|

市场调查报告书

商品编码

1844322

外墙系统市场机会、成长动力、产业趋势分析及2025-2034年预测Exterior Wall System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

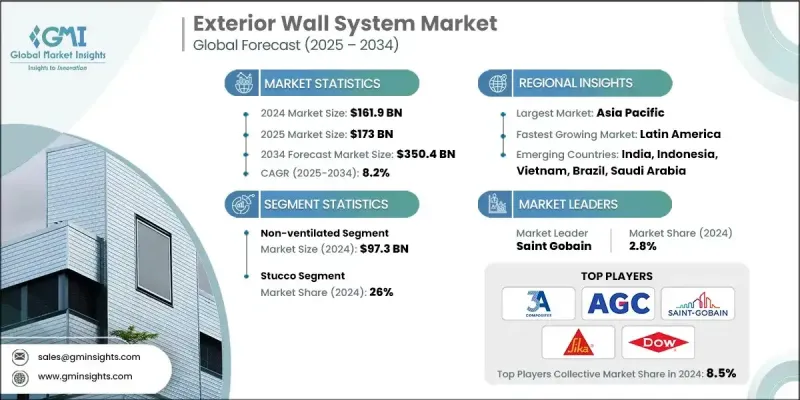

2024 年全球外墙系统市场价值为 1,619 亿美元,预计到 2034 年将以 8.2% 的复合年增长率成长至 3,504 亿美元。

这一增长的动力源于对永续建筑解决方案、节能建筑规范和模组化建筑技术日益增长的需求。对环保材料和建筑实践的日益重视正在重塑整个行业的采购决策。开发商和承包商现在优先考虑符合绿建筑认证并符合范围三排放目标的墙体系统。因此,市场正在见证保温一体化、防火和智慧材料技术的快速创新。都市化进程的加速和劳动力短缺也导致预製墙体系统的采用率不断提高,这提高了安装速度,确保了更好的品质控制,并缩短了施工时间。製造商正专注于配备隔热层、覆层和防潮层的预製面板,以满足日益增长的性能和便利性需求。此外,外墙系统也不断发展,包括相变材料、耐热涂层和智慧隔热层等节能特性。这些进步有助于创造更能源韧性的建筑环境,尤其是在北美、中东和亚洲部分地区等基础设施投资庞大的地区。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1619亿美元 |

| 预测值 | 3504亿美元 |

| 复合年增长率 | 8.2% |

2024年,不通风外墙市场规模达973亿美元,预计2034年将以7.3%的复合年增长率成长。不通风系统的普及主要归功于其较低的前期成本和较低的安装复杂性。这类墙体系统所需的组件更少,且外形更纤薄,是空间受限的城市开发项目的理想选择。其简化的设计也适用于外墙施工技术熟练劳动力资源有限的地区。因此,寻求经济高效墙体解决方案的开发商在商业和住宅应用中继续青睐不通风系统。

2024年,灰泥市场规模达421亿美元,占26%。其吸引力在于其耐用性、成本效益和多功能性。灰泥可提供持久保护,维护成本极低,并可应用于各种纹理、饰面和颜色,使建筑师能够灵活地实现各种设计目标。灰泥还可作为天然隔热材料,有助于降低能耗并增强声学性能。灰泥能够有效地黏附在混凝土、砖石和木材等各种结构材料上,使其成为各种气候条件的理想选择,尤其适合干燥或温和的气候条件。

2024年,美国外墙系统市场规模达403亿美元,预计2025年至2034年期间的复合年增长率将达到7.1%。住宅、商业和政府建筑的持续扩张推动了这一成长。城市发展、外商投资以及对节能建筑的需求不断增长是推动美国市场份额成长的关键因素。因此,旨在降低暖通空调负荷的系统正日益受到青睐,而整合隔热功能的墙体解决方案正成为建筑业的首选。

活跃于全球外墙系统市场的关键公司包括 JamesHardie、USG Corporation、Fletcher Buildings、旭硝子 (AGC)、欧文斯科宁、3A Composites Holding AG、CSR Limited、圣戈班、东丽工业有限公司、Boral Limited、SIKA Group、Kronospan Limited、拉法基豪瑞、日本玻璃板和陶氏公司。外墙系统市场的公司正在利用创新、地理扩张和永续性等多种方式来巩固其市场地位。领先的公司正在投资研发,以开发具有整合隔热、蒸汽控制和防火功能的模组化节能墙体系统。许多公司还引入了轻型预製解决方案,以减少现场劳动力、优化安装速度并满足城市环境的需求。策略性併购正在帮助扩大产品组合併进入新兴市场。公司正在使产品与绿色建筑认证和低碳材料标准保持一致,以满足不断变化的监管规范和具有永续发展意识的消费者的需求。

目录

第一章:方法论与范围

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业影响力量

- 成长动力

- 产业陷阱与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区和类型

- 监理框架

- 标准和认证

- 环境法规

- 进出口法规

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 - 2034

- 主要趋势

- 通风

- 不通风

第六章:市场估计与预测:依资料,2021 - 2034 年

- 主要趋势

- 乙烯基塑料

- 纤维水泥

- 灰泥

- 石工

- 木头

- 其他的

第七章:市场估计与预测:按应用,2021 - 2034

- 主要趋势

- 住宅

- 商业的

- 工业的

第 8 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 直销

- 间接销售

第九章:市场估计与预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 阿联酋

- 沙乌地阿拉伯

- 南非

第十章:公司简介

- 3A Composites Holding AG

- Asahi Glass (AGC)

- Boral Limited

- CSR Limited

- Fletcher Buildings

- JamesHardie

- Lafargeholcim

- Kronospan Limited

- Nippon Glass Sheet

- Owens Corning

- Saint Gobain

- SIKA Group

- The Dow Company

- Toray Industries Ltd.

- USG Corporation

The Global Exterior Wall System Market was valued at USD 161.9 billion in 2024 and is estimated to grow at a CAGR of 8.2% to reach USD 350.4 billion by 2034.

The growth is fueled by rising demand for sustainable construction solutions, energy-efficient building codes, and modular construction techniques. A growing emphasis on environmentally responsible materials and building practices is reshaping procurement decisions across the sector. Developers and contractors now prioritize wall systems that meet green building certifications and align with Scope 3 emissions objectives. As a result, the market is witnessing rapid innovation in insulation integration, fire resistance, and smart material technologies. Increasing urbanization and labor shortages have also led to higher adoption of prefabricated wall systems, which enhance installation speed, ensure better quality control, and reduce construction time. Manufacturers are focusing on prefabricated panels equipped with insulation, cladding, and vapor barriers to meet growing demands for performance and convenience. Additionally, exterior wall systems are evolving to include energy-saving features such as phase-change materials, thermal-resistant coatings, and smart insulation layers. These advancements support a more energy-resilient built environment, particularly in regions investing heavily in infrastructure, including North America, the Middle East, and parts of Asia.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $161.9 Billion |

| Forecast Value | $350.4 Billion |

| CAGR | 8.2% |

In 2024, the non-ventilated exterior wall segment generated USD 97.3 billion and is expected to grow at a CAGR of 7.3% through 2034. The popularity of non-ventilated systems is largely attributed to their lower upfront costs and reduced installation complexity. These wall systems require fewer components and offer a thinner profile, which makes them ideal for space-constrained urban developments. Their simplified design also suits regions with a limited skilled labor pool for facade construction. As a result, developers seeking cost-effective yet efficient wall solutions continue to favor non-ventilated systems across commercial and residential applications.

The stucco segment generated USD 42.1 billion in 2024 and held a 26% share. Its appeal lies in its durability, cost-efficiency, and versatility. Stucco offers long-lasting protection with minimal upkeep and can be applied in various textures, finishes, and colors, giving architects the flexibility to meet a wide range of design goals. It also serves as a natural insulator, contributing to reduced energy consumption and enhanced acoustic performance. Stucco adheres effectively to different structural materials like concrete, masonry, and wood, making it ideal for diverse climates, particularly those with dry or temperate conditions.

U.S. Exterior Wall System Market was valued at USD 40.3 billion in 2024 and is estimated to grow at a CAGR of 7.1% between 2025 and 2034. The continued expansion in residential, commercial, and government construction is fueling this growth. Urban development, foreign investments, and rising demand for energy-efficient structures are key contributors to the country's growing market share. In response, systems designed to reduce HVAC loads are gaining traction, with wall solutions offering integrated thermal insulation becoming a preferred choice across building sectors.

Key companies active in the Global Exterior Wall System Market include JamesHardie, USG Corporation, Fletcher Buildings, Asahi Glass (AGC), Owens Corning, 3A Composites Holding AG, CSR Limited, Saint Gobain, Toray Industries Ltd., Boral Limited, SIKA Group, Kronospan Limited, LafargeHolcim, Nippon Glass Sheet, and The Dow Company. Companies in the exterior wall system market are leveraging a mix of innovation, geographic expansion, and sustainability to strengthen their market positions. Leading firms are investing in R&D to develop modular and energy-efficient wall systems with integrated insulation, vapor control, and fire resistance. Many are also introducing lightweight prefabricated solutions to reduce on-site labor, optimize installation speed, and meet demand in urban environments. Strategic mergers and acquisitions are helping expand product portfolios and reach into emerging markets. Firms are aligning offerings with green building certifications and low-carbon material standards to cater to evolving regulatory norms and sustainability-conscious consumers.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Type

- 2.2.2 Material

- 2.2.3 Application

- 2.2.4 Distribution Channel

- 2.2.5 Regional

- 2.3 CXO perspective: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry Impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region and type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Billion) (Thousand Sq ft)

- 5.1 Key trends

- 5.2 Ventilated

- 5.3 Non-ventilated

Chapter 6 Market Estimates & Forecast, By Material, 2021 - 2034 (USD Billion) (Thousand Sq ft)

- 6.1 Key trends

- 6.2 Vinyl

- 6.3 Fiber cement

- 6.4 Stucco

- 6.5 Masonry

- 6.6 Wood

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion) (Thousand Sq ft)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.4 Industrial

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034, (USD Billion) (Thousand Sq ft)

- 8.1 Key trends

- 8.2 Direct Sales

- 8.3 Indirect Sales

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Thousand Sq ft)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 U.K.

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles (Business Overview, Financial Data, Product Landscape, Strategic Outlook, SWOT Analysis)

- 10.1 3A Composites Holding AG

- 10.2 Asahi Glass (AGC)

- 10.3 Boral Limited

- 10.4 CSR Limited

- 10.5 Fletcher Buildings

- 10.6 JamesHardie

- 10.7 Lafargeholcim

- 10.8 Kronospan Limited

- 10.9 Nippon Glass Sheet

- 10.10 Owens Corning

- 10.11 Saint Gobain

- 10.12 SIKA Group

- 10.13 The Dow Company

- 10.14 Toray Industries Ltd.

- 10.15 USG Corporation

外墙系统市场-全球产业规模、份额、趋势、机会及预测(按类型、材料、最终用户、地区和竞争格局划分,2021-2031年)

外墙系统市场-全球产业规模、份额、趋势、机会及预测(按类型、材料、最终用户、地区和竞争格局划分,2021-2031年) 全球外墙系统市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)

全球外墙系统市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034) 绿墙市场规模、份额及成长分析(按类型、介质、应用、最终用户和地区划分)-2026-2033年产业预测

绿墙市场规模、份额及成长分析(按类型、介质、应用、最终用户和地区划分)-2026-2033年产业预测 外墙系统市场规模、份额和成长分析(按材料、产品类型、类别、应用和地区划分)-2026-2033年产业预测

外墙系统市场规模、份额和成长分析(按材料、产品类型、类别、应用和地区划分)-2026-2033年产业预测 砌筑工具及设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

砌筑工具及设备市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 石器工具:全球市场份额和排名、总收入和需求预测(2025-2031 年)

石器工具:全球市场份额和排名、总收入和需求预测(2025-2031 年) 外墙系统市场:按类型、材料类型、应用和施工阶段 - 全球预测 2025-2032

外墙系统市场:按类型、材料类型、应用和施工阶段 - 全球预测 2025-2032 2025年全球绿墙市场报告全球外墙系统市场报告(2025年)

2025年全球绿墙市场报告全球外墙系统市场报告(2025年) 绿墙市场:按类型、安装类型、应用和地区划分

绿墙市场:按类型、安装类型、应用和地区划分