|

市场调查报告书

商品编码

1858964

电梯市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Elevators Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

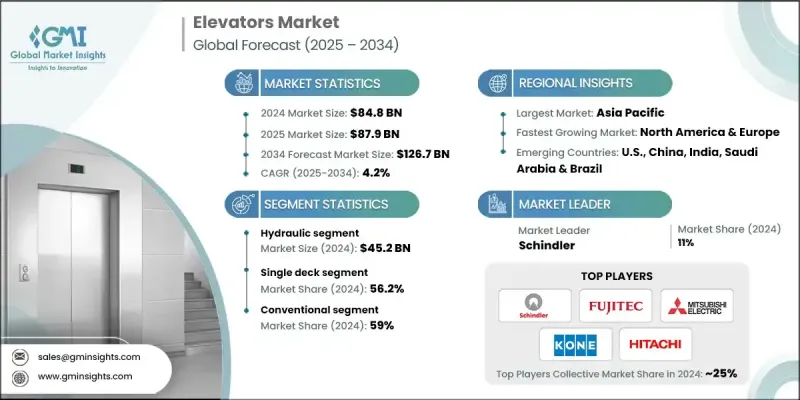

2024年全球电梯市场价值为848亿美元,预计到2034年将以4.2%的复合年增长率增长至1267亿美元。

全球基础建设和城市现代化进程的持续推进,是推动垂直交通市场成长的主要动力。商业和住宅高层建筑对高效垂直交通解决方案的需求日益增长,加速了市场发展。城市发展部门正大力投资智慧城市计画和大型基础设施项目,这些项目通常需要先进的电梯系统。建筑翻新也发挥着重要作用,业主们正在用更新、更智慧的技术升级老旧系统,以符合最新的建筑规范并提升营运效率。整合物联网、人工智慧预测性维护和目的地调度系统的智慧电梯正在塑造垂直交通的未来。这些系统透过自适应演算法、即时监控和现代化介面,提高了安全性、能源效率和使用者舒适度。此外,改造项目也持续推动市场需求,现有建筑正在配备先进的电梯技术,以提升功能并延长使用寿命。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 848亿美元 |

| 预测值 | 1267亿美元 |

| 复合年增长率 | 4.2% |

2024年,液压电梯市场规模达到452亿美元,预计2025年至2034年将以3.4%的复合年增长率成长。其持续受欢迎的原因在于其在中低层建筑的实用性。与曳引式电梯相比,液压电梯系统具有前期成本低、易于整合到紧凑空间以及维护需求更少等优点。近年来,永续液压技术的创新,包括环保液压油和更有效率的机械装置,正在提升其环保性能和运作效率,使其成为太空和预算敏感型专案的首选。

2024年,单层电梯市占率达到56.2%,预计到2034年将以3.9%的复合年增长率成长。其市场主导地位主要归功于单层电梯在住宅、中高层商业建筑和现代化改造项目中的广泛应用。单层电梯设计更简单、价格更实惠、维护更便捷,因此能够很好地适应各种建筑布局。其简便的安装流程和较低的结构要求使其成为新建项目和建筑改造的首选方案。

2024年美国电梯市场规模达130亿美元,预计2025年至2034年将以2.9%的复合年增长率成长。美国市场的主导地位得益于强劲的商业和住宅建设项目,以及旨在实现基础设施现代化改造的翻新项目。绿建筑、智慧城市规划和高楼的持续推进,也带动了对新一代电梯系统的需求。三菱电机、日立、TK电梯、通力电梯和迅达等行业领导企业的存在,以及注重安全和能源效率的有利法规,进一步巩固了美国市场的领先地位。

全球电梯市场的主要参与者包括东芝、现代电梯、TK电梯、三菱电机、富士达、日立、Electra电梯、迅达、Canny电梯、Sigma电梯、Aritco、ESCON电梯、舒马赫电梯、通力(KONE)和EMAK。这些企业透过持续投资研发和整合人工智慧、物联网以及节能组件等先进技术,不断巩固其市场地位。许多製造商正将重心转向开发配备预测性维护系统和数位控制介面的智慧电梯,以提高效能并减少停机时间。与参与基础设施项目的建筑公司、房地产开发商和政府机构建立策略合作伙伴关係,也是扩大市场份额的关键。领导品牌正日益关注改造机会,提供针对现有建筑量身订製的升级解决方案。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 产业影响因素

- 成长驱动因素

- 智慧城市与基础建设发展

- 老旧基础设施的现代化

- 创新技术的发展和对智慧电梯日益增长的需求

- 产业陷阱与挑战

- 高昂的初始投资成本

- 严格的安全法规

- 成长驱动因素

- 成长潜力分析

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 监管环境

- 标准和合规要求

- 区域监理框架

- 认证标准

- 贸易统计

- 主要进口国

- 主要出口国

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品划分,2021-2034年

- 主要趋势

- 油压

- 牵引力

- 无机房牵引

第六章:市场估算与预测:依甲板类型划分,2021-2034年

- 主要趋势

- 单层甲板

- 双层甲板

第七章:市场估算与预测:依建筑高度划分,2021-2034年

- 主要趋势

- 低层

- 中层

- 高层建筑

第八章:市场估算与预测:依速度划分,2021-2034年

- 主要趋势

- 小于1米/秒

- 速度介于 1 公尺/秒至 3 公尺/秒之间

- 速度介于 4 公尺/秒至 6 公尺/秒之间

- 速度介于 7 公尺/秒至 10 公尺/秒之间

- 速度高于 10 公尺/秒

第九章:市场估算与预测:依目的地控制,2021-2034年

- 主要趋势

- 聪明的

- 传统的

第十章:市场估计与预测:依产业划分,2021-2034年

- 主要趋势

- 新设备

- 维护

- 现代化

第十一章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 乘客

- 货运

第十二章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 住宅

- 家用电梯

- 其他的

- 工业的

- 商业的

- 办公室

- 饭店

- 卫生保健

- 其他(购物中心)

第十三章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 印尼

- 马来西亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 沙乌地阿拉伯

- 阿联酋

- 南非

第十四章:公司简介

- Aritco

- Canny Elevator

- Electra Elevators

- EMAK

- ESCON Elevators

- Fujitec

- Hitachi

- Hyundai Elevator

- KONE

- Mitsubishi Electric

- Schindler

- Schumacher Elevator

- Sigma Elevator

- TK Elevator

- Toshiba

The Global Elevators Market was valued at USD 84.8 billion in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 126.7 billion by 2034.

This growth is driven by the expanding development of infrastructure and urban modernization worldwide. The rising demand for efficient vertical mobility solutions in both commercial and residential high-rise buildings is accelerating market growth. Urban development authorities are investing in smart city initiatives and large-scale infrastructure projects, which often require sophisticated elevator systems. Building refurbishments are also contributing significantly, as property owners are upgrading aging systems with newer, smarter technologies to align with updated building codes and improve operational performance. The emergence of smart elevators integrated with IoT, AI-enabled predictive maintenance, and destination dispatch systems is shaping the future of vertical transportation. These systems offer improved safety, energy efficiency, and user comfort through adaptive algorithms, real-time monitoring, and modernized interfaces. The market is also seeing sustained demand from retrofit projects, where existing buildings are being equipped with advanced elevator technologies to boost functionality and extend service life.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $84.8 Billion |

| Forecast Value | $126.7 Billion |

| CAGR | 4.2% |

The hydraulic elevators segment generated USD 45.2 billion in 2024 and is projected to grow at a CAGR of 3.4% from 2025 to 2034. Their continued popularity stems from their practicality in low- to mid-rise buildings. These systems are recognized for their lower upfront costs, ease of integration into compact spaces, and reduced maintenance needs compared to traction elevators. Recent innovations in sustainable hydraulic technology, including eco-friendly fluids and more efficient mechanisms, are improving environmental compliance and operational performance, making them a preferred choice in space-conscious and budget-sensitive projects.

The single-deck segment held a 56.2% share in 2024 and is anticipated to grow at a CAGR of 3.9% through 2034. This dominance is attributed to its widespread use in residential, mid-rise commercial buildings, and modernization projects. Single-deck elevators are simpler in design, more affordable, and easier to maintain, making them highly compatible with a broad range of architectural layouts. Their uncomplicated installation process and lower structural requirements have made them a preferred solution for both new developments and building retrofits.

United States Elevators Market generated USD 13 billion in 2024 and is forecasted to grow at a CAGR of 2.9% from 2025 to 2034. The country's dominance is fueled by a strong pipeline of commercial and residential construction, along with renovation projects aimed at modernizing outdated infrastructure. Ongoing efforts in green building, smart urban planning, and high-rise expansion are increasing the demand for next-generation elevator systems. The presence of industry leaders such as Mitsubishi Electric, Hitachi, TK Elevator, KONE, and Schindler, coupled with favorable regulations focused on safety and energy efficiency, reinforces the U.S. market's leadership position.

Key players in the Global Elevators Market include Toshiba, Hyundai Elevator, TK Elevator, Mitsubishi Electric, Fujitec, Hitachi, Electra Elevators, Schindler, Canny Elevator, Sigma Elevator, Aritco, ESCON Elevators, Schumacher Elevator, KONE, and EMAK. Companies operating in the global elevators market are strengthening their position through continuous investment in R&D and integration of advanced technologies like AI, IoT, and energy-efficient components. Many manufacturers are shifting focus toward developing smart elevators equipped with predictive maintenance systems and digital control interfaces to enhance performance and reduce downtime. Strategic partnerships with construction firms, real estate developers, and government agencies involved in infrastructure projects are also key to expanding market share. Leading brands are increasingly focusing on retrofit opportunities, offering upgrade solutions tailored to existing buildings.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Deck type

- 2.2.4 Building height

- 2.2.5 Speed

- 2.2.6 Destination control

- 2.2.7 Business

- 2.2.8 Application

- 2.2.9 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Smart cities & infrastructure development

- 3.2.1.2 Modernization of aging infrastructure

- 3.2.1.3 Development of innovative technologies and rising demand for smart elevators

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial investment costs

- 3.2.2.2 Stringent safety regulations

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Trade statistics

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Hydraulic

- 5.3 Traction

- 5.4 Machine room-less traction

Chapter 6 Market Estimates & Forecast, By Deck Type, 2021 - 2034, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Single deck

- 6.3 Double deck

Chapter 7 Market Estimates & Forecast, By Building Height, 2021 - 2034, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low-rise

- 7.3 Mid-rise

- 7.4 High-rise

Chapter 8 Market Estimates & Forecast, By Speed, 2021 - 2034, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Less than 1m/s

- 8.3 Between 1 m/s to 3 m/s

- 8.4 Between 4 m/s to 6 m/s

- 8.5 Between 7 m/s to 10 m/s

- 8.6 Above 10 m/s

Chapter 9 Market Estimates & Forecast, By Destination Control, 2021 - 2034, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Smart

- 9.3 Conventional

Chapter 10 Market Estimates & Forecast, By Business, 2021 - 2034, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 New equipment

- 10.3 Maintenance

- 10.4 Modernization

Chapter 11 Market Estimates & Forecast, By Application, 2021 - 2034, (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 Passenger

- 11.3 Freight

Chapter 12 Market Estimates & Forecast, By End Use, 2021 - 2034, (USD Billion) (Thousand Units)

- 12.1 Key trends

- 12.2 Residential

- 12.2.1 Home lifts

- 12.2.2 Others

- 12.3 Industrial

- 12.4 Commercial

- 12.4.1 Office

- 12.4.2 Hotels

- 12.4.3 Healthcare

- 12.4.4 Others (Shopping malls)

Chapter 13 Market Estimates & Forecast, By Region, 2021 - 2034, (USD Billion) (Thousand Units)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 U.S.

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 Australia

- 13.4.6 Indonesia

- 13.4.7 Malaysia

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.6 MEA

- 13.6.1 Saudi Arabia

- 13.6.2 UAE

- 13.6.3 South Africa

Chapter 14 Company Profiles

- 14.1 Aritco

- 14.2 Canny Elevator

- 14.3 Electra Elevators

- 14.4 EMAK

- 14.5 ESCON Elevators

- 14.6 Fujitec

- 14.7 Hitachi

- 14.8 Hyundai Elevator

- 14.9 KONE

- 14.10 Mitsubishi Electric

- 14.11 Schindler

- 14.12 Schumacher Elevator

- 14.13 Sigma Elevator

- 14.14 TK Elevator

- 14.15 Toshiba

2026年全球电梯现代化市场报告

2026年全球电梯现代化市场报告 电梯现代化改造市场:按现代化改造类型、电梯类型、服务、最终用户和服务供应商划分-2026-2032年全球市场预测Z型电梯市场:按电梯类型、安装类型、产品类型、驱动系统、技术和最终用户分類的全球预测,2026-2032年小型机房搭乘用电梯市场:依安装类型、产品类型、速度范围、行程高度、门配置和最终用户产业划分,全球预测,2026-2032年电梯井道零件市场:按零件类型、安装类型、材料、最终用途和分销管道划分-全球预测,2026-2032年电梯本体市场:材料类型、电梯类型、表面处理类型、应用、最终用户划分,全球预测(2026-2032)电梯轿厢零件市场(按零件类型、电梯类型、安装类型和应用划分),全球预测(2026-2032)全球邮轮电梯市场(按电梯类型、服务类型、速度和应用程式划分)-2026-2032年预测

电梯现代化改造市场:按现代化改造类型、电梯类型、服务、最终用户和服务供应商划分-2026-2032年全球市场预测Z型电梯市场:按电梯类型、安装类型、产品类型、驱动系统、技术和最终用户分類的全球预测,2026-2032年小型机房搭乘用电梯市场:依安装类型、产品类型、速度范围、行程高度、门配置和最终用户产业划分,全球预测,2026-2032年电梯井道零件市场:按零件类型、安装类型、材料、最终用途和分销管道划分-全球预测,2026-2032年电梯本体市场:材料类型、电梯类型、表面处理类型、应用、最终用户划分,全球预测(2026-2032)电梯轿厢零件市场(按零件类型、电梯类型、安装类型和应用划分),全球预测(2026-2032)全球邮轮电梯市场(按电梯类型、服务类型、速度和应用程式划分)-2026-2032年预测 全球家用电梯市场规模、份额、趋势和成长分析报告(2026-2034年)全球电梯马达市场规模、份额、趋势和成长分析报告(2026-2034年)

全球家用电梯市场规模、份额、趋势和成长分析报告(2026-2034年)全球电梯马达市场规模、份额、趋势和成长分析报告(2026-2034年)