|

市场调查报告书

商品编码

1858846

用于光计算的光子晶体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Photonic Crystals for Optical Computing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

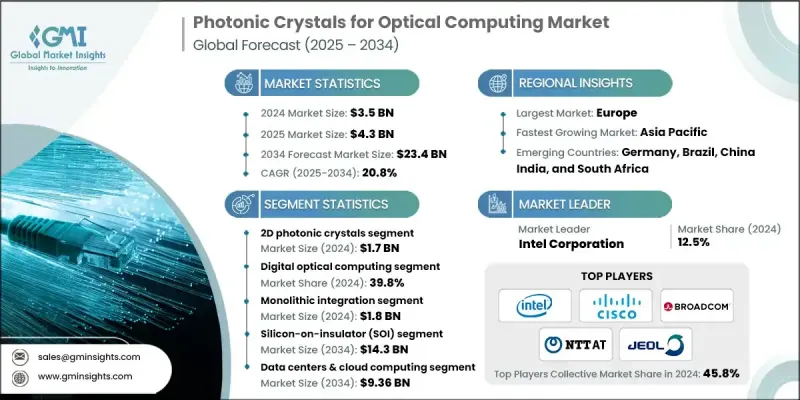

2024 年全球光子晶体光运算市场价值为 35 亿美元,预计到 2034 年将以 20.8% 的复合年增长率成长至 234 亿美元。

这一增长反映了光子晶体技术,特别是高效能运算系统中光子晶体技术的日益融合。推动这一增长的关键因素包括对指数级资料处理需求的不断增长、硅光子学的演进以及新型光计算架构的出现。政府资助和国防现代化计画对节能运算基础设施的推动也是重要因素。这些技术的潜在应用十分广泛,包括资料中心、电信、量子运算以及人工智慧/机器学习加速等,所有这些都持续推动市场成长。此外,旨在提升基于光子晶体的光计算系统性能和可扩展性的研发投入不断增加,也加速了其应用。随着製造流程的改进和成本的降低,预计这些技术将在全球各行各业和各个地区中广泛应用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 35亿美元 |

| 预测值 | 234亿美元 |

| 复合年增长率 | 20.8% |

预计2024年,二维光子晶体市场规模将达17亿美元,复合年增长率(CAGR)为20.7%。先进光运算领域对二维光子晶体的需求主要源自于其能够与波导和光子晶体平板结构高效整合。製造技术和加工流程的进步也推动了这一趋势,降低了传统上与这些系统相关的严格性能要求。

预计到2024年,数位光运算领域将占据39.8%的市场份额,高速资料处理的需求是推动这一领域发展的主要动力。先进的全光交换系统、二元逻辑运算以及速度更快的数位讯号处理等创新技术将进一步促进成长。此外,计算领域的能源效率优化以及政府对增强型运算基础设施的投资也是重要的市场驱动因素。

2024年,欧洲光子晶体光运算市场规模达12亿美元。预计到2034年,欧洲市场将显着成长,达到81亿美元,复合年增长率(CAGR)为20.8%。推动这一成长的因素包括:对节能运算解决方案的需求不断增长、对光子学研发的大量投资,以及光计算技术在资料中心和电信领域的日益普及。

全球光子晶体光运算市场的主要参与者包括英特尔公司、Lightmatter公司、NTT先进技术公司、Xanadu Quantum Technologies公司、G&H Photonics有限公司、思科系统公司、PsiQuantum公司、Ayar Labs公司、日本电子株式会社和博通公司。为了维持和扩大市场份额,该领域的公司正致力于提升产品性能并实现产品组合多元化。对研发的策略性投资是推出先进光子晶体解决方案、提高可扩展性和功能性的关键。各公司也与学术机构、研究组织和其他行业领导者合作,以推动创新并提高光计算系统的效率。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 司机:

- 对速度更快、能效更高的运算能力的需求

- 奈米技术和製造方法的进步

- 不断增长的资料流量和人工智慧/机器学习处理需求

- 量子和光学运算领域的研发投入不断成长

- 陷阱与挑战:

- 生产流程复杂且成本高

- 与现有半导体系统的集成

- 机会:

- 人工智慧、5G 和资料中心基础设施的扩展

- 新兴量子运算架构

- 学术界与科技公司之间的合作

- 政府和国防部在先进计算领域的投资

- 司机:

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按产品规格

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)

(註:贸易统计仅针对重点国家提供)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品类型划分,2021-2034年

- 主要趋势

- 一维光子晶体

- 二维光子晶体

- 三维光子晶体

第六章:市场估算与预测:依整合类型划分,2021-2034年

- 主要趋势

- 整体集成

- 混合集成

- 总消耗量

第七章:市场估计与预测:依材料平台划分,2021-2034年

- 主要趋势

- 绝缘体上硅(SOI)

- III-V族半导体

- 相变材料

第八章:市场估算与预测:依计算功能划分,2021-2034年

- 主要趋势

- 数位光学计算

- 类比光计算

- 量子光学计算

- 神经形态光学计算

第九章:市场估算与预测:依最终用途产业划分,2021-2034年

- 主要趋势

- 资料中心和云端运算

- 电信

- 国防与航太

- 研究机构

- 高效能运算

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十一章:公司简介

- Intel Corporation

- Cisco Systems Inc.

- Broadcom Inc.

- NTT Advanced Technology

- JEOL Ltd.

- G&H Photonics Ltd.

- Xanadu Quantum Technologies

- PsiQuantum Corp.

- Ayar Labs Inc.

- Lightmatter Inc.

The Global Photonic Crystals for Optical Computing Market was valued at USD 3.5 billion in 2024 and is estimated to grow at a CAGR of 20.8% to reach USD 23.4 billion by 2034.

This expansion reflects the growing integration of photonic crystal technologies, particularly in high-performance computing systems. Key factors fueling this growth include the increasing demand for exponential data processing, the evolution of silicon photonics, and new architecture for optical computing. The push for energy-efficient computing infrastructures, backed by government funding and defense modernization programs, is also a major contributor. The potential applications for these technologies are vast, including data centers, telecommunications, quantum computing, and AI/ML acceleration, all of which continue to drive market growth. Furthermore, rising investments in research and development aimed at enhancing the performance and scalability of photonic crystal-based optical computing systems are accelerating adoption. As manufacturing processes improve and costs decrease, the widespread adoption of these technologies is anticipated across various global industries and regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.5 Billion |

| Forecast Value | $23.4 Billion |

| CAGR | 20.8% |

The 2D photonic crystal segment is expected to reach USD 1.7 billion in 2024, with a CAGR of 20.7%. The demand for 2D photonic crystals in advanced optical computing is attributed to their ability to integrate efficiently with waveguides and photonic crystal slab architectures. This trend is also facilitated by advancements in manufacturing techniques and processing technologies, which are easing the strict performance criteria traditionally associated with these systems.

The digital optical computing segment held a 39.8% share in 2024 as high-speed data processing is driving demand. Innovations such as advanced all-optical switching systems, binary logic operations, and digital signal processing with faster capabilities further contribute to growth. Additionally, energy efficiency optimization in computing and government investments in enhanced computing infrastructure are major market drivers.

Europe Photonic Crystals for Optical Computing Market generated USD 1.2 billion in 2024. The European market is expected to grow significantly, reaching USD 8.1 billion by 2034, at a CAGR of 20.8%. This growth is propelled by the increasing demand for energy-efficient computing solutions, significant investments in photonics research and development, and the growing implementation of optical computing technologies in data centers and telecommunications.

Key players in the Global Photonic Crystals for Optical Computing Market include Intel Corporation, Lightmatter Inc., NTT Advanced Technology, Xanadu Quantum Technologies, G&H Photonics Ltd., Cisco Systems Inc., PsiQuantum Corp., Ayar Labs Inc., JEOL Ltd., and Broadcom Inc. To maintain and expand their market presence, companies in this space are focusing on enhancing product performance and diversifying their portfolios. Strategic investments in research and development are key to the introduction of advanced photonic crystal solutions, improving scalability and functionality. Firms are also collaborating with academic institutions, research organizations, and other industry leaders to drive innovation and improve the efficiency of optical computing systems.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Integration type

- 2.2.4 Material platform

- 2.2.5 Computing function

- 2.2.6 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Drivers:

- 3.2.1.1 Demand for faster, energy-efficient computing

- 3.2.1.2 Advancements in nanotechnology and fabrication methods

- 3.2.1.3 Rising data traffic and AI/ML processing needs

- 3.2.1.4 Growing R&D investment in quantum and optical computing

- 3.2.2 Pitfalls & Challenges:

- 3.2.2.1 High production complexity and cost

- 3.2.2.2 Integration with existing semiconductor systems

- 3.2.3 Opportunities:

- 3.2.3.1 Expansion of AI, 5G, and data center infrastructure

- 3.2.3.2 Emerging quantum computing architectures

- 3.2.3.3 Collaborations between academia and tech firms

- 3.2.3.4 Government and defense investments in advanced computing

- 3.2.1 Drivers:

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product format

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 1D photonic crystals

- 5.3 2D photonic crystals

- 5.4 3D photonic crystals

Chapter 6 Market Estimates and Forecast, By Integration Type, 2021-2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Monolithic integration

- 6.3 Hybrid integration

- 6.4 Total consumption

Chapter 7 Market Estimates and Forecast, By Material Platform, 2021-2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Silicon-on-insulator (SOI)

- 7.3 III-V semiconductors

- 7.4 Phase-change materials

Chapter 8 Market Estimates and Forecast, By Computing Function, 2021-2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 Digital optical computing

- 8.3 Analog optical computing

- 8.4 Quantum optical computing

- 8.5 Neuromorphic optical computing

Chapter 9 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Million & Units)

- 9.1 Key trends

- 9.2 Data centers & cloud computing

- 9.3 Telecommunications

- 9.4 Defense & aerospace

- 9.5 Research institutions

- 9.6 High-performance computing

Chapter 10 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Intel Corporation

- 11.2 Cisco Systems Inc.

- 11.3 Broadcom Inc.

- 11.4 NTT Advanced Technology

- 11.5 JEOL Ltd.

- 11.6 G&H Photonics Ltd.

- 11.7 Xanadu Quantum Technologies

- 11.8 PsiQuantum Corp.

- 11.9 Ayar Labs Inc.

- 11.10 Lightmatter Inc.