|

市场调查报告书

商品编码

1858862

汽车玻璃用电致变色材料市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Electrochromic Materials for Automotive Glass Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

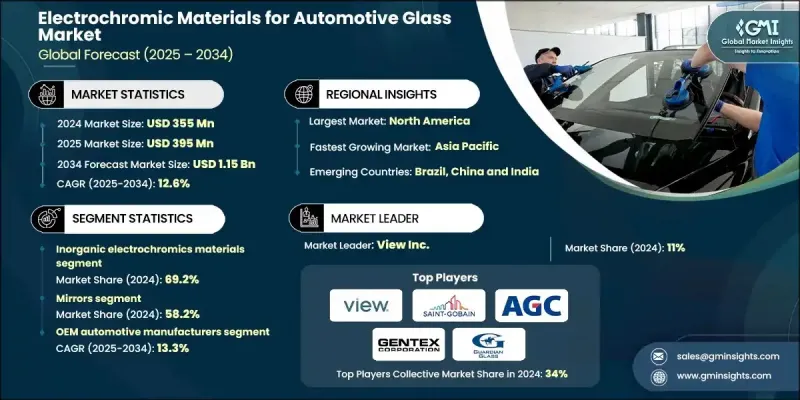

2024 年全球汽车玻璃用电致变色材料市场价值为 3.55 亿美元,预计到 2034 年将以 12.6% 的复合年增长率增长至 11.5 亿美元。

随着汽车製造商日益重视智慧、节能和以使用者为中心的技术,市场正经历变革。电致变色材料能够动态控制光线和热量的传输,透过减少眩光和调节车内温度,直接提升乘客的舒适度。这些材料有助于实现环保目标,减少空调的使用,从而提高传统汽车的燃油效率,并延长电动车的续航里程。随着永续发展成为汽车策略的重要组成部分,电致变色玻璃的应用也日益普及。北美目前引领全球市场,这得益于其成熟的汽车创新环境、强劲的电动车和豪华车市场,以及整车製造商与材料科学公司之间的积极合作。该地区良好的研发环境使其成为智慧玻璃整合领域的中心。亚太地区紧随其后,其发展动力来自不断增长的城市化进程、收入水平的提高以及对电动出行解决方案需求的急剧增长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3.55亿美元 |

| 预测值 | 11.5亿美元 |

| 复合年增长率 | 12.6% |

2024年,无机电致变色材料占据了69.2%的市场份额,预计到2034年将以11%的复合年增长率成长。这些金属氧化物基材因其优异的耐久性和视觉稳定性而备受青睐。其卓越的性能使其成为全景天窗和侧窗等大型汽车表面的理想选择。製造商正致力于提高开关速度并降低功耗,以满足混合动力汽车和电动车的能源效率需求。

2024年,后视镜市占率达到58.2%,预计到2034年将以9.7%的复合年增长率成长。后视镜和侧视镜凭藉其成本效益、成熟的市场应用和稳定的性能,继续保持领先地位。这些零件目前已成为众多中高阶车型的标配,能够提升驾驶者的视野并自动减少眩光。

2024年,北美汽车玻璃用电致变色材料市占率达36.1%。该地区受益于消费者对智慧节能汽车功能的强劲需求。北美汽车製造商已积极将电致变色玻璃应用于其车辆平台,整合先进技术,以满足现代汽车在舒适性、效率和设计方面的追求。

推动全球汽车玻璃电致变色材料市场发展的企业包括:NSG集团(Pilkington)、Pleotint LLC、Guardian Glass、Kinestral Technologies、View Inc.、Smart Glass Country、SAGE Electrochromics Inc.、Research Frontiers Inc.、Vitro Architectural Glass、Gentex Corporation、AGC Inc.、Gen-Gobain Inc.、Genmoics ABin 和 AB。这些企业在汽车玻璃电致变色材料市场竞争中,高度重视创新、策略合作和可扩展的生产能力。主要厂商正投资研发新一代材料配方,以期实现更快的切换速度、更长的使用寿命和更低的能耗。汽车製造商与智慧玻璃开发商之间的合作是将这些材料整合到主流汽车平台的关键。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- FMVSS 205 合规性要求

- 电动车市场成长

- 能源效率指令

- 产业陷阱与挑战

- 高昂的製造成本

- 切换速度限制

- 市场机会

- 多区域动态控制系统

- 自动驾驶车辆集成

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 依技术类型

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)

(註:贸易统计仅针对重点国家提供)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依技术类型划分,2021-2034年

- 主要趋势

- 无机电致变色

- 有机电致变色

- 固态电解质

- 奈米晶体系统

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 镜子

- 天窗和全景天窗

- 侧窗

- 挡风玻璃

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- OEM汽车製造商

- 售后市场供应商

- 特种车辆製造商

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- View Inc.

- Saint-Gobain

- AGC Inc.

- Gentex Corporation

- Guardian Glass

- NSG Group (Pilkington)

- Guardian Glass

- Vitro Architectural Glass

- SAGE Electrochromics Inc.

- ChromoGenics AB

- Pleotint LLC

- Smart Glass Country

- Kinestral Technologies

- Research Frontiers Inc.

The Global Electrochromic Materials for Automotive Glass Market was valued at USD 355 million in 2024 and is estimated to grow at a CAGR of 12.6 % to reach USD 1.15 billion by 2034.

The market is undergoing transformation as automakers increasingly prioritize intelligent, energy-efficient, and user-centered technologies. Electrochromic materials offer dynamic control over light and heat transmission, directly enhancing passenger comfort by minimizing glare and regulating interior temperature. These materials support environmental goals by reducing the need for air conditioning, leading to improved fuel efficiency in conventional vehicles and extended battery range in EVs. As sustainability becomes integral to automotive strategy, electrochromic glass is seeing heightened adoption. North America currently leads the global market, driven by a mature automotive innovation landscape, strong electric and luxury vehicle adoption, and active collaboration between OEMs and material science firms. The region's favorable R&D environment makes it a stronghold for smart glass integration. Asia-Pacific follows closely, fueled by growing urban development, rising income levels, and a sharp increase in demand for electric mobility solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $355 Million |

| Forecast Value | $1.15 Billion |

| CAGR | 12.6% |

In 2024, the inorganic electrochromic materials held a 69.2% share and will grow at a CAGR of 11% through 2034. These metal oxide-based materials are favored for their excellent durability and visual stability. Their performance makes them ideal for large automotive surfaces like panoramic roofs and side windows. Manufacturers are working to improve switching speed and lower power consumption to align with the efficiency needs of hybrid and electric vehicles.

The mirrors segment held a 58.2% share in 2024 and is projected to grow at a CAGR of 9.7% through 2034. Rear-view and side mirrors continue to lead due to their cost-effectiveness, mature adoption, and consistent performance. These components are now standard in various mid-tier to premium vehicle models, offering enhanced driver visibility and automatic glare reduction.

North America Electrochromic Materials for Automotive Glass Market held a 36.1% share in 2024. The region benefits from strong consumer interest in smart and energy-saving automotive features. OEMs in North America have actively incorporated electrochromic glass into their vehicle platforms, integrating advanced technologies that align with modern comfort, efficiency, and design goals.

The companies driving the Global Electrochromic Materials for Automotive Glass Market include NSG Group (Pilkington), Pleotint LLC, Guardian Glass, Kinestral Technologies, View Inc., Smart Glass Country, SAGE Electrochromics Inc., Research Frontiers Inc., Vitro Architectural Glass, Gentex Corporation, AGC Inc., Saint-Gobain, and ChromoGenics AB. Companies competing in the Electrochromic Materials for Automotive Glass Market are focusing heavily on innovation, strategic partnerships, and scalable production capabilities. Major players are investing in next-gen material formulations that offer faster switching times, longer life cycles, and reduced energy usage. Collaborations between automakers and smart glass developers are key to integrating these materials into mainstream vehicle platforms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology type

- 2.2.3 Application

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 FMVSS 205 compliance requirements

- 3.2.1.2 Electric vehicle market growth

- 3.2.1.3 Energy efficiency mandates

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High manufacturing costs

- 3.2.2.2 Switching speed limitations

- 3.2.3 Market opportunities

- 3.2.3.1 Multi-zone dynamic control systems

- 3.2.3.2 Autonomous vehicle integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By technology type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Inorganic electrochromics

- 5.3 Organic electrochromics

- 5.4 Solid-state electrolytes

- 5.5 Nanocrystal systems

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Mirrors

- 6.3 Sunroofs & moonroofs

- 6.4 Side windows

- 6.5 Windshields

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 OEM automotive manufacturers

- 7.3 Aftermarket suppliers

- 7.4 Specialty vehicle manufacturers

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 View Inc.

- 9.2 Saint-Gobain

- 9.3 AGC Inc.

- 9.4 Gentex Corporation

- 9.5 Guardian Glass

- 9.6 NSG Group (Pilkington)

- 9.7 Guardian Glass

- 9.8 Vitro Architectural Glass

- 9.9 SAGE Electrochromics Inc.

- 9.10 ChromoGenics AB

- 9.11 Pleotint LLC

- 9.12 Smart Glass Country

- 9.13 Kinestral Technologies

- 9.14 Research Frontiers Inc.

自动防眩后视镜市场 - 全球产业规模、份额、趋势、机会、预测:按车辆类型、应用、功能类型、地区和竞争格局划分,2021-2031年

自动防眩后视镜市场 - 全球产业规模、份额、趋势、机会、预测:按车辆类型、应用、功能类型、地区和竞争格局划分,2021-2031年 SPD智慧调光玻璃市场按技术、通路、应用、最终用途和安装类型划分-2026-2032年全球预测全球自动调光镜市场(按产品类型、应用、车辆类型和销售管道)预测 2025-2032

SPD智慧调光玻璃市场按技术、通路、应用、最终用途和安装类型划分-2026-2032年全球预测全球自动调光镜市场(按产品类型、应用、车辆类型和销售管道)预测 2025-2032 汽车防眩后视镜市场报告(按应用(内后视镜、外后视镜)、车辆类型(乘用车、商用车)、燃料类型(内燃机、混合动力、电动)和地区)2025 年至 2033 年

汽车防眩后视镜市场报告(按应用(内后视镜、外后视镜)、车辆类型(乘用车、商用车)、燃料类型(内燃机、混合动力、电动)和地区)2025 年至 2033 年 2025年全球自动调光镜市场报告

2025年全球自动调光镜市场报告 依车辆类型、应用程式类型、销售管道、地区、机会和预测对全球汽车自动防眩目镜市场进行评估(2018 年至 2032 年)

依车辆类型、应用程式类型、销售管道、地区、机会和预测对全球汽车自动防眩目镜市场进行评估(2018 年至 2032 年) 自动调光镜市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测

自动调光镜市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测