|

市场调查报告书

商品编码

1844318

尼古丁替代疗法市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Nicotine Replacement Therapy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

2024 年全球尼古丁替代疗法市场价值为 33 亿美元,预计到 2034 年将以 8.3% 的复合年增长率增长至 72 亿美元。

这项成长的驱动力来自于全球吸烟率的上升、政府监管力度的加强、控烟措施的推进以及尼古丁替代疗法(NRT)产品的技术进步。行动应用程式、远距医疗和人工智慧平台等数位健康工具的整合,使得即时监测烟瘾和戒断症状成为可能。这些创新有助于提高治疗依从性,并允许医疗保健提供者远端客製化治疗方案,这在农村地区尤其重要。此类技术的日益普及正在进一步加速市场发展。尼古丁替代疗法解决了吸烟者在戒烟过程中面临的挑战,因为突然戒烟通常会导致强烈的烟瘾和戒断症状。公共卫生运动、税收政策和禁烟令也推动了对NRT产品的需求。此外,具有反馈系统的蓝牙吸入器、速溶口腔膜、合成尼古丁配方以及人工智慧驱动的戒烟应用程式等新设备正在透过提高生物利用度、用户参与度和治疗效果来彻底改变市场。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 33亿美元 |

| 预测值 | 72亿美元 |

| 复合年增长率 | 8.3% |

口香糖市场占了49.6%的市场份额,预计到2034年将达到35亿美元,复合年增长率为8.2%。尼古丁口香糖仍然是控制戒断症状的可靠且便捷的选择,因此深受注重健康的消费者的青睐。随着吸烟日益被视为一种慢性成瘾,对尼古丁口香糖等长期戒烟辅助产品的需求持续成长。医疗保健专业人士经常推荐将尼古丁口香糖作为全面戒烟计画的一部分,因为它吸收迅速,能够有效缓解戒断症状。

2024年,口服电子烟市场规模达24亿美元。这类产品包括含片、口香糖和可溶解薄膜,它们为控制尼古丁渴望提供了隐藏便捷的解决方案。其便携性和非侵入性使其在工作场所和社交场所等公共场所尤其受欢迎。这些产品的便利性提高了使用者的依从性,尤其受到那些偏好精细、按需选择的年轻城市消费者的青睐。

2024年,北美尼古丁替代疗法市场占48.3%的市占率。该地区知识渊博的民众高度重视吸烟带来的健康危害,包括癌症、心臟病和呼吸系统疾病。持续的公共卫生工作、教育计画和媒体通报显着影响了消费者行为,推动了对NRT等更安全戒烟方法的需求。北美烟草相关疾病的高负担加剧了对有效戒烟解决方案的需求。此外,严格的政府政策,包括广告限制、提高烟草税和公共场所禁烟,也支持了市场的成长。

活跃于全球尼古丁替代疗法市场的关键产业参与者包括 Glenmark、强生、西普拉、Fertin Pharma、雷迪博士实验室、辉瑞、Rubicon Research、Sparsh Pharma、Niconovum、皮尔法伯集团、Perrigo Company、Rusan Pharma 和葛兰素史克。为了巩固其地位,尼古丁替代疗法市场的公司正专注于创新,开发具有更高功效、更佳用户体验和更快缓解症状的下一代产品。许多公司正在投资数位健康集成,例如行动应用程式和人工智慧工具,以提供个人化治疗和远端监控,从而提高患者的依从性。与医疗保健提供者和药局的策略合作有助于拓宽分销管道。行销工作强调安全性和便利性,以吸引更广泛的受众,包括年轻用户和农村人口。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 全球癌症病例不断增加

- 加强戒烟倡议

- 提高健康意识和教育

- 扩大NRT产品的非处方药(OTC)管道

- 产业陷阱与挑战

- 相关副作用

- 严格的监管和限制

- 市场机会

- 与数位健康平台整合

- 全球老年人口不断成长

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 我们

- 加拿大

- 欧洲

- 亚太地区

- 北美洲

- 技术格局

- 当前的技术趋势

- 新兴技术

- 未来市场趋势

- 定价分析

- 临床试验分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 全球的

- 北美洲

- 欧洲

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021 - 2034 年

- 主要趋势

- 牙龈

- 锭剂

- 透皮贴剂

- 吸入器

- 鼻喷剂

- 舌下片

第六章:市场估计与预测:按管理路线,2021 - 2034 年

- 主要趋势

- 口服

- 透皮

- 鼻腔

第七章:市场估计与预测:按模式,2021 - 2034

- 主要趋势

- 场外交易(OTC)

- 处方

第八章:市场估计与预测:按年龄组,2021 - 2034 年

- 主要趋势

- 18-34

- 35-54

- 55岁以上

第九章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 线下通路

- 医院药房

- 零售药局

- 其他线下分销通路

- 线上通路

第 10 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Cipla

- Dr. Reddy's Laboratories

- Fertin Pharma

- Glenmark

- GlaxoSmithKline

- Johnson & Johnson

- Niconovum

- Pfizer

- Rubicon Research

- Rusan Pharma

- Sparsh Pharma

- Perrigo Company

- Pierre Fabre Group

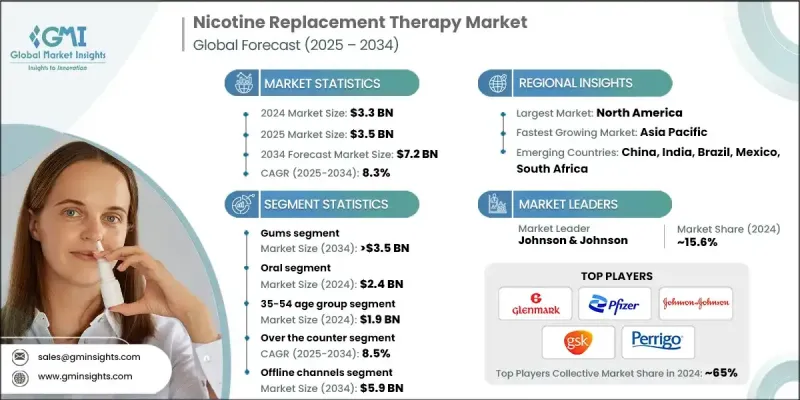

The Global Nicotine Replacement Therapy Market was valued at USD 3.3 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 7.2 billion by 2034.

The growth is driven by the increasing prevalence of smoking worldwide, stronger government regulations, tobacco control initiatives, and technological advancements in NRT products. The integration of digital health tools, including mobile applications, telemedicine, and AI-powered platforms, is enabling real-time monitoring of cravings and withdrawal symptoms. These innovations help improve treatment adherence and allow healthcare providers to tailor plans remotely, which is especially valuable in rural regions. The growing adoption of such technologies is further accelerating the market. Nicotine replacement therapy addresses the challenges smokers face when quitting, as abrupt cessation often causes intense cravings and withdrawal symptoms. Public health campaigns, taxation policies, and smoking bans are also propelling demand for NRT products. Additionally, new devices such as Bluetooth-enabled inhalers with feedback systems, fast-dissolving oral films, synthetic nicotine formulations, and AI-driven cessation apps are revolutionizing the market by enhancing bioavailability, user engagement, and treatment outcomes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.3 Billion |

| Forecast Value | $7.2 Billion |

| CAGR | 8.3% |

The gum segment held 49.6% share, and is anticipated to reach USD 3.5 billion by 2034, growing at an 8.2% CAGR. Nicotine gum remains a trusted and accessible option for managing withdrawal symptoms, making it highly favored by health-conscious consumers. As smoking is increasingly recognized as a chronic addiction, demand for long-term cessation aids like nicotine gum continues to rise. Healthcare professionals frequently recommend nicotine gum as part of comprehensive quitting plans due to its rapid absorption and effectiveness in easing withdrawal.

The oral segment generated USD 2.4 billion in 2024. This category includes lozenges, gums, and dissolvable films, which offer discreet and convenient solutions to control nicotine cravings. Their portability and non-invasive nature make them especially popular in public spaces such as workplaces and social environments. The convenience of these products enhances user compliance, particularly among younger and urban consumers who prefer subtle, on-demand options.

North America Nicotine Replacement Therapy Market held a 48.3% share in 2024. The region's well-informed population is highly aware of the health dangers related to smoking, including cancer, heart disease, and respiratory issues. Ongoing public health efforts, educational programs, and media coverage have significantly influenced consumer behavior, driving demand for safer quitting methods like NRT. The high burden of tobacco-related diseases in North America strengthens the need for effective cessation solutions. Additionally, strict government policies, including advertising restrictions, elevated tobacco taxes, and public smoking bans, support market growth.

Key industry players active in the Global Nicotine Replacement Therapy Market include Glenmark, Johnson & Johnson, Cipla, Fertin Pharma, Dr. Reddy's Laboratories, Pfizer, Rubicon Research, Sparsh Pharma, Niconovum, Pierre Fabre Group, Perrigo Company, Rusan Pharma, and GlaxoSmithKline. To fortify their presence, companies in the Nicotine Replacement Therapy Market are focusing on innovation by developing next-generation products that offer enhanced efficacy, improved user experience, and faster relief. Many are investing in digital health integrations such as mobile apps and AI tools to provide personalized treatment and remote monitoring, increasing patient adherence. Strategic collaborations with healthcare providers and pharmacies help broaden distribution channels. Marketing efforts highlight safety and convenience to appeal to a wider audience, including younger users and rural populations.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Route of administration trends

- 2.2.4 Mode trends

- 2.2.5 Age group trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing cases of cancer globally

- 3.2.1.2 Increasing smoking cessation initiatives

- 3.2.1.3 Rising health awareness and education

- 3.2.1.4 Expansion of over the counter (OTC) access of NRT products

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Associated side-effects

- 3.2.2.2 Stringent regulation and restrictions

- 3.2.3 Market opportunities

- 3.2.3.1 Integration with digital health platforms

- 3.2.3.2 Growing global aging population

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.1 North America

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Pricing analysis

- 3.8 Clinical trial analysis

- 3.9 Porter’s analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 Global

- 4.2.2 North America

- 4.2.3 Europe

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Gums

- 5.3 Lozenges

- 5.4 Transdermal patches

- 5.5 Inhaler

- 5.6 Nasal spray

- 5.7 Sublingual tablets

Chapter 6 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Oral

- 6.3 Transdermal

- 6.4 Nasal

Chapter 7 Market Estimates and Forecast, By Mode, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Over the counter (OTC)

- 7.3 Prescription

Chapter 8 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 18-34

- 8.3 35-54

- 8.4 55+

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Offline channels

- 9.2.1 Hospital pharmacies

- 9.2.2 Retail pharmacies

- 9.2.3 Other offline distribution channels

- 9.3 Online channels

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Cipla

- 11.2 Dr. Reddy’s Laboratories

- 11.3 Fertin Pharma

- 11.4 Glenmark

- 11.5 GlaxoSmithKline

- 11.6 Johnson & Johnson

- 11.7 Niconovum

- 11.8 Pfizer

- 11.9 Rubicon Research

- 11.10 Rusan Pharma

- 11.11 Sparsh Pharma

- 11.12 Perrigo Company

- 11.13 Pierre Fabre Group

尼古丁替代疗法市场分析及预测(至2035年):按类型、产品类型、应用、最终用户、形式、技术、组件、设备和解决方案划分

尼古丁替代疗法市场分析及预测(至2035年):按类型、产品类型、应用、最终用户、形式、技术、组件、设备和解决方案划分 全球尼古丁替代疗法市场规模、份额、趋势和成长分析报告(2026-2034年)

全球尼古丁替代疗法市场规模、份额、趋势和成长分析报告(2026-2034年) 尼古丁市场按产品类型、应用、分销管道和最终用户划分 - 全球预测 2026-2032尼古丁袋市场:按产品类型、口味、尼古丁浓度、包装类型、价格范围和分销管道分類的全球预测,2026-2032年尼古丁替代疗法市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2025-2034)

尼古丁市场按产品类型、应用、分销管道和最终用户划分 - 全球预测 2026-2032尼古丁袋市场:按产品类型、口味、尼古丁浓度、包装类型、价格范围和分销管道分類的全球预测,2026-2032年尼古丁替代疗法市场规模、占有率、成长及全球产业分析:按类型、应用和地区划分的洞察与预测(2025-2034) 纯尼古丁:全球市场份额和排名、总收入和需求预测(2025-2031 年)

纯尼古丁:全球市场份额和排名、总收入和需求预测(2025-2031 年) 全球尼古丁替代疗法市场按产品类型、分销管道和地区划分

全球尼古丁替代疗法市场按产品类型、分销管道和地区划分 尼古丁替代疗法市场 - 全球产业规模、份额、趋势、机会与预测,按产品、配销通路、地区和竞争细分,2020-2030 年

尼古丁替代疗法市场 - 全球产业规模、份额、趋势、机会与预测,按产品、配销通路、地区和竞争细分,2020-2030 年