|

市场调查报告书

商品编码

1871094

钛酸锂(LTO)电池市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Lithium Titanate Oxide (LTO) Battery Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

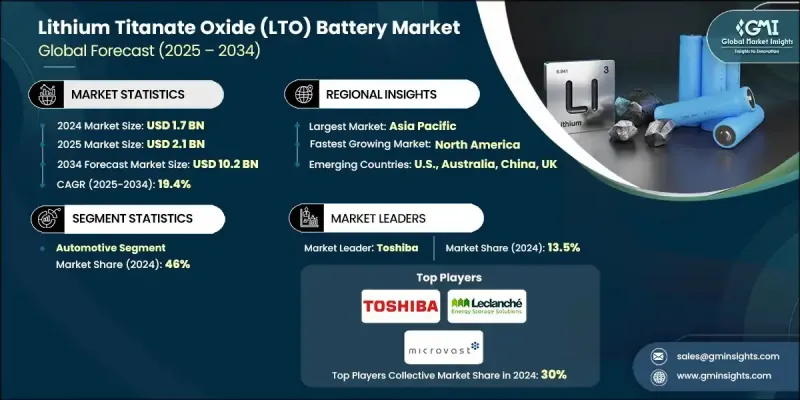

2024 年全球钛酸锂 (LTO) 电池市场价值为 17 亿美元,预计到 2034 年将以 19.4% 的复合年增长率增长至 102 亿美元。

钛酸锂(LTO)电池凭藉其卓越的充电性能和超长的循环寿命,正迅速改变现代能源和交通运输系统。这些电池可在短短几分钟内充电至80%,实现快速充电,最大限度地减少停机时间,优化车队运作。这些优势使其成为电动出行和固定式储能的首选解决方案。世界各国政府都在投资清洁交通和永续能源项目,这直接促进了钛酸锂市场的成长。钛酸锂电池能够实现超过20,000次的完整充放电循环而容量损失极小,这使其在电动交通和储能应用领域都极具优势。钛酸锂电池坚固的尖晶石晶格结构可有效防止枝晶形成,确保更高的可靠性和更长的使用寿命。随着电池即服务(BaaS)模式的日益普及,尤其是在亚太地区,钛酸锂电池的高耐久性和快速充电能力使其成为换电系统以及电动车队和电网应用中其他高需求应用场景的理想选择。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 17亿美元 |

| 预测值 | 102亿美元 |

| 复合年增长率 | 19.4% |

2024年,汽车领域占据46%的市场份额,预计到2034年将以19.5%的复合年增长率成长。该领域的强劲表现主要得益于LTO电池在城市电动出行领域的日益普及,快速充电和延长电池寿命对于日常营运至关重要。与传统的锂离子电池不同,LTO电池可在10分钟内充电至80%,为电动计程车、公车和物流车队等高利用率车辆提供了切实可行的解决方案。随着大都市地区向零排放交通和更严格的环保法规转型,车队营运商正在采用基于LTO电池的电动车,以满足性能和永续性方面的要求。这种向快速充电车辆平台的转变持续推动着该领域在私人和商业出行领域的扩张。

到2034年,美国钛酸锂(LTO)电池市场规模将达到26亿美元。美国大力推动清洁能源转型和电动车普及,并为此推出了一系列联邦计画、拨款和激励措施。支持电动车基础设施扩建、电池製造和智慧电网升级的各项倡议,为LTO电池製造商创造了巨大的发展机会。凭藉其快速充电、长寿命和高安全标准等优势,LTO电池正成为美国公共交通和商用车辆电气化计画的重要组成部分。

全球钛酸锂(LTO)电池市场的主要参与者包括东芝公司、银龙能源、Altairnano、Leclanche SA、Microvast、PLANNANO、Nichicon Corporation 和 Nav Prakriti。为了巩固市场地位,钛酸锂电池产业的企业正积极推行以技术创新、规模化生产和策略合作为核心的策略。许多製造商正投资先进材料科学,以提高电池的能量密度、充电速度和热稳定性。与电动车原始设备製造商(OEM)和能源公司建立战略合作伙伴关係,使企业能够获得长期供应合同,并拓展到储能和换电网络等新兴应用领域。此外,各公司也正在优化其全球供应链,以确保成本效益和及时的产品交付。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 监管环境

- 产业影响因素

- 成长驱动因素

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL 分析

- 技术组件分析

- 投资和融资环境分析

- 新兴科技趋势和发展

第四章:竞争格局

- 介绍

- 公司市占率分析

- 战略仪錶板

- 策略倡议

- 重要伙伴关係与合作

- 主要併购活动

- 产品创新与发布

- 市场扩张策略

- 竞争性标竿分析

- 创新与永续发展格局

第五章:市场规模及预测:依应用领域划分,2021-2034年

- 主要趋势

- 汽车

- 储能

- 工业的

- 其他的

第六章:市场规模及预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 韩国

- 日本

- 澳洲

- 世界其他地区

第七章:公司简介

- Altairnano

- Leclanche SA

- Microvast

- Nav Prakriti

- Nichicon Corporation

- PLANNANO

- Toshiba Corporation

- Yinlong Energy

The Global Lithium Titanate Oxide (LTO) Battery Market was valued at USD 1.7 Billion in 2024 and is estimated to grow at a CAGR of 19.4% to reach USD 10.2 Billion by 2034.

The rapid adoption of LTO batteries is transforming modern energy and mobility systems through their superior charging performance and exceptional cycle life. These batteries can reach up to 80% charge within just a few minutes, enabling quick recharges that minimize downtime and optimize fleet operations. Such advantages make them a preferred solution for electric mobility and stationary storage. Governments across the world are investing in clean transportation and sustainable energy initiatives, directly benefiting the growth of the LTO market. Their unique ability to deliver more than 20,000 full charge-discharge cycles without significant capacity loss enhances their suitability for both electric transport and energy storage applications. The robust spinel lattice structure of LTO batteries prevents dendrite formation, ensuring higher reliability and longer operational lifespan. With growing interest in Battery-as-a-Service (BaaS) models, particularly across Asia-Pacific, LTO's high endurance and rapid charging capabilities make it ideal for battery-swap systems and other high-demand use cases across electric fleets and grid applications.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 Billion |

| Forecast Value | $10.2 Billion |

| CAGR | 19.4% |

The automotive segment held a 46% share in 2024 and is expected to grow at a CAGR of 19.5% through 2034. The segment's strong performance is driven by the increasing use of LTO batteries in urban electric mobility, where fast-charging and extended battery life are critical for daily operations. Unlike conventional lithium-ion chemistries, LTO can achieve 80% charge in under 10 minutes, offering a practical solution for high-utilization vehicles such as electric taxis, buses, and logistics fleets. As metropolitan regions move toward zero-emission transportation and stricter environmental regulations, fleet operators are adopting LTO-based electric vehicles to meet performance and sustainability requirements. This growing shift toward rapid-charging vehicle platforms continues to fuel the segment's expansion across both private and commercial mobility sectors.

U.S. Lithium Titanate Oxide (LTO) Battery Market will reach USD 2.6 Billion by 2034. The country's commitment to clean energy transition and electric mobility adoption is reinforced by large-scale federal programs, grants, and incentives. Initiatives supporting the expansion of electric vehicle infrastructure, battery manufacturing, and smart grid upgrades are creating strong opportunities for LTO battery manufacturers. Given their fast-charging capabilities, extended life cycle, and high safety standards, LTO batteries are emerging as a critical component for public transportation and commercial fleet electrification projects in the United States.

Leading players in the Global Lithium Titanate Oxide (LTO) Battery Market include Toshiba Corporation, Yinlong Energy, Altairnano, Leclanche SA, Microvast, PLANNANO, Nichicon Corporation, and Nav Prakriti. To strengthen their market presence, companies in the lithium titanate oxide battery industry are pursuing strategies centered on technological innovation, production scaling, and strategic collaboration. Many manufacturers are investing in advanced material science to improve battery density, charging speed, and thermal stability. Strategic partnerships with electric vehicle OEMs and energy utilities are enabling companies to secure long-term supply contracts and expand into emerging applications such as energy storage and battery-swapping networks. Firms are also enhancing their global supply chains to ensure cost efficiency and timely product delivery.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Technology component analysis

- 3.8 Investment and funding landscape analysis

- 3.9 Emerging technology trends and developments

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategic dashboard

- 4.4 Strategic initiatives

- 4.4.1 Key partnerships & collaborations

- 4.4.2 Major M&A activities

- 4.4.3 Product innovations & launches

- 4.4.4 Market expansion strategies

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Automotive

- 5.3 Energy storage

- 5.4 Industrial

- 5.5 Others

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.3 Europe

- 6.3.1 UK

- 6.3.2 Germany

- 6.3.3 France

- 6.3.4 Italy

- 6.3.5 Spain

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 South Korea

- 6.4.3 Japan

- 6.4.4 Australia

- 6.5 Rest of World

Chapter 7 Company Profiles

- 7.1 Altairnano

- 7.2 Leclanche SA

- 7.3 Microvast

- 7.4 Nav Prakriti

- 7.5 Nichicon Corporation

- 7.6 PLANNANO

- 7.7 Toshiba Corporation

- 7.8 Yinlong Energy

冠状缝合器市场:按产品类型、操作类型、分销管道和最终用户划分,全球预测,2026-2032年锂电池冠状钉枪市场:按电池容量、价格范围、产品类型、应用、分销管道、最终用户划分,全球预测(2026-2032年)

冠状缝合器市场:按产品类型、操作类型、分销管道和最终用户划分,全球预测,2026-2032年锂电池冠状钉枪市场:按电池容量、价格范围、产品类型、应用、分销管道、最终用户划分,全球预测(2026-2032年) 钛酸锂 (LTO) 电池市场分析及预测(至 2035 年):按类型、产品、应用、技术、组件、最终用户、功能、安装类型、设备和解决方案划分

钛酸锂 (LTO) 电池市场分析及预测(至 2035 年):按类型、产品、应用、技术、组件、最终用户、功能、安装类型、设备和解决方案划分 全球锂电池矿物市场规模、份额、趋势和成长分析报告(2026-2034年)

全球锂电池矿物市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球电池驱动冠状缝合器市场报告2026年全球锂电池冠状钉枪市场报告2026年全球高温电池市场报告低速电动车锂电池组市场:按电池化学成分、车辆类型、电池容量、充电类型、应用和最终用户划分 - 全球预测(2026-2032 年)新型锂电池电解液添加剂市场(依添加剂类型、电池类型、形态、应用和终端用户产业划分)-全球预测(2026-2032年)锂电池旅游车市场(按电池化学成分、车辆类型、电池容量范围、充电技术、马达技术、应用和最终用户划分)—2026-2032年全球预测

2026年全球电池驱动冠状缝合器市场报告2026年全球锂电池冠状钉枪市场报告2026年全球高温电池市场报告低速电动车锂电池组市场:按电池化学成分、车辆类型、电池容量、充电类型、应用和最终用户划分 - 全球预测(2026-2032 年)新型锂电池电解液添加剂市场(依添加剂类型、电池类型、形态、应用和终端用户产业划分)-全球预测(2026-2032年)锂电池旅游车市场(按电池化学成分、车辆类型、电池容量范围、充电技术、马达技术、应用和最终用户划分)—2026-2032年全球预测