|

市场调查报告书

商品编码

1871083

生物水泥建筑应用市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Biocement for Construction Application Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

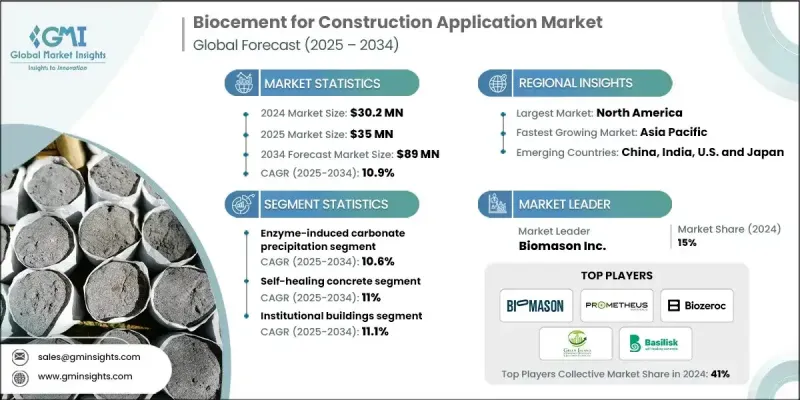

2024 年全球建筑用生物水泥市场价值为 3,020 万美元,预计到 2034 年将以 10.9% 的复合年增长率增长至 8,900 万美元。

全球对永续和环保建筑材料的日益关注正在推动生物水泥市场的快速成长。生物水泥是传统波特兰水泥的更清洁替代品,后者以其高碳排放而闻名。生物水泥透过微生物过程诱导方解石沉淀而生产,为现代建筑需求提供了耐用、低碳的黏结解决方案。该材料卓越的环境效益、更低的能耗和更高的强度特性正在推动其在基础设施、住宅和商业项目中广泛应用。生物基材料和微生物技术的不断进步,使生产更有效率且经济,增强了其与传统水泥的竞争力。全球永续发展倡议和监管要求也在加速生物水泥在大型专案中的应用。不断增长的研发投入正在拓展其在土壤稳定、修復工程和预製构件方面的应用潜力。日益增强的环境保护意识和消费者对绿建筑实践的偏好,持续推动全球建筑业对生物水泥的整体需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3020万美元 |

| 预测值 | 8900万美元 |

| 复合年增长率 | 10.9% |

到了2024年,微生物诱导碳酸盐沉淀(MICP)技术占60%的市场份额。此工艺利用天然存在的细菌沉淀碳酸钙,从而形成强度高、耐久性强的黏结材料,非常适合建筑应用。大量研究验证了MICP技术的商业可行性和环境效益,巩固了其在产业中的领先地位。持续的技术进步以及在混凝土加固和土壤稳定等领域的专门应用开发,预计将在未来几年继续保持其主导地位。

工业和製造设施领域占据29.8%的市场份额,预计到2024年将以10.6%的复合年增长率成长。这些行业的需求主要源于对具有卓越耐久性、耐化学性和自修復性能的建筑材料的需求。生物水泥能够延长使用寿命并最大限度地降低维护成本,使其在极端运行条件下的工业环境中尤为重要。其优异的耐化学腐蚀性和即使在严苛环境下也能保持结构完整性的能力,使其成为工业建筑的关键材料。

2024年,北美建筑用生物水泥市占率达到43.5%,预计到2034年将以11.1%的复合年增长率成长。该地区的成长主要归功于民众强烈的环保意识、政府的永续发展倡议以及对传统水泥生产的严格限制。美国在绿色建筑基础设施和环保建筑标准方面投入巨资,继续保持领先地位;加拿大则透过促进永续城市发展的政策不断扩大市场份额。生物水泥配方的持续创新,以及不断增长的研究活动和製造商之间的合作,预计将进一步加速该地区的市场扩张。

生物水泥建筑应用市场的主要企业包括Carbicrete Inc.、Biozeroc Ltd.、Biomason Inc.、Prometheus Materials Inc.、Green Island International Ltd.和Basilisk BV。这些领导企业正致力于研发创新、策略合作和生产规模化,以提升其市场地位。许多公司正大力投资研发,以提高微生物效率、优化方解石沉淀,并开发更快、更永续的固化製程。生技公司、建筑公司和学术机构之间的合作正在加速产品开发并拓展应用领域。多家公司正努力透过自动化和先进的生物工程技术来扩大生产规模并降低生产成本。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 按产品类别

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依技术类型划分,2021-2034年

- 主要趋势

- 微生物诱导碳酸盐沉淀(MICP)

- 尿素分解细菌系统

- 巴氏芽孢桿菌的应用

- 芽孢桿菌属的实施

- 酵素碳酸盐沉淀(EICP)

- 基于碳酸酐酶的系统

- 二氧化碳捕获酵素系统

- 环境温度下的碳酸化

- 增强二氧化碳封存

- 铁呼吸细菌系统

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 自癒混凝土

- 自主裂缝修復系统

- 胶囊细菌技术

- 长期耐久性增强

- 土壤稳定与地基改良

- 基础加固

- 液化预防

- 侵蚀控制系统

- 基础设施维修与修復

- 裂缝密封应用

- 表面压实

- 结构修復

- 预製建筑构件

- 建筑元素

- 结构部件

- 装饰应用

- 道路和路面应用

- 道路维修与养护

- 除尘系统

- 临时基础设施

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 住宅建筑

- 机构建筑

- 办公大楼

- 学校

- 医院

- 零售设施

- 商业建筑

- 道路

- 桥樑

- 机场

- 其他的

- 工业和製造设施

- 仓库

- 工厂

- 物流中心

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- Biomason Inc.

- Prometheus Materials Inc.

- Biozeroc Ltd.

- Green Island International Ltd.

- Basilisk BV

- Carbicrete Inc.

The Global Biocement for Construction Application Market was valued at USD 30.2 million in 2024 and is estimated to grow at a CAGR of 10.9% to reach USD 89 million by 2034.

The rising global focus on sustainable and eco-friendly construction materials is fueling the rapid growth of this market. Biocement offers a cleaner alternative to traditional Portland cement, which is known for its high carbon emissions. Produced through microbial processes that induce calcite precipitation, biocement provides a durable, low-carbon binding solution for modern construction needs. The material's superior environmental benefits, lower energy consumption, and improved strength characteristics are driving adoption across infrastructure, residential, and commercial projects. Continuous advancements in bio-based materials and microbial technologies are making production more efficient and cost-effective, enhancing competitiveness with conventional cement. Global sustainability initiatives and regulatory mandates are also accelerating biocement's integration into large-scale projects. Growing investment in research and development is expanding its potential for soil stabilization, repair works, and precast components. The increasing awareness of environmental conservation and consumer inclination toward green building practices continue to drive the overall demand for biocement across construction sectors worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $30.2 Million |

| Forecast Value | $89 Million |

| CAGR | 10.9% |

The microbially induced carbonate precipitation (MICP) segment held 60% share in 2024. This process utilizes naturally occurring bacteria to precipitate calcium carbonate, resulting in strong and durable binding properties that are ideal for construction applications. Extensive research validating the commercial and environmental viability of MICP has reinforced its leadership in the industry. Ongoing technological advancements and the development of specialized applications for concrete reinforcement and soil stabilization are expected to sustain its dominance in the coming years.

The industrial and manufacturing facilities segment held 29.8% share, growing at a CAGR of 10.6% in 2024. The demand from these sectors is driven by the need for construction materials with exceptional durability, chemical resistance, and self-healing properties. Biocement's ability to extend service life and minimize maintenance costs makes it particularly valuable in industrial environments that experience extreme operational conditions. Its resistance to chemical degradation and capacity to maintain structural integrity even in demanding settings have positioned it as a key material in industrial construction.

North America Biocement for Construction Application Market held 43.5% share in 2024, with an anticipated CAGR of 11.1% through 2034. The region's growth is largely attributed to strong environmental awareness, government sustainability initiatives, and strict limitations on traditional cement production. The United States remains at the forefront with major investments in green building infrastructure and eco-friendly construction standards, while Canada continues to expand through policies promoting sustainable urban development. Ongoing innovation in biocement formulations, combined with increasing research activity and collaboration among manufacturers, is expected to further accelerate the region's market expansion.

Key companies operating in the Biocement for Construction Application Market include Carbicrete Inc., Biozeroc Ltd., Biomason Inc., Prometheus Materials Inc., Green Island International Ltd., and Basilisk B.V. Leading players in the Biocement for Construction Application Market are employing strategies focused on research innovation, strategic collaborations, and production scalability to enhance their market position. Many companies are investing heavily in R&D to improve microbial efficiency, optimize calcite precipitation, and develop faster, more sustainable curing processes. Partnerships between biotechnology firms, construction companies, and academic institutions are helping accelerate product development and expand application areas. Several firms are working to scale manufacturing capacity and lower production costs through automation and advanced bioengineering techniques.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Technology type

- 2.2.3 Application

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product category

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) ( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Technology Type, 2021-2034 (USD Million & Tons)

- 5.1 Key trends

- 5.2 Microbially induced carbonate precipitation (MICP)

- 5.2.1 Ureolytic bacteria systems

- 5.2.2 Sporosarcina pasteurii applications

- 5.2.3 Bacillus species implementations

- 5.3 Enzyme-induced carbonate precipitation (EICP)

- 5.4 Carbonic anhydrase-based systems

- 5.4.1 Co2-capturing enzyme systems

- 5.4.2 Ambient temperature carbonation

- 5.4.3 Enhanced co2 sequestration

- 5.5 Iron-respiring bacterial systems

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million & Tons)

- 6.1 Key trends

- 6.2 Self-healing concrete

- 6.2.1 Autonomous crack repair systems

- 6.2.2 Encapsulated bacterial technologies

- 6.2.3 Long-term durability enhancement

- 6.3 Soil stabilization & ground improvement

- 6.3.1 Foundation strengthening

- 6.3.2 Liquefaction prevention

- 6.3.3 Erosion control systems

- 6.4 Infrastructure repair & rehabilitation

- 6.4.1 Crack sealing applications

- 6.4.2 Surface consolidation

- 6.4.3 Structural restoration

- 6.5 Precast building components

- 6.5.1 Architectural elements

- 6.5.2 Structural components

- 6.5.3 Decorative applications

- 6.6 Road & pavement applications

- 6.6.1 Road repair & maintenance

- 6.6.2 Dust control systems

- 6.6.3 Temporary infrastructure

Chapter 7 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million & Tons)

- 7.1 Key trends

- 7.2 Residential construction

- 7.3 Institutional buildings

- 7.3.1 Office buildings

- 7.3.2 Schools

- 7.3.3 Hospitals

- 7.3.4 Retail facilities

- 7.4 Commercial structures

- 7.4.1 Roads

- 7.4.2 Bridges

- 7.4.3 Airports

- 7.4.4 Others

- 7.5 Industrial & manufacturing facilities

- 7.5.1 Warehouses

- 7.5.2 Factories

- 7.5.3 Logistic centers

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 (USD Million & Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Biomason Inc.

- 9.2 Prometheus Materials Inc.

- 9.3 Biozeroc Ltd.

- 9.4 Green Island International Ltd.

- 9.5 Basilisk B.V.

- 9.6 Carbicrete Inc.

飞灰市场:依实体形态、分类、燃烧技术、等级、应用和最终用途产业划分-2026-2032年全球市场预测

飞灰市场:依实体形态、分类、燃烧技术、等级、应用和最终用途产业划分-2026-2032年全球市场预测 全球飞灰市场规模、份额、趋势和成长分析报告(2026-2034)

全球飞灰市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球飞灰市场报告

2026年全球飞灰市场报告 飞灰市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、区域及竞争格局划分,2021-2031年)全球飞灰市场规模(按类型、应用、地区、范围和预测)

飞灰市场-全球产业规模、份额、趋势、机会及预测(按类型、应用、区域及竞争格局划分,2021-2031年)全球飞灰市场规模(按类型、应用、地区、范围和预测) 2025-2029年全球飞灰市场

2025-2029年全球飞灰市场 飞灰市场规模、份额、成长分析,按类型、来源、应用、地区 - 产业预测,2024-2031 年

飞灰市场规模、份额、成长分析,按类型、来源、应用、地区 - 产业预测,2024-2031 年 全球飞灰市场规模调查:按类别、应用和地区预测:2022-2032

全球飞灰市场规模调查:按类别、应用和地区预测:2022-2032