|

市场调查报告书

商品编码

1871089

汽车射出成型自动化市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Automotive Injection Molding Automation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

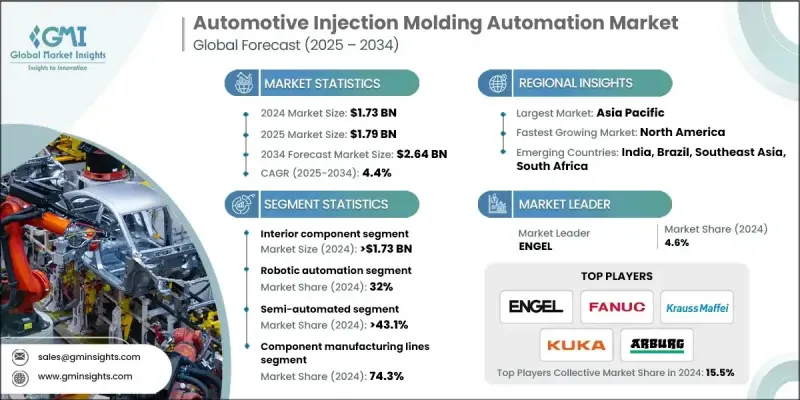

2024 年全球汽车射出成型自动化市场价值为 17.3 亿美元,预计到 2034 年将以 4.4% 的复合年增长率增长至 26.4 亿美元。

製造业自动化程度的不断提高,源自于对更高生产力、更稳定品质和更少人工依赖的需求。机器人搬运、自动化品质检测和整合成型系统正帮助製造商最大限度地减少缺陷、缩短生产週期并提升整个生产过程的效率。这一趋势在全球一级供应商和OEM组装厂中日益明显。电动车(EV)的成长加速了对轻量化、高精度和耐热塑胶零件的需求。自动化注塑成型能够生产具有高重复性和尺寸精度的复杂零件。将人工智慧(AI)、物联网(IoT)和机器学习技术融入成型操作,可实现即时监控、预测性维护和流程最佳化。利用互联自动化单元的智慧工厂正在推动基于数据的决策,减少停机时间并最大限度地减少材料浪费,从而进一步强化了汽车注塑成型製程对自动化的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 17.3亿美元 |

| 预测值 | 26.4亿美元 |

| 复合年增长率 | 4.4% |

2024年,汽车内装组件市场规模达到17.3亿美元,预计2025年至2034年将以5%的复合年增长率成长。随着电动车和先进资讯娱乐系统的普及,市场对轻量化、耐用且精密的内装组件的需求日益增长。自动化生产线能够以高产量、低废品率和稳定的品质生产仪錶板、面板和控制台,从而在提升乘客舒适度的同时降低生产成本。

预计到2024年,机器人自动化领域将占据32%的市场。整合于取放、插件装载和堆迭流程的机器人系统能够提高效率、减少人工干预、增强重复性并缩短週期时间。由于劳动成本压力和对大批量生产的需求,机器人技术在已开发市场和新兴市场的应用都在不断扩展。

2024年,美国汽车射出成型自动化市占率将达86.4%。向电动和混合动力汽车的转型正在推动电池外壳、连接器和电子外壳等零件的自动化应用。自动化可确保重复的精度、尺寸准确性和可重复性,使原始设备製造商 (OEM) 和一级供应商能够在高效生产大批量零件的同时,满足严格的品质标准。

汽车注塑成型自动化市场的主要参与者包括库卡(KUKA)、住友(SHI-Demag)、恩格尔(ENGEL)、海天(Haitian)、阿博格(ARBURG)、发那科(FANUC)、克劳斯玛菲(KraussMaffei)、威特曼巴顿菲尔德(Wittmann BatNUC)、克劳斯玛菲(KraussMaffei)、威特曼巴顿菲尔德(Wittmann Battenfeld)和日精塑胶工业(Nissle)。这些企业正利用创新、技术整合和策略合作来巩固其市场地位。他们投资研发,以改善机器人系统、人工智慧驱动的品质控制和智慧工厂解决方案。与原始设备製造商(OEM)和一级供应商的合作有助于扩大市场覆盖范围,并将解决方案直接整合到生产线中。各公司也专注于模组化自动化系统,以满足多样化的製造需求并提供可扩展的解决方案。数位化和物联网(IoT)的整合改进了製程监控和预测性维护,从而减少了停机时间和营运成本。此外,各公司也重视客户支援、培训计画和售后服务,以增强客户信任。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基准估算和计算

- 基准年计算

- 市场估算的关键趋势

- 初步研究和验证

- 原始资料

- 预报

- 研究假设和局限性

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 原物料供应商

- 零件製造商

- 系统整合商

- OEM

- 最终用途

- 供应商格局

- 产业影响因素

- 成长驱动因素

- 汽车製造自动化程度不断提高

- 电动车和轻量化趋势

- 工业4.0/智慧工厂应用

- 大批量生产需求

- 提高品质和安全标准

- 产业陷阱与挑战

- 高初始资本投入

- 熟练劳动力需求

- 市场机会

- 新兴市场的成长

- 将现有生产线进行自动化改造

- 先进机器人和人工智慧集成

- 对永续和节能係统的需求

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 目前技术

- 新兴技术

- 专利分析

- 价格趋势分析

- 按组件

- 按地区

- 成本細項分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 未来趋势

- 新兴科技趋势

- 电动车影响分析

- 永续发展与回收机会

- 工业4.0演进

- 区域成长热点

- 投资机会

- 风险评估与缓解

- 总拥有成本分析

- 实施时程和专案规划

- 培训和技能发展要求

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 重要新闻和倡议

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 内部组件

- 外部元件

- 其他的

第六章:市场估算与预测:依自动化程度划分,2021-2034年

- 主要趋势

- 机器人自动化

- 製程控制自动化

- 物料搬运自动化

- 品质检测自动化

- 包装及后处理自动化

第七章:市场估算与预测:依自动化程度划分,2021-2034年

- 主要趋势

- 半自动系统

- 全自动系统

- 智慧/工业4.0系统

第八章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 零件生产线

- 精密模具工程

- 二次生产和精加工

第九章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧

- 荷兰

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- 全球参与者

- FANUC

- ENGEL

- KraussMaffei

- ARBURG

- Sumitomo Heavy Industries

- Husky Injection Molding Systems

- Milacron

- 区域玩家

- Star Automation

- Baumuller

- Haitian

- Moog

- Wittmann Battenfeld

- JSW Plastics Machinery

- Toyo Machinery & Metal

- Nissei Plastic Industrial

- 新兴参与者和颠覆者

- JR Automation

- Absolute Haitian

- Sepro

- Yizumi

- Tederic Machinery

- LK Technology

- Specialized Automation Suppliers

- ABB Robotics

- KUKA

- Universal Robots

- Staubli

- Kawasaki Robotics

- Comau

- Denso Robotics

- Epson Robots

- Omron Adept

- Yaskawa Motoman

The Global Automotive Injection Molding Automation Market was valued at USD 1.73 Billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 2.64 Billion by 2034.

The rising adoption of automation in manufacturing is driven by the need for higher productivity, consistent quality, and reduced reliance on manual labor. Robotic handling, automated quality checks, and integrated molding systems are helping manufacturers minimize defects, shorten cycle times, and enhance efficiency throughout production. This trend is increasingly evident among Tier-1 suppliers and OEM assembly plants worldwide. The growth of electric vehicles (EVs) has accelerated demand for lightweight, precise, and heat-resistant plastic components. Automated injection molding enables the production of complex components with high repeatability and dimensional accuracy. Incorporating AI, IoT, and machine learning in molding operations allows real-time monitoring, predictive maintenance, and process optimization. Smart factories leveraging connected automation cells are driving data-based decision-making, reducing downtime, and minimizing material waste, further strengthening demand for automation across automotive injection molding processes.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.73 Billion |

| Forecast Value | $2.64 Billion |

| CAGR | 4.4% |

The interior component segment generated USD 1.73 Billion in 2024 and is expected to grow at a CAGR of 5% from 2025 to 2034. Demand for lightweight, durable, and precise interior components is rising, especially with the growth of EVs and advanced infotainment systems. Automated production lines deliver dashboards, panels, and consoles with high throughput, low scrap rates, and consistent quality, enhancing passenger comfort while reducing production costs.

The robotic automation segment captured a 32% share in 2024. Robotic systems integrated with pick-and-place, insert loading, and stacking processes improve efficiency, reduce human intervention, enhance repeatability, and shorten cycle times. The adoption of robotics is expanding in both developed and emerging markets due to labor cost pressures and the need for high-volume production.

U.S. Automotive Injection Molding Automation Market held 86.4% share in 2024. The shift to electric and hybrid vehicles is driving the use of automation for battery housings, connectors, and electronic enclosures. Automation ensures repeated precision, dimensional accuracy, and repeatability, enabling OEMs and Tier-1 suppliers to meet stringent quality standards while efficiently producing high-volume parts.

Key players in the Automotive Injection Molding Automation Market include KUKA, Sumitomo (SHI-Demag), ENGEL, Haitian, ARBURG, FANUC, KraussMaffei, Wittmann Battenfeld, and Nissei Plastic Industrial. Companies in the Automotive Injection Molding Automation Market are leveraging innovation, technological integration, and strategic partnerships to strengthen their market position. They invest in R&D to enhance robotic systems, AI-driven quality controls, and smart factory solutions. Collaborations with OEMs and Tier-1 suppliers help expand reach and integrate solutions directly into production lines. Firms are also focusing on modular automation systems to cater to diverse manufacturing needs and offer scalable solutions. Digitalization and IoT integration improve process monitoring and predictive maintenance, reducing downtime and operational costs. Additionally, companies emphasize customer support, training programs, and after-sales services to enhance client trust.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Component

- 2.2.2 Automation

- 2.2.3 Level of automation

- 2.2.4 End Use

- 2.2.5 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component manufacturers

- 3.1.1.3 System integrators

- 3.1.1.4 OEM

- 3.1.1.5 End use

- 3.1.1 Supplier landscape

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising automation in automotive manufacturing

- 3.2.1.2 EV and lightweighting trend

- 3.2.1.3 Industry 4.0 / smart factory adoption

- 3.2.1.4 High-volume production needs

- 3.2.1.5 Increasing quality and safety standards

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment

- 3.2.2.2 Skilled workforce requirement

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in emerging markets

- 3.2.3.2 Retrofitting existing lines with automation

- 3.2.3.3 Advanced robotics and AI integration

- 3.2.3.4 Demand for sustainable and energy-efficient systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle east and Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technology

- 3.7.2 Emerging technology

- 3.8 Patent analysis

- 3.9 Price Trends Analysis

- 3.9.1 By component

- 3.9.2 By region

- 3.10 Cost Breakdown Analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable Practices

- 3.11.2 Waste Reduction Strategies

- 3.11.3 Energy Efficiency in Production

- 3.11.4 Eco-friendly Initiatives

- 3.11.5 Carbon Footprint Considerations

- 3.12 Future trends

- 3.12.1 Emerging Technology Trends

- 3.12.2 Electric Vehicle Impact Analysis

- 3.12.3 Sustainability & Recycling Opportunities

- 3.12.4 Industry 4.0 Evolution

- 3.12.5 Regional Growth Hotspots

- 3.12.6 Investment Opportunities

- 3.12.7 Risk Assessment & Mitigation

- 3.13 Total Cost of Ownership Analysis

- 3.14 Implementation Timeline & Project Planning

- 3.15 Training & Skill Development Requirements

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key news and initiatives

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Interior Components

- 5.3 Exterior Components

- 5.4 Others

Chapter 6 Market Estimates & Forecast, By Automation, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Robotic automation

- 6.3 Process control automation

- 6.4 Material handling automation

- 6.5 Quality inspection automation

- 6.6 Packaging & Post-Processing Automation

Chapter 7 Market Estimates & Forecast, By Level of Automation, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Semi-Automated systems

- 7.3 Fully Automated systems

- 7.4 Smart/Industry 4.0-Enabled Systems

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Component Manufacturing Lines

- 8.3 Precision Tooling & Mold Engineering

- 8.4 Secondary Production & Finishing

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 US

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Nordics

- 9.3.7 Netherlands

- 9.3.8 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 FANUC

- 10.1.2 ENGEL

- 10.1.3 KraussMaffei

- 10.1.4 ARBURG

- 10.1.5 Sumitomo Heavy Industries

- 10.1.6 Husky Injection Molding Systems

- 10.1.7 Milacron

- 10.2 Regional Players

- 10.2.1 Star Automation

- 10.2.2 Baumuller

- 10.2.3 Haitian

- 10.2.4 Moog

- 10.2.5 Wittmann Battenfeld

- 10.2.6 JSW Plastics Machinery

- 10.2.7 Toyo Machinery & Metal

- 10.2.8 Nissei Plastic Industrial

- 10.3 Emerging Players and Disruptors

- 10.3.1 JR Automation

- 10.3.2 Absolute Haitian

- 10.3.3 Sepro

- 10.3.4 Yizumi

- 10.3.5 Tederic Machinery

- 10.3.6 LK Technology

- 10.4 Specialized Automation Suppliers

- 10.4.1 ABB Robotics

- 10.4.2 KUKA

- 10.4.3 Universal Robots

- 10.4.4 Staubli

- 10.4.5 Kawasaki Robotics

- 10.4.6 Comau

- 10.4.7 Denso Robotics

- 10.4.8 Epson Robots

- 10.4.9 Omron Adept

- 10.4.10 Yaskawa Motoman

汽车模具市场:2026-2032年全球市场预测(依模具类型、材料类型、自动化类型、车辆类型、应用和销售管道)汽车橡胶模塑件市场:按产品类型、材料、应用和车辆类型划分-2026年至2032年全球预测车载行动气象站市场:依车辆类型、应用领域、最终用户、电源划分,全球预测(2026-2032年)

汽车模具市场:2026-2032年全球市场预测(依模具类型、材料类型、自动化类型、车辆类型、应用和销售管道)汽车橡胶模塑件市场:按产品类型、材料、应用和车辆类型划分-2026年至2032年全球预测车载行动气象站市场:依车辆类型、应用领域、最终用户、电源划分,全球预测(2026-2032年) 汽车模具市场报告:按技术、应用、车辆类型和地区划分(2026-2034 年)橡胶气囊市场:依产品类型、材料类型、应用、终端用户产业和分销管道划分,全球预测,2026-2032年按产品类型、材料、製程、技术、应用和最终用户分類的保险桿模具市场,全球预测,2026-2032年

汽车模具市场报告:按技术、应用、车辆类型和地区划分(2026-2034 年)橡胶气囊市场:依产品类型、材料类型、应用、终端用户产业和分销管道划分,全球预测,2026-2032年按产品类型、材料、製程、技术、应用和最终用户分類的保险桿模具市场,全球预测,2026-2032年 全球轮胎模具市场规模、份额、趋势和成长分析报告(2026-2034年)

全球轮胎模具市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球射出成型汽车零件市场报告全球密封条市场:2026-2032年按类型、材质、应用和通路分類的预测汽车密封条市场按技术、材料、类型、车辆类型和分销管道划分-2026-2032年全球预测

2026年全球射出成型汽车零件市场报告全球密封条市场:2026-2032年按类型、材质、应用和通路分類的预测汽车密封条市场按技术、材料、类型、车辆类型和分销管道划分-2026-2032年全球预测