|

市场调查报告书

商品编码

1871117

绿色化学市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Green Chemistry Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

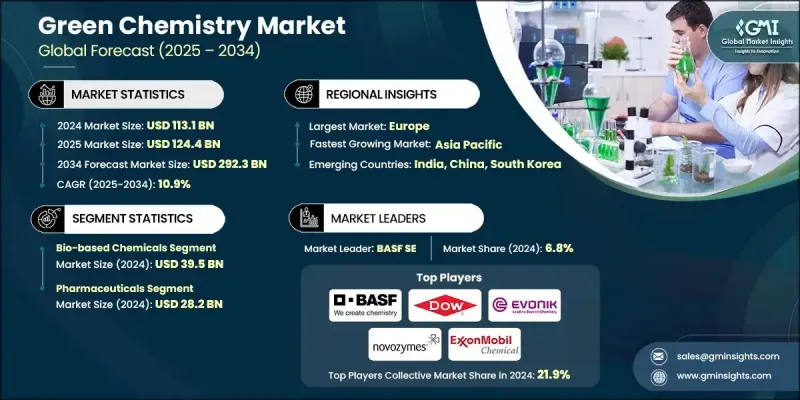

2024年全球绿色化学市场价值为1,131亿美元,预计2034年将以10.9%的复合年增长率成长至2,923亿美元。

绿色化学,通常被称为永续化学,专注于设计能够最大限度地减少或消除有害物质使用和产生的化学产品和製程。它推动了化学合成、废物减量、可再生原料和节能製造领域的进步。该产业在减少环境危害和促进符合全球永续发展目标的清洁生产方面发挥着至关重要的作用。环境法规执行力的加大、消费者对环保产品偏好的日益增长以及企业对永续发展的日益重视,都在推动这一市场的扩张。支持脱碳的国际倡议正在加速向更绿色生产方式的转型。同时,生物基材料和绿色溶剂的快速发展正在改变各行业的工业运作。绿色化学的影响范围远不止于製药业,还包括农业、汽车、包装和个人护理等行业,这些行业的企业正在采用环保催化剂、可再生材料和溶剂替代品。主要经济体的政府正在透过旨在促进负责任的生产和永续工业成长的激励措施和合规框架来强化这一转变。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1131亿美元 |

| 预测值 | 2923亿美元 |

| 复合年增长率 | 10.9% |

2024年,生物基化学品市场规模预计将达395亿美元。生物基化学品的日益普及源于全球对以可再生和可持续替代品取代石油衍生化合物的需求。这些化学品由生物质生产,碳足迹显着降低,并越来越多地应用于製药、消费品和农产品领域。绿色溶剂也因其低毒性和对环境影响小而日益受到青睐,对寻求更安全配方和生产流程的行业极具吸引力。它们在减少废弃物和提高可回收性方面发挥着越来越重要的作用,这进一步巩固了它们在各个应用领域的市场地位。

预计到2024年,製药业市场规模将达282亿美元。製药领域的绿色化学技术能够实现更清洁、更安全的生产流程,而可生物降解和生物基包装材料正日益取代传统塑胶。汽车和建筑业也积极采用永续材料和更环保的生产方式,以降低排放、减少浪费并提高整个供应链的能源效率。这些产业正在向环境友善生产模式转型,以满足监管要求和消费者对永续性的期望。

2024年,美国绿色化学市场规模预计将达270亿美元。北美地区的成长得益于健全的监管框架、丰富的可再生资源以及各行业对永续替代方案的强劲需求。该地区积极的政策支持,例如以环保材料取代有害物质,并将环保投入物整合到生产系统中,进一步加速了绿色转型。加拿大的林业和农业资源正为生物基化学品的生产做出贡献,而墨西哥的工业格局也日益与全球永续发展标准接轨。这些发展反映了北美地区向符合国际ESG目标的环保生产模式转变的趋势。

全球绿色化学市场的主要参与者包括巴斯夫公司(BASF SE)、陶氏公司(Dow Inc.)、杜邦公司(DuPont de Nemours)、嘉吉公司(Cargill Inc.)、三菱化学集团(Mitsubishi Chemical Group)、液化空气集团(Air Liquide)、埃克森美孚化工(ExxonMobil Chemical)、液化空气集团(Air Liquide)、埃克森美孚化工(ExxonMobil Chemical)、液化空气集团(Ebvonde)、埃克森美孚化工(ExxonMobil Chemical)工业工业集团(Cvon 工业公司(Cvon 工业公司Industries)、诺维信公司(Novozymes A/S)、巴斯夫公司(Braskem SA)、Genomatica Inc.、Solugen Inc.、Gevo Inc.、Amyris Inc.和Modern Meadow。为了巩固其在全球绿色化学市场的地位,领先企业正致力于拓展生物基产品组合、开发低碳生产工艺,并与技术创新者建立策略合作关係。许多公司正大力投资研发,以提高永续材料的产量效率并降低生产成本。与农业生产者和再生能源供应商建立合作关係,有助于确保可靠的原料来源,同时确保符合环境法规。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 转向生物基和可再生投入

- 将数位工具整合到绿色製程设计中

- 拓展至非传统领域

- 成长驱动因素

- 产业陷阱与挑战

- 高昂的转型和生产成本

- 再生原料供应和品质不稳定

- 市场机会

- 循环经济和废弃物资源化利用

- 智慧响应材料的开发

- 碳捕获与利用(CCU)技术的整合

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 专利格局

- 贸易统计(HS编码说明:仅提供重点国家的贸易统计)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品类型划分,2021-2034年

- 主要趋势

- 生物基化学品

- 绿色溶剂

- 再生原料

- 绿色聚合物

- 绿色界面活性剂

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 製药

- 包装

- 汽车

- 建造

- 食品和饮料

- 工业化学品

第七章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第八章:公司简介

- BASF SE

- Dow Inc.

- DuPont de Nemours

- Air Liquide

- ExxonMobil Chemical

- Mitsubishi Chemical Group

- Cargill Inc.

- Corbion NV

- Novozymes A/S

- Evonik Industries

- Braskem SA

- Solugen Inc.

- Genomatica Inc.

- Gevo Inc.

- Amyris Inc.

- Modern Meadow

The Global Green Chemistry Market was valued at USD 113.1 Billion in 2024 and is estimated to grow at a CAGR of 10.9% to reach USD 292.3 Billion by 2034.

Green chemistry, often called sustainable chemistry, focuses on designing chemical products and processes that minimize or eliminate the use and generation of hazardous substances. It drives advancements in chemical synthesis, waste reduction, renewable feedstocks, and energy-efficient manufacturing. The industry plays a vital role in reducing environmental harm and promoting cleaner production aligned with global sustainability goals. The increasing enforcement of environmental regulations, heightened consumer preference for eco-friendly products, and a growing emphasis on corporate sustainability are fueling this market's expansion. International initiatives supporting decarbonization are accelerating the transition toward greener production practices. At the same time, rapid developments in bio-based materials and green solvents are transforming industrial operations across sectors. The reach of green chemistry extends well beyond pharmaceuticals to industries such as agriculture, automotive, packaging, and personal care, where companies are adopting eco-friendly catalysts, renewable materials, solvent alternatives. Governments across major economies are reinforcing this shift through incentives and compliance frameworks designed to promote responsible manufacturing and sustainable industrial growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $113.1 Billion |

| Forecast Value | $292.3 Billion |

| CAGR | 10.9% |

The bio-based chemicals segment generated USD 39.5 Billion in 2024. The rising adoption of bio-based chemicals is driven by the global need to replace petroleum-derived compounds with renewable and sustainable alternatives. Produced from biomass, these chemicals carry a significantly smaller carbon footprint and are increasingly used in pharmaceuticals, consumer goods, and agricultural products. Green solvents are also becoming more popular for their low toxicity and reduced environmental impact, making them attractive to industries seeking safer formulations and production processes. Their growing role in minimizing waste and improving recyclability continues to strengthen their market presence across applications.

The pharmaceutical segment reached USD 28.2 Billion in 2024. Green chemistry in pharmaceuticals enables cleaner and safer manufacturing processes, while biodegradable and bio-based packaging materials are increasingly replacing traditional plastics. Automotive and construction industries are also embracing sustainable materials and greener production practices to lower emissions, reduce waste, and enhance energy efficiency throughout their supply chains. These sectors are transitioning toward environmentally responsible manufacturing models that meet both regulatory requirements and consumer expectations for sustainability.

U.S. Green Chemistry Market was valued at USD 27 Billion in 2024. Growth across North America is being driven by robust regulatory frameworks, abundant renewable resources, and strong demand for sustainable alternatives across various industries. The region's green transition is further accelerated by active policy support for the replacement of hazardous substances and the integration of eco-friendly inputs into manufacturing systems. Canada's forestry and agricultural resources are contributing to bio-based chemical production, while Mexico's industrial landscape is increasingly aligned with global sustainability standards. These developments reflect North America's broader movement toward environmentally conscious production aligned with international ESG objectives.

Prominent companies operating in the Global Green Chemistry Market include BASF SE, Dow Inc., DuPont de Nemours, Cargill Inc., Mitsubishi Chemical Group, Air Liquide, ExxonMobil Chemical, Corbion N.V., Evonik Industries, Novozymes A/S, Braskem S.A., Genomatica Inc., Solugen Inc., Gevo Inc., Amyris Inc., and Modern Meadow. To strengthen their position in the global green chemistry market, leading companies are focusing on expanding their bio-based product portfolios, developing low-carbon manufacturing processes, and forming strategic collaborations with technology innovators. Many firms are investing heavily in research and development to improve yield efficiency and reduce production costs of sustainable materials. Partnerships with agricultural producers and renewable energy suppliers help secure reliable feedstock sources while ensuring environmental compliance.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Product Type

- 2.2.2 Application

- 2.2.3 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Shift toward bio-based and renewable inputs

- 3.2.1.2 Integration of digital tools in green process design

- 3.2.1.3 Expansion into non-traditional sectors

- 3.2.1 Growth drivers

- 3.3 Industry pitfalls and challenges

- 3.3.1 High transition and production costs

- 3.3.2 Inconsistent supply and quality of renewable feedstock

- 3.4 Market opportunities

- 3.4.1 Circular economy and waste valorisation

- 3.4.2 Development of smart, responsive materials

- 3.4.3 Integration of carbon capture and utilization (CCU) technologies

- 3.5 Growth potential analysis

- 3.6 Regulatory landscape

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 Middle East & Africa

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Price trends

- 3.10.1 By region

- 3.10.2 By product type

- 3.11 Future market trends

- 3.12 Patent landscape

- 3.13 Trade statistics (HS code Note: the trade statistics will be provided for key countries only)

- 3.13.1 Major importing countries

- 3.13.2 Major exporting countries

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly initiatives

- 3.15 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Bio-based chemicals

- 5.3 Green solvents

- 5.4 Renewable feedstocks

- 5.5 Green polymers

- 5.6 Green surfactants

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Pharmaceuticals

- 6.3 Packaging

- 6.4 Automotive

- 6.5 Construction

- 6.6 Food & beverages

- 6.7 Industrial chemicals

Chapter 7 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Rest of Europe

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.4.6 Rest of Asia Pacific

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.5.4 Rest of Latin America

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

- 7.6.4 Rest of Middle East and Africa

Chapter 8 Company Profiles

- 8.1 BASF SE

- 8.2 Dow Inc.

- 8.3 DuPont de Nemours

- 8.4 Air Liquide

- 8.5 ExxonMobil Chemical

- 8.6 Mitsubishi Chemical Group

- 8.7 Cargill Inc.

- 8.8 Corbion N.V.

- 8.9 Novozymes A/S

- 8.10 Evonik Industries

- 8.11 Braskem S.A.

- 8.12 Solugen Inc.

- 8.13 Genomatica Inc.

- 8.14 Gevo Inc.

- 8.15 Amyris Inc.

- 8.16 Modern Meadow

可再生化学品市场分析及预测(至2035年):依类型、产品类型、技术、应用、材料类型、製程、最终用户、组件及功能划分

可再生化学品市场分析及预测(至2035年):依类型、产品类型、技术、应用、材料类型、製程、最终用户、组件及功能划分 2026年全球可再生化学品市场报告

2026年全球可再生化学品市场报告 全球绿色化学市场预测(至2032年):依产品类型、应用与地区划分全球绿色触媒技术市场预测(至2032年),依催化剂类型、应用、最终用户及地区划分

全球绿色化学市场预测(至2032年):依产品类型、应用与地区划分全球绿色触媒技术市场预测(至2032年),依催化剂类型、应用、最终用户及地区划分 可再生化学品市场规模、份额和成长分析(按产品、原料、应用、最终用户和地区划分)-2026-2033年产业预测

可再生化学品市场规模、份额和成长分析(按产品、原料、应用、最终用户和地区划分)-2026-2033年产业预测 绿色化学用非均相催化剂市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)可再生化学品市场预测至2032年:按产品、原料、技术、应用和地区分類的全球分析

绿色化学用非均相催化剂市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)可再生化学品市场预测至2032年:按产品、原料、技术、应用和地区分類的全球分析 靛氰绿:2025-2031年全球市占率排名、总销售额与需求预测

靛氰绿:2025-2031年全球市占率排名、总销售额与需求预测 可再生化学品市场按产品类型、应用、终端用户产业、原料类型和技术划分-2025-2032年全球预测

可再生化学品市场按产品类型、应用、终端用户产业、原料类型和技术划分-2025-2032年全球预测 绿色化学市场:绿色化学的措施,绿色化学·解决方案供应商的竞争情形,新的大趋势,大型製药公司的配合措施,企业简介,主要的促进因素与阻碍因素

绿色化学市场:绿色化学的措施,绿色化学·解决方案供应商的竞争情形,新的大趋势,大型製药公司的配合措施,企业简介,主要的促进因素与阻碍因素