|

市场调查报告书

商品编码

1858834

汽车石墨烯增强组件市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Automotive Graphene-Enhanced Components Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

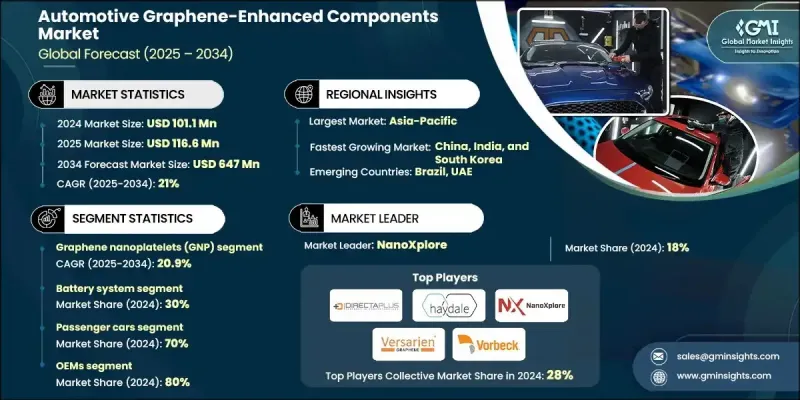

2024 年全球汽车石墨烯增强组件市场价值为 1.011 亿美元,预计到 2034 年将以 21% 的复合年增长率增长至 6.47 亿美元。

这种快速成长的动力源自于市场对兼具强度、轻量化和卓越能源性能的材料日益增长的需求。石墨烯优异的导电性、热调节性和机械耐久性使其成为汽车製造商提高效率和降低排放的首选材料。随着原始设备製造商 (OEM) 和一级供应商加大投资,整个产业正经历着从实验性应用向大规模部署的转变。亚太、北美和欧洲等主要市场的电气化进程是关键的催化剂,推动了石墨烯增强型电池、热系统和结构部件的普及应用。汽车製造商正积极与材料开发商和研究机构进行研发合作,以获得竞争优势。轻质石墨烯增强复合材料正逐步取代传统的金属零件,直接有助于提高燃油经济性和延长电动车的续航里程。这些趋势与旨在促进永续汽车生产和减少全球碳排放的严格监管目标相契合,进一步巩固了石墨烯在下一代汽车製造领域的长期潜力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1.011亿美元 |

| 预测值 | 6.47亿美元 |

| 复合年增长率 | 21% |

预计到2024年,电池系统市占率将达到30%。电动车的日益普及推动了对石墨烯电池解决方案的需求,因为石墨烯电池具有卓越的导电性和能量密度。这些优势有助于实现超快速充电、延长电池寿命和提高热安全性等功能。因此,汽车製造商和供应商持续积极致力于提升电池性能,并对该领域保持高度关注。

2025年至2034年间,石墨烯奈米片(GNP)市场预计将以20.9%的复合年增长率成长。 GNP因其价格低廉、易于规模化生产以及均衡的机械和热性能而备受青睐。它们在包括结构复合材料、电池电极和功能涂层在内的众多应用领域正日益受到关注。其成本效益和多功能性使其成为大规模汽车整合应用的理想选择。

预计到2024年,美国汽车石墨烯增强零件市场规模将达2,330万美元,成为汽车石墨烯增强零件的关键市场。电动车的强劲普及以及日益严格的排放和燃油效率法规推动了该市场的成长。美国製造商正在快速部署石墨烯基电池组、电子元件和热管理系统,以满足商用车和乘用车领域的性能标准。

在全球汽车石墨烯增强零件市场中,Vorbeck Materials、First Graphene、Graphene Nanochem、NanoXplore、Graphenea、Directa Plus、Applied Graphene Materials (AGM)、Nanotech Energy、Versarien 和 Haydale Graphene Industries 等公司占据着举足轻重的地位。为了巩固其在汽车石墨烯增强零件市场的地位,领导企业正采取以创新、规模化和合作为核心的关键策略。许多企业优先开发针对特定汽车功能的客製化石墨烯配方,例如提升电池效率、热调节和结构强度。此外,各公司也正在投资先进製造技术以支援大规模生产,同时优化成本效益。与汽车原始设备製造商 (OEM)、研究型大学和材料供应商的策略合作,有助于加速产品测试和商业化推广。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预报

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 电动车产量增加和电池普及

- 轻量化和燃油效率目标

- 高性能电子产品的兴起

- 奈米材料研发的大力投资

- 产业陷阱与挑战

- 石墨烯材料的生产成本很高

- 规模有限的大型供应链

- 市场机会

- 下一代电动车电池和超级电容器

- 热管理系统中的应用

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 用例和应用

- 最佳情况

- 成本效益分析与投资报酬率优化

- 材料成本与性能之间的权衡

- 製造成本影响评估

- 总拥有成本模型

- 价值工程策略

- 知识产权与技术许可

- 专利格局分析

- 技术授权模式

- 保护策略

- 自由实施评估

- 市场接受度与客户接受度

- OEM製造商决策标准

- 消费者认知与接受度

- 市场教育与意识提升计划

- 竞争差异化策略

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 引擎室内部件

- 泡棉垫

- 燃油导轨盖

- 泵浦盖

- 结构复合材料

- 电池系统组件

- 热管理系统

- 电子元件

第六章:市场估计与预测:依石墨烯材料划分,2021-2034年

- 主要趋势

- 石墨烯奈米片(GNP)

- 氧化石墨烯(GO)

- 还原氧化石墨烯(RGO)

- 化学气相沉积石墨烯薄膜

第七章:市场估价与预测:依车辆类型划分,2021-2034年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- SUV

- 商用车辆

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第八章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 原始设备製造商

- 售后市场及服务提供者

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- 全球参与者

- Applied Graphene Materials

- Directa Plus

- First Graphene

- Graphenea

- Haydale Graphene Industries

- Nanotech Energy

- NanoXplore

- Versarien

- Vorbeck Materials

- XG Sciences

- 区域玩家

- Angstron Materials

- Black Swan Graphene

- Graphene NanoChem

- Graphene 3D Lab

- Global Graphene Group

- Nanocyl

- Skeleton Technologies

- Talga Resources

- Graphmatech

- 新兴参与者/颠覆者

- Archer Materials

- Avancis Graphene

- Cnano Technology

- Elcora Advanced Materials

- Garmor Graphene

- Grolltex

- NanoGraphene

- Zap & Go

- 2 D Carbon Tech

The Global Automotive Graphene-Enhanced Components Market was valued at USD 101.1 million in 2024 and is estimated to grow at a CAGR of 21% to reach USD 647 million by 2034.

This rapid growth is fueled by the increasing demand for materials that deliver strength, lightweight design, and superior energy performance. Graphene's exceptional conductivity, thermal regulation, and mechanical durability make it a preferred choice for automakers aiming to enhance efficiency and lower emissions. The industry is witnessing a shift from experimental usage to large-scale implementation as OEMs and Tier-1 suppliers ramp up investments. Electrification across major markets in Asia Pacific, North America, and Europe is a key catalyst, pushing the adoption of graphene-enhanced batteries, thermal systems, and structural components. Automotive manufacturers are actively engaging in R&D collaborations with material developers and research institutions to gain a competitive edge. Lightweight graphene-reinforced composites are gradually replacing traditional metal parts, directly contributing to better fuel economy and longer EV driving range. These trends align with stringent regulatory goals that promote sustainable automotive production and reduction in carbon emissions globally, reinforcing the long-term potential of graphene in next-generation vehicle manufacturing.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $101.1 Million |

| Forecast Value | $647 Million |

| CAGR | 21% |

The battery system segment held a 30% share in 2024. The rising penetration of electric vehicles is fueling demand for graphene-enabled battery solutions, as they offer superior conductivity and energy density. These advancements support features such as ultra-fast charging, enhanced battery life, and improved thermal safety. As a result, the segment continues to see strong engagement from automakers and suppliers focused on performance improvement.

The graphene nanoplatelets (GNP) segment will grow at a CAGR of 20.9% between 2025 and 2034. GNPs are used for their affordability, scalability, and balanced mechanical and thermal performance. They are gaining traction in a broad array of applications, including structural composites, battery electrodes, and functional coatings. Their cost-effective profile and multi-functional performance make them a preferred choice for large-scale automotive integration.

United States Automotive Graphene-Enhanced Components Market reached USD 23.3 million in 2024, emerging as a key market for automotive graphene-enhanced components. Growth is supported by strong EV adoption and strict emissions and fuel efficiency regulations. American manufacturers are rapidly deploying graphene-based battery packs, electronics, and thermal systems to meet performance benchmarks in both commercial and passenger vehicle segments.

Prominent companies shaping the Global Automotive Graphene-Enhanced Components Market include Vorbeck Materials, First Graphene, Graphene Nanochem, NanoXplore, Graphenea, Directa Plus, Applied Graphene Materials (AGM), Nanotech Energy, Versarien, and Haydale Graphene Industries. To solidify their position in the Automotive Graphene-Enhanced Components Market, leading companies are adopting key strategies focused on innovation, scalability, and partnerships. Many are prioritizing the development of tailored graphene formulations for specific automotive functions such as battery efficiency, thermal regulation, and structural strength. Firms are also investing in advanced manufacturing technologies to support mass production, while optimizing the cost-performance balance. Strategic collaborations with automotive OEMs, research universities, and materials suppliers are helping accelerate product testing and commercial rollout.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Graphene material

- 2.2.4 Vehicle

- 2.2.5 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing EV production and battery adoption

- 3.2.1.2 Lightweighting and fuel efficiency targets

- 3.2.1.3 Rise in high-performance electronics

- 3.2.1.4 Strong investments in nanomaterials R&D

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production cost of graphene materials

- 3.2.2.2 Limited large-scale supply chain

- 3.2.3 Market opportunities

- 3.2.3.1 Next-gen EV batteries and supercapacitors

- 3.2.3.2 Adoption in thermal management systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Sustainability & environmental aspects

- 3.9.1 Sustainable practices

- 3.9.2 Waste reduction strategies

- 3.9.3 Energy efficiency in production

- 3.9.4 Eco-friendly Initiatives

- 3.9.5 Carbon footprint considerations

- 3.10 Use cases and applications

- 3.11 Best-case scenario

- 3.12 Cost-benefit analysis & roi optimization

- 3.12.1 Material cost vs performance trade-offs

- 3.12.2 Manufacturing cost impact assessment

- 3.12.3 Total cost of ownership models

- 3.12.4 Value engineering strategies

- 3.13 Intellectual property & technology licensing

- 3.13.1 Patent landscape analysis

- 3.13.2 Technology licensing models

- 3.13.3 Protection strategies

- 3.13.4 Freedom-to-operate assessments

- 3.14 Market adoption & customer acceptance

- 3.14.1 OEM decision-making criteria

- 3.14.2 Consumer perception & acceptance

- 3.14.3 Market education & awareness programs

- 3.14.4 Competitive differentiation strategies

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Under-hood components

- 5.2.1 Foam covers

- 5.2.2 Fuel rail covers

- 5.2.3 Pump covers

- 5.3 Structural composites

- 5.4 Battery system components

- 5.5 Thermal management systems

- 5.6 Electronic components

Chapter 6 Market Estimates & Forecast, By Graphene Material, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Graphene nanoplatelets (GNP)

- 6.3 Graphene oxide (GO)

- 6.4 Reduced graphene oxide (RGO)

- 6.5 CVD graphene films

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Medium commercial vehicles (MCV)

- 7.3.3 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 OEMs

- 8.3 Aftermarket & Service Providers

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Applied Graphene Materials

- 10.1.2 Directa Plus

- 10.1.3 First Graphene

- 10.1.4 Graphenea

- 10.1.5 Haydale Graphene Industries

- 10.1.6 Nanotech Energy

- 10.1.7 NanoXplore

- 10.1.8 Versarien

- 10.1.9 Vorbeck Materials

- 10.1.10 XG Sciences

- 10.2 Regional Players

- 10.2.1 Angstron Materials

- 10.2.2 Black Swan Graphene

- 10.2.3 Graphene NanoChem

- 10.2.4. Graphene 3D Lab

- 10.2.5 Global Graphene Group

- 10.2.6 Nanocyl

- 10.2.7 Skeleton Technologies

- 10.2.8 Talga Resources

- 10.2.9 Graphmatech

- 10.3 Emerging Players / Disruptors

- 10.3.1 Archer Materials

- 10.3.2 Avancis Graphene

- 10.3.3 Cnano Technology

- 10.3.4 Elcora Advanced Materials

- 10.3.5 Garmor Graphene

- 10.3.6 Grolltex

- 10.3.7 NanoGraphene

- 10.3.8 Zap & Go

- 10.3.9. 2 D Carbon Tech

汽车电气换向器市场:按类型、电压、应用和最终用户划分,全球预测,2026-2032年

汽车电气换向器市场:按类型、电压、应用和最终用户划分,全球预测,2026-2032年 隔振支架市场规模、份额和成长分析:按产品类型、应用、最终用户、分销管道、地区和产业预测,2026-2033年

隔振支架市场规模、份额和成长分析:按产品类型、应用、最终用户、分销管道、地区和产业预测,2026-2033年 全球汽车电气产品市场规模、份额、趋势和成长分析报告(2026-2034)

全球汽车电气产品市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球汽车纺织品市场报告

2026年全球汽车纺织品市场报告 引擎盖挡风玻璃市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、材料类型、地区和竞争格局划分,2021-2031年)汽车挡泥板市场 - 全球产业规模、份额、趋势、机会及预测(按类型、车辆类型、销售管道、地区和竞争格局划分,2021-2031年)重型车辆塑胶零件市场-全球产业规模、份额、趋势、机会及预测(按零件类型、材料类型、车辆类型、地区和竞争格局划分,2021-2031年)汽车增强薄膜市场:按薄膜类型、基材、最终用途、技术、车辆类型和应用划分-全球预测,2026-2032年汽车焊接生产线市场:依焊接方法、自动化程度、材料类型、应用、车辆类型和最终用户产业划分-2026-2032年全球预测汽车燃油管路市场按燃油类型、车辆类型、材质、应用和最终用途划分-全球预测(2026-2032 年)

引擎盖挡风玻璃市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、材料类型、地区和竞争格局划分,2021-2031年)汽车挡泥板市场 - 全球产业规模、份额、趋势、机会及预测(按类型、车辆类型、销售管道、地区和竞争格局划分,2021-2031年)重型车辆塑胶零件市场-全球产业规模、份额、趋势、机会及预测(按零件类型、材料类型、车辆类型、地区和竞争格局划分,2021-2031年)汽车增强薄膜市场:按薄膜类型、基材、最终用途、技术、车辆类型和应用划分-全球预测,2026-2032年汽车焊接生产线市场:依焊接方法、自动化程度、材料类型、应用、车辆类型和最终用户产业划分-2026-2032年全球预测汽车燃油管路市场按燃油类型、车辆类型、材质、应用和最终用途划分-全球预测(2026-2032 年)