|

市场调查报告书

商品编码

1844355

资料中心安全市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Data Center Security Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

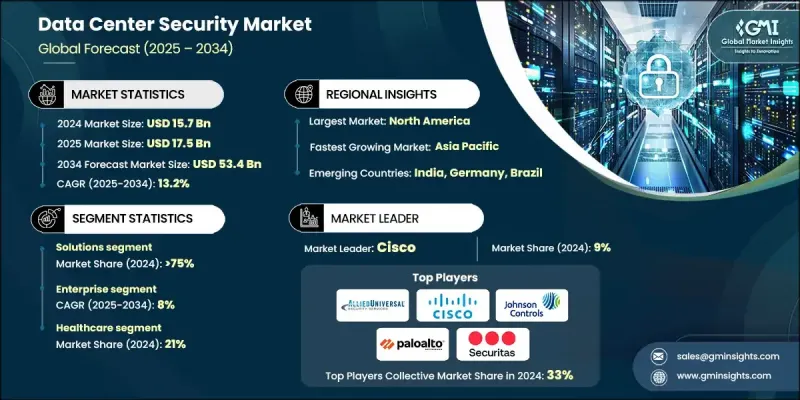

2024 年全球资料中心安全市场价值为 157 亿美元,预计将以 13.2% 的复合年增长率成长,到 2034 年达到 534 亿美元。

随着企业持续储存和管理大量关键资料,强大的资料中心安全(包括实体和网路安全)的重要性日益凸显。如今,全面的保护需要事件回应计划、风险评估、持续监控和多层防御系统之间的无缝协调。由于企业不断面临保护客户资料和维持营运连续性的压力,安全已成为资料中心策略的核心组成部分。遵守 NIST、ISO 等全球标准以及特定地区的法规不仅是必要的,而且是严格执行的,这促使企业将治理和安全管理融入日常营运中。如果忽视这些要求,公司将面临严厉的处罚,甚至可能被关闭。当今的资料中心环境需要的不仅仅是独立的防火墙或摄影机系统;完全统一的安全架构已成为行业规范,包括持续的审计和即时的事件缓解。云端基础设施和人工智慧安全技术的日益普及以及对金融、医疗保健和政府营运等关键领域的监管力度不断加强,进一步推动了市场的成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 157亿美元 |

| 预测值 | 534亿美元 |

| 复合年增长率 | 13.2% |

2024年,解决方案部门占了75%的份额。该部门包括一整套在资料中心设施内协同工作的网路安全和实体安全工具。生物识别门禁、运动感测器、围栏、警报系统和监视摄影机等实体解决方案是防止未经授权的存取和保护边界安全的关键。在网路安全方面,端点侦测和回应 (EDR)、防火墙、入侵侦测和防御系统 (IDS/IPS)、云端原生安全平台以及人工智慧驱动的监控解决方案等技术旨在即时侦测和回应威胁。

2025年至2034年间,企业级资料中心的复合年增长率将达到8%。这些企业营运的资料中心是关键业务营运的支柱。金融、医疗保健和製造等行业的公司管理的内部设施优先考虑将实体安全措施(例如受控存取和监控)与网路安全系统(包括防火墙、异常检测和基础设施监控)相结合。由于保护机密资料和满足合规性要求至关重要,企业持续大力投资整合的端到端安全解决方案。

由于其广泛的数位基础设施,美国资料中心安全市场在2024年创造了47亿美元的收入。北维吉尼亚州等地区的资料中心成长已使该地区成为国家级枢纽。然而,在良好的基础设施和商业环境的推动下,里士满等新兴市场也正在获得发展动力。

积极影响全球资料中心安全市场的关键参与者包括江森自控、霍尼韦尔、Securitas、Genetec、Allied Universal、思科、飞塔、安讯士、派拓网路和亚萨合莱。为了巩固市场地位,资料中心安全领域的公司正专注于结合实体安全和网路安全的整合解决方案。许多公司正在透过人工智慧驱动的威胁检测和即时分析来增强其产品供应。策略性收购和合作伙伴关係也有助于扩大其技术组合和市场准入。参与者正在投资研发,以开发专为混合基础设施量身定制的先进生物识别和云端原生工具。向新兴的二级资料中心市场进行地理扩张是一种常见策略,尤其是在云端运算采用率和数位基础设施项目不断增长的地区。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预报

- 研究假设和局限性

第 2 章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 实体安全基础设施投资不断增加

- 采用综合网路实体安全解决方案

- 云端和混合资料中心扩展

- 法规遵从性(ISO、NIST、GDPR)

- 增加内部威胁缓解倡议

- 产业陷阱与挑战

- 熟练劳动力有限

- 中小企业的预算限制

- 市场机会

- 边缘资料中心的成长

- 託管安全服务的采用

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术成熟度评估框架

- 当前的技术趋势

- 新兴技术

- 成本结构分析

- 专利分析

- 永续性和 ESG 影响评估

- 环境影响分析和指标

- 社会影响考量与指标

- 治理与合规框架

- ESG 投资含义与财务影响

- 用例和应用

- 最佳情况

- 投资报酬率分析和商业案例框架

- 总拥有成本(TCO)分析

- 风险缓解和安全价值量化

- 营运效率和生产力提升

- 商业案例范本和财务模型

- 资料中心建置活动

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 多边环境协定

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

- 创投与私募股权活动

- 基础建设投资模式

第五章:市场估计与预测:依组件划分,2021 - 2034 年

- 主要趋势

- 解决方案

- 实体安全

- 逻辑/网路安全

- 威胁情报

- 资料安全

- 服务

- 託管安全

- 咨询

- 支援与维护

第六章:市场估计与预测:按资料中心,2021 - 2034 年

- 主要趋势

- 超大规模

- 主机託管

- 企业

- 边缘

第七章:市场估计与预测:依最终用途,2021 - 2034

- 主要趋势

- 金融服务业协会

- 卫生保健

- 零售与电子商务

- 媒体与娱乐

- 资讯科技和电信

- 政府和国防

- 其他的

第八章:市场估计与预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧人

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 多边环境协定

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- 全球参与者

- ASSA ABLOY

- Axis Communications

- Check Point Software Technologies

- Cisco

- CrowdStrike

- Fortinet

- Genetec

- Honeywell

- Johnson Controls

- Palo Alto Networks

- Securitas

- Siemens

- Tyco International

- Verint Systems

- Zebra Technologies

- Allied Universal

- 区域参与者

- ADT

- Bosch Security Systems

- Brinks Home Security

- Dahua Technology

- Eaton

- Flir Systems

- Hanwha Techwin

- Hikvision

- LenelS2

- Motorola Solutions

- 新兴参与者/颠覆者

- Armis Security

- Chainguard

- Cynomi

- Endor Labs

- Koi

The Global Data Center Security Market was valued at USD 15.7 billion in 2024 and is estimated to grow at a CAGR of 13.2% to reach USD 53.4 billion by 2034.

As organizations continue to store and manage vast volumes of critical data, the importance of robust data center security, both physical and cyber, has grown significantly. Comprehensive protection now requires seamless coordination between incident response planning, risk assessments, continuous monitoring, and multi-layered defense systems. With businesses under constant pressure to secure customer data and maintain operational continuity, security has become a core component of data center strategy. Compliance with global standards like NIST, ISO, and region-specific regulations is not only necessary but also heavily enforced, pushing organizations to integrate governance and security management in daily operations. Companies face strict penalties and potential shutdowns if these requirements are ignored. Today's data center environments demand more than isolated firewalls or camera systems; a fully unified security architecture has become the industry norm, involving continuous audits and real-time incident mitigation. Market growth is further supported by rising adoption of cloud infrastructure, AI-enabled security technologies, and increasing regulatory oversight across critical sectors, including finance, healthcare, and government operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.7 Billion |

| Forecast Value | $53.4 Billion |

| CAGR | 13.2% |

In 2024, the solutions segment held a 75% share. This segment includes a full suite of cyber and physical security tools working together inside data center facilities. Physical solutions such as biometric access, motion sensors, fencing, alarm systems, and surveillance cameras are key to preventing unauthorized access and securing perimeter boundaries. On the cyber side, technologies like endpoint detection and response (EDR), firewalls, intrusion detection and prevention systems (IDS/IPS), cloud-native security platforms, and AI-driven monitoring solutions are designed to detect and respond to threats in real time.

The enterprises segment will grow at a CAGR of 8% between 2025 and 2034. These enterprise-run data centers serve as the backbone of critical business operations. Internal facilities managed by companies in sectors like finance, healthcare, and manufacturing prioritize a blend of physical safeguards, such as controlled access and surveillance, with cybersecurity systems that include firewalls, anomaly detection, and infrastructure monitoring. With the stakes high for protecting confidential data and meeting compliance mandates, enterprises continue to invest heavily in integrated, end-to-end security solutions.

US Data Center Security Market generated USD 4.7 billion in 2024, owing to its extensive digital infrastructure. Data center growth in areas like North Virginia has established the region as a national hub. However, newer markets such as Richmond are gaining traction as well, driven by favorable infrastructure and business environments.

Key players actively shaping the Global Data Center Security Market include Johnson Controls, Honeywell, Securitas, Genetec, Allied Universal, Cisco, Fortinet, Axis Communications, Palo Alto Networks, and ASSA ABLOY. To strengthen their foothold, companies in the data center security space are focusing on integrated solutions that combine physical and cybersecurity. Many are enhancing their product offerings through AI-driven threat detection and real-time analytics. Strategic acquisitions and partnerships are also helping expand their technology portfolios and market access. Players are investing in R&D to develop advanced biometric and cloud-native tools tailored for hybrid infrastructure. Geographic expansion into emerging secondary data center markets is a common tactic, especially in regions with rising cloud adoption and digital infrastructure projects.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Data center

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising investment in physical security infrastructure

- 3.2.1.2 Adoption of integrated cyber-physical security solutions

- 3.2.1.3 Cloud and hybrid data center expansion

- 3.2.1.4 Regulatory compliance (ISO, NIST, GDPR)

- 3.2.1.5 Increasing insider threat mitigation initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited skilled workforce

- 3.2.2.2 Budget constraints for SMEs

- 3.2.3 Market opportunities

- 3.2.3.1 Edge data centers growth

- 3.2.3.2 Managed security services adoption

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology maturity assessment framework

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost structure analysis

- 3.9 Patent analysis

- 3.10 Sustainability and ESG impact assessment

- 3.10.1 Environmental impact analysis and metrics

- 3.10.2 Social impact considerations and metrics

- 3.10.3 Governance and compliance framework

- 3.10.4 ESG investment implications and financial impact

- 3.11 Use cases and applications

- 3.12 Best-case scenario

- 3.13 ROI analysis and business case framework

- 3.13.1 Total cost of ownership (TCO) analysis

- 3.13.2 Risk mitigation and security value quantification

- 3.13.3 Operational efficiency and productivity gains

- 3.13.4 Business case templates and financial models

- 3.14 Data Center Construction Activity

- 3.14.1 North America

- 3.14.2 Europe

- 3.14.3 Asia Pacific

- 3.14.4 Latin America

- 3.14.5 Middle East & Africa

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Venture capital and private equity activity

- 4.8 Infrastructure investment patterns

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Solutions

- 5.2.1 Physical security

- 5.2.2 Logical/network security

- 5.2.3 Threat intelligence

- 5.2.4 Data security

- 5.3 Services

- 5.3.1 Managed security

- 5.3.2 Consulting

- 5.3.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Data Center, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Hyperscale

- 6.3 Colocation

- 6.4 Enterprise

- 6.5 Edge

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 BFSI

- 7.3 Healthcare

- 7.4 Retail & E-commerce

- 7.5 Media & entertainment

- 7.6 IT & telecommunication

- 7.7 Government & defense

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 US

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Nordics

- 8.3.7 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Global Players

- 9.1.1 ASSA ABLOY

- 9.1.2 Axis Communications

- 9.1.3 Check Point Software Technologies

- 9.1.4 Cisco

- 9.1.5 CrowdStrike

- 9.1.6 Fortinet

- 9.1.7 Genetec

- 9.1.8 Honeywell

- 9.1.9 Johnson Controls

- 9.1.10 Palo Alto Networks

- 9.1.11 Securitas

- 9.1.12 Siemens

- 9.1.13 Tyco International

- 9.1.14 Verint Systems

- 9.1.15 Zebra Technologies

- 9.1.16 Allied Universal

- 9.2 Regional Players

- 9.2.1 ADT

- 9.2.2 Bosch Security Systems

- 9.2.3 Brinks Home Security

- 9.2.4 Dahua Technology

- 9.2.5 Eaton

- 9.2.6 Flir Systems

- 9.2.7 Hanwha Techwin

- 9.2.8 Hikvision

- 9.2.9 LenelS2

- 9.2.10 Motorola Solutions

- 9.3 Emerging Players / Disruptors

- 9.3.1 Armis Security

- 9.3.2 Chainguard

- 9.3.3 Cynomi

- 9.3.4 Endor Labs

- 9.3.5 Koi

资料中心安全市场分析及预测(至 2035 年):类型、产品类型、服务、技术、元件、应用、部署模式、最终使用者、解决方案

资料中心安全市场分析及预测(至 2035 年):类型、产品类型、服务、技术、元件、应用、部署模式、最终使用者、解决方案 2026年全球资料中心安全市场报告

2026年全球资料中心安全市场报告 资料中心机笼市场:按类型、材质、尺寸、冷却系统、最终用户产业、组织规模和部署类型划分 - 全球预测 2026-2032

资料中心机笼市场:按类型、材质、尺寸、冷却系统、最终用户产业、组织规模和部署类型划分 - 全球预测 2026-2032 资料中心安全市场规模、份额和成长分析(按组件、类型、最终用途和地区划分)—2026-2033年产业预测

资料中心安全市场规模、份额和成长分析(按组件、类型、最终用途和地区划分)—2026-2033年产业预测 全球资料中心安全市场:市场规模、份额、趋势分析(按组件、类型和最终用途)、区域展望和未来预测(2024-2031 年)

全球资料中心安全市场:市场规模、份额、趋势分析(按组件、类型和最终用途)、区域展望和未来预测(2024-2031 年) 资料中心安全市场规模、份额、趋势分析报告:按组件、按类型、按最终用途、按地区、细分市场预测,2025-2030 年

资料中心安全市场规模、份额、趋势分析报告:按组件、按类型、按最终用途、按地区、细分市场预测,2025-2030 年 资料中心不断电系统(UPS) 市场报告:2030 年趋势、预测与竞争分析

资料中心不断电系统(UPS) 市场报告:2030 年趋势、预测与竞争分析 资料中心安全市场 - 2024 年至 2029 年预测

资料中心安全市场 - 2024 年至 2029 年预测