|

市场调查报告书

商品编码

1844307

胃肠道间质瘤治疗市场机会、成长动力、产业趋势分析及2025-2034年预测Gastrointestinal Stromal Tumor Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

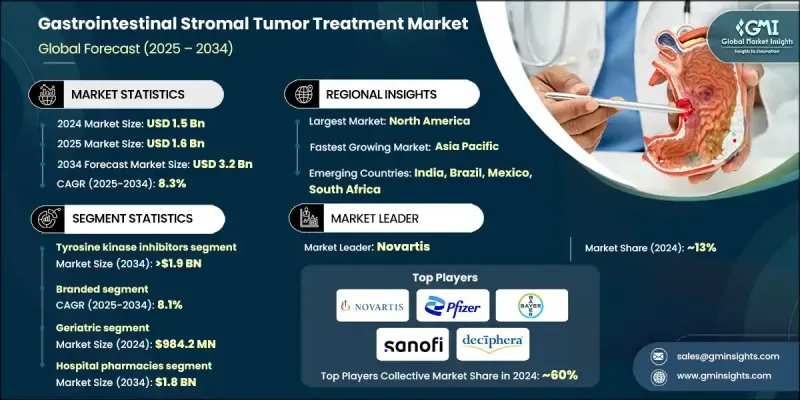

2024 年全球胃肠道间质瘤治疗市场价值为 15 亿美元,预计到 2034 年将以 8.3% 的复合年增长率增长至 32 亿美元。

这一增长可归因于全球胃肠道癌症盛行率的上升以及人们对罕见肿瘤类型认识的提高。标靶治疗,尤其是酪胺酸激酶抑制剂 (TKI) 的进展,正在显着改善治疗效果和存活率。转移性和难治性胃肠道间质瘤 (GIST) 病例的发病率不断上升,进一步刺激了对瑞普替尼、阿伐普替尼和瑞戈非尼等创新药物的需求,这些药物用于控制病情进展并改善患者在各个疾病阶段的生活品质。 GIST 的治疗通常为口服给药,可透过医院药局、零售药局和线上平台取得。这些疗法包括酪胺酸激酶抑制剂、多激酶抑制剂和联合疗法等类别,都是针对原发性肿瘤和转移性肿瘤。众多全球製药公司占据市场,它们持续大力投资研发,从而推动了新疗法的批准和治疗适应症的扩展。精准肿瘤学和突变特异性治疗的引入正在重塑市场,针对特定基因突变量身定制的药物表现出更高的疗效和更少的副作用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 15亿美元 |

| 预测值 | 32亿美元 |

| 复合年增长率 | 8.3% |

2024年,酪胺酸激酶抑制剂在胃肠道间质瘤(GIST)治疗市场中占62.3%的份额,这得益于其标靶作用和经过验证的临床疗效。随着个人化医疗的日益普及,酪胺酸激酶抑制剂的需求激增。美国国立卫生研究院 (NIH) 的研究指出,这些药物,尤其是伊马替尼,被认为是转移性GIST的标准一线治疗药物,并因其高效性而持续受到青睐。

到2034年,品牌药物市场的复合年增长率将达到8.1%。品牌疗法因其临床成功、FDA批准以及全球治疗指南的持续收录而备受青睐。这些疗法针对的是KIT和PDGFRA等胃肠道间质瘤(GIST)患者常见的特定基因突变。持续的研发投入正在推动下一代酪胺酸激酶抑制剂(TKI)和联合疗法的研发,旨在克服抗药性并改善治疗效果。

2024年,美国胃肠道间质瘤治疗市场规模达5.618亿美元,市场需求庞大。随着影像诊断和分子检测技术的进步,美国越来越多的胃肠道间质瘤病例被准确诊断,寻求治疗的患者数量也随之增加。此外,FDA的扶持性法规和报销政策也促进了品牌药和仿製药的审批和应用,进一步拓展了市场机会。

胃肠道间质瘤治疗市场的主要参与者包括拜耳、辉瑞、武田製药、罗氏、诺华、太阳製药、Shorla Oncology、Glenmark、AngioDynamics、Argon Medical Products、Natco Pharma 和 Deciphera Pharma。为了巩固其在胃肠道间质瘤治疗市场中的地位,各公司正专注于几个关键策略。这包括大力投资研发 (R&D),将创新疗法推向市场并扩展现有产品线。许多公司正在优先开发下一代酪胺酸激酶抑制剂和联合疗法,特别是那些针对抗药性机制的疗法。此外,公司正在透过与研究机构和其他製药公司建立策略合作伙伴关係来加速药物开发和拓宽分销网络,从而加强其市场立足点。透过长期临床试验资料、FDA 批准和融入全球治疗指南来增强品牌权益也是一个关键的重点。最后,各公司正在扩大其地理覆盖范围,增加新兴市场的治疗机会,而这些市场的胃肠道间质瘤发病率正在上升,从而最大限度地发挥成长潜力。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 胃肠道间质瘤盛行率不断上升

- 年龄增加和遗传倾向

- 标靶治疗的突破

- 对復发和抗药性的认识不断提高

- 产业陷阱与挑战

- 不良反应和治疗抵抗

- 低收入地区的交通受限

- 市场机会

- 突变特异性和联合疗法的开发

- 基因组检测与个人化医疗的扩展

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 未来市场趋势

- 技术格局

- 现有技术

- 新兴技术

- 管道分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按药物类型,2021 - 2034 年

- 主要趋势

- 多激酶抑制剂

- 酪胺酸激酶抑制剂

- VEGF抑制剂

第六章:市场估计与预测:按类型,2021 - 2034

- 主要趋势

- 品牌

- 泛型

第七章:市场估计与预测:按年龄组,2021 - 2034 年

- 主要趋势

- 成年人

- 老年

第 8 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 网路药局

第九章:市场估计与预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Bayer

- Deciphera Pharmaceuticals

- F. Hoffmann-La Roche

- Glenmark

- Natco Pharma

- Novartis

- Pfizer

- Sanofi

- Shorla Oncology

- Sun Pharmaceuticals

- Takeda Pharmaceuticals

The Global Gastrointestinal Stromal Tumor Treatment Market was valued at USD 1.5 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 3.2 billion by 2034.

This growth can be attributed to the increasing global prevalence of gastrointestinal cancers and heightened awareness of rare tumor types. Advancements in targeted therapies, particularly tyrosine kinase inhibitors (TKIs), are improving treatment outcomes and survival rates significantly. The rising incidence of metastatic and treatment-resistant GIST cases has further fueled demand for innovative drugs like ripretinib, avapritinib, and regorafenib, which are used to manage disease progression and enhance patient quality of life at various stages of the condition. Treatments for GIST are typically administered orally and are available through hospital pharmacies, retail pharmacies, and online platforms. These therapies include categories such as tyrosine kinase inhibitors, multikinase inhibitors, and combination treatments, all aimed at both primary and metastatic tumors. The market is populated by numerous global pharmaceutical companies that continue to invest heavily in research and development, resulting in the approval of new therapies and expanded treatment indications. The introduction of precision oncology and mutation-specific treatments is reshaping the market, with drugs tailored to specific genetic mutations demonstrating higher efficacy and fewer side effects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.5 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 8.3% |

In 2024, the tyrosine kinase inhibitors segment held a share of 62.3% in the GIST treatment market, driven by their targeted action and proven clinical effectiveness. As personalized medicine becomes more prevalent, the demand for tyrosine kinase inhibitors has surged. These drugs, particularly imatinib, are considered the standard first-line treatment for metastatic GIST and continue to be preferred due to their high efficacy, as noted by research from the National Institutes of Health (NIH).

The branded drug segment will grow at a CAGR of 8.1% through 2034. Branded therapies are favored due to their demonstrated clinical success, FDA approvals, and consistent inclusion in global treatment guidelines. These treatments target specific genetic mutations like KIT and PDGFRA, which are commonly found in GIST patients. Ongoing investments in research and development are driving the creation of next-generation tyrosine kinase inhibitors (TKIs) and combination therapies designed to overcome drug resistance and improve treatment outcomes.

United States Gastrointestinal Stromal Tumor Treatment Market was valued at USD 561.8 million in 2024, reflecting significant demand. With the advancement of diagnostic imaging and molecular testing, more GIST cases are being accurately detected in the U.S., leading to an increased number of patients seeking treatment. Additionally, supportive FDA regulations and reimbursement policies are facilitating the approval and adoption of both branded and generic treatments, further expanding market opportunities.

Major players in the Gastrointestinal Stromal Tumor Treatment Market include Bayer, Pfizer, Takeda Pharmaceuticals, F. Hoffmann-La Roche, Novartis, Sun Pharma, Shorla Oncology, Glenmark, AngioDynamics, Argon Medical Products, Natco Pharma, and Deciphera Pharma. To strengthen their position in the gastrointestinal stromal tumor treatment market, companies are focusing on several key strategies. This includes heavy investment in research and development (R&D) to bring innovative treatments to market and expand existing product lines. Many companies are prioritizing the development of next-generation tyrosine kinase inhibitors and combination therapies, particularly those targeting resistance mechanisms. Additionally, companies are enhancing their market foothold by forming strategic partnerships with research institutions and other pharmaceutical companies to accelerate drug development and broaden distribution networks. Strengthening brand equity through long-term clinical trial data, FDA approvals, and integration into global treatment guidelines is also a critical focus. Finally, companies are expanding their geographical reach and increasing access to treatments in emerging markets, where the incidence of GIST is rising, thereby maximizing growth potential.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Drug type trends

- 2.2.3 Type trends

- 2.2.4 Age group trends

- 2.2.5 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence gastrointestinal stromal tumors

- 3.2.1.2 Advancing age and genetic predisposition

- 3.2.1.3 Breakthroughs in targeted therapy

- 3.2.1.4 Growing awareness of recurrence and resistance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Adverse effects and resistance to therapy

- 3.2.2.2 Limited access in low-income regions

- 3.2.3 Market opportunities

- 3.2.3.1 Development of mutation-specific and combination therapies

- 3.2.3.2 Expansion of genomic testing and personalized medicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Future market trends

- 3.6 Technological landscape

- 3.6.1 Current technologies

- 3.6.2 Emerging technologies

- 3.7 Pipeline analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Multikinase inhibitors

- 5.3 Tyrosine kinase inhibitors

- 5.4 VEGF inhibitors

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Branded

- 6.3 Generics

Chapter 7 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Adults

- 7.3 Geriatric

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacies

- 8.3 Retail pharmacies

- 8.4 Online pharmacies

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Bayer

- 10.2 Deciphera Pharmaceuticals

- 10.3 F. Hoffmann-La Roche

- 10.4 Glenmark

- 10.5 Natco Pharma

- 10.6 Novartis

- 10.7 Pfizer

- 10.8 Sanofi

- 10.9 Shorla Oncology

- 10.10 Sun Pharmaceuticals

- 10.11 Takeda Pharmaceuticals

胃癌药物市场:依治疗方法、应用、通路和地区划分

胃癌药物市场:依治疗方法、应用、通路和地区划分 胃癌药物市场规模、份额和成长分析(按治疗方法、疾病、药物类别和地区划分)—产业预测(2026-2033 年)

胃癌药物市场规模、份额和成长分析(按治疗方法、疾病、药物类别和地区划分)—产业预测(2026-2033 年) 胃癌市场

胃癌市场 胃癌治疗市场-全球产业规模、份额、趋势、机会和预测,按治疗类型、按癌症类型、按给药途径、按药物类别、按配销通路、按地区和竞争进行细分,2020 年至 2030 年

胃癌治疗市场-全球产业规模、份额、趋势、机会和预测,按治疗类型、按癌症类型、按给药途径、按药物类别、按配销通路、按地区和竞争进行细分,2020 年至 2030 年 印度的胃癌治疗市场:各治疗类型,各类型,各类药物,各给药途径,各流通管道,各地区,机会,预测,2019年~2033年胃癌治疗市场-全球产业规模、份额、趋势、机会及预测,依治疗类型、最终用户、地区及竞争情况细分,2020-2030 年预测

印度的胃癌治疗市场:各治疗类型,各类型,各类药物,各给药途径,各流通管道,各地区,机会,预测,2019年~2033年胃癌治疗市场-全球产业规模、份额、趋势、机会及预测,依治疗类型、最终用户、地区及竞争情况细分,2020-2030 年预测 2025-2033年依类型(盐酸多柔比星、舒尼替尼、多西他赛、丝裂霉素、氟尿嘧啶、伊马替尼、曲妥珠单抗)、给药途径(口服、肠胃外)、最终用户(医院、诊所等)和地区的胃癌药物市场报告胃癌治疗药市场评估:治疗类型·类型·药物类别·给药途径·流通管道·各地区的机会及预测 (2018-2032年)

2025-2033年依类型(盐酸多柔比星、舒尼替尼、多西他赛、丝裂霉素、氟尿嘧啶、伊马替尼、曲妥珠单抗)、给药途径(口服、肠胃外)、最终用户(医院、诊所等)和地区的胃癌药物市场报告胃癌治疗药市场评估:治疗类型·类型·药物类别·给药途径·流通管道·各地区的机会及预测 (2018-2032年) 胃癌治疗市场规模、份额、趋势分析报告:依治疗类型、疾病适应症、给药途径、药物类别、地区、细分市场预测,2025-2030年

胃癌治疗市场规模、份额、趋势分析报告:依治疗类型、疾病适应症、给药途径、药物类别、地区、细分市场预测,2025-2030年 胃癌治疗市场、机会、成长动力、产业趋势分析与预测,2024-2032

胃癌治疗市场、机会、成长动力、产业趋势分析与预测,2024-2032