|

市场调查报告书

商品编码

1871125

电子业氧化锌奈米颗粒市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Zinc Oxide Nanoparticles for Electronics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

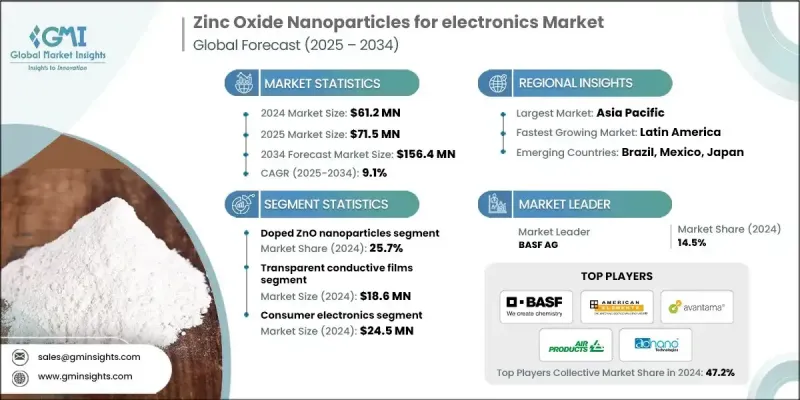

2024 年全球电子用氧化锌奈米粒子市值为 6,120 万美元,预计到 2034 年将以 9.1% 的复合年增长率增长至 1.564 亿美元。

市场扩张的驱动力在于对小型化、高性能电子元件日益增长的需求。氧化锌奈米结构具有卓越的电子迁移率、宽频隙特性以及在可见光范围内的透明性,使其成为先进电子产品(包括透明导电薄膜和高效感测器)的理想选择。其独特的特性,例如高比表面积、紫外线阻隔能力和优异的半导体性能,使其在薄膜电晶体、光电子装置和柔性电子装置中广泛应用。亚太地区凭藉其强大的电子製造生态系统、充足的熟练劳动力和成本优势,继续在生产和消费领域占据主导地位。随着製造商将重心从通用材料转向专用掺杂奈米颗粒、奈米棒和奈米线,以提升装置性能和能源效率,对下一代电子产品和新型奈米结构研究的不断投入和投入的增加,进一步推动了市场成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 6120万美元 |

| 预测值 | 1.564亿美元 |

| 复合年增长率 | 9.1% |

掺杂氧化锌奈米颗粒,连同奈米棒和奈米线,因其优异的电学和光学性能而备受关注,推动了柔性电子装置、再生能源装置和光电感测器等领域的创新。一维氧化锌结构(包括奈米棒和奈米线)占据了20.4%的市场份额,预计在2025年至2034年间将以9.7%的最高复合年增长率成长。其各向异性几何结构提供了更大的表面积和定向电子传输能力,使其在感测器应用中表现出极高的效率。然而,可控比例合成仍然是一个挑战,限制了其产量,同时也推动了持续的研发工作。此外,人们也正在探索诸如超音波辅助分散等先进製造方法来优化材料性能。

2024年,气体感测器市占率达到21.6%,预计到2034年将以8.4%的复合年增长率成长,这主要得益于物联网设备和环境监测系统日益普及。氧化锌奈米颗粒对多种气体高度敏感,某些气体的检测反应时间仅需6-8秒。其自供电特性解决了能源效率问题,使其适用于分散式智慧感测器网路和即时监测应用。

2024年,北美电子用氧化锌奈米颗粒市场规模达1,490万美元。该地区受益于强大的电子製造基础设施、先进的研究机构以及对智慧和可穿戴技术日益增长的需求。透明导电薄膜、紫外线感测器和压电器件等应用引领市场,并得到政府和私营部门的大力支持。科技公司与大学之间的策略合作正在加速商业化进程,并推动创新产品的开发。

全球电子氧化锌奈米颗粒市场的主要企业包括American Elements、MSE Supplies LLC、SAT NANO、Techinstro、巴斯夫股份公司、Noah Chemicals、Shilpa Enterprises、Silox India Pvt Ltd、Avantama AG、AdNano Technologies Pvt Ltd和Ossila Ltd。这些企业正透过大力投资研发来提升氧化锌奈米结构的电学和光学性能,从而巩固其市场地位。他们正透过开发掺杂奈米颗粒、奈米棒和奈米线等产品,丰富其产品组合,以满足柔性电子、感测器和再生能源设备等特殊应用的需求。与大学、研究机构和产业伙伴的策略合作正在加速创新和商业化进程。各企业致力于在维持产品品质的同时扩大生产规模,以满足新兴市场不断增长的需求。强调卓越性能、可靠性和能源效率的行销措施有助于提升品牌知名度并巩固市场地位。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 电子设备小型化

- 对透明导电薄膜的需求日益增长

- 柔性电子技术的进步

- 日益增长的紫外线防护需求

- 产业陷阱与挑战

- 监理合规的复杂性

- 製造规模化挑战

- 健康与安全问题

- 市场机会

- 新兴量子点应用

- 下一代太阳能电池集成

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL 分析

- 价格趋势

- 按地区

- 产品

- 应用

- 最终用户产业

- 未来市场趋势

- 技术与创新格局

- 当前技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品划分,2021-2034年

- 主要趋势

- Zno奈米颗粒(0d)

- 球形奈米颗粒(1-50 nm)

- 球形奈米颗粒(50-100 nm)

- 球形奈米颗粒(100-200 nm)

- ZnO奈米棒/奈米线(1d)

- 短奈米棒(长度<1 μm)

- 长奈米线(长度>1 μm)

- 排列整齐的奈米棒阵列

- 掺杂氧化锌奈米粒子

- 铝掺杂氧化锌(AZO)

- 镓掺杂氧化锌(GZO)

- 掺铟氧化锌(IZO)

- 其他金属掺杂变体

- Zno量子点

- 超小型量子点(<5奈米)

- 中等量子点(5-10奈米)

- Zno奈米复合材料

- ZnO-石墨烯复合材料

- 锌金属杂化结构

- Zno-聚合物奈米复合材料

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 透明导电薄膜

- 显示应用程式

- 触控面板集成

- 太阳能电池电极

- 智慧窗户技术

- 气体感测器

- 环境监测感测器

- 工业製程控制感测器

- 汽车排放感知器

- 室内空气品质感测器

- 光电探测器和紫外线感测器

- 紫外线A波段检测系统

- 紫外线B和紫外线C检测

- 火焰侦测应用

- 光通讯组件

- 薄膜电晶体(TFT)

- 显示背板 TFT

- 柔性电子薄膜电晶体

- 射频TFT

- 太阳能电池组件

- 电子传输层

- 光阳极应用

- 缓衝区集成

- 储存装置

- 阻变式随机存取记忆体(ReRAM)

- 一次写入多次读取 (WORM) 内存

- 神经形态计算应用

第七章:市场估算与预测:依最终用途产业划分,2021-2034年

- 主要趋势

- 半导体製造

- 晶圆加工应用

- 溅镀靶材生产

- 化学气相沉积

- 原子层沉积

- 消费性电子产品

- 智慧型手机和平板电脑集成

- 穿戴式装置应用

- 家用电器电子产品

- 游戏和娱乐系统

- 汽车电子

- 高级驾驶辅助系统(ADA)

- 电动汽车零件

- 资讯娱乐系统

- 引擎控制单元

- 再生能源

- 光电电池製造

- 储能係统

- 智慧电网技术

- 风能电子装置

- 工业电子

- 过程控制系统

- 工厂自动化

- 机器人应用

- 电源管理系统

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- American Elements

- BASF AG

- Air Products and Chemicals Inc

- SAT NANO

- Techinstro

- MSE Supplies LLC

- Noah Chemicals

- Silox India Pvt Ltd

- Shilpa Enterprises

- Avantama AG

- Ossila Ltd

- AdNano Technologies Pvt Ltd

The Global Zinc Oxide Nanoparticles for Electronics Market was valued at USD 61.2 million in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 156.4 million by 2034.

The market expansion is driven by rising demand for miniaturized, high-performance electronic components. Zinc oxide nanostructures exhibit exceptional electron mobility, wide bandgap properties, and transparency in the visible light spectrum, making them ideal for advanced electronics, including transparent conductive films and high-efficiency sensors. Their unique features, such as high surface area, UV-blocking capability, and superior semiconducting behavior, have led to widespread adoption in thin-film transistors, optoelectronics, and flexible electronic devices. Asia Pacific continues to dominate production and consumption due to its robust electronics manufacturing ecosystem, availability of skilled labor, and cost advantages. Increasing investment in next-generation electronics and research into novel nanostructures further fuels growth, as manufacturers shift focus from commodity-grade materials to specialized doped nanoparticles, nanorods, and nanowires to enhance device performance and energy efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $61.2 Million |

| Forecast Value | $156.4 Million |

| CAGR | 9.1% |

Doped zinc oxide nanoparticles, along with nanorods and nanowires, are gaining prominence for their electrical and optical improvements, supporting innovations in flexible electronics, renewable energy devices, and optoelectronic sensors. One-dimensional ZnO structures, including nanorods and nanowires segments, held a 20.4% share and are expected to grow at the highest CAGR of 9.7% from 2025 to 2034. Their anisotropic geometry provides increased surface area and directional electron transport, making them highly effective in sensor applications. However, controlled ratio synthesis remains a challenge, limiting production while driving ongoing research and development efforts. Advanced manufacturing methods, such as ultrasonic-assisted distribution, are also being explored to optimize material performance.

The gas sensors segment held 21.6% share in 2024 and is expected to grow at a CAGR of 8.4% through 2034, driven by increasing adoption of IoT devices and environmental monitoring systems. Zinc oxide nanoparticles are highly sensitive to various gases and provide rapid response times of 6-8 seconds for certain detections. Their self-powered capability addresses energy efficiency concerns, making them suitable for distributed smart sensor networks and real-time monitoring applications.

North America Zinc Oxide Nanoparticles for Electronics Market accounted for USD 14.9 million in 2024. The region benefits from strong electronics manufacturing infrastructure, advanced research institutions, and growing demand for smart and wearable technologies. Applications in transparent conductive films, UV sensors, and piezoelectric devices are leading the market, supported by substantial government funding and private sector investment. Strategic collaborations between technology companies and universities are accelerating commercialization and enabling innovative product development.

Key companies operating in the Global Zinc Oxide Nanoparticles for Electronics Market include American Elements, MSE Supplies LLC, SAT NANO, Techinstro, BASF AG, Noah Chemicals, Shilpa Enterprises, Silox India Pvt Ltd, Avantama AG, AdNano Technologies Pvt Ltd, and Ossila Ltd. Companies in the Global Zinc Oxide Nanoparticles for Electronics Market are adopting strategies to solidify their position by investing heavily in research and development to improve the electrical and optical performance of ZnO nanostructures. They are diversifying their product portfolios with doped nanoparticles, nanorods, and nanowires for specialized applications in flexible electronics, sensors, and renewable energy devices. Strategic collaborations with universities, research institutes, and industrial partners are accelerating innovation and commercialization. Firms are focusing on scaling production while maintaining quality to meet rising demand in emerging markets. Marketing initiatives emphasizing superior performance, reliability, and energy efficiency help enhance brand visibility and strengthen market foothold.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 End Use Industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Miniaturization of electronic devices

- 3.2.1.2 Growing demand for transparent conductive films

- 3.2.1.3 Advancement in flexible electronics

- 3.2.1.4 Increasing uv protection requirement

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Regulatory compliance complexity

- 3.2.2.2 Manufacturing scalability challenges

- 3.2.2.3 Health & safety concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging quantum dot applications

- 3.2.3.2 Next-generation solar cell integration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 Product

- 3.7.3 Application

- 3.7.4 End Use Industry

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Zno nanoparticles (0d)

- 5.2.1 Spherical nanoparticles (1-50 nm)

- 5.2.2 Spherical nanoparticles (50-100 nm)

- 5.2.3 Spherical nanoparticles (100-200 nm)

- 5.3 Zno nanorods/nanowires (1d)

- 5.3.1 Short nanorods (length <1 μm)

- 5.3.2 Long nanowires (length >1 μm)

- 5.3.3 Aligned nanorod arrays

- 5.4 Doped zno nanoparticles

- 5.4.1 Aluminum-doped zno (AZO)

- 5.4.2 Gallium-doped zno (GZO)

- 5.4.3 Indium-doped zno (IZO)

- 5.4.4 Other metal-doped variants

- 5.5 Zno quantum dots

- 5.5.1 Ultra-small quantum dots (<5 nm)

- 5.5.2 Medium quantum dots (5-10 nm)

- 5.6 Zno nanocomposites

- 5.6.1 Zno-graphene composites

- 5.6.2 Zno-metal hybrid structures

- 5.6.3 Zno-polymer nanocomposites

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Transparent conductive films

- 6.2.1 Display applications

- 6.2.2 Touch panel integration

- 6.2.3 Solar cell electrodes

- 6.2.4 Smart window technologies

- 6.3 Gas sensors

- 6.3.1 Environmental monitoring sensors

- 6.3.2 Industrial process control sensors

- 6.3.3 Automotive emission sensors

- 6.3.4 Indoor air quality sensors

- 6.4 Photodetectors & UV sensors

- 6.4.1 UV-a detection systems

- 6.4.2 UV-b & UV-c detection

- 6.4.3 Flame detection applications

- 6.4.4 Optical communication components

- 6.5 Thin Film Transistors (TFTs)

- 6.5.1 Display Backplane TFTs

- 6.5.2 Flexible Electronics TFTs

- 6.5.3 Radio Frequency TFTs

- 6.6 Solar Cell Components

- 6.6.1 Electron Transport Layers

- 6.6.2 Photoanode Applications

- 6.6.3 Buffer Layer Integration

- 6.7 Memory Devices

- 6.7.1 Resistive Random Access Memory (ReRAM)

- 6.7.2 Write-Once Read-Many (WORM) Memory

- 6.7.3 Neuromorphic Computing Applications

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Semiconductor manufacturing

- 7.2.1 Wafer processing applications

- 7.2.2 Sputtering target production

- 7.2.3 Chemical vapor deposition

- 7.2.4 Atomic layer deposition

- 7.3 Consumer electronics

- 7.3.1 Smartphone & tablet integration

- 7.3.2 Wearable device applications

- 7.3.3 Home appliance electronics

- 7.3.4 Gaming & entertainment systems

- 7.4 Automotive electronics

- 7.4.1 Advanced driver assistance systems (adas)

- 7.4.2 Electric vehicle components

- 7.4.3 Infotainment systems

- 7.4.4 Engine control units

- 7.5 Renewable energy

- 7.5.1 Photovoltaic cell manufacturing

- 7.5.2 Energy storage systems

- 7.5.3 Smart grid technologies

- 7.5.4 Wind power electronics

- 7.6 Industrial electronics

- 7.6.1 Process control systems

- 7.6.2 Factory automation

- 7.6.3 Robotics applications

- 7.6.4 Power management systems

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 American Elements

- 9.2 BASF AG

- 9.3 Air Products and Chemicals Inc

- 9.4 SAT NANO

- 9.5 Techinstro

- 9.6 MSE Supplies LLC

- 9.7 Noah Chemicals

- 9.8 Silox India Pvt Ltd

- 9.9 Shilpa Enterprises

- 9.10 Avantama AG

- 9.11 Ossila Ltd

- 9.12 AdNano Technologies Pvt Ltd

氧化锌市场:依形态、通路和应用划分-2026-2032年全球市场预测

氧化锌市场:依形态、通路和应用划分-2026-2032年全球市场预测 全球氧化锌市场(至 2031 年):按製造流程(间接法、直接法和湿化学法)、等级(标准级、加工级、USP 级和 FCC 级)、应用(橡胶、陶瓷、化学品、化妆品和个人护理用品以及药品)和地区划分。

全球氧化锌市场(至 2031 年):按製造流程(间接法、直接法和湿化学法)、等级(标准级、加工级、USP 级和 FCC 级)、应用(橡胶、陶瓷、化学品、化妆品和个人护理用品以及药品)和地区划分。 2026年全球氧化锌市场报告

2026年全球氧化锌市场报告 氧化锌市场-全球产业规模、份额、趋势、机会和预测,按形态、最终用户、地区和竞争格局划分,2020-2030年预测

氧化锌市场-全球产业规模、份额、趋势、机会和预测,按形态、最终用户、地区和竞争格局划分,2020-2030年预测 氧化锌全球市场 - 预测 2025-20302026-2032年氧化锌市场(依等级、应用、最终用途产业及地区)

氧化锌全球市场 - 预测 2025-20302026-2032年氧化锌市场(依等级、应用、最终用途产业及地区) 奈米氧化锌市场报告,按类型(未涂层奈米氧化锌、涂层奈米氧化锌)、应用(个人护理和化妆品、油漆和涂料等)和地区,2025 年至 2033 年

奈米氧化锌市场报告,按类型(未涂层奈米氧化锌、涂层奈米氧化锌)、应用(个人护理和化妆品、油漆和涂料等)和地区,2025 年至 2033 年 全球氧化锌市场需求及预测分析(2018-2034)

全球氧化锌市场需求及预测分析(2018-2034) 氧化锌市场规模、份额、成长分析(按製程、应用、等级和地区)-2025-2032 年产业预测

氧化锌市场规模、份额、成长分析(按製程、应用、等级和地区)-2025-2032 年产业预测 奈米氧化锌市场、机会、成长动力、产业趋势分析与预测,2024-2032

奈米氧化锌市场、机会、成长动力、产业趋势分析与预测,2024-2032