|

市场调查报告书

商品编码

1871227

单孔腹腔镜手术器械市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Single-Port Laparoscopic Surgery Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

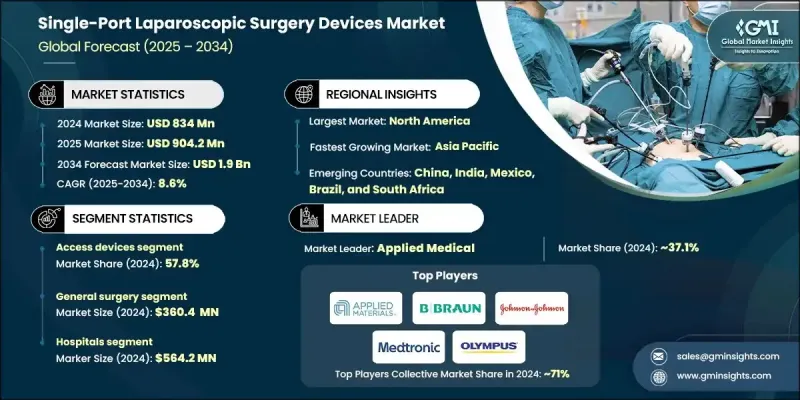

2024 年全球单孔腹腔镜手术器械市场价值为 8.34 亿美元,预计到 2034 年将以 8.6% 的复合年增长率增长至 19 亿美元。

市场成长主要受肥胖症、大肠直肠疾病和妇科疾病发病率上升、患者对微创手术方式的偏好日益增长以及门诊手术数量不断增加等因素驱动。单孔腹腔镜手术(SPLS)设备标誌着微创技术的重大进步,它使外科医生能够透过一个通常位于脐部附近的小切口完成复杂的手术,从而显着减少疤痕、组织损伤和恢復时间。这些设备迅速被寻求疼痛更轻、住院时间更短、恢復更快、美容效果更好的手术方式的医护人员和患者所接受。与传统开放性手术相比,由于切口较小,单孔腹腔镜手术併发症较少,感染风险较低。手术技术的不断发展和单孔平台的人体工学改进持续提升手术的精准度、控制性和效率,从而推动了全球医院和门诊中心的强劲需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 8.34亿美元 |

| 预测值 | 19亿美元 |

| 复合年增长率 | 8.6% |

2024年,腹腔镜器械市占率达42.2%。其成长主要源自于对专用精密器械的需求,这些器械能够支援透过单一切口进行复杂的操作,尤其是在解剖结构受限的手术区域。套管针、剪刀、分离器、抓钳和持针器等器械在确保手术过程中的精准控制和灵活性方面发挥着至关重要的作用。这些器械帮助外科医生剋服了单孔手术中常见的器械拥挤和三角定位受限等挑战。符合人体工学和可弯曲器械设计的进步进一步提升了手术效果,并推动了该细分市场的扩张。

2024年,一般外科手术市场规模达3.604亿美元。其市场主导地位源自于大量适合单孔入路的手术,例如阑尾切除术、疝气修补术和胆囊切除术。随着单孔入路技术在住院和门诊机构的接受度不断提高,该市场持续受益。由于单孔入路手术恢復时间短、疤痕小、整体临床疗效好,患者和医护人员越来越倾向选择单孔入路手术。普通外科手术病例数量的增长以及手术入路系统的不断进步,进一步巩固了该领域对单孔入路手术器械的强劲需求。

2024年,美国单孔腹腔镜手术器械市场规模预计将达3.579亿美元。美国在全球采用先进的单孔腹腔镜系统方面处于领先地位,这主要得益于其优惠的医保政策、高素质的外科医生队伍以及对医疗创新持续不断的投入。该地区大力支持外科培训、开发数位化手术平台以及整合基于模拟的学习,所有这些因素都推动了单孔腹腔镜手术(SPLS)技术在不同专科领域的广泛应用。

全球单孔腹腔镜手术器械市场的主要参与者包括强生、Applied Medical、贝朗、奥林巴斯、美敦力、史多斯、优尼迈、康基、CITEC、LOOKMED、GYTR-VII 和 Hospiinz。为了巩固其在单孔腹腔镜手术器材产业的地位,领导企业正致力于产品创新、建立合作伙伴关係和进行策略性收购,以扩大其全球影响力。许多企业正大力投资研发,以设计先进的手术入路端口、多功能器械平台和灵活的腹腔镜工具,从而提高外科医生的舒适度和手术效率。此外,各公司也正在加强分销网络,并与医院合作,以加速临床应用。同时,他们也透过优化生产流程和在地化生产来提高产品的价格竞争力,并扩大培训项目,以提高外科医生的技能水平,确保各地区市场的持续成长。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 产业影响因素

- 成长驱动因素

- 肥胖、大肠直肠疾病和妇科疾病的盛行率不断上升

- 技术进步

- 人们对微创手术的偏好日益增长

- 门诊手术量激增

- 产业陷阱与挑战

- 腹腔镜设备成本高昂

- 严格的政府法规

- 市场机会

- 医疗基础设施扩建

- 开发灵活、符合人体工学且可重复使用的仪器

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 北美洲

- 欧洲

- 亚太地区

- 2024年定价分析

- 价值链分析

- 未来市场趋势

- 报销方案

- 技术格局

- 目前技术

- 新兴技术

- 差距分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 北美洲

- 欧洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估算与预测:依产品类型划分,2021-2034年

- 主要趋势

- 存取装置

- 腹腔镜器械

第六章:市场估算与预测:依应用领域划分,2021-2034年

- 主要趋势

- 一般外科

- 妇科手术

- 泌尿外科手术

- 减重手术

- 其他应用

第七章:市场估算与预测:依最终用途划分,2021-2034年

- 主要趋势

- 医院

- 门诊手术中心

- 其他最终用途

第八章:市场估算与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Applied Medical

- B. Braun

- CITEC

- GYTR-VII

- Hospiinz

- Johnson & Johnson

- KANGJI

- LOOKMED

- Medtronic

- OLYMPUS

- STORZ

- UNIMAX

The Global Single-Port Laparoscopic Surgery Devices Market was valued at USD 834 million in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 1.9 Billion by 2034.

Market growth is driven by the rising incidence of obesity, colorectal disorders, and gynecological diseases, combined with the growing patient preference for minimally invasive surgical approaches and the increasing number of outpatient procedures. Single-port laparoscopic surgery (SPLS) devices mark a major step forward in minimally invasive techniques, allowing surgeons to perform complex operations through one small incision, typically near the umbilicus, which significantly reduces scarring, tissue trauma, and recovery time. These devices have gained rapid adoption among healthcare professionals and patients seeking procedures with reduced pain, shorter hospital stays, quicker recovery, and better cosmetic results. Compared with traditional open surgeries, single-port laparoscopy offers fewer complications and a lower infection risk due to smaller incisions. The ongoing evolution of surgical technology and ergonomic improvements in single-port platforms continue to enhance precision, control, and procedural efficiency, fueling strong demand in hospitals and ambulatory centers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $834 Million |

| Forecast Value | $1.9 Billion |

| CAGR | 8.6% |

The laparoscopic instruments segment held a 42.2% share in 2024. Its growth is primarily driven by the need for specialized precision tools that support intricate movements through a single incision, particularly in anatomically restricted surgical areas. Instruments such as trocars, scissors, dissectors, graspers, and needle holders play a critical role in ensuring precise control and dexterity during procedures. These devices help surgeons overcome common challenges associated with instrument crowding and limited triangulation, which are typical in single-port techniques. The advancement of ergonomic and articulating instrument designs is further improving surgical performance and driving the segment's expansion.

The general surgery segment generated USD 360.4 million in 2024. Its dominance stems from the high number of procedures suitable for single-port access, including appendectomy, hernia repair, and cholecystectomy. The segment continues to benefit from growing acceptance of single-port methods across both inpatient and outpatient facilities. Patients and providers are increasingly opting for SPLS due to its shorter recovery times, reduced scarring, and better overall clinical outcomes. The rising number of general surgical cases and continuous advancements in surgical access systems further reinforce the strong demand for SPLS devices in this segment.

U.S. Single-Port Laparoscopic Surgery Devices Market generated USD 357.9 million in 2024. The U.S. leads globally in adopting advanced single-port laparoscopic systems, driven by favorable reimbursement policies, the presence of a highly skilled surgical workforce, and consistent investments in healthcare innovation. The region benefits from strong support for surgical training, development of digital surgical platforms, and the integration of simulation-based learning, all of which are propelling the widespread implementation of SPLS technologies across different specialties.

Prominent companies active in the Global Single-Port Laparoscopic Surgery Devices Market include Johnson & Johnson, Applied Medical, B. Braun, Olympus, Medtronic, STORZ, UNIMAX, KANGJI, CITEC, LOOKMED, GYTR-VII, and Hospiinz. To reinforce their position in the single-port laparoscopic surgery devices industry, leading companies are focusing on product innovation, partnerships, and strategic acquisitions to expand their global reach. Many are investing heavily in research and development to design advanced access ports, multi-instrument platforms, and flexible laparoscopic tools that enhance surgeon comfort and efficiency. Firms are also strengthening distribution networks and entering collaborations with hospitals to accelerate clinical adoption. Additionally, they are emphasizing affordability through manufacturing optimization and local production, while expanding their training programs to increase surgeon proficiency and ensure consistent market growth across regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product type trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of obesity, colorectal diseases, and gynecological conditions

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising preference for minimally invasive surgery

- 3.2.1.4 Surge in outpatient surgeries

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High cost of laparoscopic devices

- 3.2.2.2 Stringent government regulations

- 3.2.3 Market opportunities

- 3.2.3.1 Healthcare infrastructure expansion

- 3.2.3.2 Development of flexible, ergonomic, and reusable instruments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.5 Pricing analysis, 2024

- 3.6 Value chain analysis

- 3.7 Future market trends

- 3.8 Reimbursement scenario

- 3.9 Technology landscape

- 3.9.1 Current technologies

- 3.9.2 Emerging technologies

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 North America

- 4.3.2 Europe

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Access devices

- 5.3 Laparoscopic instruments

Chapter 6 Market Estimates and Forecast, By Applications, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 General surgery

- 6.3 Gynecological surgery

- 6.4 Urological surgery

- 6.5 Bariatric surgery

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgery centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Applied Medical

- 9.2 B. Braun

- 9.3 CITEC

- 9.4 GYTR-VII

- 9.5 Hospiinz

- 9.6 Johnson & Johnson

- 9.7 KANGJI

- 9.8 LOOKMED

- 9.9 Medtronic

- 9.10 OLYMPUS

- 9.11 STORZ

- 9.12 UNIMAX

2026年全球机器人内视镜市场报告

2026年全球机器人内视镜市场报告 机器人辅助内视镜市场-全球产业规模、份额、趋势、机会、预测:按最终用户、地区和竞争对手划分,2021-2031年

机器人辅助内视镜市场-全球产业规模、份额、趋势、机会、预测:按最终用户、地区和竞争对手划分,2021-2031年 单切口腹腔镜手术器械市场预测至2032年:按产品类型、应用、最终用户和地区分類的全球分析

单切口腹腔镜手术器械市场预测至2032年:按产品类型、应用、最终用户和地区分類的全球分析 机器人辅助手术系统市场2025年机器人辅助腹腔镜手术全球市场报告

机器人辅助手术系统市场2025年机器人辅助腹腔镜手术全球市场报告 全球腹腔镜机器人手术市场:市场规模、份额和趋势分析(按应用、手术复杂程度、最终用途和地区划分),细分市场预测(2025-2033 年)

全球腹腔镜机器人手术市场:市场规模、份额和趋势分析(按应用、手术复杂程度、最终用途和地区划分),细分市场预测(2025-2033 年) 全球机器人辅助手术系统市场全球机器人内视镜市场2025年影像导引与机器人辅助手术市场报告

全球机器人辅助手术系统市场全球机器人内视镜市场2025年影像导引与机器人辅助手术市场报告 机器人神经外科系统市场:规模、占有率和趋势(2025-2031) - MedCore

机器人神经外科系统市场:规模、占有率和趋势(2025-2031) - MedCore