测量仪器市场(按仪器类型、测量技术、应用和最终用户产业划分)-全球预测,2026-2032年艺术装裱软体市场:按部署模式、定价模式、组织规模、最终用户和应用领域划分-全球预测,2026-2032年

非接触式三维表面轮廓仪市场:按技术、产品类型、解析度、终端用户产业和应用划分-全球预测,2026-2032年表面轮廓测量仪器市场(按仪器类型、测量技术、应用和最终用户产业划分)-全球预测,2026-2032年艺术装裱软体市场:按部署模式、定价模式、组织规模、最终用户和应用领域划分-全球预测,2026-2032年 2025-2030年全球轮廓仪市场

2025-2030年全球轮廓仪市场 硅胶轮廓仪市场规模、份额和成长分析:按类型、应用、最终用途、分销管道和地区划分-2026-2033年产业预测

硅胶轮廓仪市场规模、份额和成长分析:按类型、应用、最终用途、分销管道和地区划分-2026-2033年产业预测 2026年全球表面测量仪器市场报告按产品类型、部署方式、应用和最终用户分類的壳体深度测量仪市场,全球预测,2026-2032年照片相框製作软体市场:依软体类型、定价模式、整合功能、特性、部署模式和最终用户划分-2026-2032年全球预测

2026年全球表面测量仪器市场报告按产品类型、部署方式、应用和最终用户分類的壳体深度测量仪市场,全球预测,2026-2032年照片相框製作软体市场:依软体类型、定价模式、整合功能、特性、部署模式和最终用户划分-2026-2032年全球预测 声学多普勒流速剖面仪(ADCP)-全球市场份额和排名、总收入和需求预测(2025-2031年)

声学多普勒流速剖面仪(ADCP)-全球市场份额和排名、总收入和需求预测(2025-2031年) 全球测量和布局工具市场

全球测量和布局工具市场