|

市场调查报告书

商品编码

1858818

非公路设备传动零件市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Off-Highway Equipment Transmission Component Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

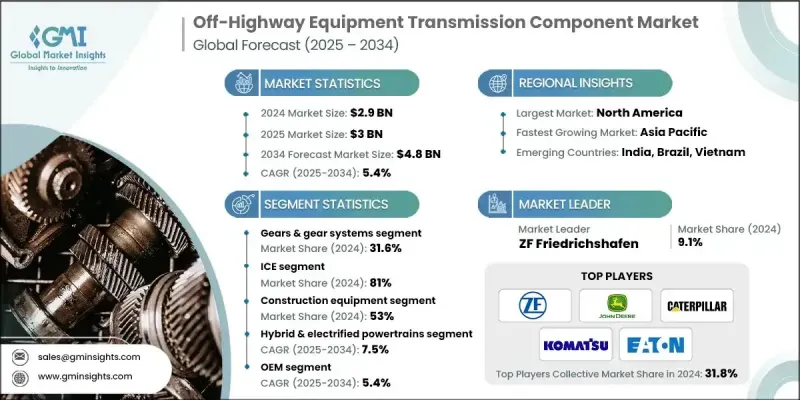

2024 年全球非公路设备变速箱零件市场价值为 29 亿美元,预计到 2034 年将以 5.4% 的复合年增长率增长至 48 亿美元。

市场成长主要受基础设施项目投资增加的推动,包括道路、桥樑和住宅开发项目。这些项目需要配备耐用传动系统的工程机械,以便长时间承受重载。快速的都市化进程,尤其是在亚洲和非洲,也带动了非公路机械的需求成长。此外,农业部门,尤其是在发展中国家,正在积极推动机械化,先进的传动系统在拖拉机、收割机和喷药机中越来越普及。这些系统,例如静液压传动和电液传动,因其高效、精准和易于操作而日益受到青睐。同样,随着对矿产和化石燃料需求的持续高涨,采矿业也持续成长,这使得重型机械更加依赖可靠的传动系统。儘管采矿设备的电气化是一个日益增长的趋势,但柴油动力机械仍然需要耐用的传动系统才能在严苛的环境中有效运作。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 29亿美元 |

| 预测值 | 48亿美元 |

| 复合年增长率 | 5.4% |

2024年,齿轮及齿轮系统细分市场占据31.6%的市场份额,预计到2034年将以6.1%的复合年增长率成长。此细分市场受惠于行星齿轮组的日益普及,行星齿轮组结构紧凑、扭力高,在非公路机械中更有效率、更可靠、更节省空间。轻质材料(如合金和复合材料)的应用也在不断增长,有助于在保持强度的同时减轻整体重量。此外,噪音和振动抑制技术的进步也被整合到齿轮系统中,以提高操作人员的舒适度并延长机器部件的使用寿命。

内燃机(ICE)市场在2024年占据81%的市场份额,预计到2034年将以5.2%的复合年增长率成长。儘管电气化趋势日益明显,但由于其可靠性和动力性,内燃机在非公路应用领域仍然更受欢迎。製造商正致力于提高燃油效率和减少排放,以满足日益严格的环保标准。

2024年,美国非公路用机械传动零件市场占86.1%的市场份额,市场规模达7.289亿美元。美国快速的城市化进程、不断增长的可支配收入以及对高端车辆日益增长的需求,都是促成这一市场主导地位的因素。在美国,由于液压传动系统具有灵活性、高效率性和动力输出平顺等优点,其在非公路用机械的应用越来越广泛。这些系统特别适用于需要变速控制的应用,例如工程机械和农业机械。

全球非公路用机械传动部件市场的主要领导者包括艾里逊变速器公司 (Allison Transmission)、博格华纳 (BorgWarner)、博世力士乐 (Bosch Rexroth)、卡特彼勒 (Caterpillar)、凯斯纽荷兰工业集团 (CNH Industrial)、伊顿山公司 (Eomton Corporation)、约翰迪森公司 (Kerea)、Milton Corporation (Eoma Corporation) Friedrichshafen)。为了巩固市场地位,非公路用机械传动零件市场的企业正致力于技术创新和产品多元化。许多企业正在投资开发先进的传动系统,例如静液压和电液传动解决方案,以提高非公路用机械的效率、耐用性和能源性能。这些企业也与整车製造商 (OEM) 建立战略合作伙伴关係,将自身的传动技术直接整合到新一代非公路用机械中。此外,这些企业正在扩大其生产能力,尤其是在北美和亚洲等基础设施需求不断增长的地区。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预测模型

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 价值链分析

- 上游价值链

- 中游价值链

- 下游价值链

- 产业影响因素

- 成长驱动因素

- 对建筑和采矿设备的需求不断增长

- 转型为电气化和混合动力系统

- 输电系统的技术进步

- 新兴市场的成长

- 产业陷阱与挑战

- 电气化系统的高资本投资

- 原物料价格波动

- 复杂的维护要求

- 新兴市场的基础设施局限性

- 市场机会

- 售后服务拓展

- 采用自主智慧设备

- 政府补贴和激励措施

- 特种设备领域的新兴应用

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 美国环保署第四阶段最终标准实施

- 欧盟第五阶段排放标准合规要求

- 区域规范架构差异

- 未来排放标准制定

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 下一代输电技术

- 设备全面电气化时间表

- 自主设备集成

- 数位孪生与仿真技术

- 永续製造趋势

- 价格趋势

- 车辆

- 地区

- 专利分析

- 生产统计

- 生产中心

- 消费中心

- 进出口

- 成本細項分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- OEM与售后市场竞争动态

- 原始设备整合策略

- 售后服务及更换车型

- 再製造与循环经济趋势

- 通路衝突与合作伙伴关係管理

- 设备自动化与连接集成

- 自主设备传输要求

- 物联网与车载资讯系统集成

- 预测性维护与诊断

- 远端监控系统

- 製造与生产挑战

- 区域製造战略

- 生产能力和可扩展性

- 品质控制与测试标准

- 精实生产与流程优化

- 设备生命週期及服务注意事项

- 组件耐久性和可靠性要求

- 服务间隔优化

- 现场服务与支援策略

- 报废组件管理

- 设备电气化与技术转型

- 电力传输技术应用

- 混合动力系统整合挑战

- 电池技术与电源管理

- 传统系统与电力系统对比

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东非洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 齿轮及齿轮系统

- 离合器和煞车

- 液力变矩器

- 油压元件

- 控制系统

- 电力传输组件

第六章:市场估算与预测:以推进方式划分,2021-2034年

- 主要趋势

- 冰

- 电的

- 电池电动车(BEV)

- 混合动力电动车(HEV)

- 插电式混合动力车(PHEV)

- 杂交种

第七章:市场估价与预测:依车辆类型划分,2021-2034年

- 主要趋势

- 工程机械

- 挖土机和反铲挖土机

- 推土机和铲运机

- 轮式装载机和滑移装载机

- 平地机和压路机

- 农业机械

- 拖拉机和多用途车辆

- 联合收割机

- 喷雾器和施药器

- 耕作和播种设备

- 采矿设备

- 运输卡车和自卸卡车

- 挖土机和铲车

- 地下设备

- 破碎加工设备

- 林业设备

- 收割机和加工机

- 集材机和集材机

- 伐木工

- 原木装载机和剥皮机

- 物料搬运设备

- 堆高机和伸缩臂堆高机

- 越野起重机

- 高空作业平台

- 容器处理器

第八章:市场估算与预测:依技术划分,2021-2034年

- 主要趋势

- 机械传动系统

- 静压和液压机械系统

- 混合动力和电动动力系统

- 控制与执行技术

第九章:市场估算与预测:依销售管道划分,2021-2034年

- 主要趋势

- OEM

- 售后市场

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 波兰

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 越南

- 新加坡

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十一章:公司简介

- 全球领导人

- ZF Friedrichshafen

- 艾里逊变速器

- 伊顿

- 博世力士乐

- 派克汉尼汾

- 毛虫

- 约翰迪尔

- CNH工业

- 博格华纳

- 区域冠军

- 小松

- 沃尔沃

- 利勃海尔

- 斗山

- 日立

- 三一

- 徐工集团

- JCB

- 新兴参与者

- 卡拉罗

- 双碟

- 邦迪奥利和帕韦西

- 液压齿轮

- 波克兰

- 布雷维尼

- 雷克斯诺德

The Global Off-Highway Equipment Transmission Component Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 4.8 billion by 2034.

The market growth is driven by increasing investments in infrastructure projects, including roads, bridges, and housing developments. These projects require construction equipment equipped with durable transmission systems capable of handling heavy loads for extended periods. The demand for off-highway machinery is also rising due to rapid urbanization, particularly in Asia and Africa. Moreover, the agriculture sector, especially in developing countries, is embracing mechanization, with advanced transmission systems becoming more common in tractors, harvesters, and sprayers. These systems, such as hydrostatic and electro-hydraulic transmissions, are gaining popularity because of their efficiency, precision, and ease of operation. Similarly, the mining industry continues to grow as demand for minerals and fossil fuels remains high, leading to greater reliance on robust transmission systems in heavy-duty machinery. Although the electrification of mining equipment is a growing trend, diesel-powered machinery still relies on durable transmissions to function efficiently in challenging environments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.8 Billion |

| CAGR | 5.4% |

The gears & gear systems segment accounted for a 31.6% share in 2024 and is expected to grow at a CAGR of 6.1% through 2034. This segment is benefiting from the increasing adoption of planetary gear sets, which provide compact, high-torque solutions that are more efficient, reliable, and space-efficient in off-highway machinery. The use of lightweight materials such as alloys and composites is also growing, helping to reduce overall weight while maintaining strength. Additionally, advancements in noise and vibration suppression technologies are being integrated into gear systems to improve both operator comfort and the longevity of machine parts.

The internal combustion engine (ICE) segment held an 81% share in 2024 and is expected to grow at a CAGR of 5.2% through 2034. Despite the growing trend toward electrification, ICEs are still preferred in off-highway applications due to their reliability and power. Manufacturers are focusing on improving fuel efficiency and reducing emissions to meet stringent environmental standards.

U.S. Off-Highway Equipment Transmission Component Market held 86.1% in 2024, with USD 728.9 million. The country's rapid urbanization, growing disposable incomes, and increasing demand for premium vehicles are all contributing factors to this dominance. In the U.S., hydrostatic transmissions are becoming more widely used in off-highway machinery due to their flexibility, efficiency, and smooth power delivery. These systems are particularly beneficial in applications that require variable speed control, such as construction and agricultural machinery.

Key companies leading the Global Off-Highway Equipment Transmission Component Market include Allison Transmission, BorgWarner, Bosch Rexroth, Caterpillar, CNH Industrial, Eaton Corporation, John Deere, Komatsu, and ZF Friedrichshafen. To strengthen their position, companies in the Off-Highway Equipment Transmission Component Market are focusing on technological innovation and product diversification. Many are investing in the development of advanced transmission systems, such as hydrostatic and electro-hydraulic solutions, to improve the efficiency, durability, and energy performance of off-highway machinery. Companies are also forming strategic partnerships with OEMs to integrate their transmission technologies directly into new-generation off-highway equipment. Furthermore, these players are expanding their manufacturing capabilities, particularly in regions with growing infrastructure needs, like North America and Asia.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Propulsion

- 2.2.4 Vehicle

- 2.2.5 Technology

- 2.2.6 Sales channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Value chain analysis

- 3.2.1 Upstream value chain

- 3.2.2 Midstream value chain

- 3.2.3 Downstream value chain

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increasing Demand for Construction and Mining Equipment

- 3.3.1.2 Shift Towards Electrification and Hybrid Powertrains

- 3.3.1.3 Technological Advancements in Transmission Systems

- 3.3.1.4 Growth in Emerging Markets

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High Capital Investment for Electrified Systems

- 3.3.2.2 Volatility in Raw Material Prices

- 3.3.2.3 Complex Maintenance Requirements

- 3.3.2.4 Infrastructure Limitations in Emerging Markets

- 3.3.3 Market opportunities

- 3.3.3.1 Expansion of Aftermarket Services

- 3.3.3.2 Adoption of Autonomous and Smart Equipment

- 3.3.3.3 Government Subsidies and Incentives

- 3.3.3.4 Emerging Applications in Specialty Equipment

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.5.1 EPA Tier 4 Final Standards Implementation

- 3.5.2 EU Stage V Emissions Compliance Requirements

- 3.5.3 Regional Regulatory Framework Variations

- 3.5.4 Future Emissions Standards Development

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

- 3.8 Technology and Innovation landscape

- 3.8.1 Next-Generation Transmission Technologies

- 3.8.2 Full Equipment Electrification Timeline

- 3.8.3 Autonomous Equipment Integration

- 3.8.4 Digital Twin & Simulation Technologies

- 3.8.5 Sustainable Manufacturing Trends

- 3.9 Price trends

- 3.9.1 Vehicles

- 3.9.2 Region

- 3.10 Patent analysis

- 3.11 Production statistics

- 3.11.1 Production hubs

- 3.11.2 Consumption hubs

- 3.11.3 Export and import

- 3.12 Cost breakdown analysis

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly Initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 OEM vs Aftermarket Competition Dynamics

- 3.14.1 Original Equipment Integration Strategies

- 3.14.2 Aftermarket Service & Replacement Models

- 3.14.3 Remanufacturing & Circular Economy Trends

- 3.14.4 Channel Conflict & Partnership Management

- 3.15 Equipment Automation & Connectivity Integration

- 3.15.1 Autonomous Equipment Transmission Requirements

- 3.15.2 IoT & Telematics Integration

- 3.15.3 Predictive Maintenance & Diagnostics

- 3.15.4 Remote Monitoring & Control Systems

- 3.16 Manufacturing & Production Challenges

- 3.16.1 Regional Manufacturing Strategies

- 3.16.2 Production Capacity & Scalability

- 3.16.3 Quality Control & Testing Standards

- 3.16.4 Lean Manufacturing & Process Optimization

- 3.17 Equipment Lifecycle & Service Considerations

- 3.17.1 Component Durability & Reliability Requirements

- 3.17.2 Service Interval Optimization

- 3.17.3 Field Service & Support Strategies

- 3.17.4 End-of-Life Component Management

- 3.18 Equipment Electrification & Technology Transition

- 3.18.1 Electric Transmission Technology Adoption

- 3.18.2 Hybrid Powertrain Integration Challenges

- 3.18.3 Battery Technology & Power Management

- 3.18.4 Traditional vs Electric System Comparison

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Gears & Gear Systems

- 5.3 Clutches & Brakes

- 5.4 Torque Converters

- 5.5 Hydraulic Components

- 5.6 Control Systems

- 5.7 Power Transfer Components

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

- 6.3.1 Battery electric vehicles (BEVs)

- 6.3.2 Hybrid electric vehicles (HEVs)

- 6.3.3 Plug-in hybrid electric vehicles (PHEVs)

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Construction Equipment

- 7.2.1 Excavators & Backhoes

- 7.2.2 Bulldozers & Scrapers

- 7.2.3 Wheel Loaders & Skid Steers

- 7.2.4 Motor Graders & Compactors

- 7.3 Agricultural Machinery

- 7.3.1 Tractors & Utility Vehicles

- 7.3.2 Combines & Harvesters

- 7.3.3 Sprayers & Applicators

- 7.3.4 Tillage & Planting Equipment

- 7.4 Mining Equipment

- 7.4.1 Haul Trucks & Dump Trucks

- 7.4.2 Draglines & Shovels

- 7.4.3 Underground Equipment

- 7.4.4 Crushing & Processing Equipment

- 7.5 Forestry Equipment

- 7.5.1 Harvesters & Processors

- 7.5.2 Forwarders & Skidders

- 7.5.3 Feller Bunchers

- 7.5.4 Log Loaders & Delimbers

- 7.6 Material Handling Equipment

- 7.6.1 Forklifts & Telehandlers

- 7.6.2 Rough Terrain Cranes

- 7.6.3 Aerial Work Platforms

- 7.6.4 Container Handlers

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Mechanical Transmission Systems

- 8.3 Hydrostatic & Hydro-mechanical Systems

- 8.4 Hybrid & Electrified Powertrains

- 8.5 Control & Actuation Technologies

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Poland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Vietnam

- 10.4.7 Singapore

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1.1 Global Leaders

- 11.1.1.1 ZF Friedrichshafen

- 11.1.1.2 Allison Transmission

- 11.1.1.3 Eaton

- 11.1.1.4 Bosch Rexroth

- 11.1.1.5 Parker Hannifin

- 11.1.1.6 Caterpillar

- 11.1.1.7 John Deere

- 11.1.1.8 CNH Industrial

- 11.1.1.9 BorgWarner

- 11.1.2 Regional Champions

- 11.1.2.1 Komatsu

- 11.1.2.2 Volvo

- 11.1.2.3 Liebherr

- 11.1.2.4 Doosan

- 11.1.2.5 Hitachi

- 11.1.2.6 SANY

- 11.1.2.7 XCMG

- 11.1.2.8 JCB

- 11.1.3 Emerging Players

- 11.1.3.1 Carraro

- 11.1.3.2 Twin Disc

- 11.1.3.3 Bondioli & Pavesi

- 11.1.3.4 Hydro-Gear

- 11.1.3.5 Poclain

- 11.1.3.6 Brevini

- 11.1.3.7 Rexnord

汽车润滑油市场分析及预测(至2035年):类型、产品、服务、技术、应用、形式、材质类型、介绍形式、最终用户、功能

汽车润滑油市场分析及预测(至2035年):类型、产品、服务、技术、应用、形式、材质类型、介绍形式、最终用户、功能 汽车润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国汽车润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南汽车润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

汽车润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)美国汽车润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)越南汽车润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球汽车润滑油市场规模、份额、趋势和成长分析报告(2026-2034)

全球汽车润滑油市场规模、份额、趋势和成长分析报告(2026-2034) 三轮车润滑油市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、销售管道、产品类型、地区及竞争格局划分,2021-2031年)商用车润滑油市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、销售管道、产品类型、地区及竞争格局划分,2021-2031年)摩托车润滑油市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、销售管道、产品类型、地区及竞争格局划分,2021-2031年)汽车润滑油市场-全球产业规模、份额、趋势、竞争格局、机会及预测(依车辆类型、销售管道、产品类型、地区及竞争状况划分,2021-2031年)乘用车润滑油市场-全球产业规模、份额、趋势、机会及预测,依车辆类型、销售通路、产品类型、地区及竞争格局划分,2021-2031年预测

三轮车润滑油市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、销售管道、产品类型、地区及竞争格局划分,2021-2031年)商用车润滑油市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、销售管道、产品类型、地区及竞争格局划分,2021-2031年)摩托车润滑油市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、销售管道、产品类型、地区及竞争格局划分,2021-2031年)汽车润滑油市场-全球产业规模、份额、趋势、竞争格局、机会及预测(依车辆类型、销售管道、产品类型、地区及竞争状况划分,2021-2031年)乘用车润滑油市场-全球产业规模、份额、趋势、机会及预测,依车辆类型、销售通路、产品类型、地区及竞争格局划分,2021-2031年预测