|

市场调查报告书

商品编码

1858854

车载整合太阳能电池半导体市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Vehicle-Integrated Solar Cell Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

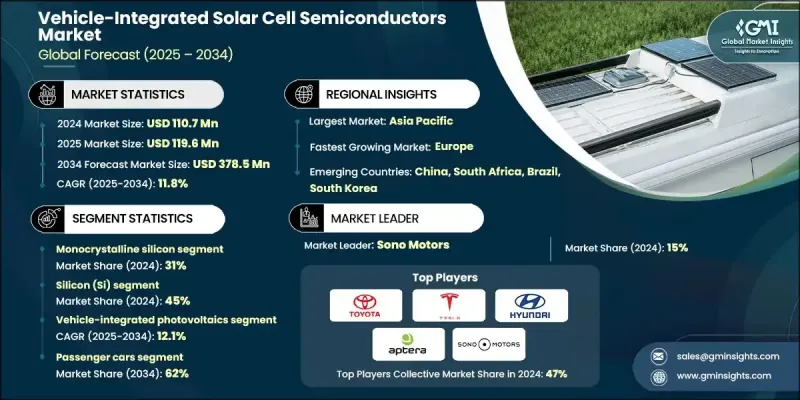

2024 年全球汽车整合太阳能电池半导体市场价值为 1.107 亿美元,预计到 2034 年将以 11.8% 的复合年增长率增长至 3.785 亿美元。

市场成长的驱动力来自于电动车的加速普及、半导体技术的持续进步以及对节能安全电源解决方案日益增长的需求。这一成长动能主要受到智慧出行创新、汽车电子设备升级以及汽车半导体生态系统竞争格局变化的影响。疫情后对晶片本地化和供应链韧性的重视也促进了这一成长,尤其是在亚洲和欧洲。在对电动交通和数位基础设施投资不断增加的推动下,这些地区正成为先进半导体製造的热点。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1.107亿美元 |

| 预测值 | 3.785亿美元 |

| 复合年增长率 | 11.8% |

全球汽车电气化进程以及对车载能源效率的需求正推动汽车製造商和一级供应商加大对晶片级集成技术的投资,使太阳能电池能够与智慧逆变器、区域控制器和先进的电源管理集成电路无缝协作。这些组件目前正被开发为可直接与光伏组件配合使用,从而实现更高的能源效率和更紧凑的系统设计。随着汽车向智慧互联繫统演进,半导体网路和架构的创新对于支持这项转型至关重要。

就材料而言,硅材料在2024年占据了45%的市场份额,预计到2034年将以12%的复合年增长率成长。硅材料的主导地位得益于其高可靠性、成熟的供应链以及在各种光照条件下的优异性能。同时,铜铟镓硒(CIGS)由于其柔韧性和适用于曲面车辆表面的特性,正日益受到青睐。

2024年,单晶硅市占率为31%,预计2025-2034年将以12.6%的复合年增长率成长。其稳定的功率输出和耐用性使其成为电动车和混合动力汽车车身整合式和车顶太阳能板的理想选择。

亚太地区车载整合式太阳能电池半导体市场预计到2024年将占据42.3%的市场份额,这主要得益于汽车和电子製造业的强劲发展。同时,欧洲正崛起为成长最快的地区,这主要归功于严格的安全法规、电动车的快速普及以及太阳能技术与半导体逻辑的日益融合,从而打造出高效、适用于车辆的能源解决方案。

推动全球车载整合太阳能电池半导体市场发展的关键企业包括特斯拉、比亚迪、Aptera、丰田、福特、Lightyear、PlanetSolar、现代和Sono Motors。这些公司正积极致力于将新一代半导体与太阳能技术结合,从而推动智慧能源汽车的发展。车载整合太阳能电池半导体市场的领导者正透过创新、合作和垂直整合等方式拓展市场份额。许多企业正大力投资研发,以开发能够实现高效能转换并与太阳能电池无缝整合的半导体。与汽车製造商和一级供应商的策略合作,正促进着能够优化电动车太阳能利用的能量管理系统的共同开发。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预测模型

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 电动车和混合动力车的普及率不断提高

- 太阳能半导体效率的进步

- 政府对绿色出行和节能车辆的激励措施

- 转型

- 消费者对永续和高端汽车设计的需求日益增长

- 产业陷阱与挑战

- 在严苛的汽车条件下仍能保持耐久性和可靠性

- 高昂的製造和整合成本

- 市场机会

- 钙钛矿和串联半导体研发领域的投资不断增加

- 与电动车和混合动力平台集成,以延长续航里程

- 拓展至两轮及三轮车市场

- 透明和玻璃整合光伏系统的出现

- 成长潜力分析

- 监管环境

- 区域太阳能併网法规

- 国际标准协调

- 环境法规的影响

- 进出口限制

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利分析

- 成本細項分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 未来展望与路线图

- 永续能源解决方案

- 跨产业融合趋势

- 监管演变和标准制定

- 市场整合与合作策略

- 汽车级太阳能半导体供应链

- 汽车业资格要求

- 长期供应保障策略

- 品质管理系统要求

- 供应链风险缓解

- 地缘政治对太阳能供应的影响

- 成本效益与能源生产优化

- 太阳能电池每瓦成本分析

- 安装和整合成本因素

- 能源回收期计算

- 总拥有成本模型

- 性能与价格权衡分析

- 汽车安全标准与太阳能集成

- 电气安全要求(ISO 6469)

- 消防安全与热失控预防

- 碰撞安全性和太阳能板性能

- 高压系统整合安全

- 紧急应变程序

- 下一代太阳能技术演进

- 钙钛矿太阳能电池的研发

- 有机光伏技术进步

- 透明太阳能电池创新

- 柔性太阳能薄膜的演变

- 多结电池集成

- 聚光光电应用

- 能源管理与车辆系统集成

- 太阳能收集优化

- 电池管理系统集成

- 电力电子与转换效率

- 储能策略优化

- 负载管理和优先权

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:依半导体产业划分,2021-2034年

- 主要趋势

- 单晶硅

- 多晶硅

- 薄膜

- 钙钛矿太阳能电池

- 多节点

- 有机光伏(OPV)

第六章:市场估算与预测:依材料类型划分,2021-2034年

- 主要趋势

- 硅(Si)

- 铜铟镓硒化物

- 碲化镉(CdTe)

- 钙钛矿化合物

- 透明导电氧化物

- 聚合物基材

第七章:市场估算与预测:依整合类型划分,2021-2034年

- 主要趋势

- 车辆整合光伏技术

- 车辆应用光伏技术

- 玻璃整合光伏

- 车身面板嵌入式光电系统

第八章:市场估算与预测:依车辆类型划分,2021-2034年

- 主要趋势

- 搭乘用车

- 商用车辆

- 电动车

- 两轮/三轮车

第九章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 牵引力补充

- 电池充电

- 暖通空调

- 车载资讯系统

- 能量收集

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧

- 葡萄牙

- 克罗埃西亚

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 新加坡

- 泰国

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

- 土耳其

第十一章:公司简介

- 全球参与者

- Toyota

- Hyundai

- Lightyear

- BMW Group

- Mercedes-Benz

- Audi AG

- Nissan Motor

- BYD Company

- Tesla

- Suno

- Aptera

- Goford

- 区域玩家

- Panasonic

- Sharp

- SunPower

- Hanwha Q CELLS

- First Solar

- Canadian Solar

- JinkoSolar Holding

- LONGi Solar

- 新兴参与者

- Ubiquitous Energy

- Heliatek

- Oxford Photovoltaics

- Saule Technologies

- Solarmer Energy

- Armor

- Infinite Power Solutions

The Global Vehicle-Integrated Solar Cell Semiconductors Market was valued at USD 110.7 million in 2024 and is estimated to grow at a CAGR of 11.8% to reach USD 378.5 million by 2034.

Market growth is fueled by the acceleration of electric vehicle adoption, ongoing advances in semiconductor technology, and increasing demand for energy-efficient and secure power solutions. This momentum is largely influenced by the convergence of smart mobility innovations, enhanced vehicle electronics, and shifting competitive dynamics within the automotive semiconductor ecosystem. Post-pandemic emphasis on chip localization and supply chain resilience has also contributed to this growth, particularly across Asia and Europe. These regions are becoming hotspots for advanced semiconductor manufacturing, supported by rising investments in electrified transportation and digital infrastructure.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $110.7 Million |

| Forecast Value | $378.5 Million |

| CAGR | 11.8% |

Global vehicle electrification and the demand for in-vehicle energy efficiency are pushing automakers and Tier-1 suppliers to invest in chip-level integration, where solar cells work seamlessly with smart inverters, zonal controllers, and advanced power management ICs. These components are now being developed to operate directly with photovoltaic modules, enabling greater energy efficiency and more compact system designs. As vehicles evolve into intelligent, connected systems, innovations in semiconductor networking and architecture are becoming crucial in supporting this transformation.

In terms of materials, the silicon segment held a 45% share in 2024 and is forecasted to grow at a 12% CAGR through 2034. Silicon's dominance is backed by its high reliability, mature supply chains, and performance in diverse lighting conditions. At the same time, copper indium gallium selenide (CIGS) is seeing rising adoption due to its flexibility and suitability for curved vehicle surfaces.

The monocrystalline silicon segment accounted for a 31% share in 2024 and is expected to grow at a CAGR of 12.6% during 2025-2034. Its consistent power delivery and durability make it ideal for body-integrated and rooftop solar panels in EVs and hybrid models.

Asia-Pacific Vehicle-Integrated Solar Cell Semiconductors Market held 42.3% share in 2024, driven by strong progress in automotive and electronics manufacturing. Meanwhile, Europe is emerging as the fastest-growing region due to stringent safety regulations, rapid EV integration, and increasing fusion of solar technology with semiconductor logic to create efficient, vehicle-ready energy solutions.

Key players shaping the Global Vehicle-Integrated Solar Cell Semiconductors Market include Tesla, BYD, Aptera, Toyota, Go Ford, Lightyear, PlanetSolar, Hyundai, and Sono Motors. These companies are actively contributing to the evolution of smart, energy-producing vehicles by integrating next-gen semiconductors with solar technologies. Leading companies in the Vehicle-Integrated Solar Cell Semiconductors Market are leveraging a mix of innovation, collaboration, and vertical integration to expand their market presence. Many are investing heavily in R&D to develop semiconductors that enable high-efficiency energy conversion and seamless integration with solar cells. Strategic partnerships with automakers and Tier-1 suppliers are facilitating the co-development of energy management systems that optimize solar energy usage in EVs.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Semiconductor

- 2.2.3 Material Type

- 2.2.4 Integration Type

- 2.2.5 Vehicle

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Rising adoption of electric and hybrid vehicles

- 3.2.1.3 Advancements in solar semiconductor efficiency

- 3.2.1.4 Government incentives for green mobility and energy-efficient vehicles

- 3.2.1.5 Shift toward energy-autonomous and smart vehicles

- 3.2.1.6 Growing consumer demand for sustainable and premium vehicle designs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Durability and reliability under harsh automotive conditions

- 3.2.2.2 High manufacturing and integration costs

- 3.2.3 Market opportunities

- 3.2.3.1 Rising investments in perovskite and tandem semiconductor R&D

- 3.2.3.2 Integration with EV and hybrid platforms for range extension

- 3.2.3.3 Expansion into two- and three-wheeler markets

- 3.2.3.4 Emergence of transparent and glass-integrated PV systems

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Regional solar integration regulations

- 3.4.2 International standards harmonization

- 3.4.3 Environmental Regulation Impact

- 3.4.4 Import/Export Restrictions

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Patent analysis

- 3.9 Cost breakdown analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly Initiatives

- 3.11 Carbon footprint considerations

- 3.12 Future outlook and roadmap

- 3.12.1 Sustainable energy solutions

- 3.12.2 Cross-industry convergence trends

- 3.12.3 Regulatory evolution and standards development

- 3.12.4 Market consolidation and partnership strategies

- 3.13 Automotive-Grade Solar Semiconductor Supply Chain

- 3.13.1 Automotive qualification requirements

- 3.13.2 Long-term supply assurance strategies

- 3.13.3 Quality management system requirements

- 3.13.4 Supply chain risk mitigation

- 3.13.5 Geopolitical impact on solar supply

- 3.14 Cost-Effectiveness vs Energy Generation Optimization

- 3.1.1 Solar cell cost per watt analysis

- 3.14.2 Installation & integration cost factors

- 3.14.3 Energy payback time calculations

- 3.14.4 Total cost of ownership models

- 3.14.5 Performance vs price trade-off analysis

- 3.15 Automotive Safety Standards & Solar Integration

- 3.15.1 Electrical safety requirements (iso 6469)

- 3.15.2 Fire safety & thermal runaway prevention

- 3.15.3 Crash safety & solar panel behavior

- 3.15.4 High voltage system integration safety

- 3.15.5 Emergency response procedures

- 3.16 Next-Generation Solar Technology Evolution

- 3.16.1 Perovskite solar cell development

- 3.16.2 Organic photovoltaic advancement

- 3.16.3 Transparent solar cell innovation

- 3.16.4 Flexible solar film evolution

- 3.16.5 Multi-junction cell integration

- 3.16.6 Concentrated photovoltaic applications

- 3.17 Energy Management & Vehicle System Integration

- 3.17.1 Solar energy harvesting optimization

- 3.17.2 Battery management system integration

- 3.17.3 Power electronics & conversion efficiency

- 3.17.4 Energy storage strategy optimization

- 3.17.5 Load management & prioritization

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Semiconductor, 2021 - 2034 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Monocrystalline Silicon

- 5.3 Polycrystalline Silicon

- 5.4 Thin-Film

- 5.5 Perovskite Solar Cells

- 5.6 Multi-Junction

- 5.7 Organic Photovoltaics (OPV)

Chapter 6 Market Estimates & Forecast, By Material Type, 2021 - 2034 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Silicon (Si)

- 6.3 Copper Indium Gallium Selenide

- 6.4 Cadmium Telluride (CdTe)

- 6.5 Perovskite compounds

- 6.6 Transparent conductive oxides

- 6.7 Polymer substrates

Chapter 7 Market Estimates & Forecast, By Integration Type, 2021 - 2034 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Vehicle-Integrated Photovoltaics

- 7.3 Vehicle-Applied Photovoltaics

- 7.4 Glass-Integrated PV

- 7.5 Body Panel-Embedded PV

Chapter 8 Market Estimates & Forecast, By Vehicle Type, 2021 - 2034 (USD Mn, Units)

- 8.1 Key trends

- 8.2 Passenger Cars

- 8.3 Commercial Vehicles

- 8.4 Electric Vehicles

- 8.5 Two/Three-Wheelers

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Traction Power Supplement

- 9.3 Battery Charging

- 9.4 HVAC

- 9.5 Telematics

- 9.6 Energy Harvesting

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Portugal

- 10.3.9 Croatia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Toyota

- 11.1.2 Hyundai

- 11.1.3 Lightyear

- 11.1.4 BMW Group

- 11.1.5 Mercedes-Benz

- 11.1.6 Audi AG

- 11.1.7 Nissan Motor

- 11.1.8 BYD Company

- 11.1.9 Tesla

- 11.1.10 Suno

- 11.1.11 Aptera

- 11.1.12 Goford

- 11.2 Regional Players

- 11.2.1 Panasonic

- 11.2.2 Sharp

- 11.2.3 SunPower

- 11.2.4 Hanwha Q CELLS

- 11.2.5 First Solar

- 11.2.6 Canadian Solar

- 11.2.7 JinkoSolar Holding

- 11.2.8 LONGi Solar

- 11.3 Emerging Players

- 11.3.1 Ubiquitous Energy

- 11.3.2 Heliatek

- 11.3.3 Oxford Photovoltaics

- 11.3.4 Saule Technologies

- 11.3.5 Solarmer Energy

- 11.3.6 Armor

- 11.3.7 Infinite Power Solutions

透明太阳能板市场:按材料类型、应用和终端用户产业划分-2026-2032年全球预测

透明太阳能板市场:按材料类型、应用和终端用户产业划分-2026-2032年全球预测 太阳能板市场 - 全球产业规模、份额、趋势、机会及预测(按技术、组件类型、并联型、应用、地区和竞争格局划分,2021-2031年)碲化镉太阳能板市场-全球产业规模、份额、趋势、竞争格局、机会及预测:按应用、材料、地区及竞争格局划分,2021-2031年太阳能建筑幕墙覆层系统市场依产品类型、材料类型、最终用户、应用和安装方式划分,全球预测(2026-2032年)太阳能板刮削市场按技术、应用、安装类型和系统类型划分-2026-2032年全球预测太阳能灌封板市场按类型、应用和最终用户划分 - 全球预测 2026-2032彩色太阳能板市场:按技术、安装方式、功率、应用、最终用户和销售管道划分-2026-2032年全球预测彩色太阳能板市场:按技术、颜色、安装类型、应用、最终用户和销售管道,全球预测,2026-2032年铝框太阳能板市场按产品类型、安装方式、安装方法和应用领域划分-全球预测,2026-2032年PERC太阳能板市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、安装方式、地区和竞争格局划分,2021-2031年预测)

太阳能板市场 - 全球产业规模、份额、趋势、机会及预测(按技术、组件类型、并联型、应用、地区和竞争格局划分,2021-2031年)碲化镉太阳能板市场-全球产业规模、份额、趋势、竞争格局、机会及预测:按应用、材料、地区及竞争格局划分,2021-2031年太阳能建筑幕墙覆层系统市场依产品类型、材料类型、最终用户、应用和安装方式划分,全球预测(2026-2032年)太阳能板刮削市场按技术、应用、安装类型和系统类型划分-2026-2032年全球预测太阳能灌封板市场按类型、应用和最终用户划分 - 全球预测 2026-2032彩色太阳能板市场:按技术、安装方式、功率、应用、最终用户和销售管道划分-2026-2032年全球预测彩色太阳能板市场:按技术、颜色、安装类型、应用、最终用户和销售管道,全球预测,2026-2032年铝框太阳能板市场按产品类型、安装方式、安装方法和应用领域划分-全球预测,2026-2032年PERC太阳能板市场-全球产业规模、份额、趋势、机会和预测(按类型、应用、安装方式、地区和竞争格局划分,2021-2031年预测)