|

市场调查报告书

商品编码

1871309

软体测试市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)Software Testing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

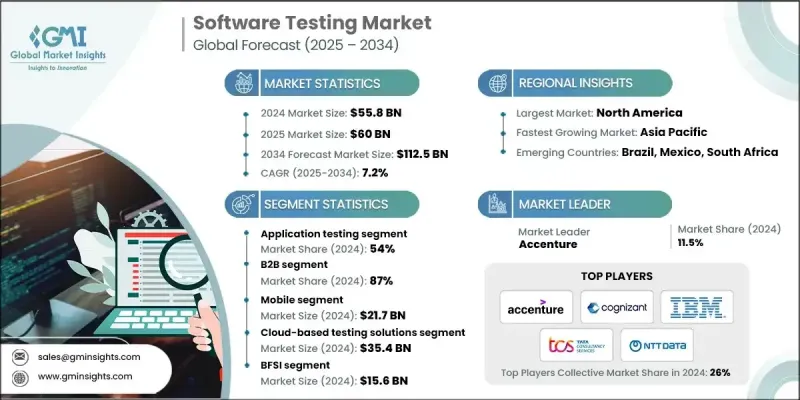

2024 年全球软体测试市场价值为 558 亿美元,预计到 2034 年将以 7.2% 的复合年增长率增长至 1125 亿美元。

敏捷开发、DevOps 和持续整合/持续交付 (CI/CD) 方法的日益普及,以及企业对数位转型措施的日益重视,共同推动了市场的发展。各行各业的组织都将高品质、安全性和可靠性的软体放在首位,从而推动了对先进测试解决方案的需求。人工智慧驱动的自动化、基于云端的测试平台以及低程式码/无程式码框架的持续创新,使企业能够部署智慧、可扩展且经济高效的测试作业。这些进步缩短了产品上市时间,提高了营运效率,并增强了软体品质。在人工智慧驱动的自动化、现代化数位基础设施以及对效能、可靠性和网路安全日益增长的期望的推动下,市场正经历着快速的技术变革。企业正越来越多地将测试解决方案整合到其 DevOps 管线中,以维持无缝营运和卓越的客户体验,同时确保符合不断变化的行业法规。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 558亿美元 |

| 预测值 | 1125亿美元 |

| 复合年增长率 | 7.2% |

软体测试解决方案,包括自动化测试平台、效能和负载测试系统、安全验证框架以及人工智慧驱动的测试管理工具,对于维护软体完整性至关重要。这些解决方案能够实现即时监控、精准缺陷检测和全面的应用验证,同时最大限度地减少人工干预。它们确保测试团队、云端基础设施和DevOps环境之间的无缝协作,从而支援更广泛的企业数位化策略。人工智慧驱动的自动化、云端采用、IT基础设施现代化以及日益严格的品质和安全监管要求正在重塑市场格局。

应用测试领域在2024年占据了54%的市场份额,预计从2025年到2034年将以10.1%的复合年增长率成长。其主导地位源自于其在确保软体在Web、行动和企业平台上的功能、效能、安全性和可靠性方面发挥的关键作用。该领域涵盖功能测试、效能评估、安全验证和使用者体验评估,这些对于软体供应商、IT服务提供者和企业交付高品质应用程式至关重要。

2024年,B2B领域占据87%的市场份额,预计到2034年将以7.4%的复合年增长率成长。这一领先地位的驱动力源于企业对安全、高效能和可靠软体日益增长的需求,这些需求涵盖金融、医疗保健、製造和IT服务等多个行业。企业正在投资全面的测试解决方案,以确保合规性、无缝整合和营运效率,同时提升最终用户满意度。

美国软体测试市场占据88%的市场份额,预计2024年市场规模将达到233亿美元。美国拥有庞大的企业IT部署规模、云端原生和行动应用程式的快速普及,以及严格的网路安全、资料隐私和产业合规监管标准,因此蕴藏着巨大的市场机会。美国成熟的IT生态系统能够协助人工智慧驱动的测试管理系统、持续整合/持续交付(CI/CD)管线以及新一代测试解决方案的快速部署。

全球软体测试市场的主要参与者包括 Tricentis、IBM、Cognizant、Wipro、EPAM Systems、SmartBear Software、Capgemini、TCS、Accenture 和 NTT Data。软体测试市场的企业正采用多种策略来扩大市场份额并巩固自身地位。他们大力投资于人工智慧驱动的测试自动化和云端平台,以提供可扩展、经济高效且智慧化的测试解决方案。各公司正专注于合作、併购,以拓展服务范围和全球影响力。产品创新和研发倡议使他们能够提供满足不断变化的企业需求的尖端解决方案。许多公司强调端到端服务集成,包括 DevOps 协同、CI/CD 支援和安全合规性。策略行销、思想领导力和行业特定解决方案有助于品牌差异化并吸引高价值企业客户,从而提升软体测试市场的竞争力并实现长期成长。

目录

第一章:方法论与范围

第二章:执行概要

第三章:行业洞察

- 产业生态系分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的价值增加

- 影响价值链的因素

- 中断

- 产业影响因素

- 成长驱动因素

- 敏捷和DevOps的日益普及

- 对高品质软体的需求日益增长

- 测试自动化技术进步

- 监管和合规要求

- 产业陷阱与挑战

- 高初始投资

- 与遗留系统的复杂集成

- 市场机会

- 快速发展的技术格局

- 资料安全和隐私问题

- 人工智慧驱动的预测性测试解决方案

- 基于云端和混合的测试服务

- 成长驱动因素

- 成长潜力分析

- 监管环境

- 全球监管环境概述

- 行业特定合规要求

- 资料隐私与保护法规

- 网路安全标准与框架

- 专业认证要求

- 品质标准与认证

- 跨境监管协调

- 波特的分析

- PESTEL 分析

- 技术与创新格局

- 人工智慧与机器学习集成

- 测试自动化演进

- 云端原生测试平台

- 低程式码/无程式码测试解决方案

- 量子计算考试准备

- 区块链测试要求

- 物联网和边缘运算测试

- 扩增实境和虚拟实境测试

- 5G网路测试要求

- 价格趋势

- 区域定价差异

- 按玩家群体分類的定价策略

- 基于服务的定价模式

- 基于价值的定价方法

- 规模经济和数量经济

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 风险评估框架

- 最佳情况

- 客户需求及选择标准分析

- 企业客户端测试要求

- 中小企业测试需求及预算限制

- 供应商选择决策因素

- 投资报酬率预期及衡量框架

- 服务等级协定要求

- 安全与合规要求

- 整合和互通性需求

- 可扩展性和灵活性要求

- 行业特定测试要求

- 合规性测试(PCI-DSS、HIPAA、GDPR的影响)

- 特定领域的复杂性(金融科技、医疗保健、自动驾驶汽车)

- 监管审计准备情况

- 行业基准和最佳实践

- 品质指标与分析框架

- 测试有效性的关键绩效指标(缺陷漏检率、测试投资报酬率、週期时间)

- 数据驱动的品质洞察

- 即时监控和仪錶板

- 预测品质分析

- 与业界标准进行基准化分析

- 客户成功与留存指标

- 实施后支援要求

- 客户满意度趋势

- 流失分析和忠诚度因素

- 价值实现时间表

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 合作伙伴关係与合作

- 新产品发布

- 扩张计划和资金

- 竞争漏洞与威胁

- 关键领域的绩效差距

- 技术债与遗留平台问题

- 客户流失指标与高风险客户群

- 来自新进入者或相邻参与者的新兴威胁

- 服务不足的市场领域

- 客户成败分析

- 竞争对手的交易规模和合约价值

- 对特定竞争对手的胜率

- 竞争性交易中的关键差异化因素

- 客户迁移模式(转换行为)

- 各细分市场的市占率增减情况

- 技术栈与平台能力矩阵

- 主要厂商的AI/ML能力比较

- 云端基础设施偏好和投资

- 测试自动化覆盖率和深度

- 整合生态系统的广度(DevOps、监控、安全工具)

- 专有方法与开源方法

第五章:市场估算与预测:依组件划分,2021-2034年

- 主要趋势

- 应用测试

- 功能

- 系统测试

- 单元测试

- 整合测试

- 烟雾测试

- 回归测试

- 其他的

- 非功能性

- 安全测试

- 性能测试

- 可用性测试

- 其他的

- 功能

- 测试服务

- 专业服务

- 託管服务

第六章:市场估算与预测:依商业模式划分,2021-2034年

- 主要趋势

- B2B

- 企业应用测试

- B2B平台测试

- 整合测试服务

- API 测试解决方案

- B2C

- 消费者应用测试

- 使用者体验测试

- 行动应用测试

- 电子商务测试

第七章:市场估计与预测:依平台划分,2021-2034年

- 主要趋势

- 移动的

- 原生行动应用程式测试

- 跨平台行动测试

- 行动装置测试

- 行动效能测试

- 行动安全测试

- 网路为基础的测试

- Web应用程式测试

- 浏览器相容性测试

- Web效能测试

- 网路安全测试

- 渐进式 Web 应用测试

第八章:市场估算与预测:依部署模式划分,2021-2034年

- 主要趋势

- 基于云端的测试解决方案

- 软体即服务 (SaaS) 测试平台

- 平台即服务 (PaaS) 测试工具

- 基础设施即服务 (IaaS) 测试

- 多云测试策略

- 本地测试解决方案

- 传统测试基础设施

- 企业测试平台

- 专用测试中心

- 混合测试解决方案

- 云端本地集成

- 灵活的部署模式

- 混合测试编排

第九章:市场估计与预测:依应用领域划分,2021-2034年

- 主要趋势

- 它

- 电信

- 金融服务业

- 製造业

- 零售

- 卫生保健

- 运输与物流

- 政府和公共部门

- 消费性电子产品

- 媒体

- 其他的

第十章:市场估计与预测:依地区划分,2021-2034年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比利时

- 荷兰

- 瑞典

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 新加坡

- 韩国

- 越南

- 印尼

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十一章:公司简介

- Global Player

- Accenture

- Atos

- Capgemini

- Cognizant Technology Solutions

- IBM

- Infosys

- NTT Data

- Tata Consultancy Services (TCS)

- Wipro

- Regional Player

- EPAM Systems

- Keysight Technologies

- Micro Focus International

- Parasoft

- Ranorex

- SmartBear Software

- Tech Mahindra

- Tricentis

- Worksoft

- 新兴参与者

- Applitools

- Katalon

- Mabl

- Sauce Labs

- Testim

The Global Software Testing Market was valued at USD 55.8 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 112.5 billion by 2034.

The market is propelled by the growing adoption of Agile, DevOps, and continuous integration/continuous delivery (CI/CD) methodologies, alongside enterprises' increasing focus on digital transformation initiatives. Organizations across industries are prioritizing high-quality, secure, and reliable software, driving demand for advanced testing solutions. Continuous innovations in AI-powered automation, cloud-based testing platforms, and low-code/no-code frameworks are allowing companies to deploy intelligent, scalable, and cost-effective testing operations. These advancements reduce time-to-market, improve operational efficiency, and enhance software quality. The market is witnessing rapid technological evolution, fueled by AI-driven automation, modernized digital infrastructures, and rising expectations for performance, reliability, and cybersecurity. Enterprises are increasingly integrating testing solutions into their DevOps pipelines to maintain seamless operations and superior customer experiences while ensuring compliance with evolving industry regulations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $55.8 Billion |

| Forecast Value | $112.5 Billion |

| CAGR | 7.2% |

Software testing solutions, including automated testing platforms, performance and load testing systems, security validation frameworks, and AI-driven test management tools, are essential for maintaining software integrity. These solutions enable real-time monitoring, accurate defect detection, and comprehensive application validation while minimizing manual intervention. They ensure seamless coordination between testing teams, cloud infrastructures, and DevOps environments, supporting broader enterprise digitalization strategies. The market is being shaped by AI-powered automation, cloud adoption, modernization of IT infrastructure, and growing regulatory requirements for quality and security.

The application testing segment held a 54% share in 2024 and is expected to grow at a CAGR of 10.1% from 2025 to 2034. Its dominance stems from its critical role in ensuring software functionality, performance, security, and reliability across web, mobile, and enterprise platforms. This segment covers functional testing, performance evaluation, security validation, and user experience assessment, which are essential for software vendors, IT service providers, and enterprises to deliver high-quality applications.

The B2B segment held 87% share in 2024 and is projected to grow at a CAGR of 7.4% through 2034. This leadership is driven by enterprises' growing need for secure, high-performance, and dependable software across sectors such as finance, healthcare, manufacturing, and IT services. Companies are investing in comprehensive testing solutions to ensure compliance, seamless integration, and operational efficiency while enhancing end-user satisfaction.

U.S. Software Testing Market held an 88% share, generating USD 23.3 billion in 2024. The U.S. represents a major opportunity due to its high volume of enterprise IT deployments, rapid adoption of cloud-native and mobile applications, and strict regulatory standards for cybersecurity, data privacy, and industry compliance. The country's mature IT ecosystem enables the swift implementation of AI-driven test management systems, CI/CD pipelines, and next-generation testing solutions.

Key players operating in the Global Software Testing Market include Tricentis, IBM, Cognizant, Wipro, EPAM Systems, SmartBear Software, Capgemini, TCS, Accenture, and NTT Data. Companies in the Software Testing Market are employing multiple strategies to expand their market presence and strengthen their position. They are investing heavily in AI-driven test automation and cloud-based platforms to provide scalable, cost-efficient, and intelligent testing solutions. Firms are focusing on partnerships, mergers, and acquisitions to broaden their service offerings and global reach. Product innovation and R&D initiatives allow them to deliver cutting-edge solutions that address evolving enterprise needs. Many companies emphasize end-to-end service integration, including DevOps alignment, CI/CD support, and security compliance. Strategic marketing, thought leadership, and industry-specific solutions help differentiate brands and attract high-value enterprise clients, boosting competitiveness and long-term growth in the software testing market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Business model

- 2.2.4 Platform

- 2.2.5 Deployment model

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of agile and devops

- 3.2.1.2 Growing demand for high-quality software

- 3.2.1.3 Technological advancements in test automation

- 3.2.1.4 Regulatory and compliance requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment

- 3.2.2.2 Complex integration with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 Rapidly evolving technology landscape

- 3.2.3.2 Data security and privacy concerns

- 3.2.3.3 Ai-driven and predictive testing solutions

- 3.2.3.4 Cloud-based and hybrid testing services

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 Global regulatory landscape overview

- 3.4.2 Industry-specific compliance requirements

- 3.4.3 Data privacy & protection regulations

- 3.4.4 Cybersecurity standards & frameworks

- 3.4.5 Professional certification requirements

- 3.4.6 Quality standards & accreditation

- 3.4.7 Cross-border regulatory harmonization

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation Landscape

- 3.7.1 AI & machine learning integration

- 3.7.2 Test automation evolution

- 3.7.3 Cloud-native testing platforms

- 3.7.4 Low-code/no-code testing solutions

- 3.7.5 Quantum computing test preparation

- 3.7.6 Blockchain testing requirements

- 3.7.7 IoT & edge computing testing

- 3.7.8 Augmented & virtual reality testing

- 3.7.9 5g network testing requirements

- 3.8 Price trends

- 3.8.1 Regional Pricing Variations

- 3.8.2 Pricing strategies by player segment

- 3.8.2.1 Service-Based Pricing Models

- 3.8.2.2 Value-Based Pricing Approach

- 3.8.2.3 Volume & Scale Economies

- 3.9 Cost breakdown analysis

- 3.10 Patent analysis

- 3.11 Sustainability and Environmental Aspects

- 3.11.1 Sustainable practices

- 3.11.2 Waste reduction strategies

- 3.11.3 Energy efficiency in production

- 3.11.4 Eco-friendly initiatives

- 3.11.5 Carbon footprint considerations

- 3.12 Risk assessment framework

- 3.13 Best case scenarios

- 3.14 Client Requirements & Selection Criteria Analysis

- 3.14.1 Enterprise client testing requirements

- 3.14.2 SME testing needs & budget constraints

- 3.14.3 Vendor selection decision factors

- 3.14.4 Roi expectations & measurement frameworks

- 3.14.5 Service level agreement requirements

- 3.14.6 Security & compliance mandates

- 3.14.7 Integration & interoperability needs

- 3.14.8 Scalability & flexibility requirements

- 3.15 Industry-Specific Testing Requirements

- 3.15.1 Compliance testing (PCI-DSS, HIPAA, GDPR implications)

- 3.15.2 Domain-specific complexities (fintech, healthcare, autonomous vehicles)

- 3.15.3 Regulatory audit readiness

- 3.15.4 Industry benchmarks and best practices

- 3.16 Quality Metrics & Analytics Framework

- 3.16.1 KPIs for testing effectiveness (defect escape rate, test ROI, cycle time)

- 3.16.2 Data-driven quality insights

- 3.16.3 Real-time monitoring and dashboards

- 3.16.4 Predictive quality analytics

- 3.16.5 Benchmarking against industry standards

- 3.17 Customer Success & Retention Metrics

- 3.17.1 Post-implementation support requirements

- 3.17.2 Client satisfaction trends

- 3.17.3 Churn analysis and loyalty factors

- 3.17.4 Value realization timelines

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 Middle East & Africa

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

- 4.7 Competitive Vulnerabilities & Threats

- 4.7.1 Performance gaps in key areas

- 4.7.2 Technology debt and legacy platform issues

- 4.7.3 Customer churn indicators and at-risk segments

- 4.7.4 Emerging threats from new entrants or adjacent players

- 4.7.5 Underserved market segments

- 4.8 Customer Win/Loss Analysis

- 4.8.1 Deal sizes and contract values by competitor

- 4.8.2 Win rates against specific competitors

- 4.8.3 Key differentiators in competitive deals

- 4.8.4 Customer migration patterns (switching behavior)

- 4.8.5 Market share gains/losses by segment

- 4.9 Technology Stack & Platform Capabilities Matrix

- 4.9.1 AI/ML capabilities comparison across major players

- 4.9.2 Cloud infrastructure preferences and investments

- 4.9.3 Test automation coverage and depth

- 4.9.4 Integration ecosystem breadth (DevOps, monitoring, security tools)

- 4.9.5 Proprietary vs. open-source approach

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($ Bn)

- 5.1 Key trends

- 5.2 Application Testing

- 5.2.1 Functional

- 5.2.1.1 System testing

- 5.2.1.2 Unit testing

- 5.2.1.3 Integration testing

- 5.2.1.4 Smoke Testing

- 5.2.1.5 Regression Testing

- 5.2.1.6 Others

- 5.2.2 Non-Functional

- 5.2.2.1 Security testing

- 5.2.2.2 Performance testing

- 5.2.2.3 Usability testing

- 5.2.2.4 Others

- 5.2.1 Functional

- 5.3 Testing Services

- 5.3.1 Professional services

- 5.3.2 Managed services

Chapter 6 Market Estimates & Forecast, By Business Model, 2021 - 2034 ($ Bn)

- 6.1 Key trends

- 6.2 B2B

- 6.2.1 Enterprise application testing

- 6.2.2 B2B platform testing

- 6.2.3 Integration testing services

- 6.2.4 API testing solutions

- 6.3 B2C

- 6.3.1 Consumer application testing

- 6.3.2 User experience testing

- 6.3.3 Mobile app testing

- 6.3.4 E-commerce testing

Chapter 7 Market Estimates & Forecast, By Platform, 2021 - 2034 ($ Bn)

- 7.1 Key trends

- 7.2 Mobile

- 7.2.1 Native mobile app testing

- 7.2.2 Cross-platform mobile testing

- 7.2.3 Mobile device testing

- 7.2.4 Mobile performance testing

- 7.2.5 Mobile security testing

- 7.3 Web-based Testing

- 7.3.1 Web application testing

- 7.3.2 Browser compatibility testing

- 7.3.3 Web performance testing

- 7.3.4 Web security testing

- 7.3.5 Progressive web app testing

Chapter 8 Market Estimates & Forecast, By Deployment Model, 2021 - 2034 ($ Bn)

- 8.1 Key trends

- 8.2 Cloud-based Testing Solutions

- 8.2.1 Software-as-a-Service (SaaS) testing platforms

- 8.2.2 Platform-as-a-Service (PaaS) testing tools

- 8.2.3 Infrastructure-as-a-Service (IaaS) testing

- 8.2.4 Multi-cloud testing strategies

- 8.3 On-premises Testing Solutions

- 8.3.1 Traditional testing infrastructure

- 8.3.2 Enterprise testing platforms

- 8.3.3 Dedicated testing centers

- 8.4 Hybrid Testing Solutions

- 8.4.1 Cloud-on-premises integration

- 8.4.2 Flexible deployment models

- 8.4.3 Hybrid testing orchestration

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($ Bn)

- 9.1 Key trends

- 9.2 IT

- 9.3 Telecom

- 9.4 BFSI

- 9.5 Manufacturing

- 9.6 Retail

- 9.7 Healthcare

- 9.8 Transportation & Logistics

- 9.9 Government & Public sector

- 9.10 Consumer electronics

- 9.11 Media

- 9.12 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($ Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Belgium

- 10.3.7 Netherlands

- 10.3.8 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 Singapore

- 10.4.6 South Korea

- 10.4.7 Vietnam

- 10.4.8 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Global Player

- 11.1.1 Accenture

- 11.1.2 Atos

- 11.1.3 Capgemini

- 11.1.4 Cognizant Technology Solutions

- 11.1.5 IBM

- 11.1.6 Infosys

- 11.1.7 NTT Data

- 11.1.8 Tata Consultancy Services (TCS)

- 11.1.9 Wipro

- 11.2 Regional Player

- 11.2.1 EPAM Systems

- 11.2.2 Keysight Technologies

- 11.2.3 Micro Focus International

- 11.2.4 Parasoft

- 11.2.5 Ranorex

- 11.2.6 SmartBear Software

- 11.2.7 Tech Mahindra

- 11.2.8 Tricentis

- 11.2.9 Worksoft

- 11.3 Emerging Players

- 11.3.1 Applitools

- 11.3.2 Katalon

- 11.3.3 Mabl

- 11.3.4 Sauce Labs

- 11.3.5 Testim

2026年全球人工智慧(AI)测试市场报告

2026年全球人工智慧(AI)测试市场报告 2026-2030年全球软体测试服务市场

2026-2030年全球软体测试服务市场 全球服务虚拟化市场规模、份额、趋势和成长分析报告(2026-2034)

全球服务虚拟化市场规模、份额、趋势和成长分析报告(2026-2034) 人工智慧赋能测试市场-全球产业规模、份额、趋势、机会和预测:按组件、部署、最终用户产业、应用、技术、地区和竞争格局划分,2021-2031年人工智慧驱动测试市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034 年)服务虚拟化市场 - 全球产业规模、份额、趋势、机会、预测:按组件、部署、产业、地区和竞争格局划分,2021-2031 年

人工智慧赋能测试市场-全球产业规模、份额、趋势、机会和预测:按组件、部署、最终用户产业、应用、技术、地区和竞争格局划分,2021-2031年人工智慧驱动测试市场规模、占有率、成长及全球产业分析:依类型、应用和地区划分的洞察与预测(2026-2034 年)服务虚拟化市场 - 全球产业规模、份额、趋势、机会、预测:按组件、部署、产业、地区和竞争格局划分,2021-2031 年 企业软体测试服务市场按服务类型、测试等级、部署类型、服务模式和组织规模划分,全球预测(2026-2032年)单迴路PID温度控制器市场(依控制器类型、安装类型、销售管道及最终用户产业划分)-2026-2032年全球预测商业智慧(BI) 测试市场按产品类型、技术、最终用户、分销管道和应用划分-2026 年至 2032 年全球预测

企业软体测试服务市场按服务类型、测试等级、部署类型、服务模式和组织规模划分,全球预测(2026-2032年)单迴路PID温度控制器市场(依控制器类型、安装类型、销售管道及最终用户产业划分)-2026-2032年全球预测商业智慧(BI) 测试市场按产品类型、技术、最终用户、分销管道和应用划分-2026 年至 2032 年全球预测 纯软体测试服务市场规模、份额和成长分析(按测试类型、组织规模、部署模式和地区划分)-2026-2033年产业预测

纯软体测试服务市场规模、份额和成长分析(按测试类型、组织规模、部署模式和地区划分)-2026-2033年产业预测